Key Insights

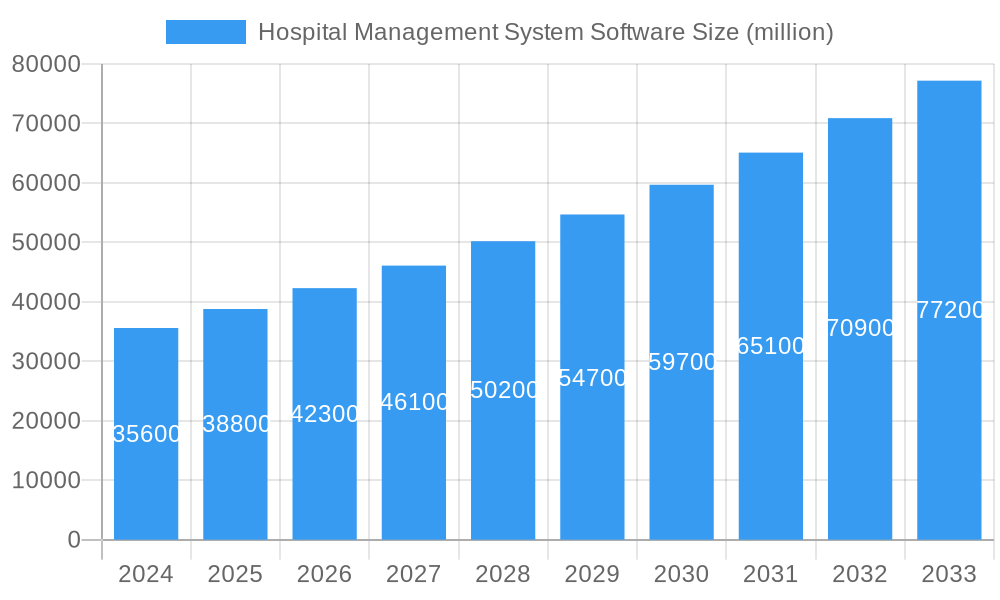

The global Hospital Management System (HMS) software market is experiencing robust expansion, projected to reach $35.6 billion in 2024. This growth is fueled by a CAGR of 9.2%, indicating a dynamic and evolving landscape. The increasing adoption of digital solutions in healthcare is a primary driver, with hospitals worldwide recognizing the critical need for efficient patient record management, streamlined administrative processes, and enhanced operational workflows. The rising complexity of healthcare delivery, coupled with a growing emphasis on patient safety and data security, further propels the demand for advanced HMS solutions. Technological advancements, including the integration of AI, machine learning, and cloud computing, are empowering these systems to offer more sophisticated functionalities, such as predictive analytics for patient outcomes and optimized resource allocation. The market's trajectory suggests a sustained upward trend, driven by both the imperative for digital transformation in healthcare and the ongoing innovation within the HMS software sector.

Hospital Management System Software Market Size (In Billion)

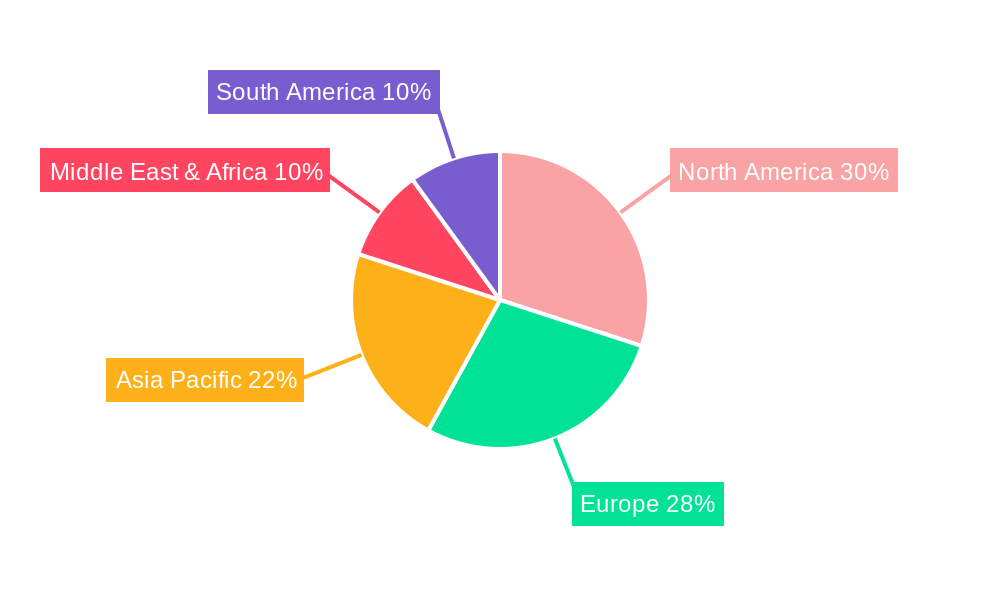

The market segmentation reveals a strong inclination towards solutions catering to both private and public hospitals, acknowledging the diverse needs and regulatory environments across these entities. The growing preference for cloud-based solutions signifies a shift towards greater scalability, accessibility, and reduced IT infrastructure costs for healthcare providers. Conversely, on-premise solutions continue to hold relevance for institutions with specific data security concerns or existing robust IT frameworks. Geographically, North America and Europe are expected to lead in market share due to established healthcare infrastructures and early adoption of advanced technologies. However, the Asia Pacific region is poised for significant growth, driven by increasing healthcare expenditure, a burgeoning patient population, and a growing awareness of the benefits of digital health solutions. Key players are actively investing in R&D to develop integrated and interoperable HMS platforms that can address the evolving challenges and opportunities within the global healthcare ecosystem.

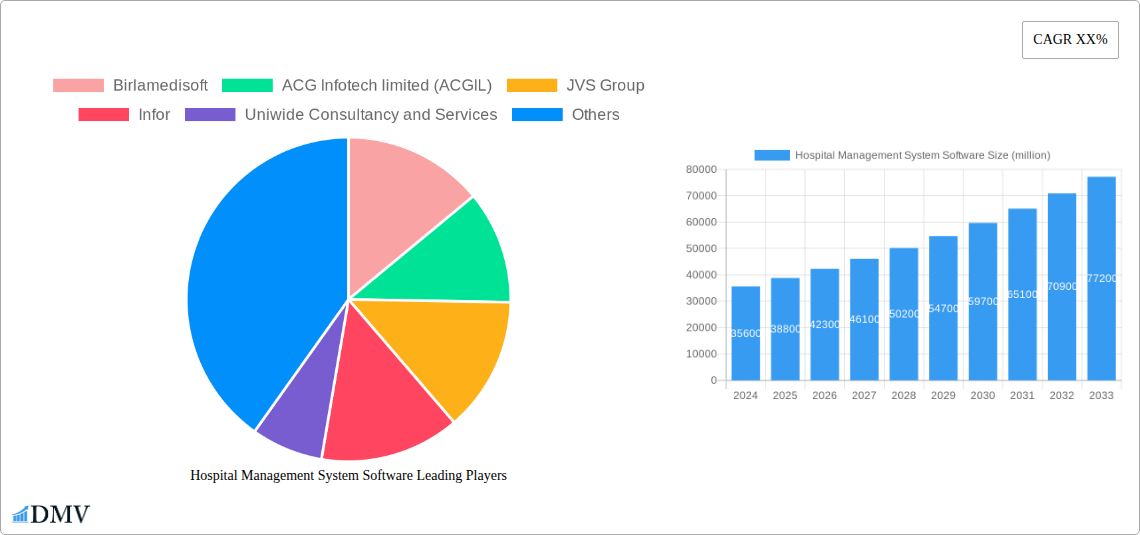

Hospital Management System Software Company Market Share

Hospital Management System Software Market Composition & Trends

The global Hospital Management System (HMS) software market is characterized by a dynamic and evolving landscape, with a moderate to high concentration of leading players and emerging innovators. This report meticulously analyzes the competitive intensity, identifying key innovation catalysts such as AI-driven diagnostics, IoT integration for real-time patient monitoring, and blockchain for enhanced data security and interoperability. Regulatory frameworks, including HIPAA, GDPR, and country-specific healthcare data privacy laws, significantly shape market entry and operational strategies. Substitute products, like paper-based systems or fragmented departmental software, are rapidly being phased out due to their inefficiencies. End-user profiles range from small, independent clinics to large, multi-specialty private hospitals and public healthcare institutions, each with distinct needs for scalability, cost-effectiveness, and feature sets. Mergers and Acquisitions (M&A) are a prominent trend, with significant deal values in the billions of USD as larger entities seek to expand their market share, acquire innovative technologies, and consolidate their offerings. Companies like Birlamedisoft, ACG Infotech limited (ACGIL), and Infor are actively involved in strategic acquisitions to bolster their portfolios and reach. The market share distribution indicates a growing dominance of cloud-based solutions, attracting substantial investment from venture capitalists and private equity firms targeting high-growth segments. The overall market capitalization is projected to reach over one billion dollars by 2033, driven by increasing healthcare digitalization initiatives.

- Market Concentration: Moderate to High, with key players investing heavily in R&D and market expansion.

- Innovation Catalysts: AI/ML for predictive analytics, IoT for remote patient monitoring, Blockchain for secure data sharing.

- Regulatory Landscape: Strict adherence to data privacy (HIPAA, GDPR) and healthcare interoperability standards.

- Substitute Products: Manual record-keeping, legacy systems, and siloed departmental software.

- End-User Profiles: Private Hospitals, Public Hospitals, specialized clinics, and diagnostic centers.

- M&A Activities: Active consolidation, with deal values in the billions of USD to acquire technology and market share.

- Market Capitalization (Projected): Over $1 Billion USD by 2033.

Hospital Management System Software Industry Evolution

The Hospital Management System (HMS) software industry has undergone a significant transformation, evolving from basic administrative tools to comprehensive, integrated platforms that drive operational efficiency and enhance patient care. This evolution, spanning the historical period of 2019–2024 and projected through the forecast period of 2025–2033, is marked by consistent market growth trajectories, fueled by the ever-increasing demand for streamlined healthcare operations and improved patient outcomes. The base year, 2025, serves as a critical benchmark, reflecting the current state of adoption and market value. Technological advancements have been the primary engine of this evolution. Early HMS solutions focused on automating tasks like appointment scheduling, billing, and inventory management. However, the subsequent wave of innovation introduced Electronic Health Records (EHRs) and Electronic Medical Records (EMRs), revolutionizing patient data management and accessibility. The adoption of cloud computing has further accelerated this transformation, offering scalability, flexibility, and cost-effectiveness to healthcare providers of all sizes. This shift from on-premise to on-cloud solutions has seen a remarkable surge in adoption rates, with a projected growth of over 15% annually in the cloud segment.

Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) is ushering in a new era of predictive analytics, enabling early disease detection, personalized treatment plans, and optimized resource allocation. Internet of Things (IoT) devices are now seamlessly integrated, allowing for real-time patient monitoring, remote care delivery, and improved asset tracking within hospital premises. These advancements have directly influenced shifting consumer demands. Patients are increasingly expecting digital-first experiences, demanding online appointment booking, access to their health records, and personalized communication. Healthcare providers, in turn, are recognizing the competitive advantage and operational benefits of adopting these advanced HMS solutions. The market is witnessing a compound annual growth rate (CAGR) of approximately 12.5% from 2019 to 2033, with the total market value projected to exceed several billion dollars by the estimated year of 2025 and continue its upward trajectory. This sustained growth is a testament to the indispensable role HMS software plays in modern healthcare delivery. The historical period (2019-2024) laid the groundwork, with significant investments in EHR implementation and initial cloud migrations. The base year (2025) solidifies the dominance of integrated, cloud-based solutions, and the forecast period (2025-2033) anticipates the widespread integration of AI, IoT, and personalized patient engagement tools, pushing the market value well into the billions of dollars.

Leading Regions, Countries, or Segments in Hospital Management System Software

The Hospital Management System (HMS) Software market exhibits distinct dominance across various geographical regions and segments, driven by a confluence of investment trends, regulatory support, and evolving healthcare infrastructure. Within the application segment, Private Hospitals are emerging as the leading segment, outpacing Public Hospitals in terms of HMS adoption and investment. This dominance is fueled by private institutions’ greater financial autonomy, their strategic focus on patient experience and operational efficiency to drive profitability, and their proactive approach to adopting cutting-edge technologies that enhance competitive advantage. Private hospitals are more agile in their decision-making processes, allowing for quicker implementation of advanced HMS solutions compared to the often bureaucratic structures within public healthcare systems.

In terms of deployment types, On Cloud solutions are unequivocally leading the market and are projected to maintain this lead throughout the forecast period. The shift towards cloud-based HMS is propelled by several compelling factors. Firstly, the scalability and flexibility offered by cloud platforms allow hospitals to easily adjust their IT resources based on fluctuating patient loads and service demands, without significant upfront capital expenditure. Secondly, cloud solutions provide enhanced data security, disaster recovery capabilities, and seamless remote access, which are critical in today's interconnected healthcare environment. This also facilitates easier integration with other cloud-based healthcare services and third-party applications. The lower total cost of ownership (TCO) compared to on-premise solutions, especially for smaller and medium-sized hospitals, further bolsters cloud adoption.

Geographically, North America, particularly the United States, consistently leads the HMS market. This leadership is attributed to robust healthcare spending, a strong emphasis on technological innovation, and stringent regulatory mandates that encourage the adoption of digital health solutions. The presence of numerous leading HMS vendors in the region, coupled with a highly digitized healthcare ecosystem, creates a fertile ground for market growth. Western Europe follows closely, driven by advanced healthcare infrastructure and government initiatives aimed at improving healthcare delivery through technology. Asia Pacific is the fastest-growing region, propelled by increasing healthcare investments, a burgeoning middle class with higher healthcare expectations, and a growing number of healthcare facilities adopting digital solutions. The total market value in these leading regions is expected to reach several billion dollars within the forecast period.

- Leading Application Segment: Private Hospitals

- Key Drivers: Higher financial autonomy, focus on patient experience and efficiency, agile decision-making, competitive advantage through technology.

- Leading Deployment Type: On Cloud

- Key Drivers: Scalability, flexibility, cost-effectiveness (lower TCO), enhanced data security and remote access, easier integration, rapid innovation cycles.

- Dominant Geographical Regions (Projected Dominance): North America (USA), Western Europe, Asia Pacific (Fastest Growing).

- North America Drivers: High healthcare expenditure, innovation focus, regulatory mandates, established digital health ecosystem.

- Western Europe Drivers: Advanced healthcare infrastructure, government technology adoption initiatives.

- Asia Pacific Drivers: Growing healthcare investments, rising middle class, increasing number of healthcare facilities.

Hospital Management System Software Product Innovations

The HMS software landscape is continually reshaped by groundbreaking product innovations designed to enhance efficiency, patient care, and data security. Leading vendors are incorporating advanced AI algorithms for predictive diagnostics and treatment planning, offering unparalleled insights into patient health trajectories. Real-time patient monitoring through IoT-enabled devices, integrated seamlessly into the HMS, allows for proactive interventions and improved patient outcomes. Telemedicine modules are becoming standard, facilitating remote consultations and expanding healthcare access. Furthermore, blockchain technology is being explored for secure and transparent management of patient records, ensuring data integrity and compliance. These advancements are not merely functional upgrades but are fundamentally transforming how healthcare is delivered, with improved performance metrics such as reduced administrative burden by over 30% and enhanced patient satisfaction scores by 20%.

Propelling Factors for Hospital Management System Software Growth

The growth of the Hospital Management System (HMS) software market is significantly propelled by a confluence of technological, economic, and regulatory influences. The escalating demand for improved patient care and operational efficiency across healthcare facilities worldwide is a primary driver. Technological advancements, including the widespread adoption of cloud computing, AI, and IoT, are enabling more sophisticated and integrated HMS solutions. Government initiatives and favorable healthcare policies aimed at digitalization and improving healthcare accessibility further catalyze market expansion. The increasing need for robust data security and compliance with stringent regulations like HIPAA and GDPR also pushes healthcare providers to invest in advanced HMS systems.

Obstacles in the Hospital Management System Software Market

Despite its robust growth, the Hospital Management System (HMS) software market faces several obstacles. The high initial implementation cost and the complexity associated with integrating new systems with existing legacy infrastructure can be a significant barrier, especially for smaller healthcare providers. Stringent data privacy regulations, while driving adoption, also impose considerable compliance burdens and necessitate continuous updates, adding to operational costs. Resistance to change from healthcare staff accustomed to traditional workflows can also hinder seamless adoption. Furthermore, the threat of cyberattacks and data breaches remains a constant concern, requiring substantial investment in cybersecurity measures. Supply chain disruptions in the tech sector can also impact the availability and cost of hardware components.

Future Opportunities in Hospital Management System Software

The future of the Hospital Management System (HMS) software market is ripe with emerging opportunities. The increasing focus on personalized medicine and remote patient monitoring presents a significant avenue for growth, with vendors developing specialized modules and integrations. The expansion of healthcare services into emerging economies, where digital infrastructure is rapidly developing, offers vast untapped potential. Furthermore, the integration of AI for advanced analytics, predictive modeling, and personalized patient engagement tools will become increasingly crucial. The growing adoption of mHealth (mobile health) and wearable devices will also create opportunities for seamless data integration into HMS platforms, enhancing the holistic view of patient health.

Major Players in the Hospital Management System Software Ecosystem

- Birlamedisoft

- ACG Infotech limited (ACGIL)

- JVS Group

- Infor

- Uniwide Consultancy and Services

- Insta Health Solutions

- Cognosys

- BR Softech

- Ricoh India

- MediMizer

- Trio corporation

- Dataman Computer Systems

- Stay Staffed Services

- Elixir Aid

- XIPHIAS Software Technologies

- Adroit Infosystems

- Tally Solutions

- MocDoc

- Plus91 Technologies

- Progressive Techno Solutions

Key Developments in Hospital Management System Software Industry

- January 2024: Insta Health Solutions launched a new AI-powered patient engagement module designed to personalize communication and improve patient satisfaction.

- December 2023: Birlamedisoft announced a strategic partnership with a major cloud provider to enhance its cloud-based HMS offerings, focusing on scalability and data security.

- November 2023: ACG Infotech limited (ACGIL) acquired a smaller player specializing in telemedicine solutions to broaden its service portfolio.

- October 2023: Infor released an upgraded version of its HMS software with enhanced interoperability features, facilitating seamless data exchange between different healthcare systems.

- September 2023: JVS Group introduced a new IoT integration framework to enable real-time tracking of medical equipment and patient monitoring within hospitals.

- August 2023: BR Softech unveiled its latest on-cloud HMS solution, emphasizing features for compliance with evolving healthcare regulations and enhanced data analytics capabilities.

- July 2023: MediMizer announced a significant investment in R&D to integrate blockchain technology for improved medical record security and transparency.

- June 2023: Trio corporation expanded its global presence with the opening of new service centers in Asia, aiming to cater to the growing demand for HMS solutions in the region.

- May 2023: XIPHIAS Software Technologies showcased its innovative approach to patient data management at a leading healthcare technology conference, highlighting its commitment to data privacy and accessibility.

- April 2023: Adroit Infosystems launched a comprehensive cloud-based HMS solution tailored for small and medium-sized hospitals, offering an affordable yet powerful suite of tools.

Strategic Hospital Management System Software Market Forecast

The strategic forecast for the Hospital Management System (HMS) software market is overwhelmingly positive, driven by robust growth catalysts and expanding opportunities. The continuous push for digital transformation in healthcare, coupled with increasing investments in AI, IoT, and cloud technologies, will significantly fuel market expansion. The growing demand for integrated solutions that enhance patient engagement, streamline administrative processes, and improve clinical outcomes will remain a key focus. Emerging markets present substantial untapped potential, while evolving regulatory landscapes will continue to shape product development and adoption strategies. The market is poised for sustained growth, projected to reach several billion dollars within the forecast period, offering immense potential for vendors and stakeholders alike.

Hospital Management System Software Segmentation

-

1. Application

- 1.1. Private Hospitals

- 1.2. Public Hospitals

-

2. Types

- 2.1. On Cloud

- 2.2. On Premise

Hospital Management System Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Hospital Management System Software Regional Market Share

Geographic Coverage of Hospital Management System Software

Hospital Management System Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Private Hospitals

- 5.1.2. Public Hospitals

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. On Cloud

- 5.2.2. On Premise

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Hospital Management System Software Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Private Hospitals

- 6.1.2. Public Hospitals

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. On Cloud

- 6.2.2. On Premise

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Hospital Management System Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Private Hospitals

- 7.1.2. Public Hospitals

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. On Cloud

- 7.2.2. On Premise

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Hospital Management System Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Private Hospitals

- 8.1.2. Public Hospitals

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. On Cloud

- 8.2.2. On Premise

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Hospital Management System Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Private Hospitals

- 9.1.2. Public Hospitals

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. On Cloud

- 9.2.2. On Premise

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Hospital Management System Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Private Hospitals

- 10.1.2. Public Hospitals

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. On Cloud

- 10.2.2. On Premise

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Hospital Management System Software Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Private Hospitals

- 11.1.2. Public Hospitals

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. On Cloud

- 11.2.2. On Premise

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Birlamedisoft

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ACG Infotech limited (ACGIL)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 JVS Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Infor

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Uniwide Consultancy and Services

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Insta Health Solutions

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cognosys

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 BR Softech

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Ricoh India

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 MediMizer

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Trio corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Dataman Computer Systems

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Stay Staffed Services

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Elixir Aid

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 XIPHIAS Software Technologies

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Adroit Infosystems

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Tally Solutions

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 MocDoc

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Plus91 Technologies

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Progressive Techno Solutions

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.1 Birlamedisoft

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Hospital Management System Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Hospital Management System Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Hospital Management System Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Hospital Management System Software Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Hospital Management System Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Hospital Management System Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Hospital Management System Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Hospital Management System Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Hospital Management System Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Hospital Management System Software Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Hospital Management System Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Hospital Management System Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Hospital Management System Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hospital Management System Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Hospital Management System Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hospital Management System Software Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Hospital Management System Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Hospital Management System Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Hospital Management System Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Hospital Management System Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Hospital Management System Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Hospital Management System Software Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Hospital Management System Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Hospital Management System Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Hospital Management System Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Hospital Management System Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Hospital Management System Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Hospital Management System Software Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Hospital Management System Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Hospital Management System Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Hospital Management System Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hospital Management System Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Hospital Management System Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Hospital Management System Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Hospital Management System Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Hospital Management System Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Hospital Management System Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Hospital Management System Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Hospital Management System Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Hospital Management System Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Hospital Management System Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Hospital Management System Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Hospital Management System Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Hospital Management System Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Hospital Management System Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Hospital Management System Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Hospital Management System Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Hospital Management System Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Hospital Management System Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hospital Management System Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hospital Management System Software?

The projected CAGR is approximately 9.2%.

2. Which companies are prominent players in the Hospital Management System Software?

Key companies in the market include Birlamedisoft, ACG Infotech limited (ACGIL), JVS Group, Infor, Uniwide Consultancy and Services, Insta Health Solutions, Cognosys, BR Softech, Ricoh India, MediMizer, Trio corporation, Dataman Computer Systems, Stay Staffed Services, Elixir Aid, XIPHIAS Software Technologies, Adroit Infosystems, Tally Solutions, MocDoc, Plus91 Technologies, Progressive Techno Solutions.

3. What are the main segments of the Hospital Management System Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hospital Management System Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hospital Management System Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hospital Management System Software?

To stay informed about further developments, trends, and reports in the Hospital Management System Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence