Key Insights

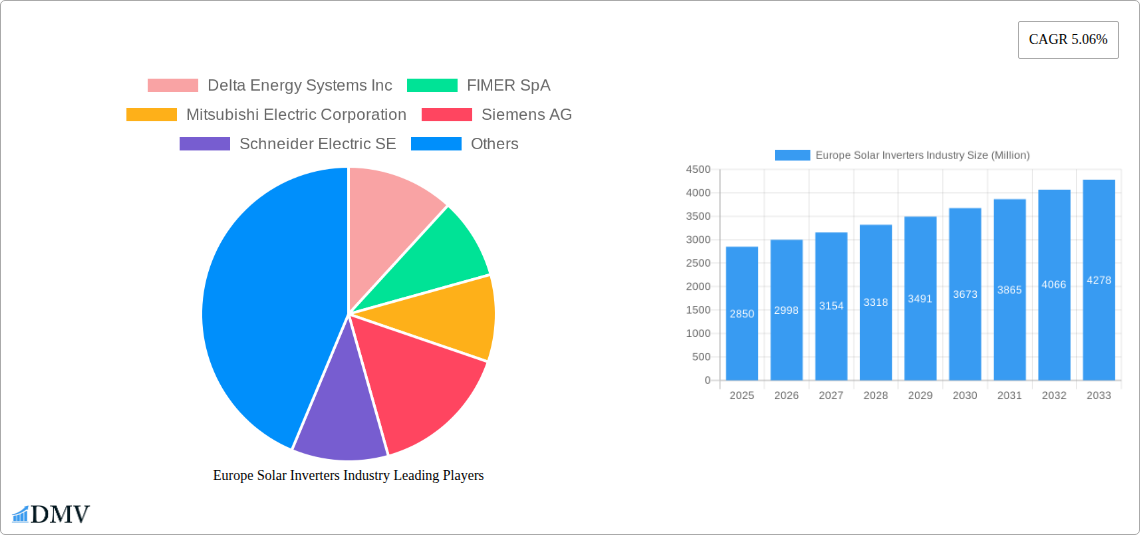

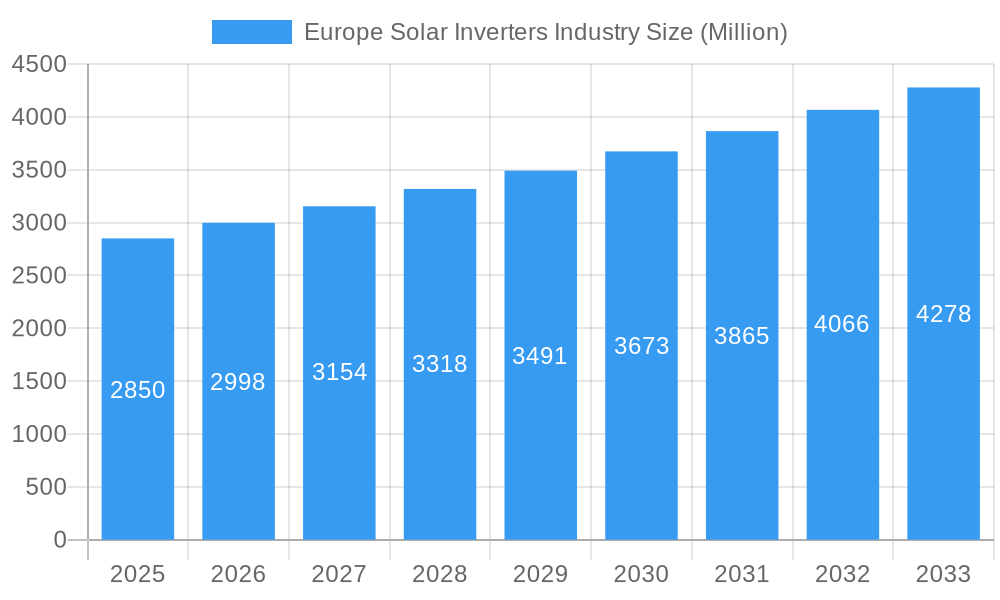

The European solar inverter market, valued at €2.85 billion in 2025, is projected to experience robust growth, driven by the increasing adoption of renewable energy sources across residential, commercial, and industrial sectors. A Compound Annual Growth Rate (CAGR) of 5.06% from 2025 to 2033 indicates a significant expansion of this market. Key drivers include supportive government policies promoting solar energy, decreasing solar panel costs making solar power more affordable, and rising energy prices incentivizing self-generation. String inverters currently dominate the market due to their cost-effectiveness and suitability for various applications. However, microinverters are gaining traction, especially in residential settings, due to their improved performance and safety features. The market is segmented by inverter type (central, string, micro) and application (residential, commercial & industrial, utility-scale), with the residential segment witnessing particularly strong growth. Germany, France, Italy, and the UK represent the largest national markets within Europe, fueled by strong renewable energy targets and favorable regulatory frameworks. Competitive landscape analysis reveals key players like Delta Energy Systems, FIMER, Mitsubishi Electric, Siemens, Schneider Electric, Omron, KACO, Huawei, General Electric, and SMA Solar Technology vying for market share through technological innovation and strategic partnerships. While supply chain constraints and potential fluctuations in raw material prices pose some challenges, the long-term outlook for the European solar inverter market remains positive, driven by the escalating demand for clean energy solutions and the continent's commitment to carbon neutrality. The increasing adoption of smart grid technologies further enhances market growth by providing optimized energy management and efficient grid integration.

Europe Solar Inverters Industry Market Size (In Billion)

The forecast period from 2025 to 2033 will likely witness significant changes in market dynamics. We anticipate continued growth in microinverter adoption, potentially impacting the market share of string inverters. The utility-scale segment is expected to expand significantly, driven by large-scale solar power plant installations aimed at meeting national renewable energy targets. Technological advancements, such as higher efficiency inverters and improved grid integration capabilities, will play a crucial role in shaping the market. Furthermore, the increasing integration of energy storage systems with solar inverters is anticipated to stimulate market expansion, enhancing energy security and grid stability. Competition among manufacturers will remain fierce, with companies focusing on product differentiation, cost reduction, and strategic partnerships to gain a competitive edge. Regional variations in growth rates will reflect differences in government policies, energy consumption patterns, and the level of solar energy adoption.

Europe Solar Inverters Industry Company Market Share

Europe Solar Inverters Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a comprehensive analysis of the Europe solar inverters industry, offering crucial data and forecasts for stakeholders seeking to navigate this dynamic market. With a focus on market trends, leading players, and future opportunities, this report is an invaluable resource for strategic decision-making. The study period covers 2019-2033, with 2025 as the base and estimated year.

Europe Solar Inverters Industry Market Composition & Trends

This section delves into the intricate composition of the European solar inverter market, analyzing its concentration, innovation drivers, regulatory landscape, substitute products, end-user profiles, and mergers and acquisitions (M&A) activity. The market is characterized by a moderately concentrated landscape with key players such as SMA Solar Technology AG, Huawei Technologies Co Ltd, and Schneider Electric SE holding significant shares. However, numerous smaller players contribute to a competitive environment.

- Market Concentration: The top 6 players hold an estimated xx% market share in 2025, indicating a moderately concentrated market.

- Innovation Catalysts: Stringent efficiency standards and the rising demand for higher power output inverters drive innovation in areas like multi-MPPT technology and improved grid integration.

- Regulatory Landscape: EU directives concerning renewable energy integration and grid stability significantly influence inverter designs and certifications.

- Substitute Products: While currently limited, advancements in power electronics could potentially introduce alternative technologies in the future.

- End-User Profiles: The market comprises residential, commercial & industrial, and utility-scale segments, with utility-scale installations driving significant volume growth.

- M&A Activity: The estimated value of M&A deals in the European solar inverter market between 2019 and 2024 totaled approximately xx Million, driven by strategic expansion and technology acquisition.

Europe Solar Inverters Industry Industry Evolution

This section charts the evolution of the European solar inverter industry, examining its growth trajectory, technological advancements, and the shifting demands of consumers. The market experienced robust growth from 2019 to 2024, with a CAGR of approximately xx%. This growth is primarily attributed to the increasing adoption of renewable energy sources across Europe, fueled by government incentives and the declining cost of solar PV systems. Technological advancements, such as the development of higher efficiency inverters and smart grid integration capabilities, have further propelled market expansion. Consumer demand is shifting towards higher-power, more efficient, and easily integrable inverters. The forecast period (2025-2033) projects a CAGR of approximately xx%, driven by sustained growth in solar PV installations and continued technological advancements.

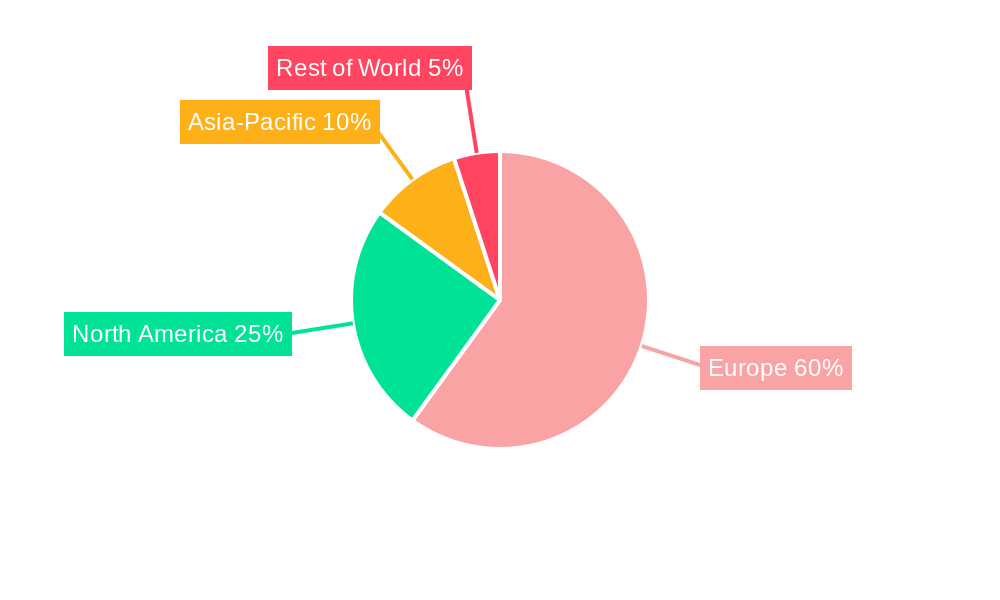

Leading Regions, Countries, or Segments in Europe Solar Inverters Industry

This section identifies the dominant regions, countries, and segments within the European solar inverter market. While precise market share data varies across segments and years, several factors contribute to regional and segment dominance.

Dominant Segments:

- Inverter Type: String inverters currently dominate the market due to their cost-effectiveness and suitability for a wide range of applications. However, microinverters are experiencing significant growth in the residential sector.

- Application: The utility-scale segment is anticipated to maintain its leading position due to large-scale solar projects across the continent. The commercial and industrial segment is also exhibiting strong growth.

Key Drivers:

- Germany: Strong government support for renewable energy and a well-established solar PV industry.

- United Kingdom: Increasing investments in renewable energy projects and supportive government policies.

- Italy: Significant growth in residential solar installations, driving demand for string and microinverters.

- France: Growing adoption of solar PV in the commercial and industrial sector.

The dominance of these regions and segments is driven by a combination of factors, including supportive government policies, favorable investment climates, and strong market acceptance of solar PV technology.

Europe Solar Inverters Industry Product Innovations

Recent years have witnessed significant product innovations in the European solar inverter market. Key advancements include the integration of advanced power electronics for higher efficiency, enhanced grid management features for improved stability, and improved monitoring and control capabilities via smart interfaces and remote diagnostics. Manufacturers are focusing on increasing power density, reducing system costs, and improving ease of installation. The introduction of modular designs and plug-and-play features enhances installation flexibility and reduces installation time. Unique selling propositions increasingly center on smart features, digital services, and enhanced warranty provisions.

Propelling Factors for Europe Solar Inverters Industry Growth

Several factors contribute to the growth of the European solar inverter industry. These include the increasing adoption of renewable energy sources, driven by climate change concerns and government incentives such as feed-in tariffs and tax credits. Technological advancements leading to higher efficiency and cost reductions in solar inverters are also key drivers. Furthermore, supportive government regulations and policies promoting renewable energy integration are significantly contributing to market expansion.

Obstacles in the Europe Solar Inverters Industry Market

Despite significant growth potential, the European solar inverter market faces challenges. Supply chain disruptions, especially the availability of key components like semiconductors, can lead to production delays and increased costs. Intense competition among manufacturers creates price pressures. Regulatory hurdles, including variations in grid codes across different European countries, also pose challenges for manufacturers and installers.

Future Opportunities in Europe Solar Inverters Industry

The European solar inverter market presents several promising opportunities. The rising demand for energy storage systems coupled with solar PV offers significant growth potential for inverters with integrated battery management capabilities. Advancements in artificial intelligence and machine learning provide opportunities for smart inverters that optimize energy production and grid integration. Expansion into emerging markets within Europe and the integration of inverters with other smart home technologies also represent lucrative avenues for growth.

Major Players in the Europe Solar Inverters Industry Ecosystem

- Delta Energy Systems Inc

- FIMER SpA

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Omron Corporation

- KACO New Energy GmbH

- Huawei Technologies Co Ltd

- General Electric Company

- SMA Solar Technology AG

Key Developments in Europe Solar Inverters Industry Industry

- June 2022: SMA Solar Technology AG announced plans to build a new gigawatt solar inverter manufacturing facility in Niestetal, Germany, aiming to double its production capacity from 21GW to 40GW by 2024. This significantly expands production capacity and strengthens SMA's market position.

- April 2022: SMA Solar Technology AG launched four new Sunny Tripower-X solar inverter models (12kW, 15kW, 20kW, and 25kW) for commercial and residential use, featuring enhanced features like an exclusive system manager, three independent MPP trackers, and six-string inputs. This strengthens their product portfolio and enhances competitiveness.

Strategic Europe Solar Inverters Industry Market Forecast

The European solar inverter market is poised for sustained growth over the forecast period (2025-2033), driven by the expanding solar PV market, supportive government policies, and ongoing technological advancements. The increasing adoption of larger-scale solar projects and the integration of energy storage solutions are expected to drive demand for high-power inverters and inverters with enhanced grid management capabilities. The market's future will be shaped by innovation in areas such as AI-powered optimization, improved grid integration, and the development of more efficient and cost-effective inverter technologies. This presents significant opportunities for established players and new entrants alike.

Europe Solar Inverters Industry Segmentation

-

1. Inverter Type

- 1.1. Central Inverters

- 1.2. String Inverters

- 1.3. Micro Inverters

-

2. Application

- 2.1. Residential

- 2.2. Commercial and Industrial

- 2.3. Utility-scale

Europe Solar Inverters Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Spain

- 5. Italy

- 6. Nordic Countries

- 7. Turkey

- 8. Russia

- 9. Rest of Europe

Europe Solar Inverters Industry Regional Market Share

Geographic Coverage of Europe Solar Inverters Industry

Europe Solar Inverters Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Inverter Type

- 5.1.1. Central Inverters

- 5.1.2. String Inverters

- 5.1.3. Micro Inverters

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential

- 5.2.2. Commercial and Industrial

- 5.2.3. Utility-scale

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Spain

- 5.3.5. Italy

- 5.3.6. Nordic Countries

- 5.3.7. Turkey

- 5.3.8. Russia

- 5.3.9. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Inverter Type

- 6. Europe Solar Inverters Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Inverter Type

- 6.1.1. Central Inverters

- 6.1.2. String Inverters

- 6.1.3. Micro Inverters

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential

- 6.2.2. Commercial and Industrial

- 6.2.3. Utility-scale

- 6.1. Market Analysis, Insights and Forecast - by Inverter Type

- 7. Germany Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Inverter Type

- 7.1.1. Central Inverters

- 7.1.2. String Inverters

- 7.1.3. Micro Inverters

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Residential

- 7.2.2. Commercial and Industrial

- 7.2.3. Utility-scale

- 7.1. Market Analysis, Insights and Forecast - by Inverter Type

- 8. United Kingdom Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Inverter Type

- 8.1.1. Central Inverters

- 8.1.2. String Inverters

- 8.1.3. Micro Inverters

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Residential

- 8.2.2. Commercial and Industrial

- 8.2.3. Utility-scale

- 8.1. Market Analysis, Insights and Forecast - by Inverter Type

- 9. France Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Inverter Type

- 9.1.1. Central Inverters

- 9.1.2. String Inverters

- 9.1.3. Micro Inverters

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Residential

- 9.2.2. Commercial and Industrial

- 9.2.3. Utility-scale

- 9.1. Market Analysis, Insights and Forecast - by Inverter Type

- 10. Spain Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Inverter Type

- 10.1.1. Central Inverters

- 10.1.2. String Inverters

- 10.1.3. Micro Inverters

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Residential

- 10.2.2. Commercial and Industrial

- 10.2.3. Utility-scale

- 10.1. Market Analysis, Insights and Forecast - by Inverter Type

- 11. Italy Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Inverter Type

- 11.1.1. Central Inverters

- 11.1.2. String Inverters

- 11.1.3. Micro Inverters

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Residential

- 11.2.2. Commercial and Industrial

- 11.2.3. Utility-scale

- 11.1. Market Analysis, Insights and Forecast - by Inverter Type

- 12. Nordic Countries Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Inverter Type

- 12.1.1. Central Inverters

- 12.1.2. String Inverters

- 12.1.3. Micro Inverters

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Residential

- 12.2.2. Commercial and Industrial

- 12.2.3. Utility-scale

- 12.1. Market Analysis, Insights and Forecast - by Inverter Type

- 13. Turkey Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Inverter Type

- 13.1.1. Central Inverters

- 13.1.2. String Inverters

- 13.1.3. Micro Inverters

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Residential

- 13.2.2. Commercial and Industrial

- 13.2.3. Utility-scale

- 13.1. Market Analysis, Insights and Forecast - by Inverter Type

- 14. Russia Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Inverter Type

- 14.1.1. Central Inverters

- 14.1.2. String Inverters

- 14.1.3. Micro Inverters

- 14.2. Market Analysis, Insights and Forecast - by Application

- 14.2.1. Residential

- 14.2.2. Commercial and Industrial

- 14.2.3. Utility-scale

- 14.1. Market Analysis, Insights and Forecast - by Inverter Type

- 15. Rest of Europe Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 15.1. Market Analysis, Insights and Forecast - by Inverter Type

- 15.1.1. Central Inverters

- 15.1.2. String Inverters

- 15.1.3. Micro Inverters

- 15.2. Market Analysis, Insights and Forecast - by Application

- 15.2.1. Residential

- 15.2.2. Commercial and Industrial

- 15.2.3. Utility-scale

- 15.1. Market Analysis, Insights and Forecast - by Inverter Type

- 16. Competitive Analysis

- 16.1. Company Profiles

- 16.1.1 Delta Energy Systems Inc

- 16.1.1.1. Company Overview

- 16.1.1.2. Products

- 16.1.1.3. Company Financials

- 16.1.1.4. SWOT Analysis

- 16.1.2 FIMER SpA

- 16.1.2.1. Company Overview

- 16.1.2.2. Products

- 16.1.2.3. Company Financials

- 16.1.2.4. SWOT Analysis

- 16.1.3 Mitsubishi Electric Corporation

- 16.1.3.1. Company Overview

- 16.1.3.2. Products

- 16.1.3.3. Company Financials

- 16.1.3.4. SWOT Analysis

- 16.1.4 Siemens AG

- 16.1.4.1. Company Overview

- 16.1.4.2. Products

- 16.1.4.3. Company Financials

- 16.1.4.4. SWOT Analysis

- 16.1.5 Schneider Electric SE

- 16.1.5.1. Company Overview

- 16.1.5.2. Products

- 16.1.5.3. Company Financials

- 16.1.5.4. SWOT Analysis

- 16.1.6 Omron Corporation

- 16.1.6.1. Company Overview

- 16.1.6.2. Products

- 16.1.6.3. Company Financials

- 16.1.6.4. SWOT Analysis

- 16.1.7 KACO New Energy GmbH*List Not Exhaustive 6 4 Market Ranking/Share Analysi

- 16.1.7.1. Company Overview

- 16.1.7.2. Products

- 16.1.7.3. Company Financials

- 16.1.7.4. SWOT Analysis

- 16.1.8 Huawei Technologies Co Ltd

- 16.1.8.1. Company Overview

- 16.1.8.2. Products

- 16.1.8.3. Company Financials

- 16.1.8.4. SWOT Analysis

- 16.1.9 General Electric Company

- 16.1.9.1. Company Overview

- 16.1.9.2. Products

- 16.1.9.3. Company Financials

- 16.1.9.4. SWOT Analysis

- 16.1.10 SMA Solar Technology AG

- 16.1.10.1. Company Overview

- 16.1.10.2. Products

- 16.1.10.3. Company Financials

- 16.1.10.4. SWOT Analysis

- 16.1.1 Delta Energy Systems Inc

- 16.2. Market Entropy

- 16.2.1 Company's Key Areas Served

- 16.2.2 Recent Developments

- 16.3. Company Market Share Analysis 2025

- 16.3.1 Top 5 Companies Market Share Analysis

- 16.3.2 Top 3 Companies Market Share Analysis

- 16.4. List of Potential Customers

- 17. Research Methodology

List of Figures

- Figure 1: Europe Solar Inverters Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Solar Inverters Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 2: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 3: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Europe Solar Inverters Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Solar Inverters Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 8: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 9: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 14: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 15: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 17: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 20: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 21: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 23: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 26: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 27: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 32: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 33: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 35: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 38: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 39: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 44: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 45: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 46: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 47: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 49: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 50: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 51: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 52: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 53: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 54: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 55: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 56: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 57: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 58: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 59: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Solar Inverters Industry?

The projected CAGR is approximately 5.06%.

2. Which companies are prominent players in the Europe Solar Inverters Industry?

Key companies in the market include Delta Energy Systems Inc, FIMER SpA, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, Omron Corporation, KACO New Energy GmbH*List Not Exhaustive 6 4 Market Ranking/Share Analysi, Huawei Technologies Co Ltd, General Electric Company, SMA Solar Technology AG.

3. What are the main segments of the Europe Solar Inverters Industry?

The market segments include Inverter Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.85 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Initiatives4.; Investment in Electrification Using Solar Energy.

6. What are the notable trends driving market growth?

Central Inverters Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Lack of General Awareness. Infrastructure Development Costs. and Recent Subsidy Cuts on Solar Panels.

8. Can you provide examples of recent developments in the market?

June 2022: SMA Solar Technology AG announced plans to build a solar inverter manufacturing facility in Niestetal, Germany. The new gigawatt factory is a part of the company’s target to double the production capacity from 21GW (present) to 40GW by 2024. The construction was expected to begin by the end of 2022.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Solar Inverters Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Solar Inverters Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Solar Inverters Industry?

To stay informed about further developments, trends, and reports in the Europe Solar Inverters Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence