Key Insights

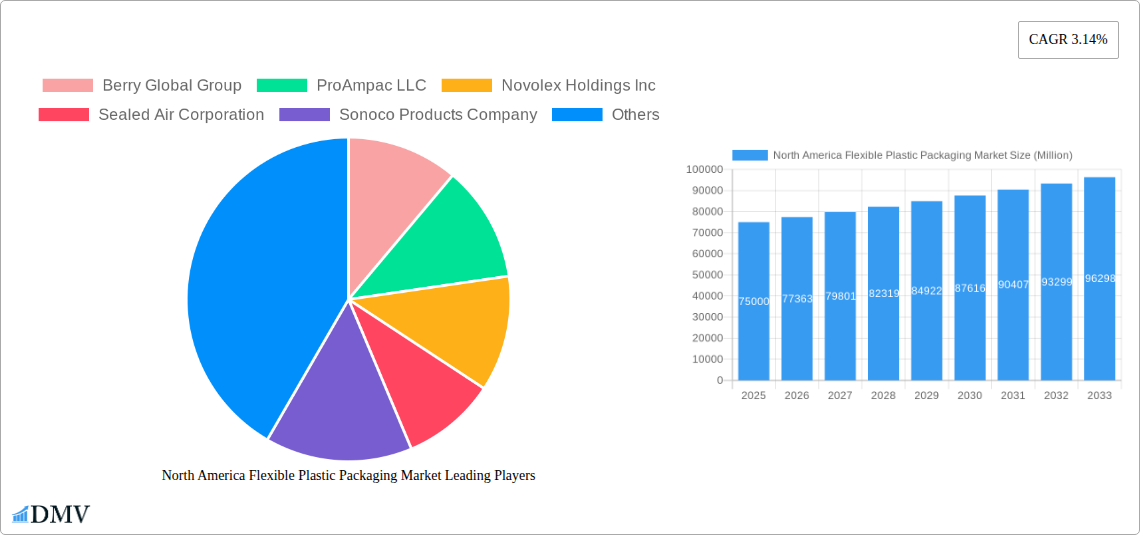

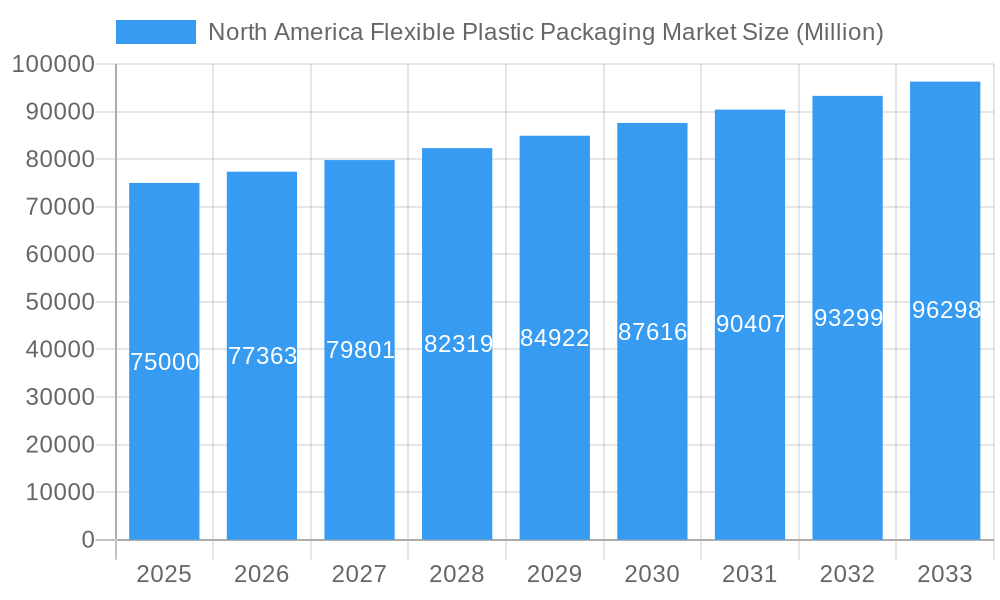

The North America Flexible Plastic Packaging Market is poised for robust growth, projected to reach an estimated market size of USD 75,000 million in 2025. This expansion is driven by a Compound Annual Growth Rate (CAGR) of 3.14%, indicating sustained and healthy market development throughout the forecast period of 2025-2033. The market's dynamism is fueled by several key factors, including the increasing demand for convenient and sustainable packaging solutions across various end-user industries. The food and beverage sector, in particular, remains a dominant force, leveraging flexible packaging for its ability to extend shelf life, enhance product presentation, and offer portability for consumers. Furthermore, the growing emphasis on lightweight and resource-efficient packaging aligns with environmental consciousness, further bolstering the adoption of flexible plastic alternatives. The medical and pharmaceutical industries are also contributing significantly to market expansion, driven by the need for sterile, tamper-evident, and easy-to-handle packaging for sensitive products.

North America Flexible Plastic Packaging Market Market Size (In Billion)

The competitive landscape of the North America Flexible Plastic Packaging Market is characterized by the presence of major global players and a host of specialized manufacturers. Companies like Berry Global Group, ProAmpac LLC, Novolex Holdings Inc, Sealed Air Corporation, and Amcor Group GmbH are at the forefront, investing in innovation and expanding their production capacities. The market is segmented across diverse material types, with Polyethene (PE) and Bi-oriented Polypropylene (BOPP) dominating due to their versatility, cost-effectiveness, and excellent barrier properties. Pouches and bags represent the leading product types, catering to a wide array of consumer and industrial needs. While the market enjoys strong growth, potential restraints include fluctuating raw material prices and increasing regulatory scrutiny concerning plastic waste management. However, the ongoing development of advanced, recyclable, and compostable flexible packaging materials is expected to mitigate these challenges, ensuring continued market vitality.

North America Flexible Plastic Packaging Market Company Market Share

North America Flexible Plastic Packaging Market: In-depth Analysis and Forecast (2019-2033)

This comprehensive market research report offers an in-depth analysis of the North America flexible plastic packaging market, providing critical insights into its current landscape, historical trends, and future trajectory. Covering the period from 2019 to 2033, with a base year of 2025, this report is an essential resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and navigate challenges in this rapidly evolving sector. We delve into key segments, leading players, technological advancements, and the economic and regulatory factors shaping the future of flexible plastic packaging across the region.

North America Flexible Plastic Packaging Market Market Composition & Trends

The North America flexible plastic packaging market is characterized by a moderately concentrated competitive landscape, with key players like Amcor Group GmbH, Berry Global Group, and Sealed Air Corporation holding significant market shares. Innovation is a primary catalyst for growth, driven by an increasing demand for sustainable packaging solutions and advanced functionalities. Regulatory landscapes, particularly concerning recyclability and the reduction of single-use plastics, are influencing material choices and product design. Substitute products, such as rigid packaging and paper-based alternatives, pose a competitive threat, though flexible packaging's superior barrier properties and cost-effectiveness often prevail. End-user profiles are diverse, with the food and beverage sector being the largest consumer, followed by personal care and medical applications. Mergers and acquisitions (M&A) are prevalent, with deal values in the tens to hundreds of millions of dollars, aimed at consolidating market presence, acquiring new technologies, and expanding product portfolios.

- Market Share Distribution: Dominant players account for approximately 55-65% of the market.

- Innovation Focus: Sustainability, extended shelf-life, and enhanced convenience.

- Key M&A Drivers: Market consolidation, technological integration, and geographic expansion.

- Estimated M&A Deal Value Range: $50 Million - $300 Million per significant transaction.

North America Flexible Plastic Packaging Market Industry Evolution

The North America flexible plastic packaging market has witnessed a remarkable evolution over the historical period (2019-2024) and is projected to continue its robust growth trajectory through the forecast period (2025-2033). This expansion is underpinned by several interconnected factors, including escalating consumer demand for convenience and product preservation, coupled with significant technological advancements in material science and manufacturing processes. The industry's ability to adapt to shifting consumer preferences, particularly the growing emphasis on sustainability and environmental responsibility, has been crucial to its sustained development.

Technological advancements have played a pivotal role in shaping the market. Innovations in polymer science have led to the development of high-performance films with enhanced barrier properties, improved puncture resistance, and extended shelf life, directly addressing the needs of diverse end-user industries like food, beverage, and pharmaceuticals. For instance, the adoption of multilayered structures incorporating materials like Ethylene Vinyl Alcohol (EVOH) has dramatically improved gas and moisture barrier capabilities, reducing food spoilage and waste. Furthermore, advancements in printing technologies, such as high-definition gravure and digital printing, allow for sophisticated branding and customization, appealing to brand owners seeking to differentiate their products.

The shifting consumer demands have been a powerful propellant for this evolution. There's a discernible trend towards smaller, on-the-go packaging formats, driving the demand for pouches and sachets. Simultaneously, a growing awareness of environmental impact has spurred the development and adoption of recyclable, compostable, and bio-based flexible packaging solutions. This has led to increased investment in research and development for these sustainable alternatives. The market has also responded to the need for packaging that offers enhanced safety and hygiene, particularly evident in the medical and pharmaceutical sectors, where stringent regulatory requirements necessitate advanced sterilization and tamper-evident features. The overall growth rate of the North America flexible plastic packaging market has been consistently above 4.5% annually, with projections indicating a sustained growth rate of approximately 5.0% through 2033. Adoption metrics for recyclable materials, while still developing, are showing an upward trend, with a projected increase of 15-20% by 2028.

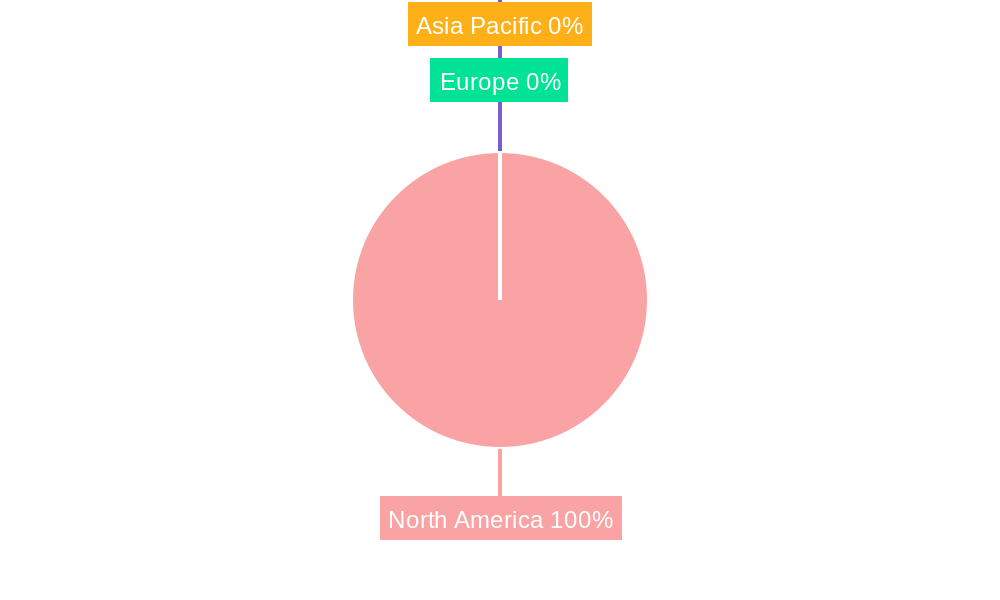

Leading Regions, Countries, or Segments in North America Flexible Plastic Packaging Market

The North America flexible plastic packaging market is largely dominated by the United States, driven by its expansive consumer base, robust manufacturing sector, and high per capita consumption of packaged goods. Within the United States, particular states with significant food processing, beverage production, and pharmaceutical manufacturing hubs exhibit the highest demand. The dominance of the United States is further amplified by its early adoption of innovative packaging technologies and its proactive approach to regulatory frameworks that, while sometimes challenging, also spur innovation in sustainable solutions.

Across the various segments, Polyethene (PE) emerges as the leading material type due to its versatility, cost-effectiveness, and wide range of applications. PE, particularly Low-Density Polyethylene (LDPE) and Linear Low-Density Polyethylene (LLDPE), is extensively used in films and bags for its excellent flexibility and moisture barrier properties. The Food end-user industry represents the largest segment, consuming a significant portion of flexible plastic packaging for products ranging from frozen foods and dry goods to meat, poultry, seafood, and dairy. The demand within the food segment is further diversified by specific sub-categories like Meat, Poultry, and Sea Food and Frozen Foods, which require superior barrier properties to maintain product freshness and extend shelf life.

In terms of product type, Films and Wraps constitute the largest share, serving a multitude of applications across industries. However, Pouches are experiencing robust growth, driven by consumer preference for convenience, resealability, and portion control, especially in the food and personal care sectors. The increasing popularity of stand-up pouches and retort pouches for ready-to-eat meals and beverages underscores this trend.

- Dominant Country: United States, accounting for over 70% of the regional market share.

- Key Material Type Drivers:

- Polyethene (PE): Cost-effectiveness, versatility, high demand in films and bags. Investment trends in high-barrier PE grades are increasing.

- Bi-oriented Polypropylene (BOPP): Excellent printability, clarity, and stiffness, crucial for confectionery and snack packaging.

- Dominant End-user Industry Drivers:

- Food: Largest consumer. Drivers include population growth, evolving dietary habits, and demand for convenience foods. Regulatory support for food safety and extended shelf life fuels adoption.

- Meat, Poultry, and Sea Food: High demand for vacuum packaging and modified atmosphere packaging, requiring specialized PE and EVOH films.

- Frozen Foods: Critical need for moisture and oxygen barriers, driving innovation in PE and multilayer films.

- Key Product Type Growth Factors:

- Pouches: Growing consumer preference for convenience, resealability, and single-serving options. Investment in pouch-filling machinery is high.

- Films and Wraps: Continued dominance due to their application in primary and secondary packaging across numerous sectors.

- Investment Trends: Significant investments in advanced extrusion and lamination technologies for high-performance and sustainable flexible packaging.

North America Flexible Plastic Packaging Market Product Innovations

Product innovations in the North America flexible plastic packaging market are heavily focused on enhancing sustainability and performance. Leading companies are developing advanced recyclable mono-material structures, such as mono-PE and mono-PP pouches, designed to meet stringent recycling infrastructure requirements. Innovations also include the integration of active and intelligent packaging features, such as oxygen scavengers and moisture regulators, to significantly extend product shelf life and reduce spoilage. Performance metrics like improved puncture resistance (up to 20% higher in new formulations) and superior barrier properties against oxygen and moisture (achieving 0.1 cc/m²/day for oxygen transmission) are key selling points. Furthermore, the development of thinner yet stronger films is contributing to material reduction and cost savings.

Propelling Factors for North America Flexible Plastic Packaging Market Growth

The North America flexible plastic packaging market is propelled by several key factors. Technologically, advancements in material science have led to the development of high-barrier, lightweight, and recyclable films, enhancing product protection and sustainability credentials. Economically, the growing demand for convenience and on-the-go consumption, particularly in the food and beverage sectors, fuels the need for versatile and user-friendly packaging solutions. Regulatory influences, while sometimes posing challenges, also drive innovation, pushing manufacturers towards more sustainable and compliant packaging options. The increasing disposable income and evolving lifestyles of consumers further contribute to the demand for packaged goods, indirectly benefiting the flexible packaging sector.

Obstacles in the North America Flexible Plastic Packaging Market Market

Despite its robust growth, the North America flexible plastic packaging market faces significant obstacles. Regulatory challenges, including evolving legislation around plastic waste and Extended Producer Responsibility (EPR) schemes, create uncertainty and necessitate costly adaptations. Supply chain disruptions, exacerbated by global events, can lead to raw material price volatility and shortages, impacting production costs and lead times. Competitive pressures from alternative packaging materials and the ongoing public perception challenges surrounding plastic waste also present barriers. Quantifiable impacts include potential cost increases of 5-10% due to regulatory compliance and intermittent material shortages affecting production schedules by up to 15%.

Future Opportunities in North America Flexible Plastic Packaging Market

Emerging opportunities in the North America flexible plastic packaging market lie in the burgeoning demand for sustainable packaging solutions, including compostable and bio-based alternatives, which are projected to witness double-digit growth. The expansion of e-commerce presents a significant opportunity, requiring specialized, durable, and lightweight packaging for shipping. Technological advancements in smart packaging, such as those incorporating QR codes for traceability and sensors for freshness monitoring, offer avenues for value-added products. Furthermore, the increasing focus on health and wellness is driving demand for specialized pharmaceutical and medical packaging with enhanced barrier and sterilization properties.

Major Players in the North America Flexible Plastic Packaging Market Ecosystem

- Berry Global Group

- ProAmpac LLC

- Novolex Holdings Inc

- Sealed Air Corporation

- Sonoco Products Company

- American Packaging Corporation

- Printpack Inc

- Sigma Plastics Group Inc

- Amcor Group GmbH

- Constantia Flexibles Group GmbH

- Winpak Co Limited

- Mondi PLC

- Uflex Limited

- Transcontinental Inc

- PPC Flex Company Inc

- C-P Flexible Packaging

- ePac Holdings LL

Key Developments in North America Flexible Plastic Packaging Market Industry

- January 2024: ProAmpac LLC announced the collaboration with Aptar CSP Technologies to launch ProActive Intelligence Moisture Protect (MP-1000), which will eliminate the need for desiccant packets. It will help the company lower the moisture level in the packaging headspace, making it ideal for applications for products that require optimal moisture control, enhancing product shelf-life and reducing waste.

- November 2023: NOVA Chemicals Corporation, a Canadian petrochemical company, notified the ink of a partnership with a key global packaging firm, Amcor Group GmbH, to supply mechanically recycled polyethylene resin (rPE) for manufacture in flexible packaging films by the latter. Increasing the use of recycled polyester (rPE) in flexible packaging is a key component of Amcor's circularity strategy. Such constant developments toward sustainability across the country would drive the demand for flexible plastic packaging across the region, emphasizing a move towards a circular economy.

Strategic North America Flexible Plastic Packaging Market Market Forecast

The strategic forecast for the North America flexible plastic packaging market anticipates continued robust growth, driven by escalating consumer demand for convenience and product preservation, alongside a strong push towards sustainable packaging solutions. Key growth catalysts include ongoing innovation in recyclable materials, the adoption of advanced barrier technologies to extend shelf life and reduce food waste, and the increasing integration of smart packaging features for enhanced traceability and consumer engagement. The market's ability to adapt to evolving regulatory landscapes and its capacity to meet the stringent requirements of diverse end-user industries, particularly food, beverage, and healthcare, will be critical. The estimated market size is projected to reach approximately $45,000 Million to $50,000 Million by 2033, with a Compound Annual Growth Rate (CAGR) of around 5.0% during the forecast period.

North America Flexible Plastic Packaging Market Segmentation

-

1. Material Type

- 1.1. Polyethene (PE)

- 1.2. Bi-oriented Polypropylene (BOPP)

- 1.3. Cast Polypropylene (CPP)

- 1.4. Polyvinyl Chloride (PVC)

- 1.5. Ethylene Vinyl Alcohol (EVOH)

- 1.6. Other Ma

-

2. Product Type

- 2.1. Pouches

- 2.2. Bags

- 2.3. Films and Wraps

- 2.4. Other Product Types (Blister Packs, Liners, etc.)

-

3. End-user Industry

-

3.1. Food

- 3.1.1. Frozen Foods

- 3.1.2. Dry Foods

- 3.1.3. Meat, Poultry, and Sea Food

- 3.1.4. Candy & Confectionery

- 3.1.5. Pet Food

- 3.1.6. Fresh Produce

- 3.1.7. Dairy Products

- 3.1.8. Other Fo

- 3.2. Beverage

- 3.3. Personal Care and Household Care

- 3.4. Medical and Pharmaceutical

- 3.5. Other En

-

3.1. Food

North America Flexible Plastic Packaging Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Flexible Plastic Packaging Market Regional Market Share

Geographic Coverage of North America Flexible Plastic Packaging Market

North America Flexible Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Polyethene (PE)

- 5.1.2. Bi-oriented Polypropylene (BOPP)

- 5.1.3. Cast Polypropylene (CPP)

- 5.1.4. Polyvinyl Chloride (PVC)

- 5.1.5. Ethylene Vinyl Alcohol (EVOH)

- 5.1.6. Other Ma

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Pouches

- 5.2.2. Bags

- 5.2.3. Films and Wraps

- 5.2.4. Other Product Types (Blister Packs, Liners, etc.)

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.1.1. Frozen Foods

- 5.3.1.2. Dry Foods

- 5.3.1.3. Meat, Poultry, and Sea Food

- 5.3.1.4. Candy & Confectionery

- 5.3.1.5. Pet Food

- 5.3.1.6. Fresh Produce

- 5.3.1.7. Dairy Products

- 5.3.1.8. Other Fo

- 5.3.2. Beverage

- 5.3.3. Personal Care and Household Care

- 5.3.4. Medical and Pharmaceutical

- 5.3.5. Other En

- 5.3.1. Food

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. North America Flexible Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Polyethene (PE)

- 6.1.2. Bi-oriented Polypropylene (BOPP)

- 6.1.3. Cast Polypropylene (CPP)

- 6.1.4. Polyvinyl Chloride (PVC)

- 6.1.5. Ethylene Vinyl Alcohol (EVOH)

- 6.1.6. Other Ma

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Pouches

- 6.2.2. Bags

- 6.2.3. Films and Wraps

- 6.2.4. Other Product Types (Blister Packs, Liners, etc.)

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.1.1. Frozen Foods

- 6.3.1.2. Dry Foods

- 6.3.1.3. Meat, Poultry, and Sea Food

- 6.3.1.4. Candy & Confectionery

- 6.3.1.5. Pet Food

- 6.3.1.6. Fresh Produce

- 6.3.1.7. Dairy Products

- 6.3.1.8. Other Fo

- 6.3.2. Beverage

- 6.3.3. Personal Care and Household Care

- 6.3.4. Medical and Pharmaceutical

- 6.3.5. Other En

- 6.3.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Berry Global Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ProAmpac LLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Novolex Holdings Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Sealed Air Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sonoco Products Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 American Packaging Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Printpack Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sigma Plastics Group Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Amcor Group GmbH

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Constantia Flexibles Group GmbH

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Winpak Co Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Mondi PLC

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Uflex Limited

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Transcontinental Inc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 PPC Flex Company Inc

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 C-P Flexible Packaging

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 ePac Holdings LL

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.1 Berry Global Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Flexible Plastic Packaging Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Flexible Plastic Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: North America Flexible Plastic Packaging Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: North America Flexible Plastic Packaging Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: North America Flexible Plastic Packaging Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: North America Flexible Plastic Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Flexible Plastic Packaging Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: North America Flexible Plastic Packaging Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: North America Flexible Plastic Packaging Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: North America Flexible Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States North America Flexible Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Flexible Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Flexible Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Flexible Plastic Packaging Market?

The projected CAGR is approximately 3.25%.

2. Which companies are prominent players in the North America Flexible Plastic Packaging Market?

Key companies in the market include Berry Global Group, ProAmpac LLC, Novolex Holdings Inc, Sealed Air Corporation, Sonoco Products Company, American Packaging Corporation, Printpack Inc, Sigma Plastics Group Inc, Amcor Group GmbH, Constantia Flexibles Group GmbH, Winpak Co Limited, Mondi PLC, Uflex Limited, Transcontinental Inc, PPC Flex Company Inc, C-P Flexible Packaging, ePac Holdings LL.

3. What are the main segments of the North America Flexible Plastic Packaging Market?

The market segments include Material Type, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 62.79 billion as of 2022.

5. What are some drivers contributing to market growth?

Expansion of the E-commerce Sector in the Region; Rising Demand for Barrier Packaging Solutions from the Food Industry.

6. What are the notable trends driving market growth?

Innovative Packaging Solutions are Driving the Market’s Growth due to the Demand from Frozen-Food Categories.

7. Are there any restraints impacting market growth?

Expansion of the E-commerce Sector in the Region; Rising Demand for Barrier Packaging Solutions from the Food Industry.

8. Can you provide examples of recent developments in the market?

January 2024: ProAmpac LLC announced the collaboration with Aptar CSP Technologies to launch ProActive Intelligence Moisture Protect (MP-1000), which will eliminate the need for desiccant packets. It will help the company lower the moisture level in the packaging headspace, making it ideal for applications for products that require optimal moisture control.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Flexible Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Flexible Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Flexible Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the North America Flexible Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence