Key Insights

The global Microcrystalline Cellulose (MCC) market is projected for substantial growth, reaching a market size of $1255.1 million by 2025, with a Compound Annual Growth Rate (CAGR) of 7.8%. This expansion is driven by increasing pharmaceutical demand for MCC as a key excipient, enhancing drug delivery and stability. The food sector also significantly contributes, utilizing MCC as a stabilizer, emulsifier, and texturizer. Emerging cosmetic applications, particularly in natural formulations, further stimulate market growth. Key drivers include the adoption of sustainable raw materials and advanced processing technologies that improve MCC functionality and purity.

Microcrystalline Cellulose Industry Market Size (In Billion)

Market dynamics are shaped by processing innovations leading to specialized MCC grades and a rising consumer preference for clean-label ingredients, boosting demand for wood-based MCC. Potential restraints include raw material price volatility and rigorous regulatory approvals. Geographically, the Asia Pacific region, led by China and India, is a major hub for MCC consumption and production due to expanding pharmaceutical and food processing industries. North America and Europe are significant markets, driven by established pharmaceutical sectors and a focus on high-purity excipients. Leading companies are investing in R&D and production to meet escalating global demand for this versatile cellulose derivative.

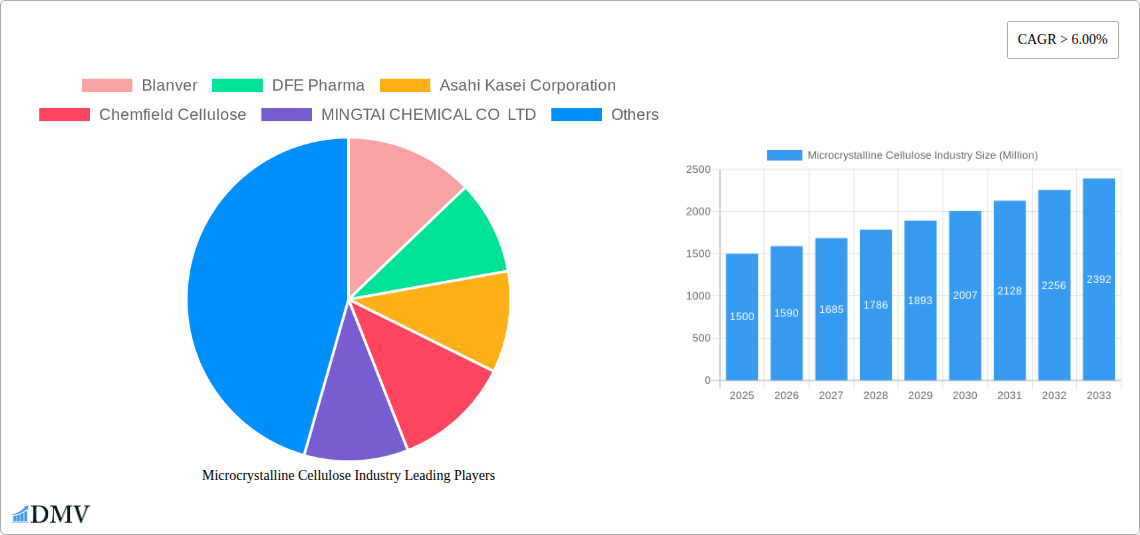

Microcrystalline Cellulose Industry Company Market Share

This report provides an SEO-optimized, insightful overview of the Microcrystalline Cellulose market, designed for maximum visibility and stakeholder engagement.

Microcrystalline Cellulose Industry Market Composition & Trends

The Microcrystalline Cellulose (MCC) industry is characterized by a moderately concentrated market, with key players like DuPont, J RETTENMAIER & SÖHNE GmbH + Co KG, and Asahi Kasei Corporation holding significant shares. Innovation is a primary catalyst, driven by the demand for high-purity, functional MCC grades for advanced pharmaceutical formulations and novel food applications. The regulatory landscape, particularly stringent quality control for excipients in the pharmaceutical sector, shapes market entry and product development. Substitute products, such as other cellulose derivatives and synthetic excipients, pose a competitive threat, but MCC's superior binding and disintegration properties offer a distinct advantage. End-user profiles are dominated by the pharmaceutical industry (over 50% market share), followed by food (approximately 30% market share) and cosmetics. The market has witnessed strategic M&A activities aimed at expanding product portfolios and geographical reach. For instance, recent acquisitions of specialty chemical distributors have strengthened market penetration. The overall market concentration is estimated at XXX, with the top five players accounting for approximately 60% of the global market. Merger and acquisition deal values have ranged from tens of millions to hundreds of millions of dollars, reflecting the industry's consolidation drive and pursuit of market leadership.

Microcrystalline Cellulose Industry Industry Evolution

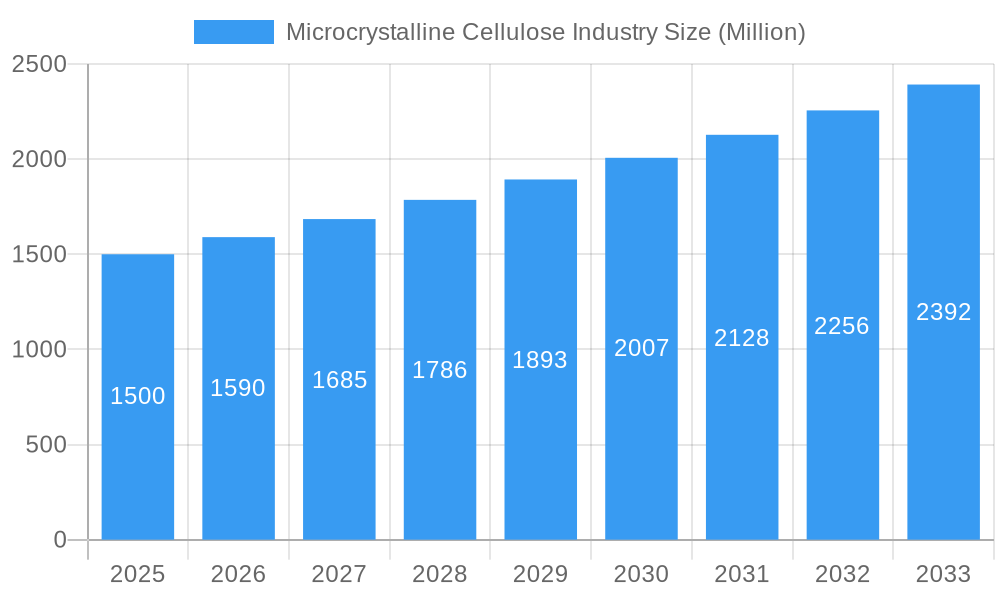

The Microcrystalline Cellulose (MCC) industry has experienced robust growth and significant evolution throughout the historical period of 2019–2024, and this trajectory is projected to continue through the forecast period of 2025–2033. The market growth has been consistently fueled by the escalating demand for high-quality excipients in the pharmaceutical sector, driven by the increasing prevalence of chronic diseases and the subsequent rise in drug manufacturing. Furthermore, the burgeoning food and beverage industry’s adoption of MCC as a functional ingredient for texture enhancement and fat replacement has also been a substantial growth contributor. Technological advancements have played a pivotal role in shaping the industry’s landscape. Innovations in processing techniques, such as the refinement of steam explosion and acid hydrolysis methods, have led to the production of MCC with improved particle size distribution, purity, and functionality, catering to more specialized applications. The transition towards more sustainable sourcing of raw materials, particularly from wood-based and non-wood-based cellulose, has also been a key evolutionary aspect. Consumer demands have shifted towards cleaner labels and natural ingredients, further boosting the appeal of MCC derived from plant sources. The estimated Compound Annual Growth Rate (CAGR) for the MCC market is predicted to be around 5.5% from 2025 to 2033. Adoption metrics for advanced MCC grades in novel drug delivery systems are showing an upward trend, with an estimated increase of 15% in the last two years. The global MCC market size is projected to reach approximately $3,000 million by 2025, demonstrating significant market expansion from its historical figures. The increasing focus on research and development for new applications, such as in nutraceuticals and biodegradable materials, is indicative of the industry's dynamic evolution and its capacity to adapt to changing market needs and technological frontiers.

Leading Regions, Countries, or Segments in Microcrystalline Cellulose Industry

The global Microcrystalline Cellulose (MCC) market's dominance is largely dictated by key segments and geographical regions, each exhibiting distinct growth drivers and adoption patterns. From a Source perspective, Wood-based MCC has traditionally held a significant market share, estimated at over 70%, due to the established infrastructure for pulp and paper production, providing a readily available and cost-effective raw material. However, Non-wood-based MCC, derived from sources like cotton linters and agricultural residues, is gaining traction due to sustainability concerns and the increasing demand for allergen-free ingredients, particularly in food and cosmetic applications.

In terms of Process, Acid Hydrolysis remains the most prevalent method for MCC production, accounting for approximately 60% of the market share. This is attributed to its established efficiency and cost-effectiveness for producing high-purity MCC. However, emerging processes like Reactive Extrusion and Enzyme Mediated methods are witnessing growing interest for their potential to produce MCC with tailored functionalities and reduced environmental impact. Steam Explosion is also gaining traction as a greener alternative.

The End-User Industry segmentation clearly highlights the Pharmaceutical sector as the undisputed leader, commanding an estimated market share exceeding 50%. This dominance is fueled by MCC's critical role as a binder, disintegrant, and filler in tablets and capsules, along with its excellent flowability and compressibility. The Food industry follows as the second-largest segment, contributing around 30% to the market, where MCC is utilized for texture improvement, anti-caking, and as a fat replacer. The Cosmetics sector, though smaller, is a growing market for MCC as a thickening agent and exfoliant.

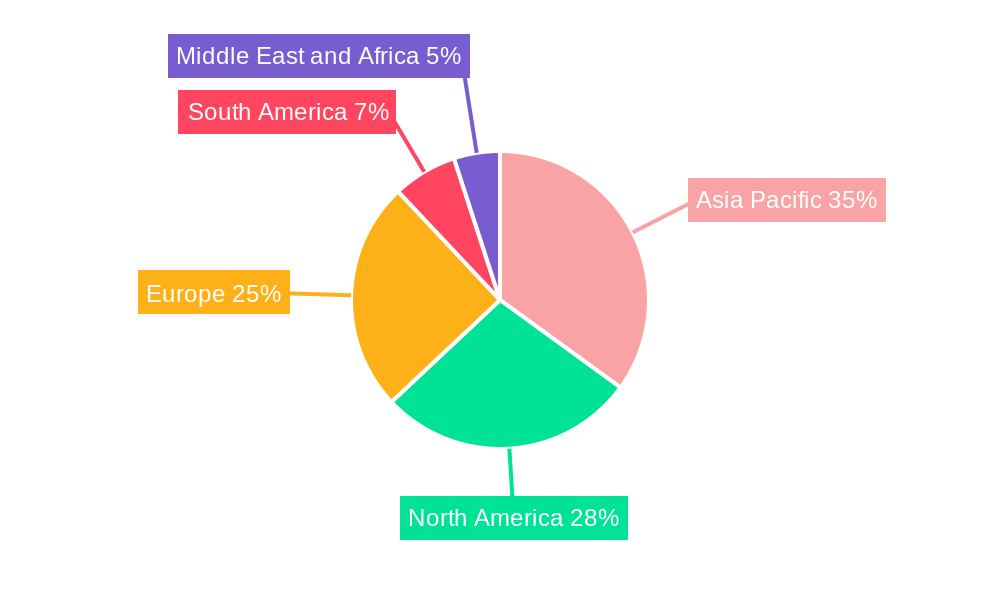

Geographically, North America and Europe have historically been leading regions due to their well-established pharmaceutical and food processing industries, robust regulatory frameworks, and high consumer spending power. These regions account for approximately 65% of the global MCC market. Investment trends in these regions are heavily focused on research and development for advanced pharmaceutical applications and sustainable production methods.

However, the Asia-Pacific region is emerging as the fastest-growing market, with an estimated CAGR of over 6% during the forecast period. This surge is attributed to the rapid expansion of the pharmaceutical and food industries in countries like China and India, coupled with increasing disposable incomes and a growing focus on healthcare and processed foods. Regulatory support in these emerging economies, coupled with a significant manufacturing base, is further propelling the region's dominance. Investment trends in APAC are geared towards expanding production capacities and adopting advanced manufacturing technologies to meet the escalating demand.

Microcrystalline Cellulose Industry Product Innovations

Product innovations in the Microcrystalline Cellulose (MCC) industry are primarily focused on enhancing functionality, purity, and sustainability. Companies are developing MCC grades with precisely controlled particle sizes and pore structures to optimize tablet disintegration and drug release profiles, crucial for advanced pharmaceutical formulations and controlled-release medications. For instance, silicified microcrystalline cellulose, such as DFE Pharma's Pharmacel MCC 90, offers improved flowability and compressibility, enabling direct compression techniques and reducing manufacturing steps. Furthermore, advancements in non-wood-based MCC production are yielding products with unique properties, addressing allergen concerns and appealing to the growing demand for natural ingredients in food and cosmetics. These innovations translate into higher tablet tensile strength, reduced tablet weight variation, and enhanced bioavailability of active pharmaceutical ingredients, leading to more effective and safer end products.

Propelling Factors for Microcrystalline Cellulose Industry Growth

Several key factors are propelling the growth of the Microcrystalline Cellulose (MCC) industry. The ever-expanding pharmaceutical sector, driven by an aging global population and the increasing prevalence of chronic diseases, remains the primary growth engine. MCC's indispensable role as a high-performance excipient in tablet manufacturing, offering superior binding, disintegration, and flow properties, ensures its sustained demand. Secondly, the growing consumer preference for natural and clean-label ingredients in the food industry significantly boosts MCC consumption as a texturizer, stabilizer, and emulsifier. Technological advancements in MCC processing, leading to improved purity and tailored functionalities, are enabling its application in more sophisticated products, from controlled-release drugs to advanced nutraceuticals. Furthermore, the rising disposable incomes and increasing healthcare expenditure in emerging economies are creating substantial market opportunities.

Obstacles in the Microcrystalline Cellulose Industry Market

Despite its robust growth, the Microcrystalline Cellulose (MCC) market faces certain obstacles. Volatile raw material prices, particularly for wood pulp, can impact production costs and profit margins. Stringent regulatory approvals for pharmaceutical-grade MCC in various regions can prolong market entry timelines and increase compliance expenses. Supply chain disruptions, exacerbated by geopolitical events and logistical challenges, can affect the availability and timely delivery of raw materials and finished products. Furthermore, the development of alternative excipients and innovative drug delivery systems that reduce the reliance on traditional MCC formulations poses a competitive threat. The increasing focus on sustainability also necessitates investment in eco-friendly production processes, which can be capital-intensive.

Future Opportunities in Microcrystalline Cellulose Industry

The future of the Microcrystalline Cellulose (MCC) industry is ripe with opportunities. The burgeoning nutraceutical and dietary supplement markets offer significant growth potential, as MCC serves as an excellent binder and filler for capsules and tablets. Advancements in biotechnology and green chemistry are paving the way for more sustainable and efficient MCC production methods, potentially from novel non-wood sources. The increasing demand for specialty MCC grades with tailored particle sizes and surface properties for advanced pharmaceutical applications, such as amorphous solid dispersions and orally disintegrating tablets, presents a lucrative niche. Furthermore, the expansion of healthcare infrastructure and pharmaceutical manufacturing in emerging economies in Asia-Pacific and Latin America will continue to drive demand for MCC. Exploring applications in biodegradable plastics and advanced materials also holds promising long-term potential.

Major Players in the Microcrystalline Cellulose Industry Ecosystem

- Blanver

- DFE Pharma

- Asahi Kasei Corporation

- Chemfield Cellulose

- MINGTAI CHEMICAL CO LTD

- JUKU ORCHEM PVT LTD

- Sigachi Industries Limited

- J RETTENMAIER & SÖHNE GmbH + Co KG

- DuPont

- GUJARAT MICROWAX PVT LTD

- VWR International LLC (Avantor Inc)

- Accent Microcell

- Huzhou City Linghu Xinwang Chemical Co Ltd

Key Developments in Microcrystalline Cellulose Industry Industry

- November 2022: DFE Pharma partnered with Azelis, a service provider in the specialty chemicals and food ingredients industry, for the distribution of its products in the EMEA region, expanding market reach and customer access.

- July 2021: DFE Pharma launched Pharmacel MCC 90, a silicified microcrystalline cellulose, to broaden its market product portfolio and offer enhanced flowability and compressibility benefits to its customers.

Strategic Microcrystalline Cellulose Industry Market Forecast

The strategic Microcrystalline Cellulose (MCC) market forecast indicates sustained growth driven by the unwavering demand from the pharmaceutical industry, which relies on MCC as a crucial excipient for tablet manufacturing. The increasing global focus on health and wellness, coupled with the rise of nutraceuticals, presents a significant expansion opportunity. Furthermore, the ongoing pursuit of sustainable and natural ingredients by consumers in the food and cosmetic sectors will continue to fuel the adoption of MCC. Technological advancements in processing, leading to more specialized and functional MCC grades, will unlock new application frontiers and enhance product performance. The growing healthcare expenditure and expanding pharmaceutical manufacturing capabilities in emerging economies are poised to be major growth catalysts, ensuring a robust market outlook for MCC in the coming years.

Microcrystalline Cellulose Industry Segmentation

-

1. Source

- 1.1. Wood-based

- 1.2. Non -wood-based

-

2. Process

- 2.1. Reactive Extrusion

- 2.2. Enzyme Mediated

- 2.3. Steam Explosion

- 2.4. Acid Hydrolysis

-

3. End-User Industry

- 3.1. Pharmaceutical

- 3.2. Food

- 3.3. Cosmetics

- 3.4. Other End-User Industries

Microcrystalline Cellulose Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Microcrystalline Cellulose Industry Regional Market Share

Geographic Coverage of Microcrystalline Cellulose Industry

Microcrystalline Cellulose Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Source

- 5.1.1. Wood-based

- 5.1.2. Non -wood-based

- 5.2. Market Analysis, Insights and Forecast - by Process

- 5.2.1. Reactive Extrusion

- 5.2.2. Enzyme Mediated

- 5.2.3. Steam Explosion

- 5.2.4. Acid Hydrolysis

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. Pharmaceutical

- 5.3.2. Food

- 5.3.3. Cosmetics

- 5.3.4. Other End-User Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Source

- 6. Global Microcrystalline Cellulose Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Source

- 6.1.1. Wood-based

- 6.1.2. Non -wood-based

- 6.2. Market Analysis, Insights and Forecast - by Process

- 6.2.1. Reactive Extrusion

- 6.2.2. Enzyme Mediated

- 6.2.3. Steam Explosion

- 6.2.4. Acid Hydrolysis

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry

- 6.3.1. Pharmaceutical

- 6.3.2. Food

- 6.3.3. Cosmetics

- 6.3.4. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Source

- 7. Asia Pacific Microcrystalline Cellulose Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Source

- 7.1.1. Wood-based

- 7.1.2. Non -wood-based

- 7.2. Market Analysis, Insights and Forecast - by Process

- 7.2.1. Reactive Extrusion

- 7.2.2. Enzyme Mediated

- 7.2.3. Steam Explosion

- 7.2.4. Acid Hydrolysis

- 7.3. Market Analysis, Insights and Forecast - by End-User Industry

- 7.3.1. Pharmaceutical

- 7.3.2. Food

- 7.3.3. Cosmetics

- 7.3.4. Other End-User Industries

- 7.1. Market Analysis, Insights and Forecast - by Source

- 8. North America Microcrystalline Cellulose Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Source

- 8.1.1. Wood-based

- 8.1.2. Non -wood-based

- 8.2. Market Analysis, Insights and Forecast - by Process

- 8.2.1. Reactive Extrusion

- 8.2.2. Enzyme Mediated

- 8.2.3. Steam Explosion

- 8.2.4. Acid Hydrolysis

- 8.3. Market Analysis, Insights and Forecast - by End-User Industry

- 8.3.1. Pharmaceutical

- 8.3.2. Food

- 8.3.3. Cosmetics

- 8.3.4. Other End-User Industries

- 8.1. Market Analysis, Insights and Forecast - by Source

- 9. Europe Microcrystalline Cellulose Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Source

- 9.1.1. Wood-based

- 9.1.2. Non -wood-based

- 9.2. Market Analysis, Insights and Forecast - by Process

- 9.2.1. Reactive Extrusion

- 9.2.2. Enzyme Mediated

- 9.2.3. Steam Explosion

- 9.2.4. Acid Hydrolysis

- 9.3. Market Analysis, Insights and Forecast - by End-User Industry

- 9.3.1. Pharmaceutical

- 9.3.2. Food

- 9.3.3. Cosmetics

- 9.3.4. Other End-User Industries

- 9.1. Market Analysis, Insights and Forecast - by Source

- 10. South America Microcrystalline Cellulose Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Source

- 10.1.1. Wood-based

- 10.1.2. Non -wood-based

- 10.2. Market Analysis, Insights and Forecast - by Process

- 10.2.1. Reactive Extrusion

- 10.2.2. Enzyme Mediated

- 10.2.3. Steam Explosion

- 10.2.4. Acid Hydrolysis

- 10.3. Market Analysis, Insights and Forecast - by End-User Industry

- 10.3.1. Pharmaceutical

- 10.3.2. Food

- 10.3.3. Cosmetics

- 10.3.4. Other End-User Industries

- 10.1. Market Analysis, Insights and Forecast - by Source

- 11. Middle East and Africa Microcrystalline Cellulose Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Source

- 11.1.1. Wood-based

- 11.1.2. Non -wood-based

- 11.2. Market Analysis, Insights and Forecast - by Process

- 11.2.1. Reactive Extrusion

- 11.2.2. Enzyme Mediated

- 11.2.3. Steam Explosion

- 11.2.4. Acid Hydrolysis

- 11.3. Market Analysis, Insights and Forecast - by End-User Industry

- 11.3.1. Pharmaceutical

- 11.3.2. Food

- 11.3.3. Cosmetics

- 11.3.4. Other End-User Industries

- 11.1. Market Analysis, Insights and Forecast - by Source

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Blanver

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 DFE Pharma

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Asahi Kasei Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Chemfield Cellulose

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 MINGTAI CHEMICAL CO LTD

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 JUKU ORCHEM PVT LTD

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sigachi Industries Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 J RETTENMAIER & SÖHNE GmbH + Co KG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DuPont

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 GUJARAT MICROWAX PVT LTD

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 VWR International LLC (Avantor Inc )*List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Accent Microcell

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Huzhou City Linghu Xinwang Chemical Co Ltd

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Blanver

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Microcrystalline Cellulose Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Microcrystalline Cellulose Industry Revenue (million), by Source 2025 & 2033

- Figure 3: Asia Pacific Microcrystalline Cellulose Industry Revenue Share (%), by Source 2025 & 2033

- Figure 4: Asia Pacific Microcrystalline Cellulose Industry Revenue (million), by Process 2025 & 2033

- Figure 5: Asia Pacific Microcrystalline Cellulose Industry Revenue Share (%), by Process 2025 & 2033

- Figure 6: Asia Pacific Microcrystalline Cellulose Industry Revenue (million), by End-User Industry 2025 & 2033

- Figure 7: Asia Pacific Microcrystalline Cellulose Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 8: Asia Pacific Microcrystalline Cellulose Industry Revenue (million), by Country 2025 & 2033

- Figure 9: Asia Pacific Microcrystalline Cellulose Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Microcrystalline Cellulose Industry Revenue (million), by Source 2025 & 2033

- Figure 11: North America Microcrystalline Cellulose Industry Revenue Share (%), by Source 2025 & 2033

- Figure 12: North America Microcrystalline Cellulose Industry Revenue (million), by Process 2025 & 2033

- Figure 13: North America Microcrystalline Cellulose Industry Revenue Share (%), by Process 2025 & 2033

- Figure 14: North America Microcrystalline Cellulose Industry Revenue (million), by End-User Industry 2025 & 2033

- Figure 15: North America Microcrystalline Cellulose Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 16: North America Microcrystalline Cellulose Industry Revenue (million), by Country 2025 & 2033

- Figure 17: North America Microcrystalline Cellulose Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Microcrystalline Cellulose Industry Revenue (million), by Source 2025 & 2033

- Figure 19: Europe Microcrystalline Cellulose Industry Revenue Share (%), by Source 2025 & 2033

- Figure 20: Europe Microcrystalline Cellulose Industry Revenue (million), by Process 2025 & 2033

- Figure 21: Europe Microcrystalline Cellulose Industry Revenue Share (%), by Process 2025 & 2033

- Figure 22: Europe Microcrystalline Cellulose Industry Revenue (million), by End-User Industry 2025 & 2033

- Figure 23: Europe Microcrystalline Cellulose Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 24: Europe Microcrystalline Cellulose Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Europe Microcrystalline Cellulose Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Microcrystalline Cellulose Industry Revenue (million), by Source 2025 & 2033

- Figure 27: South America Microcrystalline Cellulose Industry Revenue Share (%), by Source 2025 & 2033

- Figure 28: South America Microcrystalline Cellulose Industry Revenue (million), by Process 2025 & 2033

- Figure 29: South America Microcrystalline Cellulose Industry Revenue Share (%), by Process 2025 & 2033

- Figure 30: South America Microcrystalline Cellulose Industry Revenue (million), by End-User Industry 2025 & 2033

- Figure 31: South America Microcrystalline Cellulose Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 32: South America Microcrystalline Cellulose Industry Revenue (million), by Country 2025 & 2033

- Figure 33: South America Microcrystalline Cellulose Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Microcrystalline Cellulose Industry Revenue (million), by Source 2025 & 2033

- Figure 35: Middle East and Africa Microcrystalline Cellulose Industry Revenue Share (%), by Source 2025 & 2033

- Figure 36: Middle East and Africa Microcrystalline Cellulose Industry Revenue (million), by Process 2025 & 2033

- Figure 37: Middle East and Africa Microcrystalline Cellulose Industry Revenue Share (%), by Process 2025 & 2033

- Figure 38: Middle East and Africa Microcrystalline Cellulose Industry Revenue (million), by End-User Industry 2025 & 2033

- Figure 39: Middle East and Africa Microcrystalline Cellulose Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 40: Middle East and Africa Microcrystalline Cellulose Industry Revenue (million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Microcrystalline Cellulose Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Source 2020 & 2033

- Table 2: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Process 2020 & 2033

- Table 3: Global Microcrystalline Cellulose Industry Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 4: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Source 2020 & 2033

- Table 6: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Process 2020 & 2033

- Table 7: Global Microcrystalline Cellulose Industry Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 8: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: China Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: India Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Japan Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: South Korea Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Asia Pacific Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Source 2020 & 2033

- Table 15: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Process 2020 & 2033

- Table 16: Global Microcrystalline Cellulose Industry Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 17: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Country 2020 & 2033

- Table 18: United States Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Canada Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Mexico Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Source 2020 & 2033

- Table 22: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Process 2020 & 2033

- Table 23: Global Microcrystalline Cellulose Industry Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 24: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Country 2020 & 2033

- Table 25: Germany Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: United Kingdom Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: France Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Italy Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Source 2020 & 2033

- Table 31: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Process 2020 & 2033

- Table 32: Global Microcrystalline Cellulose Industry Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 33: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Country 2020 & 2033

- Table 34: Brazil Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Argentina Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of South America Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Source 2020 & 2033

- Table 38: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Process 2020 & 2033

- Table 39: Global Microcrystalline Cellulose Industry Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 40: Global Microcrystalline Cellulose Industry Revenue million Forecast, by Country 2020 & 2033

- Table 41: Saudi Arabia Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: South Africa Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: Rest of Middle East and Africa Microcrystalline Cellulose Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Microcrystalline Cellulose Industry?

The projected CAGR is approximately 7.8%.

2. Which companies are prominent players in the Microcrystalline Cellulose Industry?

Key companies in the market include Blanver, DFE Pharma, Asahi Kasei Corporation, Chemfield Cellulose, MINGTAI CHEMICAL CO LTD, JUKU ORCHEM PVT LTD, Sigachi Industries Limited, J RETTENMAIER & SÖHNE GmbH + Co KG, DuPont, GUJARAT MICROWAX PVT LTD, VWR International LLC (Avantor Inc )*List Not Exhaustive, Accent Microcell, Huzhou City Linghu Xinwang Chemical Co Ltd.

3. What are the main segments of the Microcrystalline Cellulose Industry?

The market segments include Source, Process, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1255.1 million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Microcrystalline Cellulose from Pharmaceutical Industry.

6. What are the notable trends driving market growth?

Increasing Demand from Pharmaceutical Industry.

7. Are there any restraints impacting market growth?

High Manufacturing and Production Cost.

8. Can you provide examples of recent developments in the market?

November 2022: DFE Pharma partnered with Azelis, which is a service provider in the specialty chemicals and food ingredients industry, for the distribution of its products in the EMEA region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Microcrystalline Cellulose Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Microcrystalline Cellulose Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Microcrystalline Cellulose Industry?

To stay informed about further developments, trends, and reports in the Microcrystalline Cellulose Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence