Key Insights

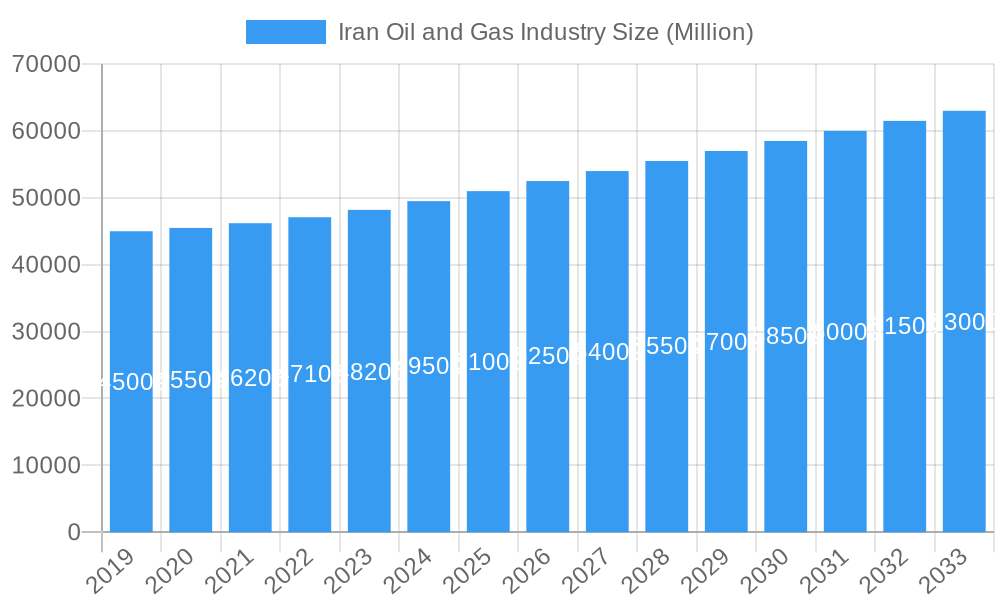

The Iran Oil and Gas Industry is projected for substantial growth, with an estimated market size of $80 billion by 2033, reflecting a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period of 2024-2033. This expansion is driven by significant upstream investments in exploration and production, leveraging Iran's extensive hydrocarbon reserves and strategic initiatives to increase output. The midstream sector, focusing on transportation and storage, is also expanding to support heightened production volumes. Key growth catalysts include government national development plans aimed at bolstering energy security and export revenue, alongside sustained global demand for oil and gas, despite the ongoing energy transition. Technological advancements in extraction and refining are enhancing operational efficiency and accessing previously untapped reserves.

Iran Oil and Gas Industry Market Size (In Billion)

The downstream sector, encompassing refining and petrochemicals, is expected to see considerable growth fueled by rising domestic and international demand for refined products and petrochemical derivatives. Trends include the expansion of petrochemical complexes to add value to crude oil and gas, alongside a focus on advanced lubricants and specialty chemicals. While rich resources and strategic location are advantageous, potential challenges include geopolitical uncertainties, sanctions affecting investment and technology, and the global shift towards cleaner energy. Leading companies such as Pars Oil Company, National Petrochemical Company, Iranol Oil Company, National Iranian Oil Company, and National Iranian Oil Refining and Distribution Company are spearheading innovation and expansion across the value chain.

Iran Oil and Gas Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Iran Oil and Gas Industry's market composition, trends, and future outlook. Covering the period from 2019 to 2033, with a base year of 2024 and a forecast period of 2025-2033, this research offers critical insights for stakeholders in the dynamic Iranian energy sector. Optimized for search engines with keywords such as Iran oil and gas, Iranian energy sector, petrochemical industry Iran, and oil refining Iran, this report aims to enhance visibility and engagement for decision-makers.

Iran Oil and Gas Industry Market Composition & Trends

The Iran oil and gas industry is characterized by a significant level of market concentration, with key national entities dominating production and refining. Innovation within the sector is primarily driven by the need to enhance extraction efficiency and meet evolving environmental standards. The regulatory landscape, while subject to international dynamics, plays a pivotal role in shaping investment and operational strategies. Substitute products, though emerging in the global energy mix, currently hold a limited impact on Iran's oil and gas dominance. End-user profiles range from domestic industrial consumers to international export markets. Merger and acquisition (M&A) activities are typically strategic, focused on consolidating assets and expanding capabilities.

- Market Share Distribution: Dominated by National Iranian Oil Company (NIOC) and National Petrochemical Company (NPC) for exploration, production, and downstream processing.

- M&A Deal Values: Focused on domestic consolidation and capacity expansion, with significant investments in refinery upgrades and petrochemical plant construction.

- Innovation Catalysts: Driven by technological upgrades for enhanced recovery, gas processing, and the development of specialized petrochemical products.

- Regulatory Landscapes: Heavily influenced by government policies, international sanctions, and national energy security objectives.

- End-User Profiles: Includes a broad spectrum from domestic power generation and industrial manufacturing to international export markets for crude oil, refined products, and petrochemicals.

Iran Oil and Gas Industry Industry Evolution

The Iran oil and gas industry has witnessed a compelling evolution marked by ambitious development plans and strategic investments aimed at bolstering both production capacity and value-added processing. Throughout the historical period of 2019–2024, the sector has focused on maintaining and optimizing existing infrastructure while laying the groundwork for future expansion. Market growth trajectories have been influenced by global energy demand and geopolitical factors. Technological advancements are continuously being integrated, particularly in the upstream segment to improve extraction rates from mature fields and in the downstream sector for producing higher-value products. Shifting consumer demands, both domestically and internationally, are prompting a greater emphasis on cleaner fuels and specialized petrochemicals. The industry's journey reflects a strategic push towards greater self-sufficiency and enhanced export competitiveness, with a clear roadmap for the forecast period.

Leading Regions, Countries, or Segments in Iran Oil and Gas Industry

The Upstream segment stands as the most dominant force within the Iran oil and gas industry, underpinned by the nation's vast hydrocarbon reserves. This dominance is fueled by strategic investments in exploration and production activities, coupled with a supportive regulatory framework designed to maximize resource extraction. The sheer scale of Iran's oil and gas fields necessitates continuous development and technological integration to maintain and enhance production levels.

- Upstream Dominance: Iran possesses some of the world's largest proven oil and natural gas reserves, making exploration and production the foundational pillar of its energy sector. This segment commands the largest share of investment and contributes significantly to the nation's GDP and export revenue.

- Key Drivers in Upstream:

- Investment Trends: Consistent government allocation of capital towards developing onshore and offshore fields, including significant planned investments in fields like North Pars and Kish.

- Regulatory Support: Favorable policies aimed at attracting domestic and, historically, international investment in exploration and production projects.

- Technological Advancements: Adoption of enhanced oil recovery (EOR) techniques and advanced drilling technologies to optimize output from existing and new reserves.

- Geological Advantages: The presence of large, prolific hydrocarbon reservoirs provides a natural advantage for upstream dominance.

While Midstream and Downstream segments are crucial for value chain integration, the sheer magnitude of Iran's reserves and the primary focus on extracting these resources firmly place Upstream at the forefront of the industry's overall significance and economic impact. The nation's commitment to expanding gas production capacity, as evidenced by the planned USD 11 billion investment in offshore fields, further solidifies the strategic importance of the Upstream segment.

Iran Oil and Gas Industry Product Innovations

Product innovations in the Iran oil and gas industry are increasingly focused on enhancing the value chain and meeting evolving market demands. This includes the development of specialized petrochemicals with higher purity and specific application characteristics, catering to industries such as plastics, fertilizers, and synthetic fibers. In the refining sector, advancements are aimed at producing cleaner fuels and maximizing the yield of high-value distillates. For instance, efforts to increase refinery production by one million liters per day, as announced by the Lavan Refinery, signify a push towards greater output efficiency and product diversification.

Propelling Factors for Iran Oil and Gas Industry Growth

Several key factors are propelling the growth of the Iran oil and gas industry. Technologically, the ongoing development and application of enhanced oil recovery (EOR) techniques are crucial for maximizing output from mature fields. Economically, the nation's vast reserves present a significant opportunity for both domestic energy security and export revenue generation. Regulatory influences, such as government incentives for investment in upstream and downstream projects, further stimulate expansion. The planned USD 11 billion investment to raise gas production capacity by 240 million cubic meters/day, particularly in offshore fields like North Pars and Kish, exemplifies this growth-driving commitment.

Obstacles in the Iran Oil and Gas Industry Market

The Iran oil and gas industry faces several significant obstacles. International sanctions continue to pose a considerable challenge, impacting access to foreign technology, capital, and export markets. Supply chain disruptions, often exacerbated by geopolitical tensions, can hinder the timely procurement of essential equipment and services. Regulatory complexities, while aimed at national benefit, can sometimes create barriers to entry and investment. Furthermore, the global push towards renewable energy presents a long-term competitive pressure that the sector must strategically address.

Future Opportunities in Iran Oil and Gas Industry

Emerging opportunities for the Iran oil and gas industry lie in expanding petrochemical production to capture higher value, developing advanced refining capabilities for cleaner fuels, and leveraging its vast gas reserves to meet growing regional and international energy demands. The development of new gas fields and the optimization of existing infrastructure present significant potential. Furthermore, exploring opportunities in niche petrochemical markets and investing in cleaner energy technologies can diversify revenue streams and enhance market resilience.

Major Players in the Iran Oil and Gas Industry Ecosystem

- Pars Oil Company

- National Petrochemical Company

- Iranol Oil Company

- National Iranian Oil Company

- National Iranian Oil Refining and Distribution Company

Key Developments in Iran Oil and Gas Industry Industry

- January 2022: Lavan Refinery announces the construction of a 150,000-barrel petro-refinery, alongside efforts to increase the refinery's daily production by one million liters, impacting downstream capacity and product availability.

- November 2021: Iran plans a USD 11 billion investment to boost offshore gas production capacity by 240 million cubic meters/day. This includes USD 4 billion for the North Pars field and funds for the Kish gas field, Phase 11 of South Pars, and onshore fields of the Iranian Central Oil Fields Company, significantly enhancing upstream gas reserves and future supply.

Strategic Iran Oil and Gas Industry Market Forecast

The strategic forecast for the Iran oil and gas industry is one of sustained growth, driven by substantial investments in upstream development and downstream value addition. The planned expansion of gas production capacity, particularly in offshore fields, and the construction of new refining facilities signal a robust outlook for increased output and product diversification. By focusing on technological upgrades and capitalizing on its immense hydrocarbon reserves, the industry is poised to strengthen its position in both domestic and international energy markets, contributing significantly to economic development through 2033.

Iran Oil and Gas Industry Segmentation

- 1. Upstream

- 2. Midstream

- 3. Downstream

Iran Oil and Gas Industry Segmentation By Geography

- 1. Iran

Iran Oil and Gas Industry Regional Market Share

Geographic Coverage of Iran Oil and Gas Industry

Iran Oil and Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Upstream

- 5.2. Market Analysis, Insights and Forecast - by Midstream

- 5.3. Market Analysis, Insights and Forecast - by Downstream

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Iran

- 6. Iran Oil and Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Upstream

- 6.2. Market Analysis, Insights and Forecast - by Midstream

- 6.3. Market Analysis, Insights and Forecast - by Downstream

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pars Oil Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 National Petrochemical Company

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Iranol Oil Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 National Iranian Oil Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 National Iranian Oil Refining and Distribution Company*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Pars Oil Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Iran Oil and Gas Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Iran Oil and Gas Industry Share (%) by Company 2025

List of Tables

- Table 1: Iran Oil and Gas Industry Revenue billion Forecast, by Upstream 2020 & 2033

- Table 2: Iran Oil and Gas Industry Volume Tonnes Forecast, by Upstream 2020 & 2033

- Table 3: Iran Oil and Gas Industry Revenue billion Forecast, by Midstream 2020 & 2033

- Table 4: Iran Oil and Gas Industry Volume Tonnes Forecast, by Midstream 2020 & 2033

- Table 5: Iran Oil and Gas Industry Revenue billion Forecast, by Downstream 2020 & 2033

- Table 6: Iran Oil and Gas Industry Volume Tonnes Forecast, by Downstream 2020 & 2033

- Table 7: Iran Oil and Gas Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Iran Oil and Gas Industry Volume Tonnes Forecast, by Region 2020 & 2033

- Table 9: Iran Oil and Gas Industry Revenue billion Forecast, by Upstream 2020 & 2033

- Table 10: Iran Oil and Gas Industry Volume Tonnes Forecast, by Upstream 2020 & 2033

- Table 11: Iran Oil and Gas Industry Revenue billion Forecast, by Midstream 2020 & 2033

- Table 12: Iran Oil and Gas Industry Volume Tonnes Forecast, by Midstream 2020 & 2033

- Table 13: Iran Oil and Gas Industry Revenue billion Forecast, by Downstream 2020 & 2033

- Table 14: Iran Oil and Gas Industry Volume Tonnes Forecast, by Downstream 2020 & 2033

- Table 15: Iran Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Iran Oil and Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Iran Oil and Gas Industry?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Iran Oil and Gas Industry?

Key companies in the market include Pars Oil Company, National Petrochemical Company, Iranol Oil Company, National Iranian Oil Company, National Iranian Oil Refining and Distribution Company*List Not Exhaustive.

3. What are the main segments of the Iran Oil and Gas Industry?

The market segments include Upstream, Midstream, Downstream.

4. Can you provide details about the market size?

The market size is estimated to be USD 80 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Abundant Oil and Gas Reserves4.; Favorable Investment in Upstream Sector.

6. What are the notable trends driving market growth?

Upstream Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Volatility of Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

In January 2022, the Lavan Refinery, in the south of Iran, announced the construction of a 150,000-barrel petro-refinery next to the Lavan Refinery and its efforts to increase the refinery's production by one million liters per day.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Iran Oil and Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Iran Oil and Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Iran Oil and Gas Industry?

To stay informed about further developments, trends, and reports in the Iran Oil and Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence