Key Insights

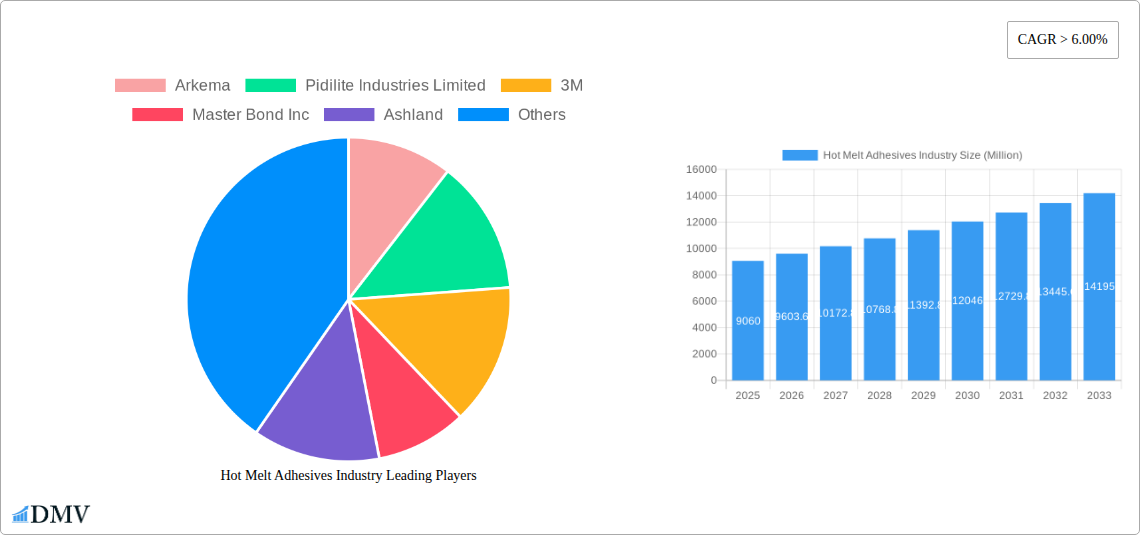

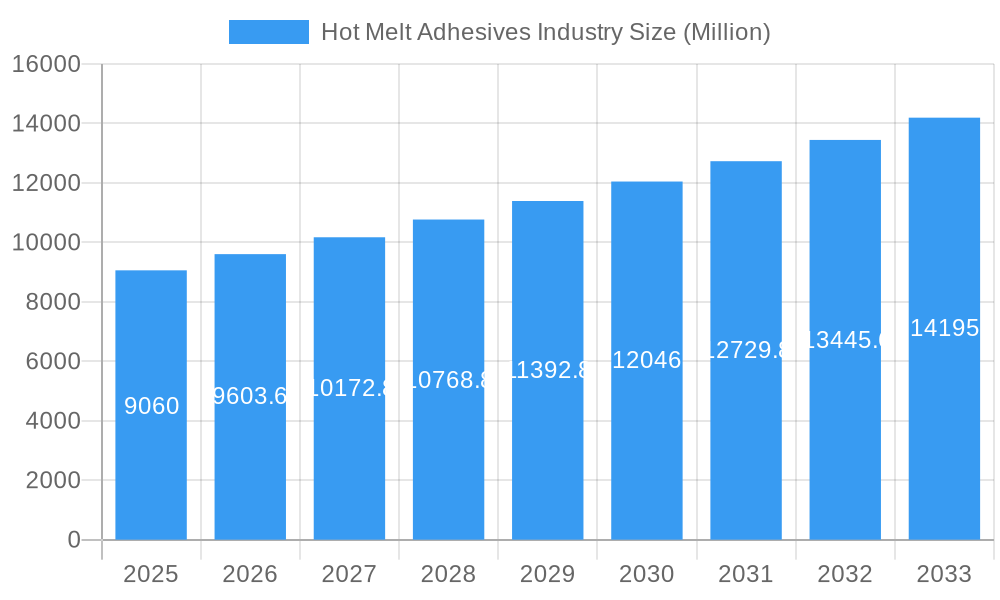

The global Hot Melt Adhesives market is poised for significant expansion, currently valued at USD 9,060 Million in 2025 and projected to grow at a robust Compound Annual Growth Rate (CAGR) exceeding 6.00% over the forecast period from 2025 to 2033. This upward trajectory is fueled by a confluence of factors, most notably the escalating demand from the building and construction sector, driven by urbanization and infrastructure development worldwide. The paper, board, and packaging industry also presents a substantial growth engine, with an increasing emphasis on sustainable packaging solutions and efficient assembly processes. Furthermore, the automotive industry's continuous innovation in lightweighting and interior component assembly contributes to the uptake of hot melt adhesives due to their fast setting times and strong bonding capabilities. Emerging economies, particularly in the Asia Pacific region, are becoming key consumption hubs, owing to rapid industrialization and a growing manufacturing base.

Hot Melt Adhesives Industry Market Size (In Billion)

The market's dynamism is further shaped by advancements in resin technologies, with Ethylene Vinyl Acetate (EVA) and Styrenic Block Copolymers (SBCs) dominating the landscape due to their versatility and cost-effectiveness. Thermoplastic Polyurethane (TPU) adhesives are gaining traction in applications demanding higher performance, such as in the automotive and footwear industries. While the market exhibits strong growth potential, certain restraints, such as fluctuating raw material prices and the emergence of alternative bonding technologies in specific niche applications, warrant strategic attention from market players. Nevertheless, the overarching trends of sustainability, increased automation in manufacturing processes, and the demand for high-performance bonding solutions are expected to propel the hot melt adhesives market to new heights, creating lucrative opportunities for established and emerging companies alike.

Hot Melt Adhesives Industry Company Market Share

Hot Melt Adhesives Industry Market Composition & Trends

The global Hot Melt Adhesives market is characterized by a moderate to high market concentration, with key players like Arkema, Pidilite Industries Limited, 3M, and H.B. Fuller Company holding significant market share. Innovation catalysts are primarily driven by the demand for sustainable and eco-friendly adhesive solutions, pushing for advancements in bio-based and recyclable formulations. The regulatory landscape is increasingly influenced by environmental concerns, impacting the use of certain chemicals and promoting the development of compliant alternatives. Substitute products, such as water-based adhesives and solvent-based adhesives, present competition, but hot melts offer distinct advantages in terms of fast setting times, high bond strength, and versatility across diverse applications. End-user profiles range from large-scale manufacturers in the paper, board, and packaging, and building and construction sectors, to niche applications in automotive, woodworking, and healthcare. Mergers and acquisitions (M&A) activities are a notable trend, with an estimated M&A deal value of over $2,000 Million in the historical period, indicating consolidation and strategic expansion within the industry. The market share distribution sees Paper, Board, and Packaging as the largest segment, followed by Building and Construction.

- Market Concentration: Moderate to High

- Key Innovation Drivers: Sustainability, recyclability, enhanced performance

- Regulatory Landscape: Growing emphasis on environmental compliance

- Substitute Products: Water-based adhesives, solvent-based adhesives

- Dominant End-user Industries: Paper, Board, and Packaging; Building and Construction

- M&A Deal Value (Historical): > $2,000 Million

Hot Melt Adhesives Industry Industry Evolution

The Hot Melt Adhesives industry has witnessed a robust growth trajectory over the historical period, driven by a confluence of technological advancements, shifting consumer demands, and the expansion of key end-user industries. Between 2019 and 2024, the market has experienced a compound annual growth rate (CAGR) of approximately 5.5%, translating into a market valuation that grew from an estimated $30,000 Million in 2019 to over $40,000 Million by the end of 2024. This consistent expansion is a testament to the inherent advantages of hot melt adhesives, including their rapid setting times, solvent-free formulations, and strong bonding capabilities across a wide spectrum of substrates.

Technological advancements have been a significant catalyst for this evolution. The development of new polymer formulations, such as advanced Styrenic Block Copolymers and Thermoplastic Polyurethanes (TPUs), has unlocked new application possibilities and improved adhesive performance. For instance, advancements in EVA (Ethylene Vinyl Acetate) based hot melts have led to enhanced flexibility and temperature resistance, making them ideal for demanding packaging applications. Similarly, the introduction of reactive hot melts has provided superior bond strength and durability for challenging industrial uses.

Shifting consumer demands have also played a crucial role. The increasing consumer awareness regarding environmental impact has spurred the development of eco-friendly hot melt adhesives. Manufacturers are actively investing in research and development to create adhesives with lower VOC emissions, increased recyclability, and the use of bio-based raw materials. This trend is particularly evident in the packaging sector, where brand owners are seeking sustainable solutions to meet regulatory requirements and consumer preferences. The Paper, Board, and Packaging segment, a dominant force in the market, has seen a surge in demand for hot melts that facilitate easier recycling and reduce the environmental footprint of products.

Furthermore, the growth of key end-user industries has directly fueled the demand for hot melt adhesives. The Building and Construction sector, for example, utilizes hot melts in applications like flooring installation, insulation bonding, and window sealing, all of which have experienced steady growth due to global urbanization and infrastructure development. The automotive industry's increasing reliance on lightweight materials and advanced assembly techniques also presents a significant avenue for hot melt adhesive penetration, particularly in interior trim and component bonding. The Automotive and Transportation segment is projected to contribute significantly to market growth in the forecast period.

The Electrical and Electronic Appliances sector, driven by the miniaturization of devices and the need for efficient assembly processes, also represents a growing market for specialized hot melt adhesives that offer thermal management and electrical insulation properties. The adoption metrics for hot melts in these sectors are continuously rising, with an estimated increase in application volume by over 15% across all major industries from 2019 to 2024. The historical period, therefore, has been a phase of significant innovation and market expansion, setting a strong foundation for future growth.

Leading Regions, Countries, or Segments in Hot Melt Adhesives Industry

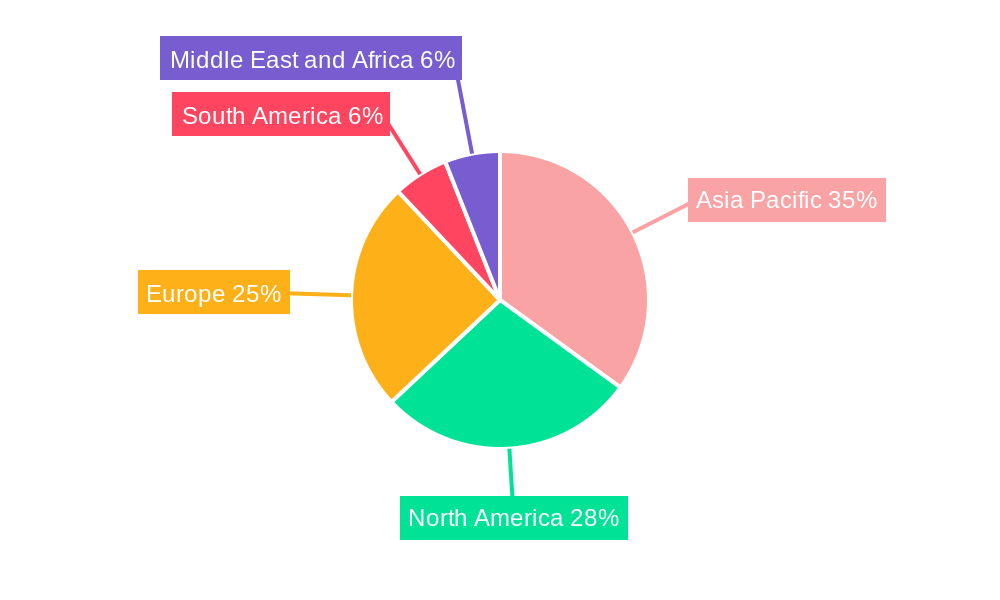

The global Hot Melt Adhesives market is segmented across various geographies and end-user industries, with certain regions and segments demonstrating exceptional dominance. Among the Resin Types, Ethylene Vinyl Acetate (EVA) continues to be a leading segment due to its cost-effectiveness and versatility, finding extensive use in packaging and woodworking. However, Styrenic Block Copolymers (SBCs) are rapidly gaining traction, particularly in applications requiring higher elasticity and adhesion to a wider range of substrates, including Automotive and Transportation and Footwear and Leather industries. Thermoplastic Polyurethanes (TPUs), known for their superior thermal resistance and durability, are carving out a significant niche in demanding applications like Building and Construction and specialized industrial assembly.

In terms of End-user Industries, the Paper, Board, and Packaging segment stands as the undisputed leader, accounting for an estimated 35% of the global market share. This dominance is fueled by the continuous demand for efficient and reliable bonding solutions for corrugated boxes, flexible packaging, labels, and bookbinding. The increasing global e-commerce penetration further amplifies this demand. Following closely is the Building and Construction segment, representing approximately 20% of the market share. Hot melt adhesives are integral to various construction applications, including flooring installation, insulation bonding, panel lamination, and window and door sealing, driven by global infrastructure development and urbanization trends.

Geographically, Asia Pacific is the leading region, driven by its robust manufacturing base, rapid industrialization, and burgeoning consumer markets. Countries like China, India, and Southeast Asian nations are significant consumers of hot melt adhesives, particularly in the Paper, Board, and Packaging and Automotive and Transportation sectors. North America and Europe are also mature and substantial markets, characterized by a strong focus on innovation, sustainability, and high-performance applications, especially within the Automotive and Transportation, Healthcare, and Electrical and Electronic Appliances industries.

Key drivers for the dominance of these segments and regions include:

- Investment Trends: Significant investments in manufacturing infrastructure and R&D by major players in Asia Pacific and established markets like North America and Europe.

- Regulatory Support: Favorable regulations promoting the use of solvent-free adhesives and sustainable packaging solutions are bolstering demand in key regions.

- Urbanization and Infrastructure Development: Driving demand in the Building and Construction sector globally, with a strong focus on emerging economies.

- Growth of E-commerce: Directly impacting the Paper, Board, and Packaging segment, necessitating efficient and reliable packaging solutions.

- Technological Advancements: Continuous innovation in resin types and formulations catering to evolving industry needs, particularly in high-performance applications like Automotive and Transportation and Electrical and Electronic Appliances.

The Woodworking and Joinery segment, while smaller, exhibits consistent growth due to the demand for furniture and cabinetry. The Healthcare sector is also an emerging growth area, utilizing specialized hot melts for medical device assembly and wound care products, driven by an aging global population and advancements in healthcare technology. The Other End-user Industries, encompassing textiles, graphic arts, and consumer goods, collectively contribute to the diverse application landscape of hot melt adhesives.

Hot Melt Adhesives Industry Product Innovations

Product innovation in the Hot Melt Adhesives industry is primarily focused on enhancing sustainability, improving application efficiency, and expanding performance capabilities. Recent advancements include the development of bio-based hot melts derived from renewable resources, offering a reduced carbon footprint. Innovations in formulation have also led to hot melts with improved thermal stability, allowing for higher processing temperatures and stronger bonds in demanding environments. Furthermore, the industry is seeing the introduction of adhesives with tailored rheology, enabling better penetration into porous substrates and faster tack development for high-speed automated assembly lines. For instance, novel formulations are emerging that offer enhanced adhesion to difficult-to-bond substrates like polyolefins and recycled plastics, aligning with circular economy initiatives. These product innovations are directly addressing the evolving needs of industries seeking performance, sustainability, and cost-effectiveness.

Propelling Factors for Hot Melt Adhesives Industry Growth

The growth of the Hot Melt Adhesives industry is propelled by several key factors. Technologically, the constant development of new polymer chemistries and formulations, such as Ethylene Vinyl Acetate, Styrenic Block Copolymers, and Thermoplastic Polyurethanes, enables a wider range of applications with improved performance characteristics like faster setting times and enhanced bond strength. Economically, the expanding global Paper, Board, and Packaging industry, driven by e-commerce and rising consumer goods consumption, is a significant demand generator. Furthermore, the growth in Building and Construction and Automotive and Transportation sectors worldwide, coupled with an increasing preference for solvent-free and fast-curing adhesives, contributes substantially to market expansion. Regulatory push towards sustainable and eco-friendly solutions also indirectly fuels innovation and demand for compliant hot melt adhesives.

Obstacles in the Hot Melt Adhesives Industry Market

Despite its strong growth, the Hot Melt Adhesives industry faces several obstacles. Regulatory challenges related to volatile organic compound (VOC) emissions and the use of certain raw materials can increase compliance costs and necessitate reformulation efforts. Supply chain disruptions, as experienced in recent years, can lead to price volatility and availability issues for key raw materials, impacting production schedules and profitability. Intense competitive pressures from established players and emerging manufacturers, particularly in price-sensitive markets, can limit profit margins. Furthermore, the high initial investment cost for specialized application equipment can be a barrier for smaller enterprises looking to adopt hot melt technologies. The presence of established substitute products, like water-based and solvent-based adhesives, also presents ongoing competition.

Future Opportunities in Hot Melt Adhesives Industry

The Hot Melt Adhesives industry is poised for significant future opportunities. The growing global emphasis on sustainability and circular economy principles presents a major avenue for the development and adoption of bio-based, compostable, and easily recyclable hot melt adhesives. Emerging markets in Asia Pacific and Latin America, with their rapidly expanding manufacturing sectors and growing middle class, offer substantial untapped potential. Advancements in reactive hot melt technologies are opening doors for new applications in high-performance sectors like aerospace and advanced manufacturing. The increasing demand for lightweighting solutions in the Automotive and Transportation industry and the miniaturization trends in Electrical and Electronic Appliances also present promising opportunities for specialized hot melt formulations.

Major Players in the Hot Melt Adhesives Industry Ecosystem

- Arkema

- Pidilite Industries Limited

- 3M

- Master Bond Inc

- Ashland

- Huntsman International LLC

- Paramelt RMC B V

- Beardow Adams

- Dow

- H B Fuller Company

- Alfa International

- Sika AG

- Franklin International

- Henkel Corporation

- Hexcel Corporation

- Jowat SE

- AVERY DENNISON CORPORATION

- Mactac

- DRYTAC

Key Developments in Hot Melt Adhesives Industry Industry

- April 2023: Avery Dennison and Dow collaborated to develop an innovative and sustainable new hot melt label adhesive solution. This enables polyolefin film labels and polypropylene (PP) or polyethylene (PE) packaging to be mechanically recycled together in one stream. It is based on AFFINITY™ GA Polymers from Dow and sold by Avery Dennison under the name CF3050 in the Europe, Middle East, and North Africa (EMENA) region.

- June 2022: Henkel expanded its hot melt adhesives manufacturing facilities by opening a plant in Nuevo Leon, Mexico.

Strategic Hot Melt Adhesives Industry Market Forecast

The strategic forecast for the Hot Melt Adhesives market is characterized by sustained and robust growth, projected to achieve a market valuation exceeding $70,000 Million by 2033. This expansion will be primarily driven by the escalating demand for sustainable and high-performance adhesive solutions across key end-user industries. The Paper, Board, and Packaging segment will continue its dominance, propelled by e-commerce growth and increasing consumer packaged goods demand. Simultaneously, the Building and Construction and Automotive and Transportation sectors are anticipated to exhibit significant growth, fueled by global infrastructure development and advancements in vehicle manufacturing. Innovations in bio-based and recyclable hot melts will be critical catalysts, aligning with stringent environmental regulations and growing consumer preference for eco-friendly products. The increasing adoption of advanced technologies like reactive hot melts in specialized applications will further diversify the market and unlock new growth avenues, ensuring a dynamic and evolving landscape for hot melt adhesives.

Hot Melt Adhesives Industry Segmentation

-

1. Resin Type

- 1.1. Ethylene Vinyl Acetate

- 1.2. Styrenic Block Co-polymers

- 1.3. Thermoplastic Polyurethane

- 1.4. Other Resin Types (Polyolefin, polyamide)

-

2. End-user Industry

- 2.1. Building and Construction

- 2.2. Paper, Board, and Packaging

- 2.3. Woodworking and Joinery

- 2.4. Automotive and Transportation

- 2.5. Footwear and Leather

- 2.6. Healthcare

- 2.7. Electrical and Electronic Appliances

- 2.8. Other End-user Industries

Hot Melt Adhesives Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Malaysia

- 1.6. Thailand

- 1.7. Indonesia

- 1.8. Vietnam

- 1.9. ASEAN Countries

- 1.10. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Turkey

- 3.6. Spain

- 3.7. Russia

- 3.8. NORDIC

- 3.9. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Colombia

- 4.4. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Nigeria

- 5.4. Egypt

- 5.5. Qatar

- 5.6. UAE

- 5.7. Rest of Middle East and Africa

Hot Melt Adhesives Industry Regional Market Share

Geographic Coverage of Hot Melt Adhesives Industry

Hot Melt Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 6.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Ethylene Vinyl Acetate

- 5.1.2. Styrenic Block Co-polymers

- 5.1.3. Thermoplastic Polyurethane

- 5.1.4. Other Resin Types (Polyolefin, polyamide)

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Building and Construction

- 5.2.2. Paper, Board, and Packaging

- 5.2.3. Woodworking and Joinery

- 5.2.4. Automotive and Transportation

- 5.2.5. Footwear and Leather

- 5.2.6. Healthcare

- 5.2.7. Electrical and Electronic Appliances

- 5.2.8. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. Global Hot Melt Adhesives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Ethylene Vinyl Acetate

- 6.1.2. Styrenic Block Co-polymers

- 6.1.3. Thermoplastic Polyurethane

- 6.1.4. Other Resin Types (Polyolefin, polyamide)

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Building and Construction

- 6.2.2. Paper, Board, and Packaging

- 6.2.3. Woodworking and Joinery

- 6.2.4. Automotive and Transportation

- 6.2.5. Footwear and Leather

- 6.2.6. Healthcare

- 6.2.7. Electrical and Electronic Appliances

- 6.2.8. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. Asia Pacific Hot Melt Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 7.1.1. Ethylene Vinyl Acetate

- 7.1.2. Styrenic Block Co-polymers

- 7.1.3. Thermoplastic Polyurethane

- 7.1.4. Other Resin Types (Polyolefin, polyamide)

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Building and Construction

- 7.2.2. Paper, Board, and Packaging

- 7.2.3. Woodworking and Joinery

- 7.2.4. Automotive and Transportation

- 7.2.5. Footwear and Leather

- 7.2.6. Healthcare

- 7.2.7. Electrical and Electronic Appliances

- 7.2.8. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 8. North America Hot Melt Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 8.1.1. Ethylene Vinyl Acetate

- 8.1.2. Styrenic Block Co-polymers

- 8.1.3. Thermoplastic Polyurethane

- 8.1.4. Other Resin Types (Polyolefin, polyamide)

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Building and Construction

- 8.2.2. Paper, Board, and Packaging

- 8.2.3. Woodworking and Joinery

- 8.2.4. Automotive and Transportation

- 8.2.5. Footwear and Leather

- 8.2.6. Healthcare

- 8.2.7. Electrical and Electronic Appliances

- 8.2.8. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 9. Europe Hot Melt Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 9.1.1. Ethylene Vinyl Acetate

- 9.1.2. Styrenic Block Co-polymers

- 9.1.3. Thermoplastic Polyurethane

- 9.1.4. Other Resin Types (Polyolefin, polyamide)

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Building and Construction

- 9.2.2. Paper, Board, and Packaging

- 9.2.3. Woodworking and Joinery

- 9.2.4. Automotive and Transportation

- 9.2.5. Footwear and Leather

- 9.2.6. Healthcare

- 9.2.7. Electrical and Electronic Appliances

- 9.2.8. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 10. South America Hot Melt Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 10.1.1. Ethylene Vinyl Acetate

- 10.1.2. Styrenic Block Co-polymers

- 10.1.3. Thermoplastic Polyurethane

- 10.1.4. Other Resin Types (Polyolefin, polyamide)

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Building and Construction

- 10.2.2. Paper, Board, and Packaging

- 10.2.3. Woodworking and Joinery

- 10.2.4. Automotive and Transportation

- 10.2.5. Footwear and Leather

- 10.2.6. Healthcare

- 10.2.7. Electrical and Electronic Appliances

- 10.2.8. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 11. Middle East and Africa Hot Melt Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 11.1.1. Ethylene Vinyl Acetate

- 11.1.2. Styrenic Block Co-polymers

- 11.1.3. Thermoplastic Polyurethane

- 11.1.4. Other Resin Types (Polyolefin, polyamide)

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Building and Construction

- 11.2.2. Paper, Board, and Packaging

- 11.2.3. Woodworking and Joinery

- 11.2.4. Automotive and Transportation

- 11.2.5. Footwear and Leather

- 11.2.6. Healthcare

- 11.2.7. Electrical and Electronic Appliances

- 11.2.8. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Arkema

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Pidilite Industries Limited

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 3M

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Master Bond Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ashland

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Huntsman International LLC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Paramelt RMC B V

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Beardow Adams

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Dow

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 H B Fuller Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Alfa International

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Sika AG*List Not Exhaustive

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Franklin International

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Henkel Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Hexcel Corporation

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Jowat SE

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 AVERY DENNISON CORPORATION

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Mactac

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 DRYTAC

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 Arkema

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Hot Melt Adhesives Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Hot Melt Adhesives Industry Revenue (Million), by Resin Type 2025 & 2033

- Figure 3: Asia Pacific Hot Melt Adhesives Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 4: Asia Pacific Hot Melt Adhesives Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Hot Melt Adhesives Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Hot Melt Adhesives Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: Asia Pacific Hot Melt Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Hot Melt Adhesives Industry Revenue (Million), by Resin Type 2025 & 2033

- Figure 9: North America Hot Melt Adhesives Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 10: North America Hot Melt Adhesives Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 11: North America Hot Melt Adhesives Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Hot Melt Adhesives Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: North America Hot Melt Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hot Melt Adhesives Industry Revenue (Million), by Resin Type 2025 & 2033

- Figure 15: Europe Hot Melt Adhesives Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 16: Europe Hot Melt Adhesives Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: Europe Hot Melt Adhesives Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Hot Melt Adhesives Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Hot Melt Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Hot Melt Adhesives Industry Revenue (Million), by Resin Type 2025 & 2033

- Figure 21: South America Hot Melt Adhesives Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 22: South America Hot Melt Adhesives Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: South America Hot Melt Adhesives Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Hot Melt Adhesives Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Hot Melt Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Hot Melt Adhesives Industry Revenue (Million), by Resin Type 2025 & 2033

- Figure 27: Middle East and Africa Hot Melt Adhesives Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 28: Middle East and Africa Hot Melt Adhesives Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Hot Melt Adhesives Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Hot Melt Adhesives Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Hot Melt Adhesives Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 2: Global Hot Melt Adhesives Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 5: Global Hot Melt Adhesives Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: China Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: India Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Japan Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: South Korea Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Malaysia Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Thailand Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Indonesia Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Vietnam Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: ASEAN Countries Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Rest of Asia Pacific Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 18: Global Hot Melt Adhesives Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 19: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: United States Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Canada Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 24: Global Hot Melt Adhesives Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 25: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Germany Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: France Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Italy Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Turkey Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Spain Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Russia Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: NORDIC Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of Europe Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 36: Global Hot Melt Adhesives Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 37: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 38: Brazil Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Argentina Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Colombia Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Rest of South America Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 43: Global Hot Melt Adhesives Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 44: Global Hot Melt Adhesives Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 45: Saudi Arabia Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: South Africa Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 47: Nigeria Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Egypt Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 49: Qatar Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: UAE Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East and Africa Hot Melt Adhesives Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hot Melt Adhesives Industry?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the Hot Melt Adhesives Industry?

Key companies in the market include Arkema, Pidilite Industries Limited, 3M, Master Bond Inc, Ashland, Huntsman International LLC, Paramelt RMC B V, Beardow Adams, Dow, H B Fuller Company, Alfa International, Sika AG*List Not Exhaustive, Franklin International, Henkel Corporation, Hexcel Corporation, Jowat SE, AVERY DENNISON CORPORATION, Mactac, DRYTAC.

3. What are the main segments of the Hot Melt Adhesives Industry?

The market segments include Resin Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.06 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand from Packaging Industry; Rising Demand from Construction Sector; Other Drivers.

6. What are the notable trends driving market growth?

Paper. Board. and Packaging Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Volatility in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

April 2023: Avery Dennison and Dow collaborated to develop an innovative and sustainable new hot melt label adhesive solution. This enables polyolefin film labels and polypropylene (PP) or polyethylene (PE) packaging to be mechanically recycled together in one stream. It is based on AFFINITY™ GA Polymers from Dow and sold by Avery Dennison under the name CF3050 in the Europe, Middle East, and North Africa (EMENA) region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hot Melt Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hot Melt Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hot Melt Adhesives Industry?

To stay informed about further developments, trends, and reports in the Hot Melt Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence