Key Insights

The Middle East and Africa Bunker Fuel Market is projected for substantial expansion, forecasted to grow at a Compound Annual Growth Rate (CAGR) of 5.6%. This growth is propelled by increased global trade, rising shipping volumes on strategic maritime routes, and the growing demand for cleaner fuel alternatives. Driven by stringent environmental regulations and the IMO 2020 mandate, Very-Low Sulfur Fuel Oil (VLSFO) and Liquefied Natural Gas (LNG) are gaining traction. VLSFO is particularly favored for its cost-effectiveness in meeting sulfur emission limits, making it a preferred choice for various vessel types. Infrastructure development for enhanced bunkering capabilities and port facilities in key nations like the UAE, Saudi Arabia, and Nigeria further supports market dynamism.

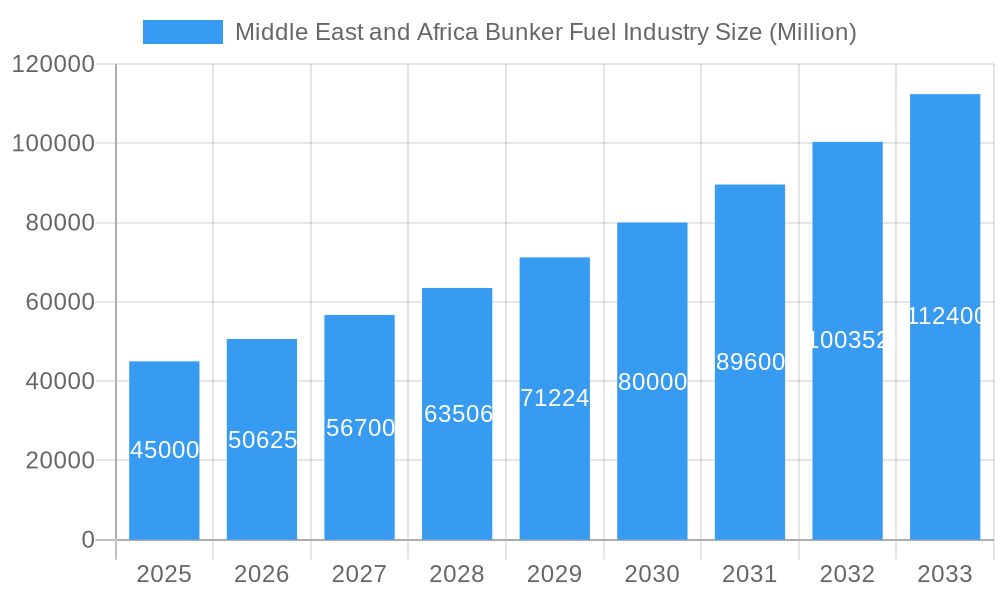

Middle East and Africa Bunker Fuel Industry Market Size (In Billion)

Market restraints include volatility in crude oil prices, directly impacting bunker fuel costs and creating challenges for end-users. The transition to alternative fuels requires significant capital investment in new infrastructure and vessel retrofitting, posing a hurdle for smaller players and developing nations. Despite these challenges, the long-term trend points towards decarbonization and improved fuel efficiency. Investments in advanced bunkering technologies and the exploration of fuels such as methanol and ammonia are expected to shape the future landscape, ensuring sustained growth for the Middle East and Africa Bunker Fuel Market from a base year of 2025, reaching a market size of 172.5 billion by 2033.

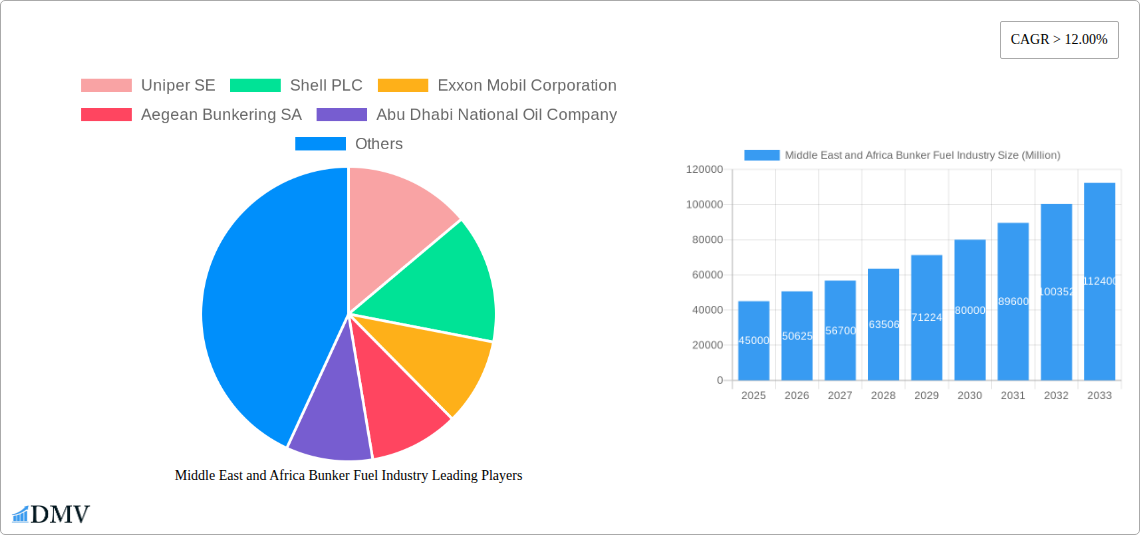

Middle East and Africa Bunker Fuel Industry Company Market Share

Middle East and Africa Bunker Fuel Industry Market Analysis: Forecast 2025-2033

This comprehensive report delves deep into the Middle East and Africa (MEA) Bunker Fuel Industry, providing an in-depth market analysis for the period 2019–2033, with a base and estimated year of 2025. It offers critical insights for stakeholders navigating this dynamic sector, covering market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, future opportunities, major players, key developments, and strategic market forecasts. This report is an essential tool for understanding the intricate interplay of fuel types, vessel categories, and geographical focuses within the MEA bunker fuel landscape.

Middle East and Africa Bunker Fuel Industry Market Composition & Trends

The MEA bunker fuel market exhibits a dynamic composition influenced by evolving regulatory landscapes and technological advancements. Market concentration is moderate, with key players like Shell PLC, Exxon Mobil Corporation, and Abu Dhabi National Oil Company (ADNOC) holding significant market shares, estimated at 15%, 12%, and 10% respectively in the base year of 2025. Innovation is primarily driven by the transition towards cleaner fuels, with Very-Low Sulfur Fuel Oil (VLSFO) and Liquefied Natural Gas (LNG) gaining traction, albeit at varying adoption rates across the region. Regulatory frameworks, particularly those aligned with International Maritime Organization (IMO) standards, are crucial catalysts for market shifts. Substitute products, such as alternative marine fuels, present a growing competitive pressure, especially in environmentally conscious shipping segments. End-user profiles are diverse, ranging from large container shipping lines to bulk carrier operators, each with unique fuel procurement strategies. Mergers and acquisitions (M&A) activities, while not yet extensive, are anticipated to increase as companies seek to consolidate their positions and expand their service offerings. For instance, hypothetical M&A deals in the historical period (2019-2024) might have seen regional distributors acquiring smaller players to enhance their geographical reach, with estimated deal values in the range of USD 50-100 Million. The market's trajectory is closely tied to global trade volumes and shipping efficiency improvements.

Middle East and Africa Bunker Fuel Industry Industry Evolution

The Middle East and Africa (MEA) bunker fuel industry has witnessed a significant evolutionary arc, driven by a confluence of technological innovation, shifting regulatory demands, and evolving global trade dynamics. From 2019 to 2024, the historical period, the industry primarily revolved around High Sulfur Fuel Oil (HSFO), with its cost-effectiveness making it the dominant choice for a majority of vessel types, particularly Tankers and General Cargo ships. However, the advent of stricter environmental regulations, spearheaded by the International Maritime Organization (IMO) 2020 sulfur cap, catalyzed a dramatic shift towards Very-Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO). This transition was not without its challenges, requiring significant investment in refining capabilities and supply chain adjustments across the MEA region. For instance, the adoption rate of VLSFO jumped from an estimated 20% in 2019 to over 65% by 2024, demonstrating the rapid response to regulatory pressures.

Technological advancements have played a pivotal role in shaping this evolution. The development of advanced refining processes has enabled the consistent production of lower-sulfur fuels, while innovations in fuel testing and monitoring have ensured compliance and quality assurance. Furthermore, the burgeoning interest in alternative fuels, particularly Liquefied Natural Gas (LNG), has begun to reshape the future outlook. While currently a niche segment, LNG adoption is projected to witness substantial growth driven by its cleaner emission profile and increasing availability of bunkering infrastructure in key MEA ports. The growth rate of LNG as a bunker fuel in the MEA region, starting from a negligible percentage in 2019, is forecast to reach an estimated 8% by 2033.

Shifting consumer demands, influenced by corporate sustainability goals and increasing public awareness of environmental issues, have also been instrumental. Shipping companies are actively seeking greener solutions to reduce their carbon footprint, thereby creating a market pull for more sustainable bunker fuel options. This has also led to increased demand for advanced lubricant technologies and fuel additives that enhance engine performance and reduce emissions, even with traditional fuels. The industry has responded by investing in research and development, leading to the introduction of a wider array of fuel options and associated services designed to meet these evolving needs. The entire ecosystem, from fuel producers and distributors to shipping lines and port authorities, has undergone significant transformation to adapt to these evolving market dynamics and embrace a more sustainable future in maritime fuel supply.

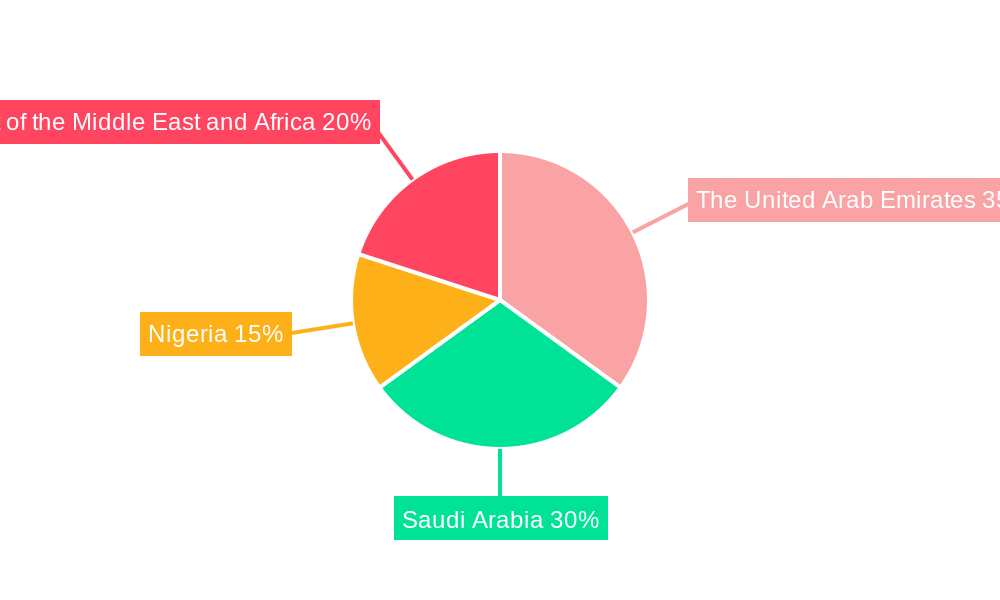

Leading Regions, Countries, or Segments in Middle East and Africa Bunker Fuel Industry

The Middle East and Africa (MEA) bunker fuel industry is characterized by the pronounced dominance of specific regions, countries, and fuel types, driven by a complex interplay of economic, logistical, and regulatory factors. Among the geographical focuses, The United Arab Emirates (UAE) stands out as a leading hub, primarily due to its strategic location, advanced port infrastructure, and significant investments in its maritime sector. The UAE's commitment to becoming a global maritime center has fostered an environment conducive to robust bunker fuel demand, particularly for VLSFO and MGO, which are increasingly favored by international shipping lines adhering to stringent environmental regulations. Saudi Arabia also plays a crucial role, with its extensive coastline and major oil production capacity providing a strong foundation for its bunker fuel market. Nigeria, though facing unique challenges, remains a significant player due to its substantial maritime trade volume, particularly for Tankers and General Cargo vessels.

When examining fuel types, Very-Low Sulfur Fuel Oil (VLSFO) has emerged as the dominant segment, reflecting the global mandate for lower sulfur emissions. Its market share is projected to account for an estimated 60% of the total MEA bunker fuel market by 2025, a substantial increase from its historical share. Marine Gas Oil (MGO) follows closely, especially for smaller vessels and in specific geographical pockets where its use is mandated or preferred for environmental reasons. High Sulfur Fuel Oil (HSFO), while still present, is experiencing a gradual decline in market share as regulatory pressures intensify and cleaner alternatives become more accessible. The rise of Liquefied Natural Gas (LNG) as a bunker fuel, though currently in its nascent stages, represents a significant growth opportunity, with projections indicating a steady increase in its market penetration over the forecast period.

In terms of vessel types, Containers and Tankers represent the largest consumers of bunker fuel in the MEA region. Container shipping is a cornerstone of global trade, and the MEA region serves as a vital transshipment hub, driving substantial demand for bunker fuels. Tankers, essential for the transport of oil and other liquid commodities, also contribute significantly to bunker fuel consumption. Bulk Carriers and General Cargo vessels form the next tier of demand.

Key drivers for the dominance of these segments include:

- Strategic Location and Trade Volumes: The UAE's position as a gateway between East and West, coupled with its high volume of container and tanker traffic, directly translates to substantial bunker fuel demand.

- Investment in Port Infrastructure: Significant investments in port development and expansion by countries like the UAE and Saudi Arabia have enhanced their bunkering capabilities, attracting more vessels and increasing fuel throughput.

- Regulatory Compliance: The overarching influence of IMO regulations drives the demand for VLSFO and MGO, making them the most sought-after fuel types.

- Availability and Cost-Effectiveness: While cleaner fuels are in demand, the relative availability and cost-competitiveness of certain fuel types in specific MEA locations can still influence their adoption rates.

- Emerging LNG Infrastructure: The gradual development of LNG bunkering facilities in key MEA ports is a significant factor supporting the potential growth of LNG as a bunker fuel.

The dominance of these regions, countries, and segments is a testament to the strategic importance of maritime trade in the MEA economy and the ongoing adaptation of the bunker fuel industry to meet global environmental standards and evolving market needs.

Middle East and Africa Bunker Fuel Industry Product Innovations

Product innovation in the MEA bunker fuel industry is increasingly focused on sustainability and enhanced performance. The primary innovation lies in the development and consistent supply of Very-Low Sulfur Fuel Oil (VLSFO) formulations that meet the stringent <0.5% sulfur content requirement, ensuring regulatory compliance and reduced emissions. Furthermore, advancements in Marine Gas Oil (MGO) production are yielding cleaner-burning variants with improved combustion properties. Research into Liquefied Natural Gas (LNG) bunkering solutions is gaining momentum, with innovations in liquefaction, storage, and delivery systems being crucial for its broader adoption. Beyond fuel types, innovations in fuel additives and lubricants are enhancing engine efficiency, reducing wear and tear, and further minimizing pollutant output, thereby offering unique selling propositions for integrated fuel and service providers.

Propelling Factors for Middle East and Africa Bunker Fuel Industry Growth

The Middle East and Africa (MEA) bunker fuel industry is propelled by several interconnected factors. Primarily, the growing global trade volumes and the region's strategic position as a key maritime transit point are driving increased shipping activity and, consequently, bunker fuel demand. The increasing adoption of stricter environmental regulations, such as the IMO 2020 sulfur cap and upcoming carbon intensity reduction targets, is a significant catalyst, compelling the shift towards cleaner fuels like VLSFO and MGO, and fostering the development of LNG bunkering. Furthermore, significant investments in port infrastructure and maritime logistics across the MEA region are enhancing bunkering capabilities and attracting more vessels. The economic growth and industrialization within many African nations are also contributing to rising maritime trade and associated fuel requirements. Finally, technological advancements in refining and fuel production are making cleaner fuel options more accessible and economically viable, further supporting market expansion.

Obstacles in the Middle East and Africa Bunker Fuel Industry Market

Despite robust growth prospects, the MEA bunker fuel industry faces several significant obstacles. Volatile crude oil prices can lead to unpredictable bunker fuel costs, impacting the profitability of shipping operations and making long-term planning challenging. Inconsistent regulatory enforcement and varying implementation timelines across different MEA countries can create market fragmentation and compliance complexities. Limited availability of advanced bunkering infrastructure, particularly for alternative fuels like LNG in certain sub-regions, can hinder their widespread adoption. Supply chain disruptions, often exacerbated by geopolitical instability or logistical challenges, can lead to shortages and price spikes. Furthermore, the capital investment required for transitioning to cleaner fuels and upgrading bunkering facilities poses a significant barrier for smaller players and developing nations within the region.

Future Opportunities in Middle East and Africa Bunker Fuel Industry

The MEA bunker fuel industry is ripe with future opportunities, primarily driven by the accelerating global push for decarbonization. The increasing demand for alternative marine fuels, especially LNG, presents a substantial growth avenue as more countries invest in bunkering infrastructure. The development of green methanol and ammonia as future marine fuels also represents a nascent but promising opportunity for early movers in research, production, and bunkering. Expansion of LNG bunkering services in landlocked African countries with significant riverine or lake-based maritime activity could unlock new markets. Furthermore, innovations in digital solutions for fuel management, optimization, and trading offer opportunities to enhance efficiency and transparency. The establishment of dedicated bunkering hubs in strategic MEA locations, coupled with the integration of renewable energy sources for fuel production, could further bolster the industry's sustainable growth trajectory.

Major Players in the Middle East and Africa Bunker Fuel Industry Ecosystem

- Uniper SE

- Shell PLC

- Exxon Mobil Corporation

- Aegean Bunkering SA

- Abu Dhabi National Oil Company

- Gulf Agency Company Ltd

- Chevron Corporation

- TotalEnergies SE

Key Developments in Middle East and Africa Bunker Fuel Industry Industry

- May 2022: European Bank for Reconstruction and Development (EBRD) provided a USD 41.6 Million loan to Agence Nationale des Ports (ANP) for the development of Moroccan ports. The loan will be supplemented by an investment grant of USD 5.7 Million from the Global Environment Facility (GEF), enhancing port infrastructure crucial for bunkering operations.

- December 2022: Sudan signed a USD 6 Billion agreement with a consortium led by the United Arab Emirates' AD Ports Group and Invictus Investment to develop a new port and economic zone in the Red Sea, signaling significant future growth in maritime trade and associated bunkering demand.

Strategic Middle East and Africa Bunker Fuel Industry Market Forecast

The strategic forecast for the MEA bunker fuel industry indicates a sustained growth trajectory, primarily fueled by increasing global trade, stringent environmental regulations, and ongoing investments in maritime infrastructure. The transition towards cleaner fuel types, particularly VLSFO and MGO, will continue to dominate the market in the near to medium term, while LNG is poised for significant expansion as bunkering facilities become more widespread. Emerging opportunities in green fuels and digital solutions present long-term potential for market diversification and innovation. The region's strategic geographical positioning ensures its continued relevance as a vital hub for maritime traffic, underpinning the robust demand for bunker fuels throughout the forecast period, with an estimated market growth rate of 4-6% annually from 2025 to 2033.

Middle East and Africa Bunker Fuel Industry Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Other Fuel Types

-

2. Vessel Type

- 2.1. Containers

- 2.2. Tankers

- 2.3. General Cargo

- 2.4. Bulk Carrier

- 2.5. Other Vessel Types

-

3. Geography

- 3.1. The United Arab Emirates

- 3.2. Saudi Arabia

- 3.3. Nigeria

- 3.4. Rest of the Middle-East and Africa

Middle East and Africa Bunker Fuel Industry Segmentation By Geography

- 1. The United Arab Emirates

- 2. Saudi Arabia

- 3. Nigeria

- 4. Rest of the Middle East and Africa

Middle East and Africa Bunker Fuel Industry Regional Market Share

Geographic Coverage of Middle East and Africa Bunker Fuel Industry

Middle East and Africa Bunker Fuel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Other Fuel Types

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Containers

- 5.2.2. Tankers

- 5.2.3. General Cargo

- 5.2.4. Bulk Carrier

- 5.2.5. Other Vessel Types

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. The United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Nigeria

- 5.3.4. Rest of the Middle-East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. The United Arab Emirates

- 5.4.2. Saudi Arabia

- 5.4.3. Nigeria

- 5.4.4. Rest of the Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Other Fuel Types

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Containers

- 6.2.2. Tankers

- 6.2.3. General Cargo

- 6.2.4. Bulk Carrier

- 6.2.5. Other Vessel Types

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. The United Arab Emirates

- 6.3.2. Saudi Arabia

- 6.3.3. Nigeria

- 6.3.4. Rest of the Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. The United Arab Emirates Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. High Sulfur Fuel Oil (HSFO)

- 7.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 7.1.3. Marine Gas Oil (MGO)

- 7.1.4. Liquefied Natural Gas (LNG)

- 7.1.5. Other Fuel Types

- 7.2. Market Analysis, Insights and Forecast - by Vessel Type

- 7.2.1. Containers

- 7.2.2. Tankers

- 7.2.3. General Cargo

- 7.2.4. Bulk Carrier

- 7.2.5. Other Vessel Types

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. The United Arab Emirates

- 7.3.2. Saudi Arabia

- 7.3.3. Nigeria

- 7.3.4. Rest of the Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Saudi Arabia Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. High Sulfur Fuel Oil (HSFO)

- 8.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 8.1.3. Marine Gas Oil (MGO)

- 8.1.4. Liquefied Natural Gas (LNG)

- 8.1.5. Other Fuel Types

- 8.2. Market Analysis, Insights and Forecast - by Vessel Type

- 8.2.1. Containers

- 8.2.2. Tankers

- 8.2.3. General Cargo

- 8.2.4. Bulk Carrier

- 8.2.5. Other Vessel Types

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. The United Arab Emirates

- 8.3.2. Saudi Arabia

- 8.3.3. Nigeria

- 8.3.4. Rest of the Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Nigeria Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. High Sulfur Fuel Oil (HSFO)

- 9.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 9.1.3. Marine Gas Oil (MGO)

- 9.1.4. Liquefied Natural Gas (LNG)

- 9.1.5. Other Fuel Types

- 9.2. Market Analysis, Insights and Forecast - by Vessel Type

- 9.2.1. Containers

- 9.2.2. Tankers

- 9.2.3. General Cargo

- 9.2.4. Bulk Carrier

- 9.2.5. Other Vessel Types

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. The United Arab Emirates

- 9.3.2. Saudi Arabia

- 9.3.3. Nigeria

- 9.3.4. Rest of the Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Rest of the Middle East and Africa Middle East and Africa Bunker Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10.1.1. High Sulfur Fuel Oil (HSFO)

- 10.1.2. Very-Low Sulfur Fuel Oil (VLSFO)

- 10.1.3. Marine Gas Oil (MGO)

- 10.1.4. Liquefied Natural Gas (LNG)

- 10.1.5. Other Fuel Types

- 10.2. Market Analysis, Insights and Forecast - by Vessel Type

- 10.2.1. Containers

- 10.2.2. Tankers

- 10.2.3. General Cargo

- 10.2.4. Bulk Carrier

- 10.2.5. Other Vessel Types

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. The United Arab Emirates

- 10.3.2. Saudi Arabia

- 10.3.3. Nigeria

- 10.3.4. Rest of the Middle-East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Uniper SE

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Shell PLC

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Exxon Mobil Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Aegean Bunkering SA

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Abu Dhabi National Oil Company

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Gulf Agency Company Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Chevron Corporation

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 TotalEnergies SE

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.1 Uniper SE

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Bunker Fuel Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Bunker Fuel Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 3: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 4: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 5: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 7: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Region 2020 & 2033

- Table 9: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 10: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 11: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 12: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 13: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 14: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 15: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 17: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 18: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 19: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 20: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 21: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 23: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 25: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 26: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 27: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 28: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 29: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 30: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 31: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

- Table 33: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 34: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 35: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 36: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 37: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 38: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Geography 2020 & 2033

- Table 39: Middle East and Africa Bunker Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Middle East and Africa Bunker Fuel Industry Volume metric tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Bunker Fuel Industry?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Middle East and Africa Bunker Fuel Industry?

Key companies in the market include Uniper SE, Shell PLC, Exxon Mobil Corporation, Aegean Bunkering SA, Abu Dhabi National Oil Company, Gulf Agency Company Ltd, Chevron Corporation, TotalEnergies SE.

3. What are the main segments of the Middle East and Africa Bunker Fuel Industry?

The market segments include Fuel Type, Vessel Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 172.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Declining Cost of Solar PV Installations4.; Supportive Government Policies For Renewable Energy.

6. What are the notable trends driving market growth?

VLSFO to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Penetration of Other Energy Sources.

8. Can you provide examples of recent developments in the market?

May 2022: European Bank for Reconstruction and Development (EBRD) provided a USD 41.6 million loan to Agence Nationale des Ports (ANP) for the development of Moroccan ports. The loan will be supplemented by an investment grant of USD 5.7 million from the Global Environment Facility (GEF).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Bunker Fuel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Bunker Fuel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Bunker Fuel Industry?

To stay informed about further developments, trends, and reports in the Middle East and Africa Bunker Fuel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence