Key Insights

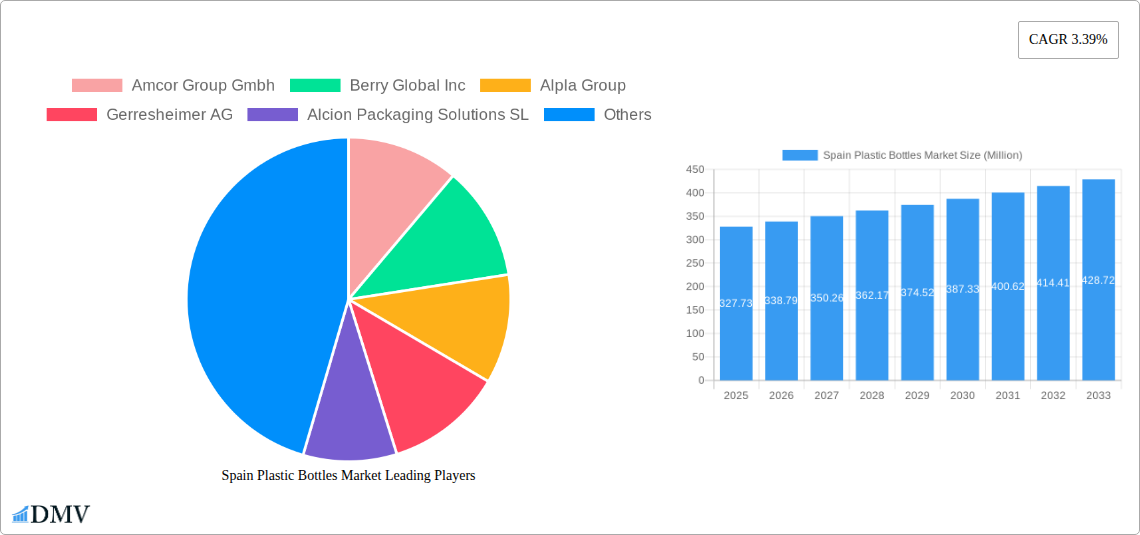

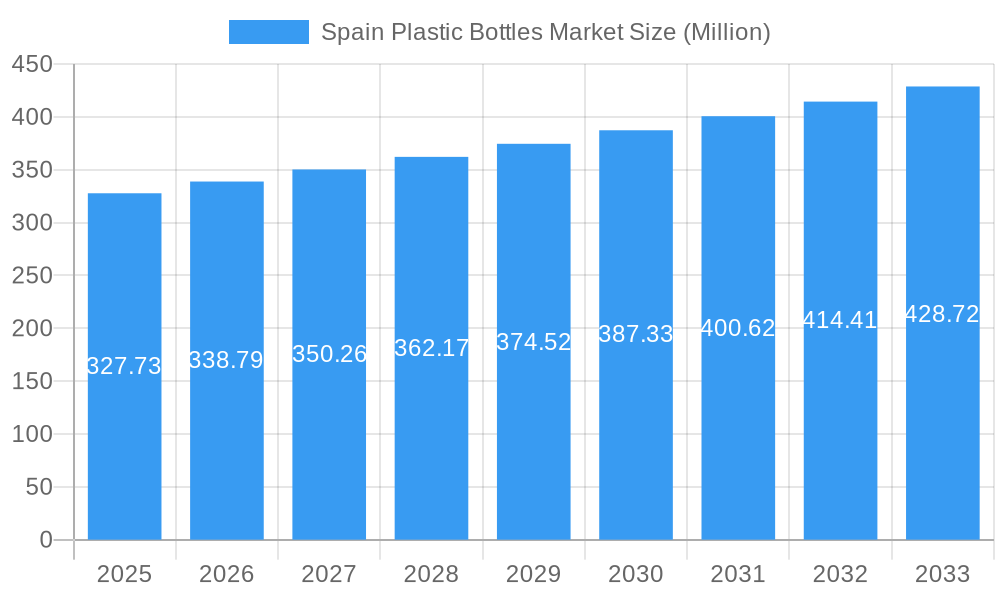

The Spanish plastic bottles market is poised for steady growth, projected to reach a significant valuation of approximately EUR 327.73 million. This expansion is underpinned by a Compound Annual Growth Rate (CAGR) of 3.39% over the forecast period of 2025-2033. The market's vitality is driven by sustained demand across key end-user industries, particularly food and beverage, which represent a substantial portion of plastic bottle consumption. Within the beverage sector, bottled water and carbonated soft drinks are leading segments, benefiting from evolving consumer preferences for convenience and portability. The pharmaceutical and personal care industries also contribute to market demand, driven by stringent packaging requirements and the growing trend of single-use and travel-sized products. Furthermore, increasing urbanization and a rising middle class in Spain continue to fuel the consumption of packaged goods, indirectly boosting the plastic bottles market.

Spain Plastic Bottles Market Market Size (In Million)

The market's trajectory is also influenced by ongoing trends such as the development of innovative lightweight bottle designs aimed at reducing material usage and transportation costs. Advances in recycling technologies and the increasing adoption of recycled PET (rPET) are also shaping the market, aligning with growing environmental consciousness and regulatory pressures. However, the market faces certain restraints, including fluctuating raw material prices, particularly for resins like Polyethylene (PE), Polyethylene Terephthalate (PET), and Polypropylene (PP), which can impact manufacturing costs. Growing environmental concerns and stricter regulations surrounding single-use plastics, though driving innovation in sustainable alternatives, can also pose challenges. Despite these factors, the strategic focus on sustainability, coupled with the inherent versatility and cost-effectiveness of plastic bottles, ensures a robust outlook for the Spanish market. The competitive landscape features a mix of established global players and agile domestic manufacturers, all vying for market share through product innovation and strategic partnerships.

Spain Plastic Bottles Market Company Market Share

Spain Plastic Bottles Market: In-Depth Analysis & Future Outlook (2019-2033)

This comprehensive report delves into the dynamic Spain Plastic Bottles Market, providing a detailed analysis of market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, and future opportunities. Covering the historical period of 2019-2024 and a robust forecast period extending to 2033, with a base year of 2025, this study offers critical insights for stakeholders seeking to navigate the complexities of the Spanish packaging sector. We meticulously examine key segments including Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), and Other Resins, alongside crucial end-user industries such as Food, Beverage (Bottled Water, Carbonated Soft Drinks, Alcoholic Beverages, Juices and Energy Drinks, Other Beverages), Pharmaceuticals, Personal Care and Toiletries, Industrial, Household Chemicals, Paints and Coatings, and Other End-user Industries. This report also features a detailed Competitor Analysis, including a Heat Map Analysis and distinctions between emerging and established players, along with an exhaustive list of major market participants.

Spain Plastic Bottles Market Market Composition & Trends

The Spain Plastic Bottles Market exhibits a moderately concentrated landscape, influenced by evolving consumer preferences and stringent environmental regulations. Innovation is a significant catalyst, with manufacturers focusing on sustainable plastic bottles, recycled PET (rPET) solutions, and lightweighting technologies to reduce material usage and carbon footprint. The regulatory environment is increasingly pushing for circular economy principles, impacting raw material sourcing and end-of-life management for plastic packaging. The presence of substitute products, such as glass and metal containers, necessitates a continuous focus on cost-effectiveness and functional superiority for plastic alternatives. End-user profiles are diverse, with the beverage and food sectors leading consumption, followed by pharmaceuticals and personal care. Mergers and acquisitions (M&A) activities are strategically shaping the market, with companies acquiring competitors or investing in sustainable technologies to enhance their market share and operational capabilities. For instance, the estimated M&A deal value for sustainability-focused acquisitions is projected to be in the range of EUR 150-250 Million, reflecting a strong trend. Market share distribution is dynamic, with PET holding the largest segment, estimated at around 60% of the total market value in 2025, primarily driven by its extensive use in the beverage industry.

Spain Plastic Bottles Market Industry Evolution

The Spain Plastic Bottles Market has undergone significant evolution, driven by a confluence of technological advancements, shifting consumer demands for sustainability, and evolving regulatory frameworks. Over the historical period (2019-2024), the market experienced a steady growth trajectory, estimated at an average annual growth rate (AAGR) of approximately 3.5%. This growth was underpinned by the increasing consumption of packaged goods, particularly in the beverage and food sectors, where plastic bottles offer a cost-effective, lightweight, and durable packaging solution. Technological advancements in PET bottle manufacturing, including improvements in injection molding and blow molding techniques, have enabled the production of more sophisticated and thinner-walled bottles, leading to material savings and enhanced product appeal. The adoption of recycled PET (rPET) has accelerated considerably, spurred by both corporate sustainability goals and consumer pressure. By the base year of 2025, the adoption rate of rPET in beverage bottles is estimated to reach 35%, a significant increase from just 15% in 2019. Consumer preferences have demonstrably shifted towards brands that prioritize environmental responsibility. This has compelled manufacturers and brand owners to invest in eco-friendly packaging solutions, including bio-based plastics and enhanced recyclability. The regulatory landscape has also played a pivotal role, with the introduction of Extended Producer Responsibility (EPR) schemes and targets for recycled content in plastic packaging, creating a favorable environment for sustainable innovation and investment. The forecast period (2025-2033) is expected to witness continued expansion, with an estimated AAGR of 4.2%, driven by further advancements in material science, increased investment in recycling infrastructure, and a growing consumer awareness of the environmental impact of packaging choices.

Leading Regions, Countries, or Segments in Spain Plastic Bottles Market

Within the Spain Plastic Bottles Market, the Beverage end-user industry stands as the dominant segment, accounting for an estimated 55% of the market value in 2025. This dominance is largely attributable to the high per capita consumption of bottled water and carbonated soft drinks in Spain.

Beverage Segment Dominance:

- Bottled Water: Spain's strong demand for convenient and portable hydration options makes bottled water a cornerstone of the plastic bottle market. Market share for bottled water is estimated at 25% of the total beverage segment.

- Carbonated Soft Drinks (CSDs): CSDs remain a significant consumer of plastic bottles, with PET being the preferred resin due to its clarity, strength, and cost-effectiveness. CSDs represent approximately 20% of the beverage plastic bottle market.

- Juices and Energy Drinks: These sub-segments are also substantial contributors, driven by health and wellness trends and the demand for convenient on-the-go beverages.

Resin Trends:

- Polyethylene Terephthalate (PET): This resin reigns supreme in the Spain Plastic Bottles Market, estimated to hold a market share of approximately 62% in 2025. Its versatility, clarity, barrier properties, and recyclability make it ideal for a wide range of beverage and food applications. Investment trends in PET recycling infrastructure are projected to exceed EUR 50 Million by 2027, further solidifying its position.

- Polyethylene (PE): Primarily used for household chemicals and personal care products, PE accounts for around 20% of the market. High-Density Polyethylene (HDPE) is a key variant within this segment.

- Polypropylene (PP): While less dominant than PET and PE, PP finds applications in specific food packaging and industrial uses, holding an estimated 10% market share.

Regional Insights (Implied): While this report focuses on the national market, it's important to note that major consumption hubs within Spain, such as Catalonia and Madrid, are significant drivers of demand for plastic bottles, supported by robust logistics and distribution networks. Regulatory support for recycling initiatives is also a key driver in regions actively pursuing circular economy goals.

Spain Plastic Bottles Market Product Innovations

Product innovation in the Spain Plastic Bottles Market is sharply focused on enhancing sustainability and functionality. Manufacturers are increasingly developing bottles with higher percentages of recycled PET (rPET), achieving up to 100% recycled content in some beverage applications. Advancements in lightweighting technologies have led to bottles with reduced wall thickness, thereby decreasing material consumption without compromising structural integrity. Furthermore, the introduction of tethered caps, mandated by European regulations, is a significant innovation aimed at improving recyclability and reducing plastic litter. Companies are also exploring bio-based plastic alternatives and improved barrier coatings to extend product shelf life, further differentiating their offerings in a competitive market.

Propelling Factors for Spain Plastic Bottles Market Growth

Several key factors are propelling the growth of the Spain Plastic Bottles Market. The expanding food and beverage sector, driven by increasing consumer demand for convenient and portable products, is a primary growth engine. Technological advancements in plastic bottle manufacturing, leading to more efficient and sustainable production processes, further bolster market expansion. Furthermore, supportive government regulations and initiatives promoting recycling and the use of recycled plastic are creating a favorable ecosystem for growth. The growing consumer awareness regarding environmental issues is also a significant driver, pushing brands to adopt more sustainable packaging solutions. The forecast indicates a continued upward trend, with an estimated market value of EUR 4,500 Million by 2028.

Obstacles in the Spain Plastic Bottles Market Market

Despite robust growth prospects, the Spain Plastic Bottles Market faces several obstacles. Stringent environmental regulations, while promoting sustainability, can also increase operational costs for manufacturers in terms of compliance and investment in new technologies. Fluctuations in the price of raw materials, particularly virgin resins like PET, can impact profitability and pricing strategies. Supply chain disruptions, exacerbated by geopolitical events or logistical challenges, can lead to production delays and increased costs. Furthermore, intense competition within the market, coupled with the growing availability of alternative packaging materials, necessitates continuous innovation and cost optimization. The public perception of plastic as an environmental hazard, despite advancements in recycling, also presents a reputational challenge.

Future Opportunities in Spain Plastic Bottles Market

The Spain Plastic Bottles Market is poised to capitalize on several emerging opportunities. The increasing demand for sustainable packaging solutions, particularly rPET and bio-based plastics, presents a significant growth avenue. The expansion of recycling infrastructure and collection schemes across Spain will further support the circular economy and increase the availability of recycled materials. Innovation in smart packaging, incorporating features like enhanced traceability and tamper-evidence, is another promising area. Furthermore, the growing trend of personalized and premium beverage offerings will likely drive demand for specialized and aesthetically pleasing plastic bottles. Exploring untapped potential in niche end-user industries, such as specialized industrial chemicals, could also unlock new markets. The market is projected to reach EUR 5,200 Million by 2030.

Major Players in the Spain Plastic Bottles Market Ecosystem

- Amcor Group Gmbh

- Berry Global Inc

- Alpla Group

- Gerresheimer AG

- Alcion Packaging Solutions SL

- Berlin Packaging

- Urola Packaging

- Caiba Packaging

- Frapak Packaging

- Pascual i Eduardo SL

Key Developments in Spain Plastic Bottles Market Industry

May 2024: Nestlé Spain's Water division announced its aim to ensure that by 2025, at least 50% of the PET plastic used in its bottle production will be recycled. To advance this initiative, the 'Nestlé Aquarel' formats of 0.75 cl and 1.5 l, previously using 50% rPET, are set toward the transition to 100% recycled plastic. Consequently, this year, Nestlé Spain plans to incorporate over 2,600 tons of rPET across its water formats. These bottles are produced at Nestlé’s bottling plants located in Herrera del Duque (Badajoz) and Arbúcies (Girona), both of which have been certified to the Alliance for Water Stewardship (AWS) standard for several years. This development significantly boosts the adoption of rPET and highlights the commitment to sustainable water bottling.

May 2024: PepsiCo's beverage plant in Northern Spain was on track to become the company's first global facility to achieve net-zero emissions by 2025. This achievement was made possible through the electrification of its operations, leading to the elimination of 1,849 tonnes of CO2 annually. Over the past five years, the plant has invested EUR 27 million (USD 29.54) in innovation and sustainability projects. These efforts align with PepsiCo Positive’s strategy, emphasizing a positive value chain and a comprehensive strategic transformation. This milestone comes on the heels of Spain's 2021 introduction of 100% recycled plastic bottles across the entire Pepsi range and a novel cardboard solution for can grouping. Moreover, Spain piloted tethered caps a year ahead of the European regulation. This signifies a major stride towards decarbonization and sustainable packaging within the beverage industry.

Strategic Spain Plastic Bottles Market Market Forecast

The strategic forecast for the Spain Plastic Bottles Market indicates sustained and robust growth, driven by an increasing demand for convenient packaging in the food and beverage sectors and a strong push towards sustainability. Key growth catalysts include the ongoing adoption of recycled PET (rPET), spurred by regulatory mandates and corporate social responsibility initiatives. Investments in advanced recycling technologies and infrastructure are expected to further enhance the circularity of plastic packaging. The market's potential is further amplified by innovation in lightweighting and bio-based materials, catering to environmentally conscious consumers. Emerging trends in specialized packaging for niche beverage categories and pharmaceuticals will also contribute to market expansion, ensuring a positive outlook for stakeholders investing in sustainable and innovative plastic bottle solutions. The market is projected to reach EUR 5,800 Million by 2033.

Spain Plastic Bottles Market Segmentation

-

1. Resin

- 1.1. Polyethylene (PE)

- 1.2. Polyethylene Terephthalate (PET)

- 1.3. Polypropylene (PP)

- 1.4. Other Re

-

2. End-user Industry

- 2.1. Food

-

2.2. Beverage

- 2.2.1. Bottled Water

- 2.2.2. Carbonated Soft Drinks

- 2.2.3. Alcoholic Beverages

- 2.2.4. Juices and Energy Drinks

- 2.2.5. Other Beverages

- 2.3. Pharmaceuticals

- 2.4. Personal Care and Toiletries

- 2.5. Industrial

- 2.6. Household Chemicals

- 2.7. Paints and Coatings

- 2.8. Other End-user Industries

Spain Plastic Bottles Market Segmentation By Geography

- 1. Spain

Spain Plastic Bottles Market Regional Market Share

Geographic Coverage of Spain Plastic Bottles Market

Spain Plastic Bottles Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Polyethylene (PE)

- 5.1.2. Polyethylene Terephthalate (PET)

- 5.1.3. Polypropylene (PP)

- 5.1.4. Other Re

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food

- 5.2.2. Beverage

- 5.2.2.1. Bottled Water

- 5.2.2.2. Carbonated Soft Drinks

- 5.2.2.3. Alcoholic Beverages

- 5.2.2.4. Juices and Energy Drinks

- 5.2.2.5. Other Beverages

- 5.2.3. Pharmaceuticals

- 5.2.4. Personal Care and Toiletries

- 5.2.5. Industrial

- 5.2.6. Household Chemicals

- 5.2.7. Paints and Coatings

- 5.2.8. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. Spain Plastic Bottles Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Polyethylene (PE)

- 6.1.2. Polyethylene Terephthalate (PET)

- 6.1.3. Polypropylene (PP)

- 6.1.4. Other Re

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Food

- 6.2.2. Beverage

- 6.2.2.1. Bottled Water

- 6.2.2.2. Carbonated Soft Drinks

- 6.2.2.3. Alcoholic Beverages

- 6.2.2.4. Juices and Energy Drinks

- 6.2.2.5. Other Beverages

- 6.2.3. Pharmaceuticals

- 6.2.4. Personal Care and Toiletries

- 6.2.5. Industrial

- 6.2.6. Household Chemicals

- 6.2.7. Paints and Coatings

- 6.2.8. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amcor Group Gmbh

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Global Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Alpla Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gerresheimer AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Alcion Packaging Solutions SL

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Berlin Packaging

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Urola Packaging

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Caiba Packaging

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Frapak Packaging

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Pascual i Eduardo SL7 2 Heat Map Analysis7 3 Competitor Analysis - Emerging vs Established Player

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Amcor Group Gmbh

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Plastic Bottles Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Spain Plastic Bottles Market Share (%) by Company 2025

List of Tables

- Table 1: Spain Plastic Bottles Market Revenue Million Forecast, by Resin 2020 & 2033

- Table 2: Spain Plastic Bottles Market Volume Million Forecast, by Resin 2020 & 2033

- Table 3: Spain Plastic Bottles Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Spain Plastic Bottles Market Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 5: Spain Plastic Bottles Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Spain Plastic Bottles Market Volume Million Forecast, by Region 2020 & 2033

- Table 7: Spain Plastic Bottles Market Revenue Million Forecast, by Resin 2020 & 2033

- Table 8: Spain Plastic Bottles Market Volume Million Forecast, by Resin 2020 & 2033

- Table 9: Spain Plastic Bottles Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 10: Spain Plastic Bottles Market Volume Million Forecast, by End-user Industry 2020 & 2033

- Table 11: Spain Plastic Bottles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Spain Plastic Bottles Market Volume Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Plastic Bottles Market?

The projected CAGR is approximately 3.39%.

2. Which companies are prominent players in the Spain Plastic Bottles Market?

Key companies in the market include Amcor Group Gmbh, Berry Global Inc, Alpla Group, Gerresheimer AG, Alcion Packaging Solutions SL, Berlin Packaging, Urola Packaging, Caiba Packaging, Frapak Packaging, Pascual i Eduardo SL7 2 Heat Map Analysis7 3 Competitor Analysis - Emerging vs Established Player.

3. What are the main segments of the Spain Plastic Bottles Market?

The market segments include Resin, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 327.73 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Lightweight Packaging Methods; Changing Demographic and Lifestyle Factors.

6. What are the notable trends driving market growth?

Rising Demand From Beverage Sector.

7. Are there any restraints impacting market growth?

Increasing Adoption of Lightweight Packaging Methods; Changing Demographic and Lifestyle Factors.

8. Can you provide examples of recent developments in the market?

May 2024: Nestlé Spain's Water division announced its aim to ensure that by 2025, at least 50% of the PET plastic used in its bottle production will be recycled. To advance this initiative, the 'Nestlé Aquarel' formats of 0.75 cl and 1.5 l, previously using 50% rPET, are set toward the transition to 100% recycled plastic. Consequently, this year, Nestlé Spain plans to incorporate over 2,600 tons of rPET across its water formats. These bottles are produced at Nestlé’s bottling plants located in Herrera del Duque (Badajoz) and Arbúcies (Girona), both of which have been certified to the Alliance for Water Stewardship (AWS) standard for several years.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Plastic Bottles Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Plastic Bottles Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Plastic Bottles Market?

To stay informed about further developments, trends, and reports in the Spain Plastic Bottles Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence