Key Insights

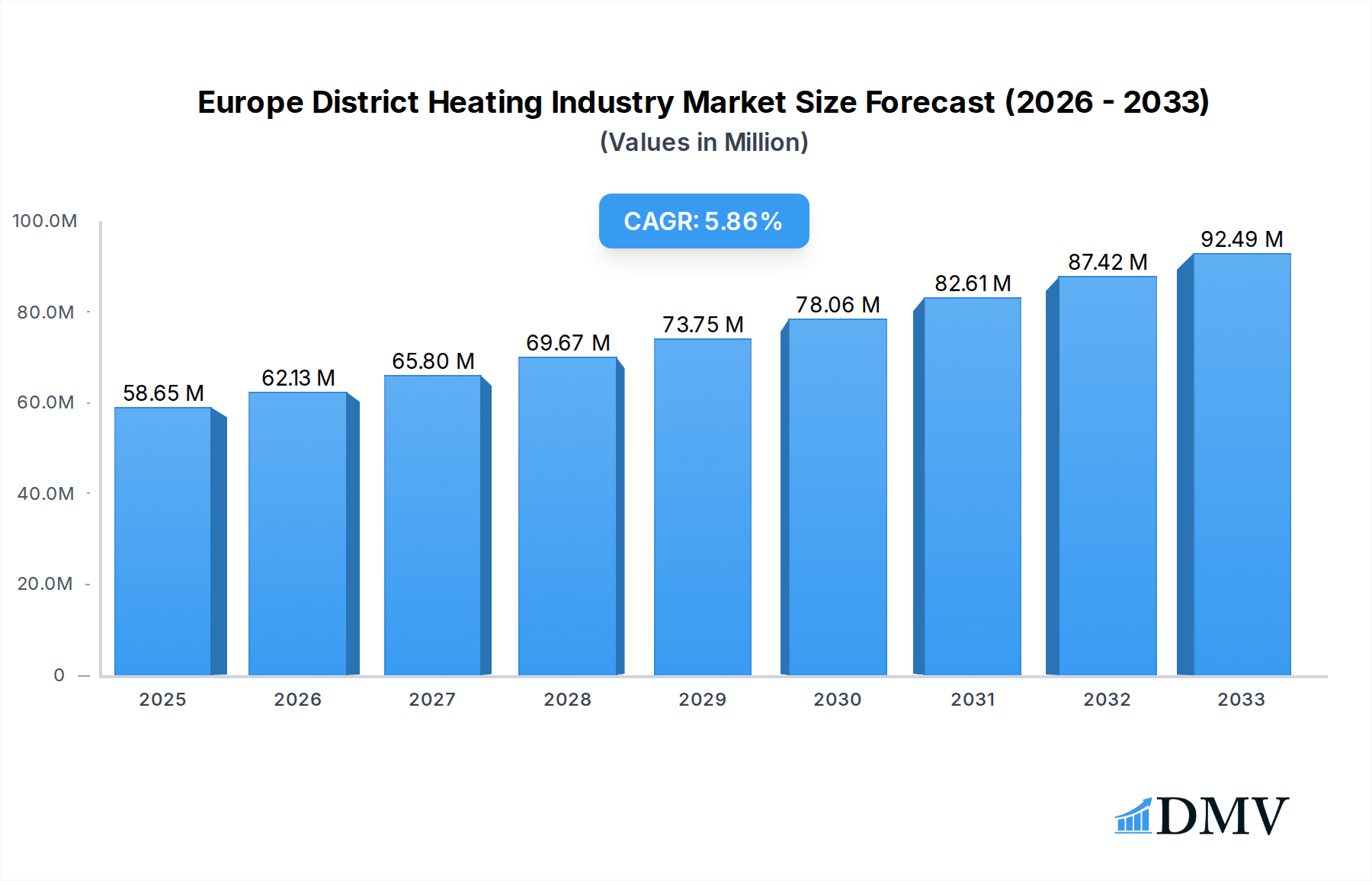

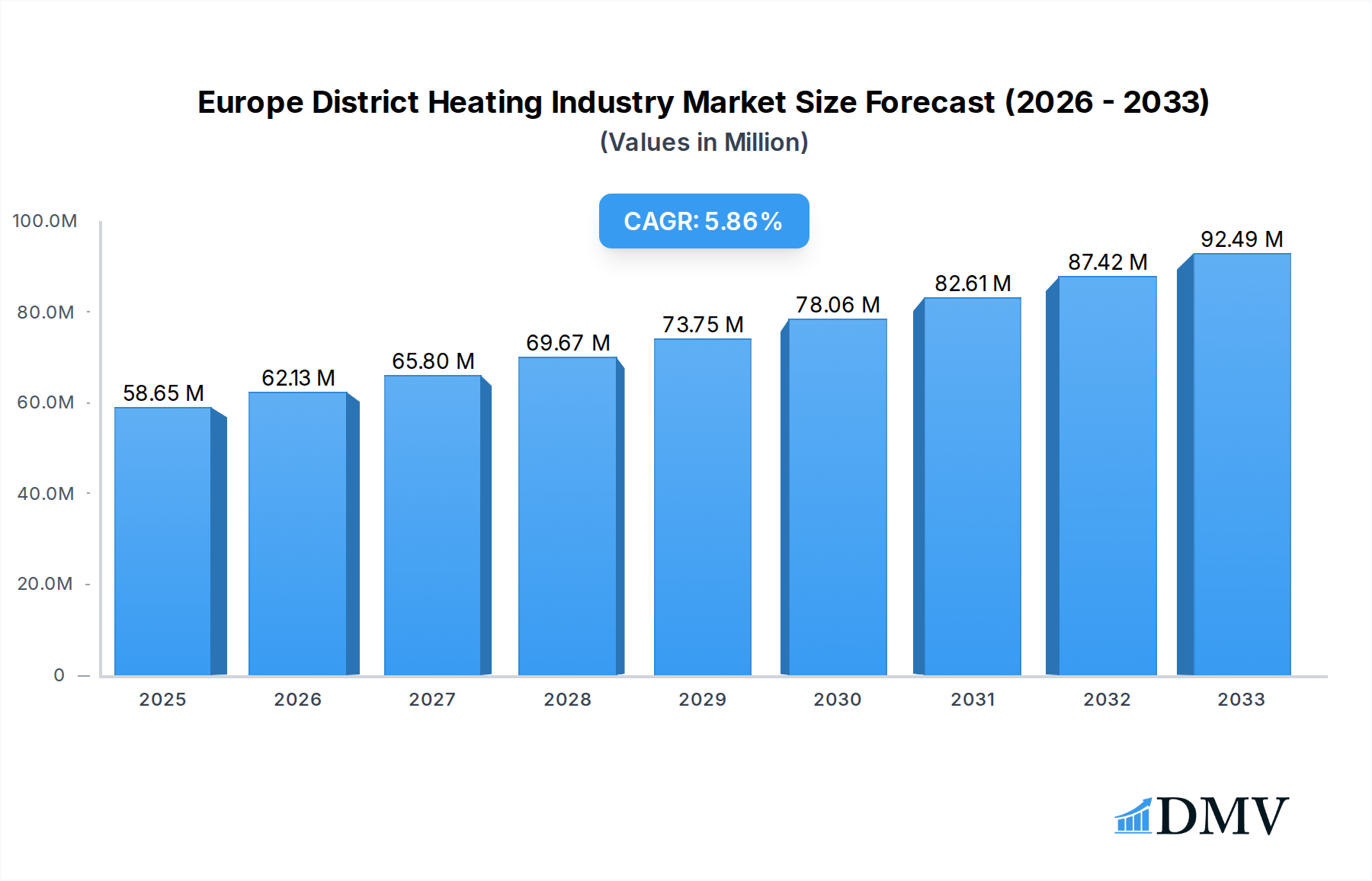

The Europe District Heating Industry is poised for substantial growth, projected to reach an estimated USD 58.65 Million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.90% anticipated over the forecast period of 2025-2033. This upward trajectory is fueled by a confluence of driving forces, primarily the increasing demand for sustainable and energy-efficient heating solutions across residential, commercial, and industrial sectors. Governments across Europe are actively promoting district heating networks as a key strategy to decarbonize their energy systems, reduce reliance on fossil fuels, and combat climate change. The inherent benefits of district heating, such as improved energy efficiency, reduced emissions at the local level, and enhanced grid stability, are increasingly recognized and valued. Furthermore, ongoing technological advancements in heat generation (including renewable sources like geothermal, solar thermal, and waste heat recovery) and distribution systems are making district heating more competitive and attractive to both consumers and utility providers.

Europe District Heating Industry Market Size (In Million)

Despite the promising outlook, certain restraints could temper the pace of expansion. High initial investment costs for establishing new district heating infrastructure and upgrading existing ones remain a significant hurdle, particularly in regions with less developed networks. The complex regulatory landscape and the need for extensive planning and permitting processes can also introduce delays. However, these challenges are increasingly being addressed through supportive government policies, public-private partnerships, and innovative financing models. Key trends shaping the market include the integration of smart grid technologies for better management and optimization of heat distribution, the growing adoption of renewable energy sources for heat generation, and a shift towards decentralized energy systems where district heating plays a crucial role in balancing supply and demand. Leading companies such as Danfoss AS, Engie SA, Vattenfall AB, and Alfa Laval AB are actively investing in research, development, and expansion to capitalize on these evolving market dynamics. The market's concentration in key European countries like the United Kingdom, Germany, France, and Sweden underscores the significant potential and ongoing commitment to this sustainable heating solution.

Europe District Heating Industry Company Market Share

Europe District Heating Industry Market Composition & Trends

The Europe district heating market is characterized by a dynamic composition driven by increasing decarbonization mandates and robust energy efficiency initiatives. Market concentration is gradually shifting as established players like Danfoss AS, Engie SA, Vattenfall AB, and Statkraft AS strategically invest in expanding their network reach and integrating renewable energy sources. Innovation catalysts are predominantly focused on advanced heat recovery technologies, smart grid integration, and the utilization of waste heat, exemplified by Alfa Laval AB's deployments. The regulatory landscape across European nations strongly favors the adoption of district heating, with supportive policies and carbon pricing mechanisms acting as significant drivers. Substitute products, primarily individual heating systems (e.g., gas boilers, electric heaters), are facing increasing pressure due to their higher carbon footprint and less efficient energy distribution. End-user profiles encompass residential, commercial, and industrial sectors, each with unique demands for reliable and sustainable heating solutions. Mergers and acquisitions (M&A) activities are on the rise, indicating a consolidation trend with significant deal values anticipated as companies seek to gain market share and technological expertise. For instance, partnerships like the one between Ameresco and Vattenfall AB for the Bristol City Leap project underscore the substantial investment flowing into this sector, aiming to deliver substantial low-carbon energy infrastructure valued in the hundreds of millions of Euros. Historical data indicates a steady growth trajectory, with the market expected to see accelerated expansion in the coming years, driven by ambitious climate targets and a growing consumer preference for green energy solutions. The market share distribution is still evolving, with opportunities for both established and emerging companies to carve out significant portions of this expanding sector.

Europe District Heating Industry Industry Evolution

The Europe district heating industry has witnessed a significant evolution, transforming from a traditional method of energy distribution to a pivotal component of the continent's ambitious decarbonization strategy. Over the historical period from 2019 to 2024, the market has experienced a consistent upward trajectory, driven by increasing environmental awareness and stringent governmental regulations aimed at reducing carbon emissions. The base year of 2025 sets the stage for continued robust growth throughout the forecast period of 2025–2033, with projections indicating sustained compound annual growth rates of approximately 7-9%. This growth is underpinned by a multifaceted approach to energy sourcing. Technological advancements have been a critical enabler, moving beyond fossil fuel-based sources to incorporate a diverse array of renewable and waste heat alternatives. Innovations in heat pump technology, solar thermal integration, and advanced waste heat recovery systems, as pioneered by companies like Alfa Laval AB, are becoming increasingly sophisticated and economically viable. The adoption of smart grid technologies and advanced control systems has also played a crucial role, enhancing the efficiency, reliability, and flexibility of district heating networks. Consumer demand has shifted significantly, with a growing segment of end-users – residential, commercial, and industrial – actively seeking cleaner, more cost-effective, and sustainable heating solutions. This shift is reflected in increased investment in modernizing existing infrastructure and developing new, large-scale district heating projects across major European cities. For example, the significant investment attracted by the Bristol City Leap project involving Vattenfall AB highlights the market's capacity to secure substantial funding for transformative decarbonization initiatives. The industry is actively moving towards a more decentralized and integrated energy system, where district heating networks act as hubs for various low-carbon energy sources. This evolution is not merely about distributing heat; it is about creating intelligent, sustainable energy ecosystems that contribute significantly to achieving Europe's climate neutrality goals. The market's growth trajectory is further bolstered by supportive policy frameworks, including carbon pricing mechanisms and subsidies for renewable energy adoption, creating a favorable investment climate.

Leading Regions, Countries, or Segments in Europe District Heating Industry

The dominance within the Europe district heating industry is not monolithic but rather a complex interplay of regional strengths, national policies, and specific end-user segment demands. However, Scandinavian countries, particularly Sweden, Denmark, and Finland, consistently emerge as leaders in district heating adoption and innovation. This leadership is intrinsically linked to a long-standing commitment to renewable energy integration and a proactive approach to tackling climate change.

- Key Drivers for Regional Dominance:

- Early Adoption and Policy Support: These nations were pioneers in developing extensive district heating networks, supported by decades of favorable government policies, including dedicated subsidies and regulatory frameworks promoting energy efficiency and renewable energy sources.

- Abundant Renewable Resources: Access to readily available biomass, geothermal energy, and waste heat from industrial processes provides a strong foundation for sustainable district heating.

- High Population Density and Urbanization: Concentrated urban populations in these countries make the centralized delivery of heat via district heating networks economically and logistically more efficient than individual heating systems.

- Public Acceptance and Awareness: A high level of public environmental consciousness and trust in public utility services facilitates the widespread acceptance and expansion of district heating infrastructure.

In terms of end-user segments, the Residential sector often represents the largest consumer base for district heating across Europe. This dominance stems from several factors:

- High Volume Demand: The sheer number of residential units in urban and suburban areas creates a substantial and consistent demand for heating.

- Decarbonization Pressure: Residential buildings are a significant contributor to overall building emissions, making them a key target for decarbonization efforts through cleaner heating solutions like district heating.

- Cost-Effectiveness and Convenience: For many households, district heating offers predictable and often lower heating bills compared to individual systems, coupled with the convenience of minimal maintenance.

- Retrofitting Opportunities: The extensive stock of older residential buildings presents a significant opportunity for retrofitting with district heating connections, contributing to the revitalization of urban energy infrastructure.

While the residential segment holds a considerable share, the Commercial and Industrial segments are rapidly gaining prominence, driven by their unique requirements and capacity for large-scale energy consumption. Commercial entities, such as office buildings, hospitals, and retail complexes, are increasingly prioritizing sustainability to meet corporate social responsibility goals and attract environmentally conscious tenants. The industrial sector, particularly those with high-temperature processes, can leverage district heating for process heat and building heating, often benefiting from waste heat recovery opportunities. Companies like Engie SA and Vattenfall AB are actively developing bespoke solutions for these larger consumers, recognizing their potential for significant decarbonization impact and long-term contracts. The strategic focus on these segments is crucial for achieving overall energy system efficiency and meeting ambitious climate targets across the continent.

Europe District Heating Industry Product Innovations

Product innovation in the Europe district heating industry is characterized by a drive towards greater efficiency, sustainability, and smart integration. Leading companies are investing heavily in advanced heat exchangers, such as those developed by Alfa Laval AB, which are critical for optimizing heat transfer from diverse sources like industrial waste heat and geothermal energy. The integration of highly efficient heat pumps, coupled with sophisticated control systems, allows for the utilization of lower-grade heat sources that were previously uneconomical. Innovations in pipe materials and insulation technologies are reducing heat losses throughout the distribution network, thereby enhancing overall system efficiency. Furthermore, the development of smart metering and demand-side management solutions empowers end-users and network operators to optimize energy consumption and distribution. These advancements collectively contribute to a more resilient, cost-effective, and environmentally friendly district heating infrastructure across Europe, making it an increasingly attractive solution for decarbonizing heat.

Propelling Factors for Europe District Heating Industry Growth

The Europe district heating industry's growth is propelled by a potent combination of factors. Firstly, stringent European Union climate targets and national decarbonization policies mandate a significant shift away from fossil fuels, making low-carbon district heating a preferred solution. Secondly, technological advancements in heat recovery from industrial waste, renewable energy integration (biomass, geothermal, solar thermal), and efficient heat pump technologies are making district heating more viable and cost-effective. Thirdly, increasing energy security concerns are driving demand for diversified and localized energy sources, with district heating offering a reliable and stable supply. Finally, growing consumer and corporate demand for sustainable and efficient heating solutions further fuels market expansion, as evidenced by the significant investments attracted by projects like the Bristol City Leap.

Obstacles in the Europe District Heating Industry Market

Despite its strong growth potential, the Europe district heating industry faces several obstacles. High upfront investment costs for developing new infrastructure and modernizing existing networks remain a significant barrier, particularly for smaller municipalities. Complex regulatory landscapes and permitting processes across different European countries can lead to project delays and increased administrative burdens. Competition from established individual heating systems and the inertia of consumer preference can also slow down adoption rates. Furthermore, supply chain disruptions for key components and volatile energy prices can impact project feasibility and operational costs. Ensuring a consistent and affordable supply of sustainable heat sources also presents ongoing challenges.

Future Opportunities in Europe District Heating Industry

Future opportunities in the Europe district heating industry are abundant and diverse. The expansion of circular economy initiatives presents a significant opportunity to leverage waste heat from various industrial and urban processes, moving towards zero-waste heat solutions. The increasing adoption of digitalization and smart grid technologies will enable more efficient network management, predictive maintenance, and personalized heating services for end-users. Emerging technologies like geothermal district heating and the integration of large-scale heat storage solutions offer pathways to enhance grid stability and reliability. Furthermore, the development of new business models such as energy-as-a-service and community-led heating projects can unlock new markets and accelerate adoption, particularly in regions with less developed infrastructure. The ongoing focus on decarbonizing the built environment will continue to be a primary driver for growth.

Major Players in the Europe District Heating Industry Ecosystem

- Danfoss AS

- Engie SA

- Vattenfall AB

- Göteborg Energi

- Statkraft AS

- Logstor AS

- Vital Energi Ltd

- Ramboll Group AS

- Alfa Laval AB

Key Developments in Europe District Heating Industry Industry

- May 2022: Alfa Laval deployed its unique technology to recover industrial waste heat from a sulphuric acid plant for reuse in a district heating network in Hamburg, Germany. This expansion benefits over 23,000 households, hotels, offices, and the university, contributing to the city’s green footprint as part of a German government initiative.

- March 2022: Ameresco partnered with Vattenfall, attracting investment worth around EUR 1.2 billion (USD 1.28 billion) for the Bristol City Leap project, a 20-year concession to decarbonize the city. Over the first five years, the project will deliver around GBP 424 million (USD 521.49 million) in low-carbon energy infrastructure across heat networks, renewable energy, heat pumps, energy efficiency, and electric vehicle charging, accounting for approximately 140,000 tonnes of carbon savings and 182 MW of zero-carbon energy generation.

Strategic Europe District Heating Industry Market Forecast

The strategic outlook for the Europe district heating industry is exceptionally positive, driven by accelerating decarbonization imperatives and robust policy support. The forecast period of 2025–2033 anticipates significant market expansion, fueled by continuous investment in renewable energy integration, waste heat recovery technologies, and smart grid infrastructure. The increasing demand for sustainable and efficient heating solutions across residential, commercial, and industrial sectors will solidify district heating's role as a cornerstone of Europe's energy transition. Growth catalysts include ambitious climate targets, technological innovation, and a growing awareness of the economic and environmental benefits of centralized heating networks. The market is poised for substantial growth, projected to reach several hundred billion Euros, offering substantial opportunities for stakeholders to contribute to a greener and more secure energy future for the continent.

Europe District Heating Industry Segmentation

-

1. End User

- 1.1. Residential

- 1.2. Commercial and Industrial

Europe District Heating Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe District Heating Industry Regional Market Share

Geographic Coverage of Europe District Heating Industry

Europe District Heating Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Residential

- 5.1.2. Commercial and Industrial

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. Europe District Heating Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User

- 6.1.1. Residential

- 6.1.2. Commercial and Industrial

- 6.1. Market Analysis, Insights and Forecast - by End User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Danfoss AS

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Engie SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Vattenfall AB

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Göteborg Energi

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Statkraft AS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Logstor AS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Vital Energi Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ramboll Group AS*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Alfa Laval AB

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Danfoss AS

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe District Heating Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe District Heating Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe District Heating Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 2: Europe District Heating Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Europe District Heating Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Europe District Heating Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: France Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe District Heating Industry?

The projected CAGR is approximately 5.90%.

2. Which companies are prominent players in the Europe District Heating Industry?

Key companies in the market include Danfoss AS, Engie SA, Vattenfall AB, Göteborg Energi, Statkraft AS, Logstor AS, Vital Energi Ltd, Ramboll Group AS*List Not Exhaustive, Alfa Laval AB.

3. What are the main segments of the Europe District Heating Industry?

The market segments include End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 58.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Augmented Demand for Energy-efficient and Cost effective Heating Systems; Rising Urbanization and Industrialization.

6. What are the notable trends driving market growth?

Residential End User Segment is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Stringent Regulations and Validatory Guidelines.

8. Can you provide examples of recent developments in the market?

May 2022: Alfa Laval deployed its unique technology to recover industrial waste heat from a sulphuric acid plant for reuse in a district heating network in Hamburg, Germany. More than 23,000 households, hotels, offices, and the university will benefit from more heating as the company expands the waste heat recovery project, which Alfa Laval first installed in 2018. The project contributes to the city’s green footprint as a part of a German government initiative.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe District Heating Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe District Heating Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe District Heating Industry?

To stay informed about further developments, trends, and reports in the Europe District Heating Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence