Key Insights

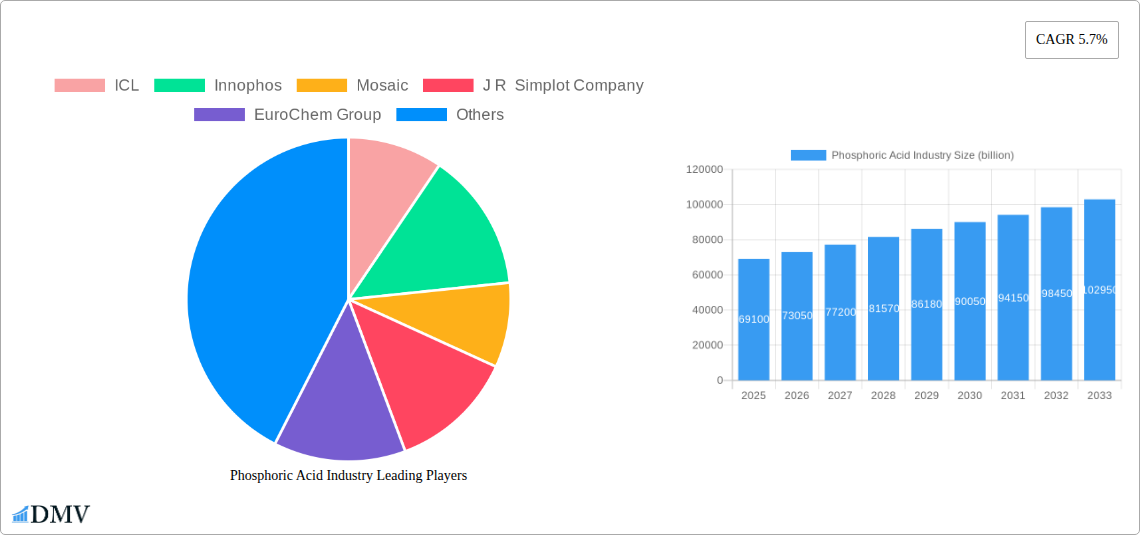

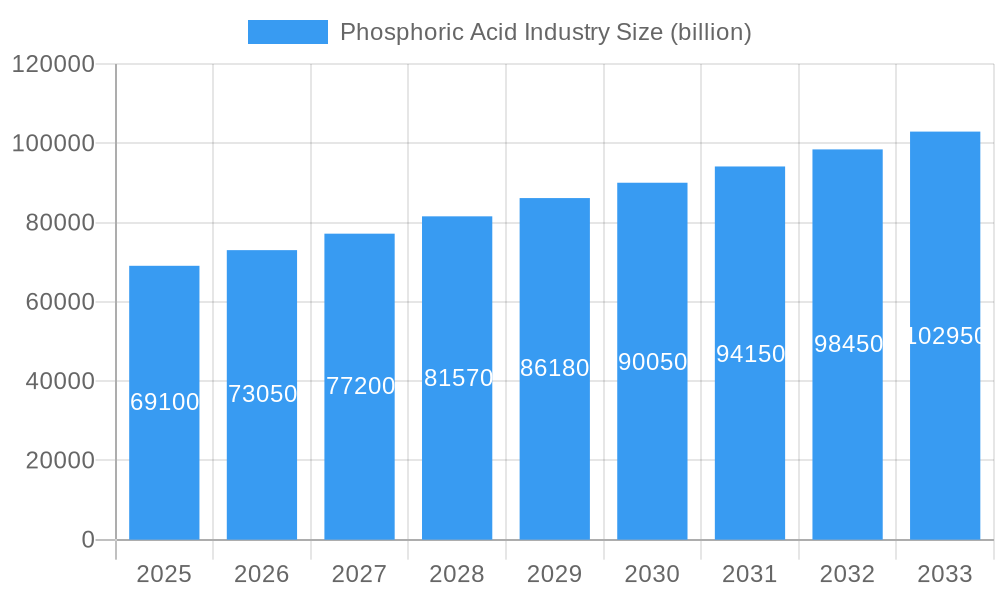

The global Phosphoric Acid Industry is poised for significant expansion, projected to reach a market size of $69.1 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 5.7% anticipated over the forecast period of 2025-2033. This robust growth is primarily fueled by the escalating demand from the fertilizer sector, driven by the global need for enhanced food security and agricultural productivity. The food and beverage industry also presents a substantial avenue for growth, utilizing phosphoric acid as an acidulant and flavoring agent. Furthermore, its critical applications in medicine for pharmaceuticals and its role in metallurgy for metal treatment and rust removal contribute to sustained market momentum. Emerging economies, particularly in the Asia Pacific region, are expected to be key drivers of this growth due to rapid industrialization and increasing agricultural output. The industry is also witnessing a trend towards the development of higher-purity phosphoric acid for specialized applications, alongside a growing emphasis on sustainable production methods and waste management in its manufacturing processes.

Phosphoric Acid Industry Market Size (In Billion)

Despite the strong growth trajectory, the Phosphoric Acid Industry faces certain restraints. Fluctuations in the prices of raw materials, particularly phosphate rock, can impact profit margins and market stability. Stringent environmental regulations concerning the production and disposal of phosphogypsum, a byproduct of phosphoric acid manufacturing, also pose a challenge, necessitating investment in advanced waste treatment technologies. Geopolitical factors influencing the supply chain of phosphate rock can also create volatility. However, ongoing research and development into more efficient extraction and purification techniques, coupled with the exploration of alternative raw material sources, are expected to mitigate these challenges. The increasing adoption of innovative production processes and a focus on product diversification across various end-user industries will further solidify the market's positive outlook.

Phosphoric Acid Industry Company Market Share

Sure, here is the SEO-optimized and insightful report description for the Phosphoric Acid Industry:

Phosphoric Acid Industry Market Composition & Trends

The global phosphoric acid market is characterized by a moderately consolidated landscape, with key players like Mosaic, Nutrien Ltd, and PhosAgro holding substantial market share. Innovation is driven by the demand for high-purity phosphoric acid in food and beverage applications and the development of sustainable production methods to meet stringent environmental regulations. The regulatory environment, particularly concerning fertilizer production and industrial waste management, significantly influences market dynamics. Substitute products, such as organic fertilizers and alternative acids in certain industrial processes, present a competitive challenge, though phosphoric acid's unique properties and broad applicability, especially in agriculture, maintain its dominance. The end-user profiles reveal a strong reliance on the fertilizer segment, followed by food and beverages, chemicals, and medicine. Mergers and acquisitions (M&A) are active, with significant deal values shaping the competitive landscape and expanding market reach. For instance, strategic acquisitions in the animal nutrition sector by OCP Group and expansion of retail networks by Nutrien Ltd underscore the trend of vertical integration and market consolidation. Market share distribution indicates a concentration among a few major producers, with ongoing efforts to expand production capacity and diversify product portfolios.

Phosphoric Acid Industry Industry Evolution

The phosphoric acid industry has undergone a dynamic evolution, marked by consistent market growth trajectories fueled by the indispensable role of phosphoric acid in global food security and industrial manufacturing. The historical period from 2019 to 2024 witnessed steady demand, primarily driven by the agricultural sector's reliance on phosphate-based fertilizers. The base year of 2025 represents a pivotal point, with the market poised for accelerated expansion throughout the forecast period extending to 2033. Technological advancements have played a crucial role in this evolution, from improvements in wet process phosphoric acid production efficiency to the development of higher-purity grades for specialized applications. Innovations in nutrient management and precision agriculture have indirectly boosted the demand for tailored fertilizer formulations, thereby increasing the need for high-quality phosphoric acid.

Consumer demand has also shifted, with a growing emphasis on food safety and quality driving the adoption of food-grade phosphoric acid in the beverage and processed food industries. This has led to an increased focus on purification technologies and stringent quality control measures. The medicine sector, while a smaller segment, shows consistent growth due to phosphoric acid's use in pharmaceuticals and dental applications.

The industry's growth rates have been robust, with projections indicating a Compound Annual Growth Rate (CAGR) of approximately 4.5% to 5.5% from 2025 to 2033. Adoption metrics for advanced production techniques and sustainable practices are on the rise as companies seek to optimize resource utilization and minimize environmental impact. The integration of digital technologies in supply chain management and production monitoring is also becoming more prevalent, enhancing operational efficiency and market responsiveness. The strategic importance of phosphate rock reserves and the geopolitical factors influencing their availability continue to shape the industry's development. The increasing global population and the resultant demand for agricultural output remain the overarching drivers of sustained market growth.

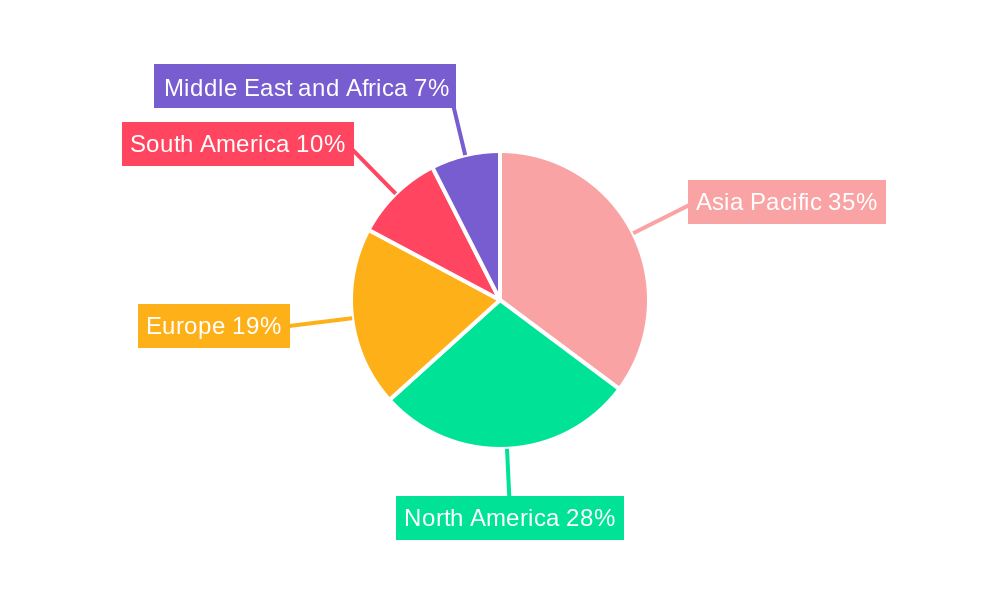

Leading Regions, Countries, or Segments in Phosphoric Acid Industry

The Fertilizer end-user industry stands as the undeniable dominant segment within the global phosphoric acid market. This dominance stems from the fundamental role of phosphoric acid as a key ingredient in the production of phosphate fertilizers, which are critical for enhancing crop yields and ensuring global food security.

- Dominance Factors in the Fertilizer Segment:

- Global Food Demand: A continuously growing global population necessitates increased agricultural output, directly translating to higher demand for phosphate fertilizers.

- Arable Land Limitations: With limited arable land expansion, maximizing yields from existing land through fertilization is paramount.

- Nutrient Essentiality: Phosphorus is an essential macronutrient for plant growth, making phosphoric acid-derived fertilizers indispensable.

- Investment Trends: Significant investments are consistently channeled into agricultural infrastructure and fertilizer production facilities, particularly in regions with large agricultural bases.

- Regulatory Support: Governments worldwide often implement policies supporting agricultural productivity, including subsidies for fertilizer use, further bolstering demand.

In-depth analysis reveals that regions with extensive agricultural economies, such as Asia-Pacific (particularly China and India), North America (USA), and South America (Brazil), are the largest consumers of phosphoric acid for fertilizer production. China, for instance, is a major producer and consumer of fertilizers, driven by its vast agricultural sector. India's increasing focus on food self-sufficiency also fuels substantial demand. Brazil's booming agricultural exports, especially soybeans, also contribute significantly to the demand for phosphate fertilizers.

While the Food and Beverages segment is crucial for high-purity phosphoric acid, its overall volume consumption is considerably lower than fertilizers. Similarly, the Chemicals, Medicine, and Other End-user Industries segments, although important, do not match the sheer scale of demand from agriculture. The strategic importance of phosphoric acid in the fertilizer value chain solidifies its position as the leading segment, driving market trends, investment decisions, and regional consumption patterns within the broader phosphoric acid industry.

Phosphoric Acid Industry Product Innovations

Product innovations in the phosphoric acid industry are increasingly focusing on enhancing purity and sustainability. Advancements in purification techniques are yielding ultra-high purity phosphoric acid, crucial for the semiconductor industry and specialized food applications, meeting stringent industry standards like FCC (Food Chemicals Codex). Furthermore, efforts are underway to develop greener production processes, including the utilization of industrial by-products and the reduction of waste streams, aligning with global sustainability goals. Innovations in controlled-release fertilizer formulations utilizing phosphoric acid derivatives are also gaining traction, offering improved nutrient delivery to crops and minimizing environmental runoff. These advancements aim to enhance product performance, reduce environmental impact, and open new market avenues.

Propelling Factors for Phosphoric Acid Industry Growth

The phosphoric acid industry's growth is primarily propelled by the escalating global demand for food, driven by a rising population that necessitates enhanced agricultural productivity through fertilizers. Technological advancements in fertilizer manufacturing, leading to more efficient and targeted nutrient delivery, further stimulate demand. Government initiatives promoting agricultural development and food security in developing nations also act as significant growth catalysts. The expanding use of phosphoric acid in food and beverage processing, as an acidulant and flavor enhancer, contributes to steady market expansion. Economic growth in emerging markets fuels industrial development, increasing the demand for phosphoric acid in various chemical applications. The ongoing M&A activities, like those seen with OCP Group and Nutrien Ltd, strategically consolidate market positions and expand distribution networks, thereby propelling overall industry growth.

Obstacles in the Phosphoric Acid Industry Market

Significant obstacles in the phosphoric acid industry include the volatility of raw material prices, particularly phosphate rock and sulfur, which directly impact production costs. Supply chain disruptions, exacerbated by geopolitical tensions and logistics challenges, can lead to shortages and price fluctuations. Stringent environmental regulations concerning emissions, wastewater discharge, and mining practices necessitate substantial investments in compliance, adding to operational expenses. The presence of substitute products in certain niche applications and the cyclical nature of the fertilizer market, influenced by weather patterns and crop prices, also pose market challenges. Furthermore, the capital-intensive nature of establishing new production facilities and the long lead times for project development can hinder rapid expansion to meet surging demand.

Future Opportunities in Phosphoric Acid Industry

Future opportunities in the phosphoric acid industry lie in the growing demand for specialty and food-grade phosphoric acid, driven by evolving consumer preferences and stringent quality standards. The development of sustainable and eco-friendly production technologies, including enhanced recycling of phosphorus from waste streams, presents a significant growth avenue. Emerging markets in Africa and Southeast Asia, with their rapidly expanding agricultural sectors and increasing food demand, offer substantial untapped potential. The increasing adoption of precision agriculture and advanced fertilizer formulations will also create new demand for customized phosphoric acid products. Furthermore, research into novel applications of phosphoric acid in areas like renewable energy storage and advanced materials could unlock entirely new market segments.

Major Players in the Phosphoric Acid Industry Ecosystem

- ICL

- Innophos

- Mosaic

- J R Simplot Company

- EuroChem Group

- Sterlite Copper (A Unit of Vedanta Limited)

- Agropolychim

- Aditya Birla Chemicals

- Phosagro

- IFFCO

- Nutrien Ltd

Key Developments in Phosphoric Acid Industry Industry

- May 2023: The OCP Group secured a 50% ownership share in GlobalFeed SL. This strategic acquisition enabled OCP to broaden its presence in the animal nutrition industry and enhance customers' accessibility to the company's phosphoric acid products.

- July 2022: Nutrien Ltd acquired Brazilian company Casa do Adubo SA (Casa do Adubo). This acquisition included the transaction of 39 retail stores and ten distribution centers, which allows Nutrien to expand its reach to customers and is expected to generate a sales revenue of USD 400 million.

- February 2022: EuroChem Group completed the acquisition of the Serra do Salitre phosphate project and took over the advanced-stage mine and plant in Minas Gerais. This complex comprises an open-pit phosphate mine with over 350 million metric tons (MMT) of reserves and a plant with a production capacity of 1 MMT of fertilizers per year.

Strategic Phosphoric Acid Industry Market Forecast

The strategic outlook for the phosphoric acid industry is exceptionally robust, underpinned by fundamental drivers of global food demand and industrial growth. The forecast period from 2025 to 2033 is expected to witness sustained expansion, fueled by investments in agricultural modernization, particularly in emerging economies. Innovations in fertilizer technology and the rising demand for high-purity phosphoric acid in food, beverage, and specialized chemical applications will further bolster market potential. Companies are strategically expanding production capacities and optimizing supply chains to meet this burgeoning demand. The industry's ability to adapt to environmental regulations and embrace sustainable practices will be crucial for unlocking long-term growth and capitalizing on new market opportunities in sectors such as animal nutrition and advanced materials.

Phosphoric Acid Industry Segmentation

-

1. End-user Industry

- 1.1. Fertilizer

- 1.2. Food and Beverages

- 1.3. Chemicals

- 1.4. Medicine

- 1.5. Metallurgy

- 1.6. Other End-user Industries

Phosphoric Acid Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Mexico

- 2.3. Canada

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Phosphoric Acid Industry Regional Market Share

Geographic Coverage of Phosphoric Acid Industry

Phosphoric Acid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 5.1.1. Fertilizer

- 5.1.2. Food and Beverages

- 5.1.3. Chemicals

- 5.1.4. Medicine

- 5.1.5. Metallurgy

- 5.1.6. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.2.2. North America

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6. Global Phosphoric Acid Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6.1.1. Fertilizer

- 6.1.2. Food and Beverages

- 6.1.3. Chemicals

- 6.1.4. Medicine

- 6.1.5. Metallurgy

- 6.1.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7. Asia Pacific Phosphoric Acid Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7.1.1. Fertilizer

- 7.1.2. Food and Beverages

- 7.1.3. Chemicals

- 7.1.4. Medicine

- 7.1.5. Metallurgy

- 7.1.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by End-user Industry

- 8. North America Phosphoric Acid Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End-user Industry

- 8.1.1. Fertilizer

- 8.1.2. Food and Beverages

- 8.1.3. Chemicals

- 8.1.4. Medicine

- 8.1.5. Metallurgy

- 8.1.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by End-user Industry

- 9. Europe Phosphoric Acid Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End-user Industry

- 9.1.1. Fertilizer

- 9.1.2. Food and Beverages

- 9.1.3. Chemicals

- 9.1.4. Medicine

- 9.1.5. Metallurgy

- 9.1.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by End-user Industry

- 10. South America Phosphoric Acid Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End-user Industry

- 10.1.1. Fertilizer

- 10.1.2. Food and Beverages

- 10.1.3. Chemicals

- 10.1.4. Medicine

- 10.1.5. Metallurgy

- 10.1.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by End-user Industry

- 11. Middle East and Africa Phosphoric Acid Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by End-user Industry

- 11.1.1. Fertilizer

- 11.1.2. Food and Beverages

- 11.1.3. Chemicals

- 11.1.4. Medicine

- 11.1.5. Metallurgy

- 11.1.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by End-user Industry

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ICL

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Innophos

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mosaic

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 J R Simplot Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 EuroChem Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sterlite Copper (A Unit of Vedanta Limited) *List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Agropolychim

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Aditya Birla Chemicals

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Phosagro

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 IFFCO

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nutrien Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 ICL

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Phosphoric Acid Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Phosphoric Acid Industry Volume Breakdown (Million, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Phosphoric Acid Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 4: Asia Pacific Phosphoric Acid Industry Volume (Million), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Phosphoric Acid Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Phosphoric Acid Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 7: Asia Pacific Phosphoric Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 8: Asia Pacific Phosphoric Acid Industry Volume (Million), by Country 2025 & 2033

- Figure 9: Asia Pacific Phosphoric Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Phosphoric Acid Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: North America Phosphoric Acid Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 12: North America Phosphoric Acid Industry Volume (Million), by End-user Industry 2025 & 2033

- Figure 13: North America Phosphoric Acid Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: North America Phosphoric Acid Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 15: North America Phosphoric Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Phosphoric Acid Industry Volume (Million), by Country 2025 & 2033

- Figure 17: North America Phosphoric Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Phosphoric Acid Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Phosphoric Acid Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 20: Europe Phosphoric Acid Industry Volume (Million), by End-user Industry 2025 & 2033

- Figure 21: Europe Phosphoric Acid Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: Europe Phosphoric Acid Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 23: Europe Phosphoric Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Phosphoric Acid Industry Volume (Million), by Country 2025 & 2033

- Figure 25: Europe Phosphoric Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Phosphoric Acid Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: South America Phosphoric Acid Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 28: South America Phosphoric Acid Industry Volume (Million), by End-user Industry 2025 & 2033

- Figure 29: South America Phosphoric Acid Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: South America Phosphoric Acid Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 31: South America Phosphoric Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: South America Phosphoric Acid Industry Volume (Million), by Country 2025 & 2033

- Figure 33: South America Phosphoric Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Phosphoric Acid Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Middle East and Africa Phosphoric Acid Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 36: Middle East and Africa Phosphoric Acid Industry Volume (Million), by End-user Industry 2025 & 2033

- Figure 37: Middle East and Africa Phosphoric Acid Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 38: Middle East and Africa Phosphoric Acid Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 39: Middle East and Africa Phosphoric Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 40: Middle East and Africa Phosphoric Acid Industry Volume (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Phosphoric Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Phosphoric Acid Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Phosphoric Acid Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 2: Global Phosphoric Acid Industry Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Phosphoric Acid Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Phosphoric Acid Industry Volume Million Forecast, by Region 2020 & 2033

- Table 5: Global Phosphoric Acid Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Phosphoric Acid Industry Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 7: Global Phosphoric Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Phosphoric Acid Industry Volume Million Forecast, by Country 2020 & 2033

- Table 9: China Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: China Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 11: India Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: India Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 13: Japan Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Japan Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 15: South Korea Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: South Korea Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Asia Pacific Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Asia Pacific Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Phosphoric Acid Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Phosphoric Acid Industry Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 21: Global Phosphoric Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Global Phosphoric Acid Industry Volume Million Forecast, by Country 2020 & 2033

- Table 23: United States Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: United States Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 25: Mexico Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Mexico Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 27: Canada Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Canada Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 29: Global Phosphoric Acid Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 30: Global Phosphoric Acid Industry Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 31: Global Phosphoric Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Global Phosphoric Acid Industry Volume Million Forecast, by Country 2020 & 2033

- Table 33: Germany Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Germany Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 35: United Kingdom Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: United Kingdom Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 37: Italy Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 39: France Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: France Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 43: Global Phosphoric Acid Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 44: Global Phosphoric Acid Industry Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 45: Global Phosphoric Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Global Phosphoric Acid Industry Volume Million Forecast, by Country 2020 & 2033

- Table 47: Brazil Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Brazil Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 49: Argentina Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Argentina Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 51: Rest of South America Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of South America Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 53: Global Phosphoric Acid Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 54: Global Phosphoric Acid Industry Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 55: Global Phosphoric Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 56: Global Phosphoric Acid Industry Volume Million Forecast, by Country 2020 & 2033

- Table 57: Saudi Arabia Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Saudi Arabia Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 59: South Africa Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South Africa Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

- Table 61: Rest of Middle East and Africa Phosphoric Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Middle East and Africa Phosphoric Acid Industry Volume (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Phosphoric Acid Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Phosphoric Acid Industry?

Key companies in the market include ICL, Innophos, Mosaic, J R Simplot Company, EuroChem Group, Sterlite Copper (A Unit of Vedanta Limited) *List Not Exhaustive, Agropolychim, Aditya Birla Chemicals, Phosagro, IFFCO, Nutrien Ltd.

3. What are the main segments of the Phosphoric Acid Industry?

The market segments include End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 69.1 billion as of 2022.

5. What are some drivers contributing to market growth?

High Demand for Fertilizer Industry; Increasing Usage in the Food and Beverage Industry.

6. What are the notable trends driving market growth?

Fertilizer Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

Health Hazards Caused by Phosphoric Acid.

8. Can you provide examples of recent developments in the market?

May 2023: The OCP Group secured a 50% ownership share in GlobalFeed SL. This strategic acquisition enabled OCP to broaden its presence in the animal nutrition industry and enhance customers' accessibility to the company's phosphoric acid products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Phosphoric Acid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Phosphoric Acid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Phosphoric Acid Industry?

To stay informed about further developments, trends, and reports in the Phosphoric Acid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence