Key Insights

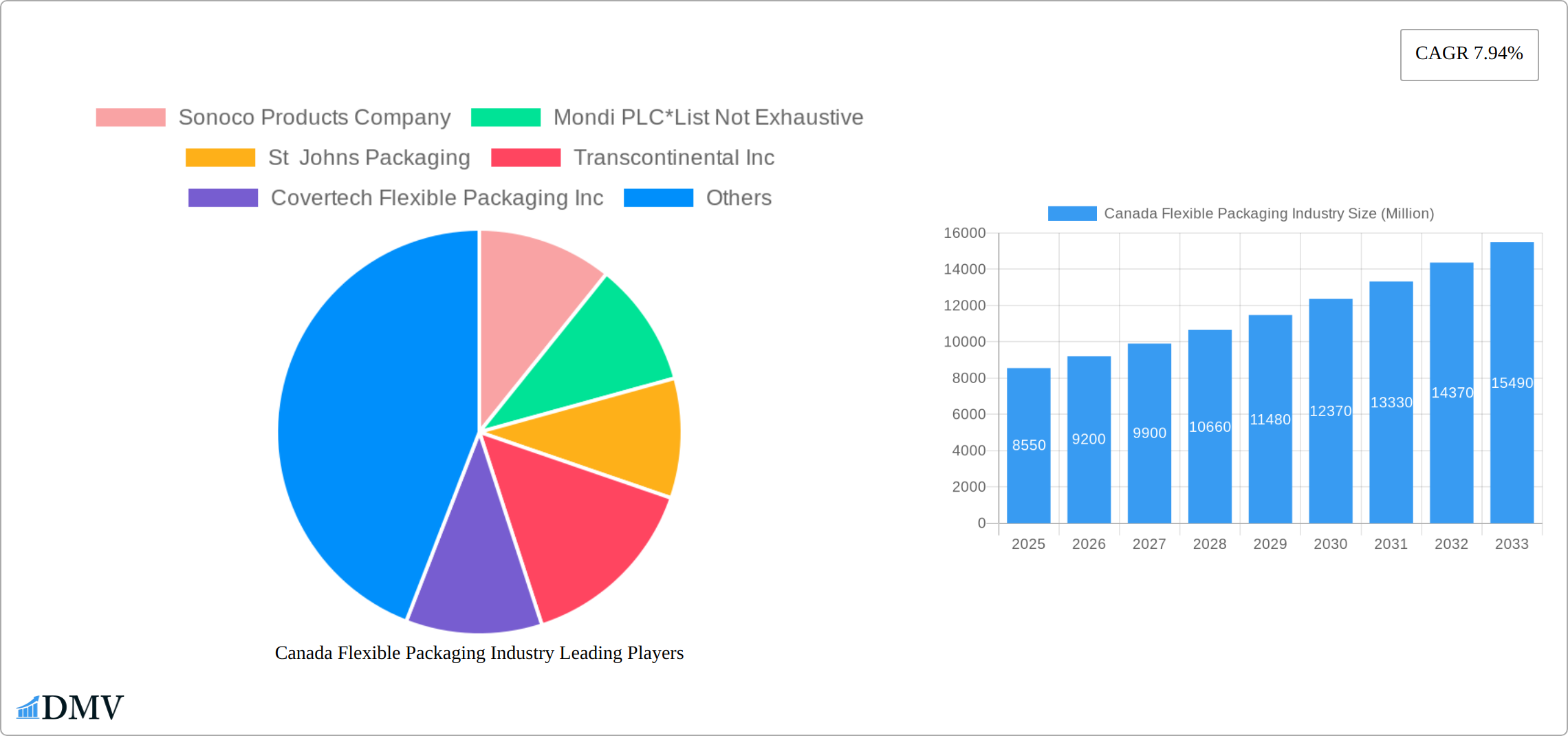

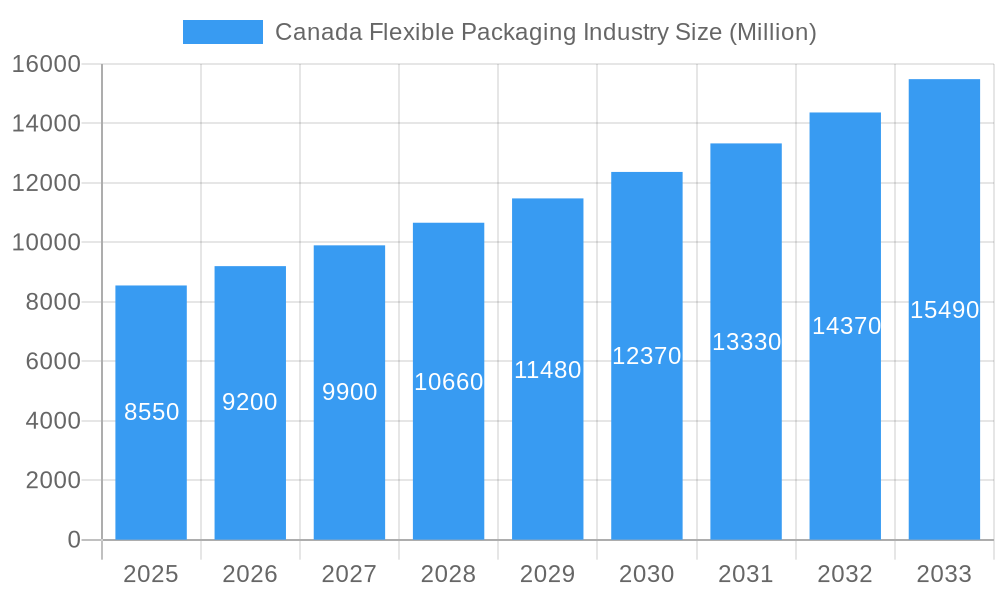

The Canadian flexible packaging market, valued at $8.55 billion in 2025, is projected to experience robust growth, driven by a compound annual growth rate (CAGR) of 7.94% from 2025 to 2033. This expansion is fueled by several key factors. The burgeoning food and beverage sector in Canada, coupled with increasing demand for convenient and shelf-stable products, is a significant driver. Furthermore, the growing popularity of e-commerce and the associated need for efficient and protective packaging solutions are contributing to market growth. Consumer preference for sustainable and eco-friendly packaging options is also shaping industry trends, leading to increased innovation in materials like biodegradable plastics and paper-based alternatives. While fluctuating raw material prices and environmental regulations present potential restraints, the overall outlook for the Canadian flexible packaging market remains positive. The market segmentation reveals a strong presence of pouches, bags, films, and wraps, largely serving the food, beverage, household, and personal care sectors. Major players like Amcor PLC, Berry Global Inc., and Sonoco Products Company are actively shaping market dynamics through technological advancements and strategic acquisitions. Regional variations exist, with Eastern, Western, and Central Canada exhibiting different growth trajectories based on consumer preferences and industrial activity. The continued growth of the Canadian economy and its expanding retail and manufacturing sectors are expected to further propel the flexible packaging market's expansion throughout the forecast period.

Canada Flexible Packaging Industry Market Size (In Billion)

The competitive landscape is characterized by a mix of large multinational corporations and regional players. These companies compete primarily on price, quality, innovation, and sustainability. The increasing focus on customization and specialized packaging solutions is creating opportunities for smaller players to differentiate themselves. However, the large established players are continuously investing in research and development to maintain their market share and offer innovative solutions. The historical data from 2019-2024 indicates a consistent, albeit perhaps slightly lower, growth rate, suggesting the 7.94% CAGR for 2025-2033 represents a period of accelerated expansion likely driven by the factors mentioned above. Analysis of regional data, though limited, highlights the potential for targeted marketing strategies based on specific regional needs and consumer behaviors within Canada. Future growth will likely be influenced by government policies supporting sustainable packaging, evolving consumer demands, and technological advancements in packaging materials and manufacturing processes.

Canada Flexible Packaging Industry Company Market Share

Canada Flexible Packaging Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Canada flexible packaging industry, offering valuable insights for stakeholders seeking to understand market dynamics, growth trajectories, and future opportunities. Covering the period from 2019 to 2033, with a focus on 2025, this report is essential for strategic decision-making in this dynamic sector. The Canadian flexible packaging market, valued at xx Million in 2024, is projected to reach xx Million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of xx%.

Canada Flexible Packaging Industry Market Composition & Trends

The Canadian flexible packaging market presents a dynamic landscape shaped by a complex interplay of factors. This analysis dissects the market's structure, identifying key trends, influential forces, and challenges facing industry participants. We explore market concentration, innovation drivers, regulatory pressures, substitute products, end-user demands, and the impact of mergers and acquisitions (M&A) activity.

Market Concentration & Competition: The Canadian flexible packaging industry is characterized by a diverse competitive environment, encompassing both large multinational corporations and smaller, specialized firms. While a few major players hold significant market share, the overall distribution is fragmented, resulting in intense competition. This competition is fueled by ongoing innovation in materials, processes, and designs, along with aggressive pricing strategies and a focus on superior customer service. Precise market share data for 2024 will be available in the full report.

Innovation Catalysts: Sustainability is paramount, driving significant innovation toward eco-friendly materials such as recycled content, bioplastics, and compostable films. Simultaneously, advancements in barrier technologies extend shelf life, enhancing product preservation. Innovations in printing techniques allow for visually appealing and highly customizable packaging designs, further boosting brand differentiation and consumer appeal.

Regulatory Landscape: The Canadian regulatory environment significantly impacts the flexible packaging industry. Stringent food safety standards, evolving material recyclability requirements, and increasingly stringent environmental regulations present ongoing compliance challenges. Companies must invest in sustainable practices and adapt to evolving legislation to ensure ongoing market access.

Substitute Products: Rigid packaging options (e.g., cans, glass bottles) compete with flexible packaging, but the latter's advantages—lighter weight, improved portability, enhanced shelf life, and cost-effectiveness—maintain its dominance in many applications. However, the growing preference for sustainable options presents both a challenge and an opportunity for innovation.

End-User Profiles: Key end-user industries include food and beverages (the largest segment), household and personal care products, industrial goods, and others. The ongoing growth in convenience foods and ready-to-eat meals is a key driver of demand within the food and beverage sector. E-commerce continues to drive demand for packaging solutions that ensure product safety during shipping and handling.

M&A Activity: Consolidation is a noteworthy trend in the Canadian flexible packaging market, reflected in significant M&A activity in recent years. These transactions, ranging in value from [Update with actual range if available], signal a pursuit of scale, enhanced market share, and broader product portfolios. Further analysis of specific transactions and their strategic implications will be provided in the full report.

Canada Flexible Packaging Industry Industry Evolution

This section analyzes the evolution of the Canadian flexible packaging market, highlighting its growth trajectory, technological advancements, and changing consumer preferences.

The Canadian flexible packaging market has witnessed consistent growth over the past five years (2019-2024), expanding at a CAGR of xx%. This growth is attributed to several factors, including increasing demand from the food and beverage sector, the rise of e-commerce, and the adoption of flexible packaging in various applications. Technological advancements in materials science and manufacturing processes have significantly improved the functionality and performance of flexible packaging. Examples include the development of recyclable materials, improved barrier properties, and the use of advanced printing techniques. Consumer preferences for convenience, portability, and sustainability have also fueled the demand for innovative flexible packaging solutions.

Specifically, the adoption of sustainable packaging solutions is growing rapidly, with a projected adoption rate of xx% by 2033. The shift toward e-commerce has also increased the demand for lightweight and durable flexible packaging, ensuring safe product transportation and handling. The market is further segmented by product type (pouches, bags, films, and wraps, other product types), end-user industry (food, beverage, household and personal care, other end-user industries), and material type (plastics, EVOH, paper, aluminum foil). The demand for pouches and bags is increasing, representing approximately xx% of the market share in 2024.

Leading Regions, Countries, or Segments in Canada Flexible Packaging Industry

This section identifies the dominant regions, countries, and segments within the Canadian flexible packaging market, analyzing the factors contributing to their leading positions.

- Dominant Segment: The food and beverage sector is the leading end-user industry, accounting for xx% of total market value in 2024. This dominance stems from the high demand for flexible packaging solutions across various food and beverage categories.

- Product Type: Pouches remain the most dominant product type in 2024, representing xx% of market share, thanks to their convenience and versatility.

- Material Type: Plastics continue to be the most widely used material, but there is a strong growth trend toward eco-friendly alternatives.

Key Drivers:

- Investment Trends: Significant investments in research and development are driving innovation in sustainable packaging materials and technologies.

- Regulatory Support: Government initiatives promoting sustainable packaging are creating a favorable environment for the adoption of eco-friendly solutions. Increased consumer awareness of environmental issues further strengthens this trend.

Canada Flexible Packaging Industry Product Innovations

Recent product innovations have focused on enhancing sustainability, functionality, and convenience. For example, biodegradable and compostable films are gaining popularity, catering to increasing environmental concerns. Improved barrier properties offer extended shelf life for sensitive products. Moreover, innovations in printing technologies allow for personalized and eye-catching packaging designs.

Propelling Factors for Canada Flexible Packaging Industry Growth

Several factors are driving growth within the Canadian flexible packaging industry. These include increasing demand from the food and beverage industry due to rising consumer preferences for convenience and ready-to-eat meals. Advancements in materials science and manufacturing technologies contribute to superior product performance. Government regulations promoting sustainability are accelerating the adoption of eco-friendly packaging solutions. Finally, the thriving e-commerce sector boosts demand for packaging that is suitable for efficient shipping and handling.

Obstacles in the Canada Flexible Packaging Industry Market

The Canadian flexible packaging industry faces several challenges, including fluctuating raw material prices, stringent environmental regulations that can increase production costs, and intense competition from established players. Supply chain disruptions, exacerbated by global events, can lead to production delays and increased costs. Further, the industry faces pressure to continuously innovate and adapt to meet shifting consumer demands and evolving environmental concerns.

Future Opportunities in Canada Flexible Packaging Industry

Future opportunities lie in developing and implementing sustainable packaging solutions, expanding into new markets, and adopting innovative technologies. Growth is expected in high-barrier films for sensitive products and pouches designed for greater convenience. Furthermore, focusing on custom packaging and providing personalized solutions is expected to create more demand.

Major Players in the Canada Flexible Packaging Industry Ecosystem

- Sonoco Products Company

- Mondi PLC

- St Johns Packaging

- Transcontinental Inc

- Covertech Flexible Packaging Inc

- American Packaging Corporation

- Cascades Flexible Packaging

- Flair Flexible Packaging Corporation

- Sigma Plastics Group

- Winpak Ltd

- Amcor PLC

- Emmerson Packaging

- Novolex Holdings Inc

- Constantia Flexibles

- Tetra Pak International SA

- ProAmpac LLC

- Berry Global Inc

- Printpack Inc

- Sealed Air Corporation

- Sit Group SpA

Key Developments in Canada Flexible Packaging Industry Industry

- June 2022: ePac Flexible Packaging expands to three Canadian locations (Montreal, Toronto, Vancouver), enhancing its service to CPG brands across the country. This expansion signifies increased market competitiveness and capacity to cater to short-run packaging demands.

- April 2022: WestRock and Swiss Chalet collaborate to introduce recyclable paperboard packaging, replacing less sustainable PET trays and lids. This highlights the growing adoption of sustainable packaging practices within the Canadian food service industry.

Strategic Canada Flexible Packaging Industry Market Forecast

The Canadian flexible packaging market is poised for continued growth, driven by factors including increasing demand for sustainable packaging and technological innovation. Opportunities exist in developing innovative packaging materials and designs that meet the evolving needs of consumers and businesses. The market's future trajectory is positive, anticipating substantial growth throughout the forecast period.

Canada Flexible Packaging Industry Segmentation

-

1. Material Type

-

1.1. Plastics

- 1.1.1. Polyethene (PE)

- 1.1.2. Bi-orientated Polypropylene (BOPP)

- 1.1.3. Cast Polypropylene (CPP)

- 1.1.4. Polyvinyl Chloride (PVC)

- 1.1.5. Ethylene Vinyl Alcohol (EVOH)

- 1.2. Paper

- 1.3. Aluminum Foil

-

1.1. Plastics

-

2. Product Type

- 2.1. Pouches

- 2.2. Bags

- 2.3. Films and Wraps

- 2.4. Other Product Types

-

3. End-user Industry

- 3.1. Food

- 3.2. Beverage

- 3.3. Household and Personal Care

- 3.4. Other End-user Industries

Canada Flexible Packaging Industry Segmentation By Geography

- 1. Canada

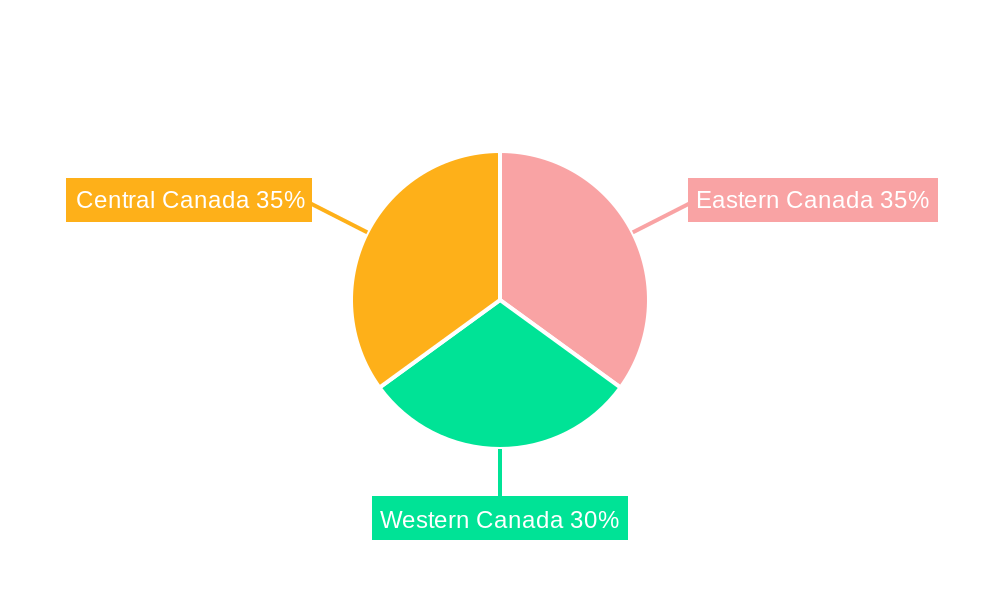

Canada Flexible Packaging Industry Regional Market Share

Geographic Coverage of Canada Flexible Packaging Industry

Canada Flexible Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.94% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Plastics

- 5.1.1.1. Polyethene (PE)

- 5.1.1.2. Bi-orientated Polypropylene (BOPP)

- 5.1.1.3. Cast Polypropylene (CPP)

- 5.1.1.4. Polyvinyl Chloride (PVC)

- 5.1.1.5. Ethylene Vinyl Alcohol (EVOH)

- 5.1.2. Paper

- 5.1.3. Aluminum Foil

- 5.1.1. Plastics

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Pouches

- 5.2.2. Bags

- 5.2.3. Films and Wraps

- 5.2.4. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Beverage

- 5.3.3. Household and Personal Care

- 5.3.4. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Canada Flexible Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Plastics

- 6.1.1.1. Polyethene (PE)

- 6.1.1.2. Bi-orientated Polypropylene (BOPP)

- 6.1.1.3. Cast Polypropylene (CPP)

- 6.1.1.4. Polyvinyl Chloride (PVC)

- 6.1.1.5. Ethylene Vinyl Alcohol (EVOH)

- 6.1.2. Paper

- 6.1.3. Aluminum Foil

- 6.1.1. Plastics

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Pouches

- 6.2.2. Bags

- 6.2.3. Films and Wraps

- 6.2.4. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Beverage

- 6.3.3. Household and Personal Care

- 6.3.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sonoco Products Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mondi PLC*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 St Johns Packaging

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Transcontinental Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Covertech Flexible Packaging Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 American Packaging Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Cascades Flexible Packaging

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Flair Flexible Packaging Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sigma Plastics Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Winpak Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Amcor PLC

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Emmerson Packaging

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Novolex Holdings Inc

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Constantia Flexibles

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Tetra Pak International SA

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 ProAmpac LLC

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Berry Global Inc

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Printpack Inc

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Sealed Air Corporation

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 Sit Group SpA

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.1 Sonoco Products Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Flexible Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Flexible Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Flexible Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Canada Flexible Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 3: Canada Flexible Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Canada Flexible Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Canada Flexible Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 6: Canada Flexible Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 7: Canada Flexible Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Canada Flexible Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Flexible Packaging Industry?

The projected CAGR is approximately 7.94%.

2. Which companies are prominent players in the Canada Flexible Packaging Industry?

Key companies in the market include Sonoco Products Company, Mondi PLC*List Not Exhaustive, St Johns Packaging, Transcontinental Inc, Covertech Flexible Packaging Inc, American Packaging Corporation, Cascades Flexible Packaging, Flair Flexible Packaging Corporation, Sigma Plastics Group, Winpak Ltd, Amcor PLC, Emmerson Packaging, Novolex Holdings Inc, Constantia Flexibles, Tetra Pak International SA, ProAmpac LLC, Berry Global Inc, Printpack Inc, Sealed Air Corporation, Sit Group SpA.

3. What are the main segments of the Canada Flexible Packaging Industry?

The market segments include Material Type, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.55 Million as of 2022.

5. What are some drivers contributing to market growth?

The Increased Demand for Convenient Packaging; Changing Demographic and Lifestyle Factors.

6. What are the notable trends driving market growth?

Food Industry is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

; High Cost of Label Converting Equipment.

8. Can you provide examples of recent developments in the market?

June 2022: ePac Flexible Packaging, the industry player in quick turn, short, and medium run-length flexible packaging has announced it will add a third sales and manufacturing location in Canada. With the addition of operations in Vancouver and Toronto, ePac Montreal will provide CPG brands of all sizes with service throughout the province of Quebec, bringing the total number of Canadian locations to three.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Flexible Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Flexible Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Flexible Packaging Industry?

To stay informed about further developments, trends, and reports in the Canada Flexible Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence