Key Insights

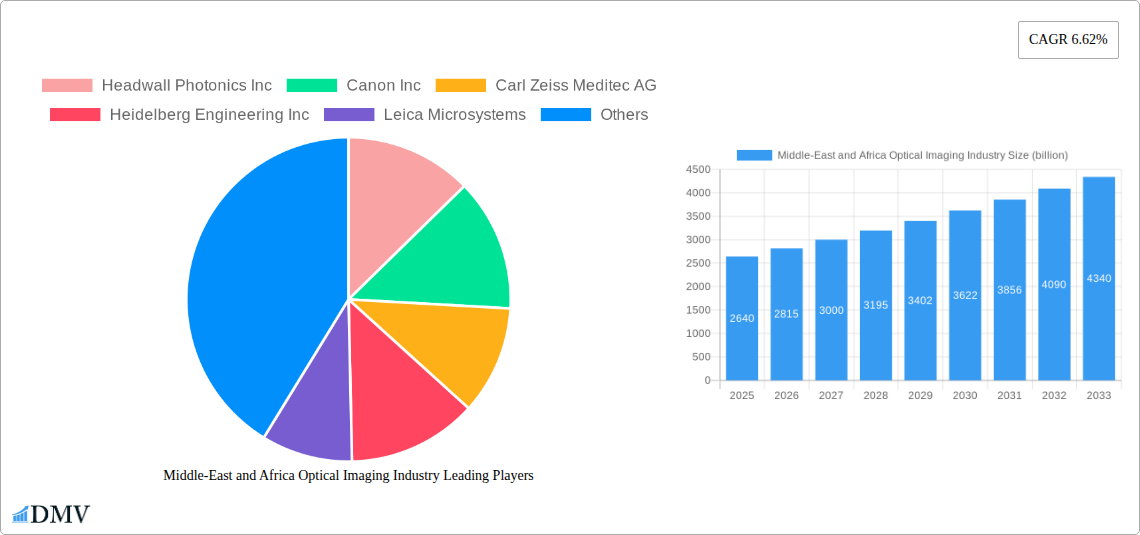

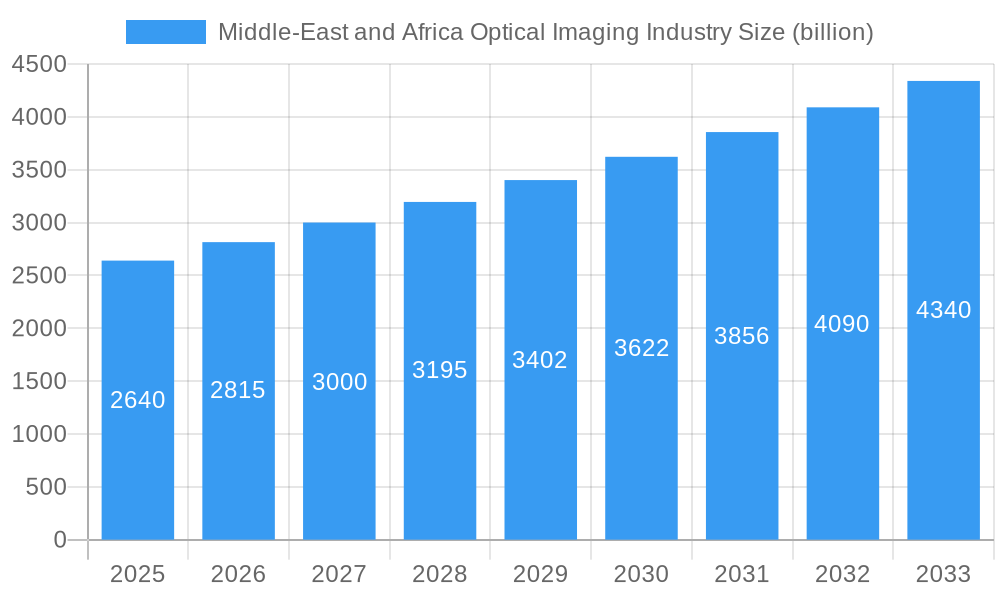

The Middle East and Africa optical imaging market is poised for significant expansion, projected to reach an estimated USD 2.64 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.62% anticipated throughout the forecast period of 2025-2033. This growth is underpinned by a confluence of advancing healthcare infrastructure, increasing prevalence of chronic diseases, and a rising demand for minimally invasive diagnostic and therapeutic solutions. Emerging economies in the region are witnessing substantial investments in healthcare, leading to the adoption of sophisticated medical technologies, including advanced optical imaging systems. The expanding healthcare tourism sector further contributes to this upward trajectory, drawing patients for specialized treatments where optical imaging plays a crucial role in diagnosis and surgical guidance.

Middle-East and Africa Optical Imaging Industry Market Size (In Billion)

Key drivers for this market surge include the increasing incidence of ophthalmic, oncological, and dermatological conditions, which necessitate precise visualization for early detection and effective management. Technological advancements in photoacoustic tomography, optical coherence tomography, and hyperspectral imaging are enhancing diagnostic accuracy and patient outcomes, thereby fueling market adoption. The growing emphasis on preventative healthcare and early disease screening also presents a substantial opportunity. Furthermore, the development and widespread availability of advanced imaging systems, illumination systems, and specialized optical imaging software are contributing to the market's dynamism. Hospitals, clinics, and research institutions are increasingly investing in these technologies to improve their diagnostic capabilities and research endeavors.

Middle-East and Africa Optical Imaging Industry Company Market Share

Middle-East and Africa Optical Imaging Industry Market Analysis and Forecast 2025-2033

Report Description:

Embark on a comprehensive exploration of the burgeoning Middle-East and Africa (MEA) Optical Imaging Industry, a sector poised for significant expansion driven by advanced healthcare infrastructure, increasing adoption of cutting-edge diagnostic tools, and robust investment in medical technologies. This in-depth report provides an unparalleled analysis of market dynamics, strategic imperatives, and future growth trajectories for optical imaging solutions across the MEA region. Delve into the intricate segmentation of this vibrant market, encompassing key technologies like Optical Coherence Tomography (OCT) and Hyperspectral Imaging, alongside product categories such as Imaging Systems and Optical Imaging Software. Understand the critical applications in Ophthalmology, Oncology, and Cardiology, and identify the primary end-user industries, including Hospitals and Clinics and Research and Diagnostic Laboratories. With a detailed forecast period of 2025–2033 and a base year of 2025, this report leverages precise data and expert insights to equip stakeholders with actionable intelligence for strategic decision-making. Uncover the competitive landscape featuring industry leaders like Canon Inc., Carl Zeiss Meditec AG, and Abbott Laboratories, and gain foresight into upcoming innovations and market opportunities. This report is essential for businesses, investors, and policymakers seeking to capitalize on the transformative potential of optical imaging in the MEA region.

Middle-East and Africa Optical Imaging Industry Market Composition & Trends

The MEA Optical Imaging Industry is characterized by a dynamic market composition driven by a confluence of innovation catalysts and evolving regulatory landscapes. While market concentration is moderately fragmented, key players are continuously investing in research and development to introduce novel solutions, particularly in Optical Coherence Tomography and Hyperspectral Imaging. Substitute products, though present in some niche applications, are increasingly being outpaced by the superior diagnostic capabilities offered by advanced optical imaging technologies. End-user profiles are shifting, with a growing demand for higher resolution, faster imaging speeds, and non-invasive diagnostic methods across Ophthalmology, Oncology, and Cardiology. Mergers and acquisitions (M&A) activities are anticipated to play a crucial role in market consolidation and the expansion of technological portfolios. The overall market size is projected to reach tens of billions USD in the coming years, with M&A deal values expected to escalate as larger entities seek to acquire innovative startups and specialized technology providers.

- Market Concentration: Moderately fragmented with key players driving innovation.

- Innovation Catalysts: Growing healthcare expenditure, demand for advanced diagnostics, and government initiatives promoting medical technology adoption.

- Regulatory Landscapes: Increasingly favorable with focus on patient safety and data integrity, though varying across individual MEA countries.

- Substitute Products: Limited in advanced applications, with optical imaging offering superior specificity and sensitivity.

- End-User Profiles: Primarily Hospitals and Clinics, Research and Diagnostic Laboratories, with growing interest from Pharmaceutical and Biotechnology Companies.

- M&A Activities: Expected to increase, facilitating market consolidation and technology integration.

Middle-East and Africa Optical Imaging Industry Industry Evolution

The Middle-East and Africa Optical Imaging Industry has witnessed a remarkable evolutionary trajectory, fueled by rapid technological advancements, increasing healthcare infrastructure development, and a growing awareness of the benefits of advanced diagnostic modalities. From its nascent stages, the industry has transitioned into a robust market, with a compound annual growth rate (CAGR) projected to be in the high single digits over the forecast period. This growth is intrinsically linked to the increasing prevalence of chronic diseases such as diabetes-related eye conditions, cancer, and cardiovascular diseases, all of which benefit significantly from early and accurate diagnosis facilitated by optical imaging techniques. The adoption of Optical Coherence Tomography in ophthalmology has revolutionized the diagnosis and management of retinal diseases, contributing significantly to market expansion. Similarly, Hyperspectral Imaging is gaining traction in oncology for its ability to differentiate between cancerous and healthy tissue with unprecedented precision, reducing the need for invasive biopsies and improving treatment outcomes.

The evolution is further marked by significant investments in healthcare infrastructure across key MEA nations, particularly in the UAE, Saudi Arabia, and South Africa. These investments have led to the establishment of state-of-the-art medical facilities equipped with the latest optical imaging systems. The demand for improved patient care and diagnostic accuracy is a primary driver for this evolution, pushing manufacturers to develop more sophisticated and user-friendly imaging solutions. Near-Infrared Spectroscopy (NIRS) is also carving out a significant niche, especially in monitoring tissue oxygenation and blood flow, finding applications in neurology and cardiology. The integration of artificial intelligence (AI) and machine learning with optical imaging systems is another critical aspect of this evolution, enhancing image analysis, automating diagnostic processes, and improving diagnostic accuracy.

Furthermore, the growing emphasis on preventative healthcare and early disease detection is accelerating the adoption of optical imaging technologies across various application areas. For instance, advancements in Pathological Imaging using optical methods are enabling more precise cancer diagnosis and staging. The report highlights that the market is moving towards integrated solutions that combine imaging hardware with advanced software for data management, analysis, and reporting. The increasing per capita healthcare spending in several MEA countries, coupled with supportive government policies aimed at enhancing healthcare access and quality, is creating a fertile ground for sustained growth. The development of portable and more affordable optical imaging devices is also expanding access to these technologies in underserved regions within Africa, further contributing to the industry's inclusive evolution. The forecast period, 2025–2033, is expected to see continued acceleration in adoption rates, driven by further innovation and a deepening understanding of the clinical benefits of optical imaging.

Leading Regions, Countries, or Segments in Middle-East and Africa Optical Imaging Industry

The Middle-East and Africa Optical Imaging Industry exhibits distinct regional dominance and segment leadership, with the United Arab Emirates (UAE) emerging as a frontrunner due to its advanced healthcare infrastructure, significant investment in medical technology, and a strong focus on specialized medical tourism. Within the UAE, the Ophthalmology application area is a particularly dominant segment, driven by the high prevalence of eye conditions and the early adoption of sophisticated diagnostic tools. The opening of advanced eye clinics, such as the Barraquer clinic in Dubai, equipped with the latest technologies and staffed by highly trained professionals, underscores this leadership.

Technologically, Optical Coherence Tomography (OCT) stands out as a leading segment, revolutionizing the diagnosis and management of a wide range of ocular diseases, from diabetic retinopathy to glaucoma. Its non-invasive nature, high resolution, and ability to provide cross-sectional images of retinal layers make it indispensable for ophthalmologists. Coupled with advancements in Imaging Systems specifically designed for OCT, this technology has seen widespread adoption in hospitals and specialized eye care centers across the region.

The Hospitals and Clinics end-user industry is the primary driver of demand for optical imaging solutions. These institutions are increasingly investing in advanced diagnostic equipment to improve patient care, reduce diagnostic turnaround times, and enhance their competitive edge. The Pharmaceutical Industry and Biotechnology Companies are also emerging as significant stakeholders, utilizing optical imaging for drug discovery, preclinical research, and clinical trial support, particularly for applications in Oncology and Cardiology.

Dominant Region: United Arab Emirates (UAE)

- Key Drivers: High healthcare expenditure, government support for medical innovation, advanced infrastructure, and medical tourism.

- In-depth Analysis: The UAE's strategic vision for a robust healthcare ecosystem has fostered an environment conducive to the adoption of cutting-edge technologies like optical imaging. Investments in specialized medical centers and the presence of a skilled workforce further solidify its leadership position.

Dominant Technology: Optical Coherence Tomography (OCT)

- Key Drivers: Clinical efficacy in ophthalmology, non-invasive diagnostic capabilities, technological advancements in imaging speed and resolution.

- In-depth Analysis: OCT's ability to provide detailed cross-sectional views of tissues, particularly the retina, has made it a cornerstone of modern ophthalmological diagnostics. Its ongoing development promises further applications in other medical fields.

Dominant Application Area: Ophthalmology

- Key Drivers: High prevalence of eye diseases (e.g., diabetic retinopathy, glaucoma, age-related macular degeneration), increasing aging population, and demand for early detection and precise management.

- In-depth Analysis: The sheer volume of patients requiring comprehensive eye care, coupled with the proven benefits of optical imaging in diagnosing and monitoring these conditions, makes ophthalmology a consistently strong performer in the optical imaging market.

Dominant Product Category: Imaging Systems

- Key Drivers: Demand for integrated and high-performance imaging solutions across various medical specialties, continuous innovation in hardware design and functionality.

- In-depth Analysis: The core of optical imaging lies in its advanced imaging systems. As technologies like OCT and hyperspectral imaging evolve, so too do the sophisticated imaging systems that power them, meeting the growing clinical and research demands.

Dominant End-User Industry: Hospitals and Clinics

- Key Drivers: Central role in patient care, direct access to patients, and significant budgets allocated for medical equipment procurement.

- In-depth Analysis: Hospitals and clinics are the primary point of care for most patients, making them the most significant adopters of optical imaging technologies for diagnostic and therapeutic purposes. Their investment decisions directly shape market trends.

Middle-East and Africa Optical Imaging Industry Product Innovations

Product innovations in the MEA Optical Imaging Industry are rapidly transforming diagnostic capabilities. Companies are focusing on developing highly sensitive and specific Imaging Systems that offer enhanced resolution and faster acquisition times. Innovations in Optical Coherence Tomography are enabling deeper tissue penetration and real-time imaging for Intraoperative Imaging, particularly in neurological surgeries. Furthermore, advancements in Hyperspectral Imaging are leading to the development of portable devices for early cancer detection in dermatology. These innovations are characterized by user-friendly interfaces, AI-driven image analysis, and improved data management, ultimately enhancing diagnostic accuracy and streamlining clinical workflows.

Propelling Factors for Middle-East and Africa Optical Imaging Industry Growth

Several factors are propelling the growth of the MEA Optical Imaging Industry. A significant driver is the increasing prevalence of chronic diseases, including diabetes, cancer, and cardiovascular conditions, necessitating early and accurate diagnosis. Government initiatives aimed at improving healthcare infrastructure and promoting the adoption of advanced medical technologies across the region are also playing a crucial role. Furthermore, rising disposable incomes and a growing awareness among the population regarding the importance of early disease detection are boosting demand for sophisticated diagnostic solutions. The influx of investments from both public and private sectors into healthcare innovation further fuels research and development, leading to continuous technological advancements and product improvements in optical imaging.

Obstacles in the Middle-East and Africa Optical Imaging Industry Market

Despite its promising growth, the MEA Optical Imaging Industry faces several obstacles. High initial procurement costs of advanced optical imaging systems can be a significant barrier, particularly for smaller healthcare facilities or in less economically developed regions. The availability of skilled healthcare professionals trained to operate and interpret data from these complex technologies is also a concern, necessitating substantial investment in training programs. Furthermore, varying regulatory frameworks across different countries within the MEA region can create complexities in market access and product registration. Supply chain disruptions, geopolitical instability in certain areas, and limited reimbursement policies for advanced diagnostic procedures also pose challenges to widespread adoption.

Future Opportunities in Middle-East and Africa Optical Imaging Industry

The MEA Optical Imaging Industry is ripe with future opportunities. The untapped potential of many African nations presents a significant avenue for market expansion, especially with the development of more affordable and portable optical imaging devices. Growing interest in personalized medicine and precision diagnostics will drive demand for advanced technologies like Hyperspectral Imaging and Photoacoustic Tomography. The increasing focus on early disease detection in Oncology and Cardiology will open up new avenues for innovative imaging solutions. Strategic collaborations between technology providers and healthcare institutions, along with supportive government policies, will further unlock growth potential, particularly in emerging markets within the region.

Major Players in the Middle-East and Africa Optical Imaging Industry Ecosystem

- Headwall Photonics Inc

- Canon Inc

- Carl Zeiss Meditec AG

- Heidelberg Engineering Inc

- Leica Microsystems

- Cytoviva Inc

- Topcon Corporation

- Optovue Inc

- Bioptigen Inc

- Abbott Laboratories

- Perkinelmer Inc

- ChemImage Corporation

Key Developments in Middle-East and Africa Optical Imaging Industry Industry

- November 2021: MedX Health Corp. and Al Zahrawi Medical Supplies LLC signed a Memorandum of Understanding on a two-phase commercialization pilot and distribution agreement for MedX's leading-edge DermSecure Screening Platform at select United Arab Emirates oncology and dermatology clinics.

- October 2021: The Barraquer opened its new clinic in Dubai with the latest technology, and seven senior ophthalmologists trained at the Barcelona clinic provide top-quality care. Located in the Dubai Healthcare City 2 medical complex in the Emirati city, the new hospital is a six-story building measuring 13,000 m2.

Strategic Middle-East and Africa Optical Imaging Industry Market Forecast

The strategic forecast for the MEA Optical Imaging Industry points towards robust growth, driven by escalating healthcare investments and the increasing demand for advanced diagnostic tools. The expanding applications in Ophthalmology, Oncology, and Cardiology will continue to be key growth catalysts. Investments in new technologies such as Photoacoustic Tomography and further refinement of existing modalities like Optical Coherence Tomography are expected to unlock new market segments. The strategic emphasis on improving healthcare accessibility and quality across the region, coupled with supportive regulatory environments, will foster a conducive ecosystem for market expansion, anticipating significant revenue growth in the coming years.

Middle-East and Africa Optical Imaging Industry Segmentation

-

1. Technology

- 1.1. Photoacoustic Tomography

- 1.2. Optical Coherence Tomography

- 1.3. Hyperspectral Imaging

- 1.4. Near-Infrared Spectroscopy

- 1.5. Other Technologies

-

2. Product

- 2.1. Imaging Systems

- 2.2. Illumination Systems

- 2.3. Optical Imaging Software

- 2.4. Cameras

- 2.5. Other Products

-

3. Application Area

- 3.1. Ophthalmology

- 3.2. Oncology

- 3.3. Cardiology

- 3.4. Dermatology

- 3.5. Neurology

- 3.6. Other Application Areas

-

4. Application

- 4.1. Pathological Imaging

- 4.2. Intraoperative Imaging

-

5. End-user Industry

- 5.1. Hospitals and Clinics

- 5.2. Research and Diagnostic Laboratories

- 5.3. Pharmaceutical Industry

- 5.4. Biotechnology Companies

- 5.5. Other End-user Industries

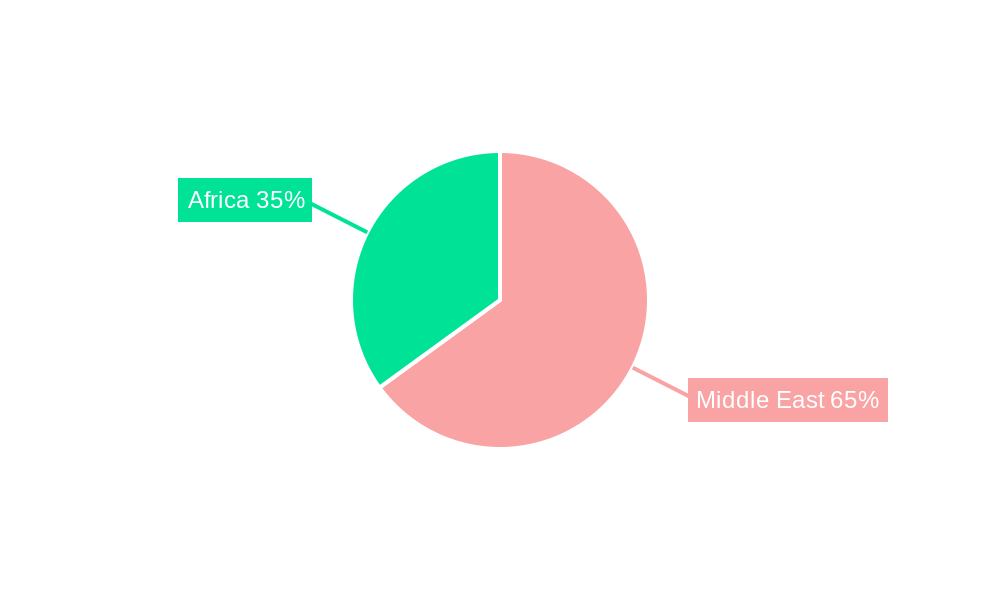

Middle-East and Africa Optical Imaging Industry Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle-East and Africa Optical Imaging Industry Regional Market Share

Geographic Coverage of Middle-East and Africa Optical Imaging Industry

Middle-East and Africa Optical Imaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Photoacoustic Tomography

- 5.1.2. Optical Coherence Tomography

- 5.1.3. Hyperspectral Imaging

- 5.1.4. Near-Infrared Spectroscopy

- 5.1.5. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Imaging Systems

- 5.2.2. Illumination Systems

- 5.2.3. Optical Imaging Software

- 5.2.4. Cameras

- 5.2.5. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Application Area

- 5.3.1. Ophthalmology

- 5.3.2. Oncology

- 5.3.3. Cardiology

- 5.3.4. Dermatology

- 5.3.5. Neurology

- 5.3.6. Other Application Areas

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Pathological Imaging

- 5.4.2. Intraoperative Imaging

- 5.5. Market Analysis, Insights and Forecast - by End-user Industry

- 5.5.1. Hospitals and Clinics

- 5.5.2. Research and Diagnostic Laboratories

- 5.5.3. Pharmaceutical Industry

- 5.5.4. Biotechnology Companies

- 5.5.5. Other End-user Industries

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Middle-East and Africa Optical Imaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Photoacoustic Tomography

- 6.1.2. Optical Coherence Tomography

- 6.1.3. Hyperspectral Imaging

- 6.1.4. Near-Infrared Spectroscopy

- 6.1.5. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Imaging Systems

- 6.2.2. Illumination Systems

- 6.2.3. Optical Imaging Software

- 6.2.4. Cameras

- 6.2.5. Other Products

- 6.3. Market Analysis, Insights and Forecast - by Application Area

- 6.3.1. Ophthalmology

- 6.3.2. Oncology

- 6.3.3. Cardiology

- 6.3.4. Dermatology

- 6.3.5. Neurology

- 6.3.6. Other Application Areas

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Pathological Imaging

- 6.4.2. Intraoperative Imaging

- 6.5. Market Analysis, Insights and Forecast - by End-user Industry

- 6.5.1. Hospitals and Clinics

- 6.5.2. Research and Diagnostic Laboratories

- 6.5.3. Pharmaceutical Industry

- 6.5.4. Biotechnology Companies

- 6.5.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Headwall Photonics Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Canon Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Carl Zeiss Meditec AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Heidelberg Engineering Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Leica Microsystems

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cytoviva Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Topcon Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Optovue Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Bioptigen Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Abbott Laboratories

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Perkinelmer Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 ChemImage Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Headwall Photonics Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle-East and Africa Optical Imaging Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Middle-East and Africa Optical Imaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 3: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 4: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 5: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Application Area 2020 & 2033

- Table 6: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Application Area 2020 & 2033

- Table 7: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 9: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 10: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 11: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 12: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 13: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 14: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 15: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 16: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 17: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Application Area 2020 & 2033

- Table 18: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Application Area 2020 & 2033

- Table 19: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 21: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 22: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 23: Middle-East and Africa Optical Imaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Middle-East and Africa Optical Imaging Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Saudi Arabia Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Saudi Arabia Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Arab Emirates Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: United Arab Emirates Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Israel Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Israel Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Qatar Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Qatar Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Kuwait Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Kuwait Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Oman Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Oman Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Bahrain Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Bahrain Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Jordan Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Jordan Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Lebanon Middle-East and Africa Optical Imaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Lebanon Middle-East and Africa Optical Imaging Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle-East and Africa Optical Imaging Industry?

The projected CAGR is approximately 6.62%.

2. Which companies are prominent players in the Middle-East and Africa Optical Imaging Industry?

Key companies in the market include Headwall Photonics Inc, Canon Inc, Carl Zeiss Meditec AG, Heidelberg Engineering Inc, Leica Microsystems, Cytoviva Inc, Topcon Corporation, Optovue Inc, Bioptigen Inc, Abbott Laboratories, Perkinelmer Inc, ChemImage Corporation.

3. What are the main segments of the Middle-East and Africa Optical Imaging Industry?

The market segments include Technology, Product, Application Area, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.64 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Eye diseases such as dry eyes in MENA region; High Demand from Professional Services in Healthcare.

6. What are the notable trends driving market growth?

Ophthalmology to Show Significant Growth.

7. Are there any restraints impacting market growth?

Competition from Other Substitutes.

8. Can you provide examples of recent developments in the market?

November 2021 - MedX Health Corp. and Al Zahrawi Medical Supplies LLC signed a Memorandum of Understanding between the companies on a two-phase commercialization pilot and distribution agreement for MedX's leading-edge DermSecure Screening Platform at select United Arab Emirates oncology and dermatology clinics beginning this month.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle-East and Africa Optical Imaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle-East and Africa Optical Imaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle-East and Africa Optical Imaging Industry?

To stay informed about further developments, trends, and reports in the Middle-East and Africa Optical Imaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence