Key Insights

The South America Defense Aircraft Aviation Fuel Market is projected for substantial growth, expected to surpass $12.25 billion by 2033, with a compound annual growth rate (CAGR) of 8.6%. This expansion is driven by escalating geopolitical concerns and an intensified focus on national security across the region, necessitating significant investments in defense aviation fleet modernization. Governments are prioritizing the acquisition of advanced fighter jets, transport aircraft, and surveillance platforms, requiring a consistent supply of specialized aviation fuels. The increasing demand for aerial capabilities in border patrol, disaster relief, and rapid deployment operations further fuels sustained market demand. Additionally, efforts to enhance operational readiness and extend the service life of existing aircraft, through regular fueling and maintenance, contribute to market value.

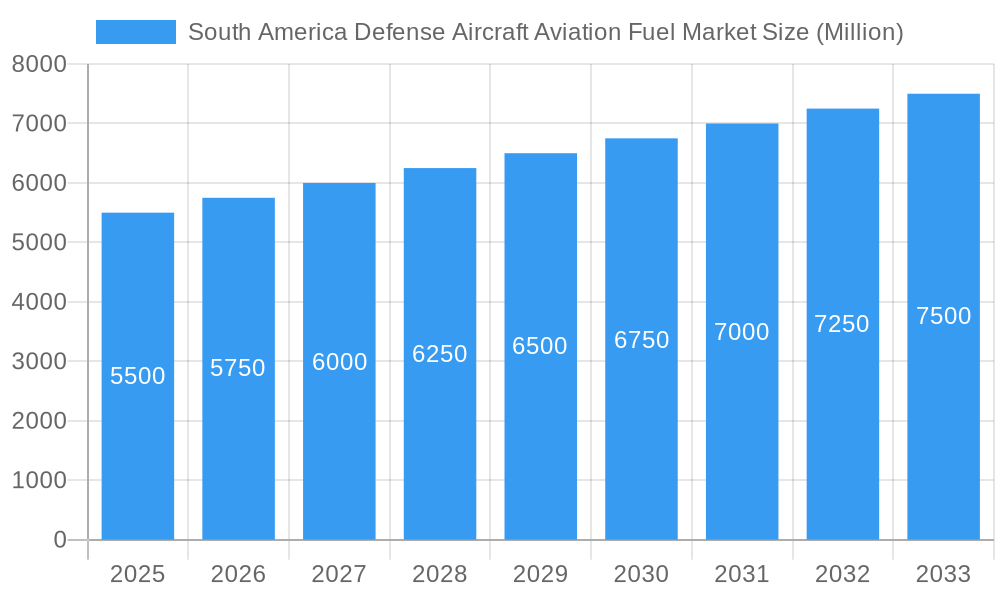

South America Defense Aircraft Aviation Fuel Market Market Size (In Billion)

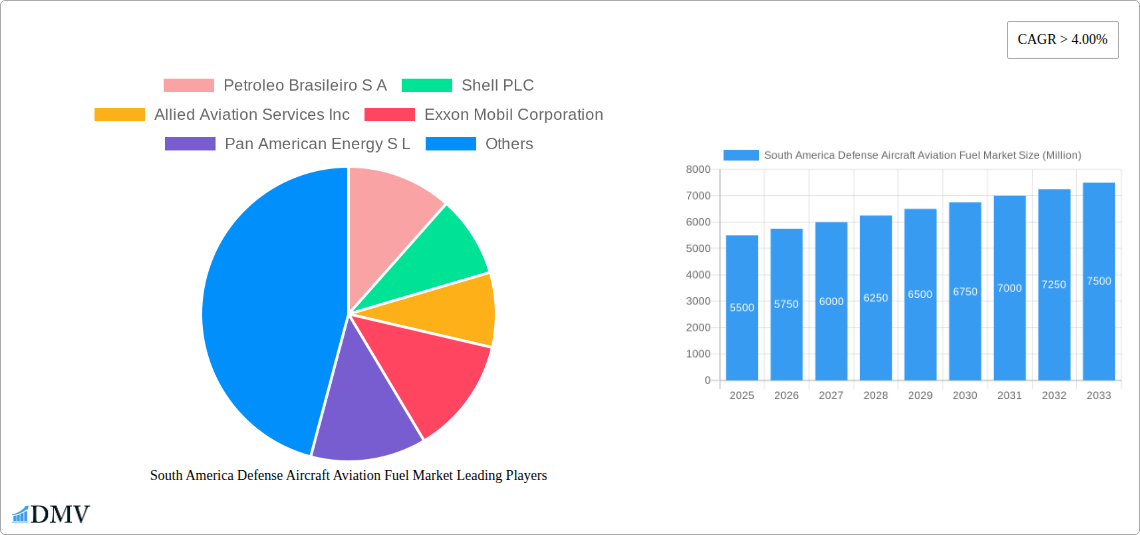

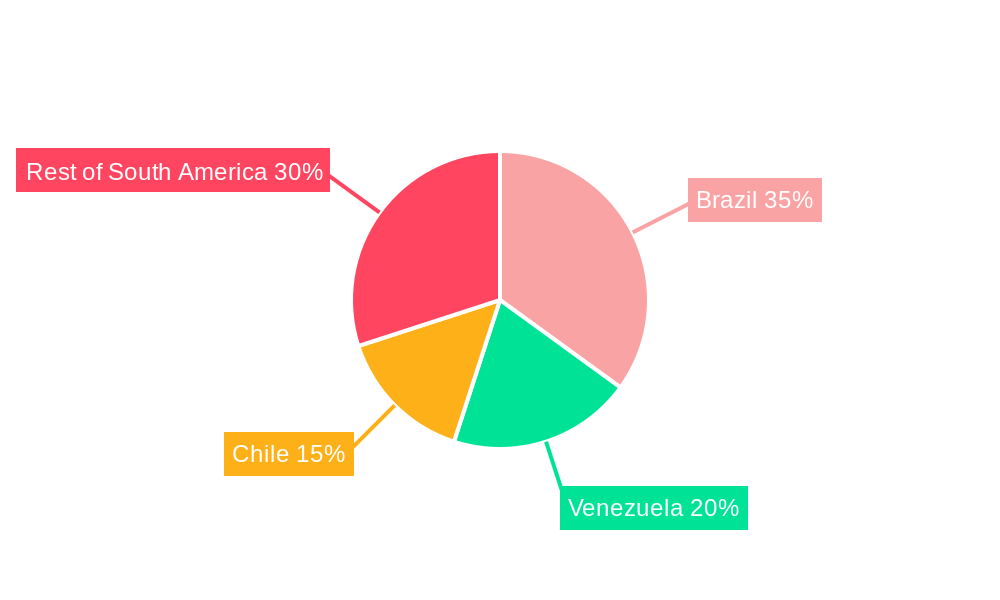

The market segmentation highlights the dominance of Air Turbine Fuel, the primary fuel for most defense aircraft. While the "Other Fuel Types" segment is smaller, it is anticipated to experience notable growth with the introduction of specialized aircraft into defense inventories. Geographically, Brazil emerges as a key market due to its substantial defense budget and extensive aerial operations. Venezuela and Chile are also significant markets, supported by ongoing defense modernization programs. The "Rest of South America" segment, including nations such as Argentina, Colombia, and Peru, collectively contributes to market growth as they invest in enhancing their aerial defense capabilities. Leading companies including Petroleo Brasileiro S.A., Shell PLC, and Exxon Mobil Corporation are strategically positioned to leverage these opportunities by optimizing supply chains and providing high-quality fuels that meet stringent defense specifications.

South America Defense Aircraft Aviation Fuel Market Company Market Share

This comprehensive report offers a definitive analysis of the South America Defense Aircraft Aviation Fuel Market, providing critical insights into its current state and future outlook. Spanning a study period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, this report is an essential resource for stakeholders seeking to understand market dynamics, growth drivers, and strategic opportunities. The analysis covers market composition, industry evolution, leading regional segments, product innovations, growth drivers, challenges, and future opportunities, all supported by robust data and expert analysis.

South America Defense Aircraft Aviation Fuel Market Market Composition & Trends

The South America Defense Aircraft Aviation Fuel Market exhibits a dynamic composition characterized by evolving regulatory frameworks and continuous innovation. Market concentration is influenced by major energy corporations and specialized aviation fuel suppliers, with significant players like Petroleo Brasileiro S.A., Shell PLC, and Exxon Mobil Corporation holding substantial sway. The drive towards greater fuel efficiency and the burgeoning interest in sustainable aviation fuels (SAF) are key innovation catalysts. Regulatory landscapes are adapting to accommodate environmental mandates and national security imperatives. Substitute products, while limited in the defense sector due to stringent performance requirements, are seeing exploration in the broader aviation context. End-user profiles are dominated by national air forces and defense ministries, with procurement decisions heavily influenced by operational readiness, cost-effectiveness, and technological superiority. Mergers and acquisition (M&A) activities, though not yet widespread, are anticipated to increase as companies seek to consolidate market presence and invest in advanced fuel technologies. The overall market share distribution is a complex interplay of established fuel providers and emerging entrants focused on specialized defense applications. M&A deal values are projected to rise as strategic partnerships form to address the increasing demand for advanced and sustainable aviation fuel solutions for defense aircraft.

South America Defense Aircraft Aviation Fuel Market Industry Evolution

The South America Defense Aircraft Aviation Fuel Market has undergone a significant evolution, driven by geopolitical shifts, technological advancements, and an increasing emphasis on national security and operational readiness. Throughout the historical period of 2019-2024, the market primarily saw steady demand for traditional jet fuels, supporting the operational needs of various South American air forces. However, the forecast period of 2025-2033 is poised for transformative changes, largely influenced by the global push towards sustainability and the modernization of defense fleets.

Market Growth Trajectories: The market's growth trajectory is intricately linked to defense budgets, regional security concerns, and the adoption of new military aircraft platforms. The increasing investment in advanced fighter jets and transport aircraft by countries like Brazil and Chile is a primary growth catalyst. Furthermore, the need for secure and reliable fuel supply chains for military operations across the vast South American continent underpins consistent demand. The estimated market size for 2025 is projected to reach xx Million, with an expected Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period, driven by these factors.

Technological Advancements: Technological advancements are playing a pivotal role in shaping the industry. The development and eventual adoption of Sustainable Aviation Fuels (SAF) are emerging as a critical trend. While initial adoption in the defense sector might be slower than in the commercial aviation space due to stringent performance and certification requirements, the long-term outlook is promising. Research and development into bio-based and synthetic fuels that can offer equivalent or superior performance to conventional jet fuels are gaining traction. Furthermore, advancements in fuel storage, logistics, and refueling technologies are enhancing operational efficiency and extending the reach of defense aircraft. The incorporation of advanced fuel management systems to optimize consumption and reduce emissions is also a key technological focus.

Shifting Consumer Demands: The "consumers" in this market, predominantly national defense ministries and air forces, are exhibiting a shift in their demands. Beyond cost and availability, there is an increasing demand for fuels that align with environmental sustainability goals, driven by international agreements and national climate action plans. The desire for enhanced operational range, reduced logistical footprint, and improved fuel efficiency in aging and new aircraft fleets is also a significant factor. Military end-users are increasingly seeking solutions that not only meet performance metrics but also contribute to decarbonization efforts and long-term energy security. The emphasis on interoperability and the ability to source fuel from diverse suppliers, including those offering greener alternatives, is also shaping procurement strategies.

Leading Regions, Countries, or Segments in South America Defense Aircraft Aviation Fuel Market

The South America Defense Aircraft Aviation Fuel Market is a multifaceted landscape, with distinct geographical regions and fuel types playing pivotal roles in its overall structure and growth. Among the geographical segments, Brazil consistently emerges as a dominant force, driven by its robust defense industry, significant military expenditure, and its strategic importance within the continent. The Brazilian Air Force (FAB), with its ambitious modernization programs and its role in regional security, presents substantial demand for aviation fuels. The recent announcement in December 2022 regarding the start of operational activities for its Gripen E fighter aircraft at the Anápolis Air Base (BAAN) underscores Brazil's commitment to advanced aerial capabilities, directly translating to sustained demand for specialized fuels.

Within the Fuel Type segmentation, Air Turbine Fuel (ATF) commands the largest share. This is directly attributable to its widespread use across the diverse fleet of defense aircraft, including fighter jets, transport planes, and helicopters operated by South American nations. The stringent performance requirements for military aviation necessitate the use of high-quality ATF that can withstand extreme operational conditions. While Other Fuel Types represent a smaller segment, their importance is growing, particularly with the increasing focus on sustainable aviation fuels (SAF). Initiatives exploring bio-kerosene and synthetic fuels are gaining momentum, driven by environmental mandates and the desire for energy independence.

Key Drivers of Dominance in Brazil:

- Defense Modernization Initiatives: Brazil's ongoing investment in modernizing its air force, including the acquisition of advanced fighter jets like the Gripen E, directly fuels demand for high-performance ATF.

- Strategic Geographic Location: Brazil's vast territory and its role as a regional power necessitate a well-equipped and operational air force, leading to consistent fuel consumption.

- Domestic Fuel Production Capacity: Petroleo Brasileiro S.A. (Petrobras) plays a significant role in supplying aviation fuels, contributing to market stability and local sourcing capabilities.

- Regulatory Support for Aviation: Government policies aimed at supporting and developing the aviation sector, including defense aviation, indirectly benefit the aviation fuel market.

While Brazil leads, other countries like Chile and Venezuela also represent significant markets. Chile's proactive approach to defense procurement and its well-trained air force contribute to a stable demand for aviation fuels. Venezuela, despite its economic challenges, maintains a substantial air force that requires ongoing fuel supplies, albeit with potential supply chain volatilities. The Rest of South America segment encompasses a collection of nations with varying defense postures and fuel demands, collectively contributing to the overall market size. The integration of these diverse markets presents a complex yet opportunity-rich environment for aviation fuel suppliers.

South America Defense Aircraft Aviation Fuel Market Product Innovations

Product innovation in the South America Defense Aircraft Aviation Fuel Market is primarily driven by the pursuit of enhanced performance, sustainability, and operational efficiency. A significant development is the research and commercialization of Sustainable Aviation Fuels (SAF). For instance, the March 2022 collaboration announced by United Airlines, Oxy Low Carbon Ventures, and Comvita Factory to commercialize SAF produced using carbon dioxide and synthetic microbes, while originating in North America, signals a global trend that will undoubtedly influence South American defense aviation. These innovative fuels aim to reduce the carbon footprint of military operations without compromising the critical performance metrics required for defense aircraft. Advancements are also focused on improving the energy density and thermal stability of existing aviation fuels to extend flight range and operational endurance. The development of more efficient fuel additive technologies to enhance engine performance and reduce wear and tear on critical components is another area of active innovation.

Propelling Factors for South America Defense Aircraft Aviation Fuel Market Growth

The South America Defense Aircraft Aviation Fuel Market is propelled by a confluence of powerful factors. Firstly, increasing defense budgets across key South American nations, driven by regional security concerns and the need for modernization, directly translates to higher demand for aviation fuels. For example, Brazil's commitment to upgrading its air force with advanced platforms like the Gripen E fighter aircraft (December 2022 FAB announcement) signifies substantial fuel requirements. Secondly, the growing emphasis on national security and border protection necessitates well-equipped and operationally ready air forces, requiring a consistent supply of aviation fuel. Thirdly, technological advancements in aircraft design are leading to more fuel-efficient engines and platforms, but also to a demand for specialized fuels that can meet the performance requirements of these advanced systems. Finally, the global push towards sustainability is gradually influencing the defense sector, creating opportunities for the introduction and adoption of Sustainable Aviation Fuels (SAF), supported by collaborations like the one between United Airlines, Oxy Low Carbon Ventures, and Comvita Factory (March 2022).

Obstacles in the South America Defense Aircraft Aviation Fuel Market Market

Despite robust growth prospects, the South America Defense Aircraft Aviation Fuel Market faces several significant obstacles. Volatility in crude oil prices can lead to unpredictable fuel costs, impacting defense budgets and procurement strategies. Supply chain disruptions, exacerbated by geopolitical instability or logistical challenges inherent in vast geographical regions, can threaten the consistent availability of fuels. Furthermore, stringent regulatory and certification processes for aviation fuels, particularly for novel SAF, can slow down their adoption in the defense sector, where performance and safety are paramount. Limited domestic production capacity for certain specialized aviation fuels in some countries can lead to increased reliance on imports, creating potential vulnerabilities. Lastly, budgetary constraints within national defense ministries can limit investment in newer, potentially more expensive, but sustainable fuel alternatives.

Future Opportunities in South America Defense Aircraft Aviation Fuel Market

The South America Defense Aircraft Aviation Fuel Market is ripe with emerging opportunities. The growing adoption of Sustainable Aviation Fuels (SAF) presents a significant avenue for growth, driven by environmental commitments and the desire for energy independence. The modernization of aging defense aircraft fleets across the continent will require significant volumes of both conventional and potentially advanced aviation fuels. The development of regional partnerships for fuel sourcing and production can mitigate supply chain risks and foster greater self-sufficiency. Furthermore, innovations in fuel logistics and infrastructure development can enhance the efficiency and reach of defense operations. The increasing focus on drones and unmanned aerial vehicles (UAVs) within defense strategies also opens up new segments for specialized fuel requirements.

Major Players in the South America Defense Aircraft Aviation Fuel Market Ecosystem

- Petroleo Brasileiro S.A.

- Shell PLC

- Allied Aviation Services Inc

- Exxon Mobil Corporation

- Pan American Energy S L

- TotalEnergies SE

- BP PLC

- Repsol SA

Key Developments in South America Defense Aircraft Aviation Fuel Market Industry

- March 2022: United Airlines, through its corporate venture capital fund, United Airlines Ventures (UAV), and Oxy Low Carbon Ventures (a subsidiary of Occidental), announced a collaboration with Houston-based biotech firm Comvita Factory to commercialize the production of sustainable aviation fuel (SAF) developed through a new process using carbon dioxide (CO2) and synthetic microbes. This development signals a global push towards SAF that will influence future supply and demand dynamics in defense aviation.

- December 2022: The Brazilian Air Force (FAB) announced the start of operational activities for its Gripen E fighter aircraft at the Anápolis Air Base (BAAN) in the country. This significant milestone indicates an increased demand for high-performance aviation fuels to support advanced fighter jet operations, contributing to market growth.

Strategic South America Defense Aircraft Aviation Fuel Market Market Forecast

The strategic forecast for the South America Defense Aircraft Aviation Fuel Market is overwhelmingly positive, driven by escalating defense modernization efforts and a burgeoning interest in sustainable solutions. Countries like Brazil are at the forefront, with initiatives like the operationalization of the Gripen E fighter aircraft in December 2022 directly translating into sustained demand for advanced aviation fuels. The global momentum towards Sustainable Aviation Fuels (SAF), as exemplified by collaborations like the one announced in March 2022 involving United Airlines, Oxy Low Carbon Ventures, and Comvita Factory, is poised to influence regional strategies, creating a significant opportunity for market players to invest in and supply greener alternatives. This shift towards sustainability, coupled with ongoing security imperatives, positions the market for robust growth and innovation throughout the forecast period.

South America Defense Aircraft Aviation Fuel Market Segmentation

-

1. Fuel Type

- 1.1. Air Turbine Fuel

- 1.2. Other Fuel Types

-

2. Geography

- 2.1. Brazil

- 2.2. Venezuela

- 2.3. Chile

- 2.4. Rest of South America

South America Defense Aircraft Aviation Fuel Market Segmentation By Geography

- 1. Brazil

- 2. Venezuela

- 3. Chile

- 4. Rest of South America

South America Defense Aircraft Aviation Fuel Market Regional Market Share

Geographic Coverage of South America Defense Aircraft Aviation Fuel Market

South America Defense Aircraft Aviation Fuel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. Air Turbine Fuel

- 5.1.2. Other Fuel Types

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. Brazil

- 5.2.2. Venezuela

- 5.2.3. Chile

- 5.2.4. Rest of South America

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Brazil

- 5.3.2. Venezuela

- 5.3.3. Chile

- 5.3.4. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. South America Defense Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. Air Turbine Fuel

- 6.1.2. Other Fuel Types

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. Brazil

- 6.2.2. Venezuela

- 6.2.3. Chile

- 6.2.4. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. Brazil South America Defense Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. Air Turbine Fuel

- 7.1.2. Other Fuel Types

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. Brazil

- 7.2.2. Venezuela

- 7.2.3. Chile

- 7.2.4. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Venezuela South America Defense Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. Air Turbine Fuel

- 8.1.2. Other Fuel Types

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. Brazil

- 8.2.2. Venezuela

- 8.2.3. Chile

- 8.2.4. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Chile South America Defense Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. Air Turbine Fuel

- 9.1.2. Other Fuel Types

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. Brazil

- 9.2.2. Venezuela

- 9.2.3. Chile

- 9.2.4. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Rest of South America South America Defense Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10.1.1. Air Turbine Fuel

- 10.1.2. Other Fuel Types

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. Brazil

- 10.2.2. Venezuela

- 10.2.3. Chile

- 10.2.4. Rest of South America

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Petroleo Brasileiro S A

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Shell PLC

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Allied Aviation Services Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Exxon Mobil Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Pan American Energy S L

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 TotalEnergies SE

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 BP PLC

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Repsol SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.1 Petroleo Brasileiro S A

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: South America Defense Aircraft Aviation Fuel Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America Defense Aircraft Aviation Fuel Market Share (%) by Company 2025

List of Tables

- Table 1: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 5: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 8: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 9: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 11: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 14: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: South America Defense Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Defense Aircraft Aviation Fuel Market?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the South America Defense Aircraft Aviation Fuel Market?

Key companies in the market include Petroleo Brasileiro S A, Shell PLC, Allied Aviation Services Inc, Exxon Mobil Corporation, Pan American Energy S L, TotalEnergies SE, BP PLC, Repsol SA.

3. What are the main segments of the South America Defense Aircraft Aviation Fuel Market?

The market segments include Fuel Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.25 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising Industrialization across the Globe4.; Increasing Utilization of Natural Gas.

6. What are the notable trends driving market growth?

Air Turbine Fuel to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Cost of Installation and Maintenance.

8. Can you provide examples of recent developments in the market?

March 2022: United Airlines, through its corporate venture capital fund, United Airlines Ventures (UAV), and Oxy Low Carbon Ventures (a subsidiary of Occidental), announced a collaboration with Houston-based biotech firm Comvita Factory to commercialize the production of sustainable aviation fuel (SAF) developed through a new process using carbon dioxide (CO2) and synthetic microbes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Defense Aircraft Aviation Fuel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Defense Aircraft Aviation Fuel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Defense Aircraft Aviation Fuel Market?

To stay informed about further developments, trends, and reports in the South America Defense Aircraft Aviation Fuel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence