Key Insights

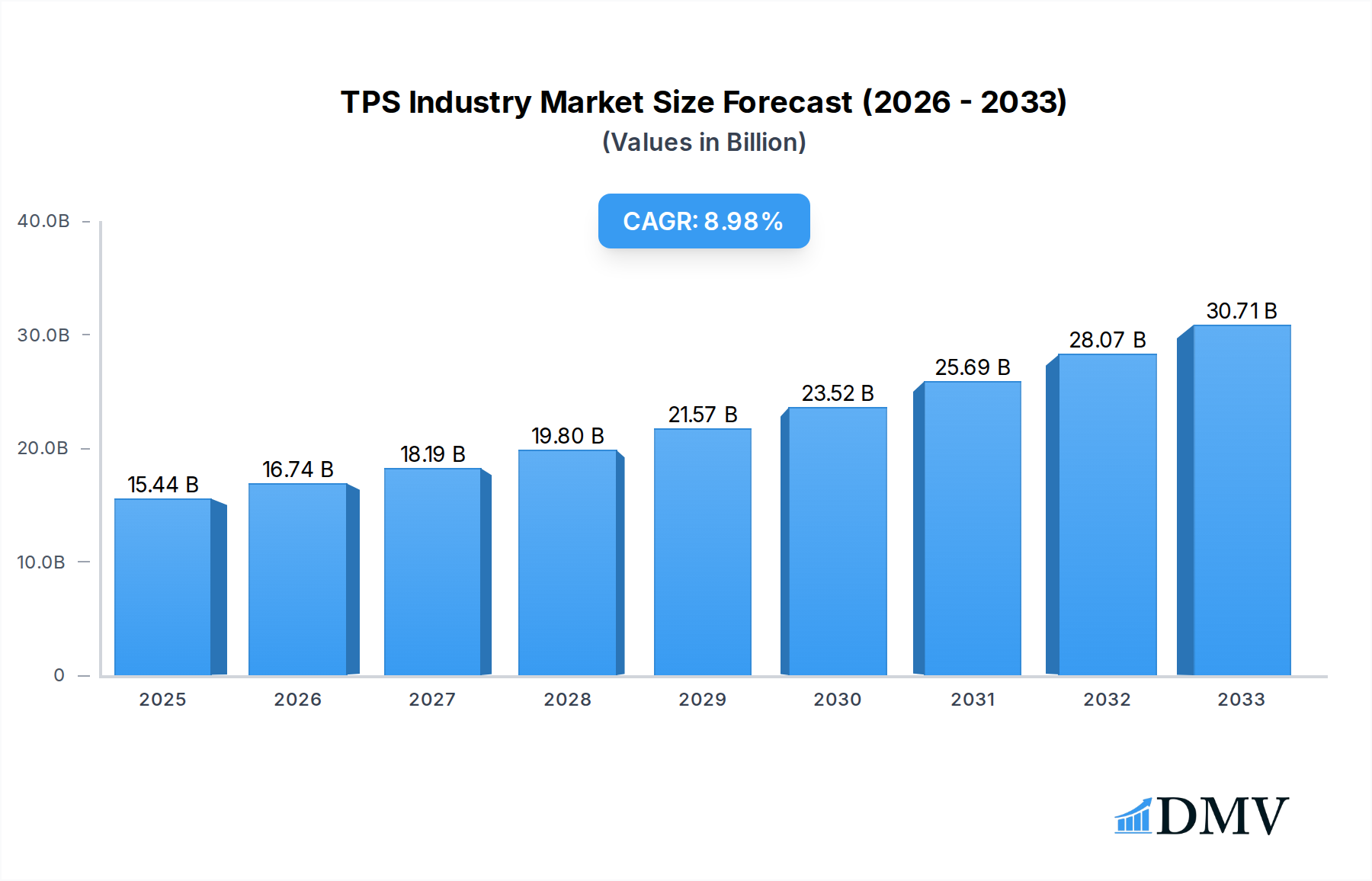

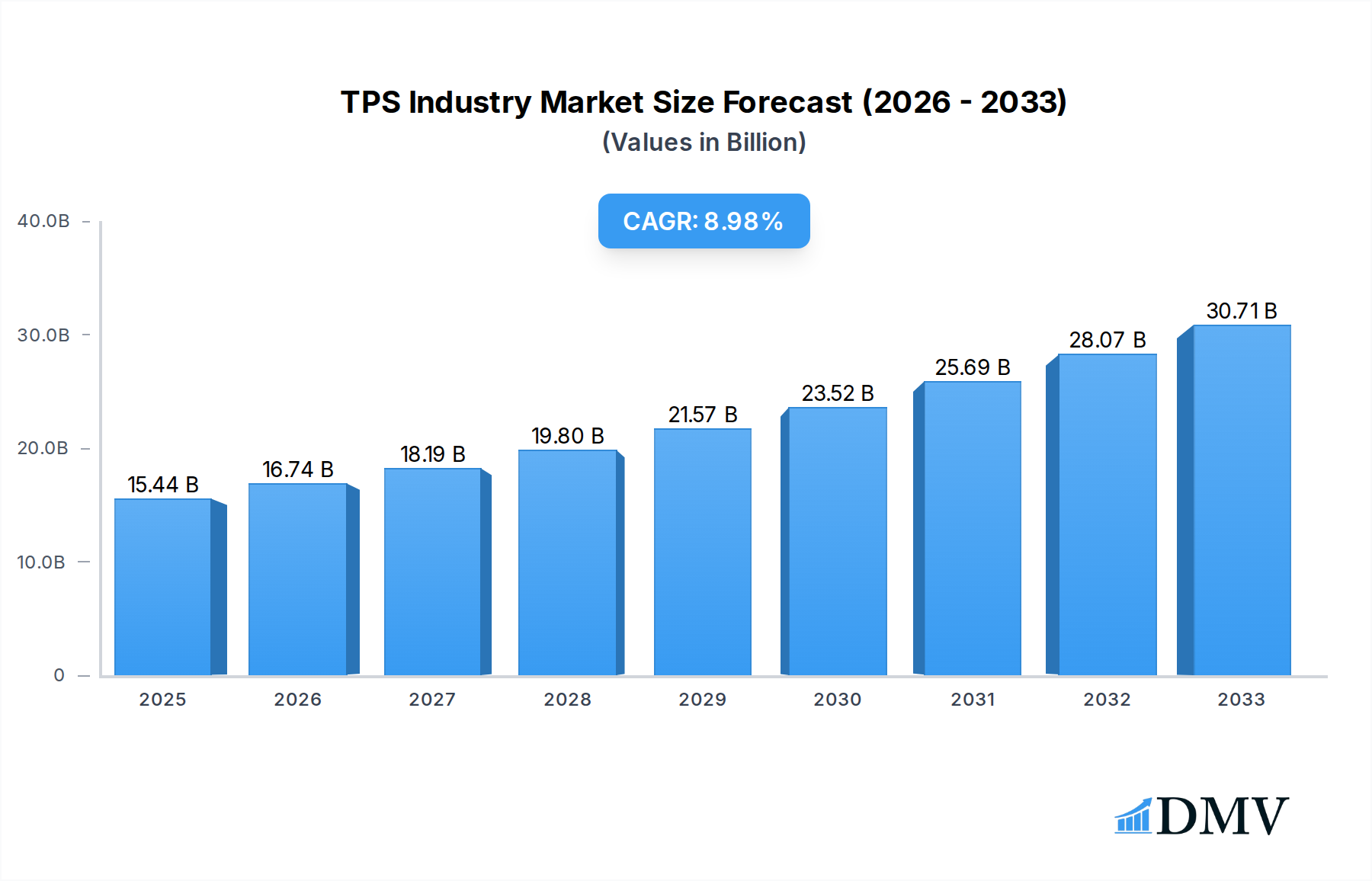

The Thermoplastic Starch (TPS) market is poised for significant expansion, projected to reach USD 15.44 billion by 2025. This growth is underpinned by a robust CAGR of 8.51% during the forecast period. The increasing demand for sustainable and biodegradable packaging solutions is a primary driver, directly addressing environmental concerns associated with conventional plastics. Key applications such as bags and films are witnessing substantial uptake, driven by the food & beverage and retail sectors' transition towards eco-friendly alternatives. Furthermore, the burgeoning 3D printing industry, seeking bio-based filaments, is opening new avenues for TPS. Emerging applications in agriculture, textiles, and medical devices are also contributing to this upward trajectory. The market's expansion is also fueled by advancements in manufacturing technologies, particularly extrusion molding, which enhances the performance and versatility of TPS-based products.

TPS Industry Market Size (In Billion)

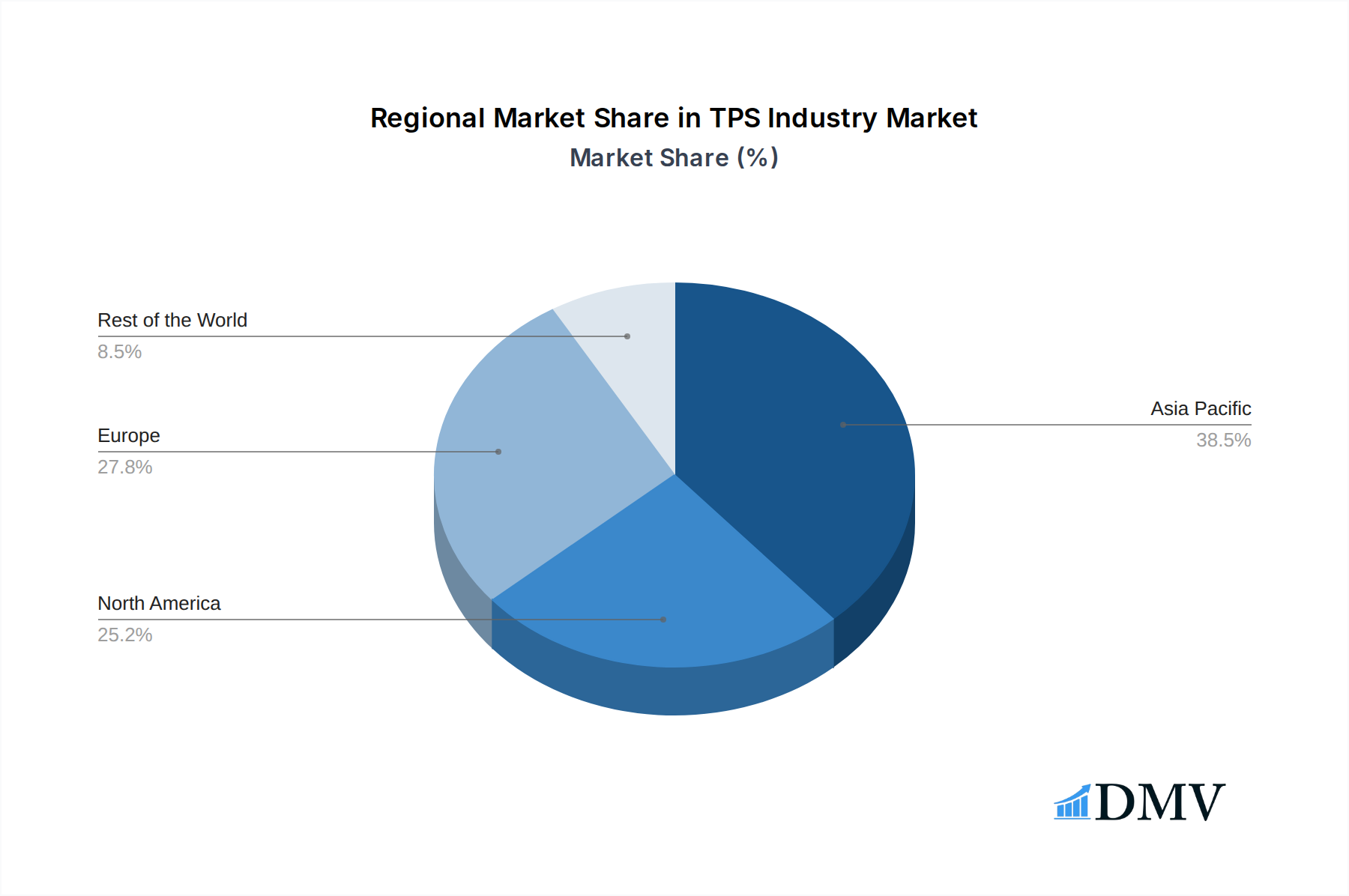

Despite the promising outlook, certain factors could influence the pace of growth. The inherent properties of TPS, such as its sensitivity to moisture, can pose challenges in certain humid environments or applications requiring extended water resistance. This necessitates ongoing research and development into advanced formulations and barrier coatings. The cost competitiveness compared to traditional petroleum-based plastics, while improving, can still be a consideration for price-sensitive markets. However, the growing regulatory pressure favoring sustainable materials and increasing consumer awareness are expected to offset these restraints. Geographically, the Asia Pacific region, led by China and India, is anticipated to be a dominant force due to its large manufacturing base and increasing environmental consciousness. North America and Europe are also crucial markets, driven by stringent environmental regulations and a strong consumer preference for green products. Key players in the market, including Kuraray Co. Ltd., Rodenburg Biopolymers, and Versalis SpA, are actively investing in innovation to expand their product portfolios and cater to diverse application needs.

TPS Industry Company Market Share

TPS Industry Market Composition & Trends

The TPS Industry is experiencing a dynamic evolution, marked by increasing market concentration and a robust pace of innovation, particularly in the realm of sustainable materials. Key companies like Kuraray Co Ltd, Rodenburg Biopolymers, Versalis SpA, and Biologiq Inc. are at the forefront, driving advancements and influencing market share distribution. The Extrusion Molding manufacturing type dominates, catering to a broad spectrum of applications including Bags, Films, and 3D Print. Regulatory landscapes are increasingly favoring bio-based and compostable alternatives, creating a fertile ground for growth while also presenting challenges related to standardization and certifications. Substitute products, primarily traditional petroleum-based plastics, are facing growing pressure from eco-conscious consumers and stringent environmental policies. End-user profiles are diverse, ranging from packaging converters to additive manufacturing enthusiasts, all seeking sustainable and high-performance solutions. Mergers and acquisitions (M&A) are becoming pivotal, with significant deal values facilitating portfolio expansion and market consolidation. For instance, the October 2023: Versalis announced its acquisition of Novamont SpA underscores a strategic move to bolster bio-based product offerings, with an estimated deal value in the billions. This consolidation trend is expected to continue as companies seek to enhance their competitive edge and secure a larger share of the burgeoning bio-based plastics market. The market's trajectory suggests a significant shift towards circular economy principles, with a projected market size in the billions by 2033.

TPS Industry Industry Evolution

The TPS Industry is charting an impressive growth trajectory, fueled by a confluence of technological breakthroughs, evolving consumer preferences, and supportive regulatory frameworks. Over the Study Period: 2019–2033, the market has witnessed a substantial expansion, driven by the global imperative to reduce environmental impact and embrace sustainable alternatives. During the Historical Period: 2019–2024, significant strides were made in material science, leading to the development of advanced biodegradable and compostable TPS materials that rival the performance of conventional plastics. For example, innovations in polymerization techniques have resulted in enhanced thermal stability and mechanical strength, making these materials viable for a wider range of applications. The Base Year: 2025, marks a pivotal point where adoption rates are accelerating, with projections indicating a compound annual growth rate (CAGR) in the high single to low double digits for the Forecast Period: 2025–2033. Technological advancements are not merely incremental; they are transformative. Research into novel bio-sources, such as agricultural waste and algae, is expanding the feedstock options and driving down production costs. Furthermore, advancements in processing technologies, including sophisticated Extrusion Molding techniques, are enabling the efficient and cost-effective manufacturing of complex TPS products like specialized Films and intricate 3D Print components. Consumer demand for eco-friendly products is a powerful catalyst, with an increasing segment of the population actively seeking out and willing to pay a premium for sustainable goods. This demand extends across various sectors, from consumer packaging to automotive interiors and healthcare applications. Regulatory initiatives worldwide, promoting plastic reduction and waste management, are further incentivizing the adoption of TPS, creating a favorable market environment. The market's evolution is characterized by a steady increase in adoption metrics, with the Estimated Year: 2025 showing a significant uptick in market penetration for TPS across key application areas. The industry's growth is underpinned by a sustained investment in research and development, with billions dedicated to uncovering new material compositions and optimizing production processes. This relentless pursuit of innovation ensures that the TPS industry remains at the cutting edge of sustainable material solutions, poised for continued exponential growth in the coming decade, projected to reach market values in the hundreds of billions.

Leading Regions, Countries, or Segments in TPS Industry

The TPS Industry is characterized by distinct regional strengths and segment dominance, with Extrusion Molding emerging as the predominant manufacturing type. This segment's leadership is intrinsically linked to its versatility and cost-effectiveness in producing high-volume TPS products for critical applications like Bags and Films. The global market's landscape is shaped by a combination of regulatory support, investment trends, and consumer awareness.

Dominant Manufacturing Type: Extrusion Molding:

- Key Drivers: The inherent efficiency and scalability of extrusion molding make it the go-to process for TPS. Its ability to handle a wide range of viscosities and melt strengths allows for the production of continuous films, sheets, and profiles essential for packaging and other high-volume applications.

- Investment Trends: Significant investments are being channeled into advanced extrusion lines capable of processing bio-polymers with greater precision and speed. This includes upgrades to screw designs, die heads, and cooling systems to optimize material flow and final product quality.

- Regulatory Support: Policies promoting the use of biodegradable and compostable materials in packaging directly benefit the extrusion molding segment. Stricter regulations on single-use plastics further accelerate the demand for TPS produced via this method.

- Technological Advancements: Innovations in co-extrusion and multi-layer film technology enable the creation of TPS packaging with enhanced barrier properties, extending shelf life and reducing food waste, a key selling point for consumers and businesses alike.

Dominant Application: Films:

- In-depth Analysis: The Films application segment is a powerhouse within the TPS industry, driven by the insatiable demand from the packaging sector. TPS films are increasingly replacing conventional plastic films in areas such as food packaging, agricultural films, and industrial wrapping. The ability of TPS to be compostable or biodegradable directly addresses mounting environmental concerns associated with plastic waste accumulating in landfills and oceans. The market is witnessing a surge in demand for compostable films for single-use items, where end-of-life management is a critical consideration. Furthermore, advancements in TPS film technology are yielding products with improved clarity, puncture resistance, and heat sealability, making them technically superior for many applications. The growth in e-commerce has also boosted the demand for protective packaging films, where sustainable alternatives are highly sought after. Countries with robust recycling and composting infrastructure, or those actively investing in them, are seeing higher adoption rates for TPS films. The projected market value for TPS films alone is expected to reach billions within the forecast period.

Emerging Application: 3D Print:

- In-depth Analysis: While currently a smaller segment compared to films and bags, 3D Print applications for TPS are rapidly gaining traction. The ability to create complex geometries with sustainable materials is opening up new possibilities in prototyping, custom manufacturing, and even end-use parts. Researchers are developing TPS filaments with enhanced printability and mechanical properties, catering to the growing additive manufacturing market. The eco-conscious nature of TPS aligns perfectly with the ethos of many 3D printing communities and businesses seeking to reduce their environmental footprint. As 3D printing technology matures and becomes more accessible, the demand for TPS filaments is expected to experience exponential growth, reaching billions in market value.

Other Applications: This broad category encompasses a diverse range of products, including automotive components, consumer goods, textiles, and medical devices. The inherent sustainability and customizability of TPS materials make them attractive for niche applications where specific environmental or performance criteria must be met.

Geographically, regions with strong environmental regulations and a high consumer awareness of sustainability, such as Europe and North America, are currently leading the TPS market. However, Asia-Pacific is poised for significant growth due to increasing investments and rising environmental consciousness. The overall market is projected to reach hundreds of billions in value by 2033, with the Films segment consistently holding the largest market share.

TPS Industry Product Innovations

The TPS Industry is a hotbed of innovation, with manufacturers continuously developing advanced materials and applications to meet growing sustainability demands. Recent breakthroughs include the development of TPS grades with enhanced barrier properties, crucial for extending the shelf life of packaged goods and reducing food waste. Furthermore, advancements in Extrusion Molding techniques have enabled the creation of ultra-thin yet robust TPS Films with superior puncture resistance, making them ideal for challenging packaging applications. For 3D Print, new TPS filaments are emerging with improved printability and mechanical strength, allowing for the creation of functional prototypes and end-use parts with a reduced environmental impact. These innovations not only address the environmental concerns but also offer competitive performance metrics, driving adoption across diverse industries and contributing to a projected market expansion into the hundreds of billions.

Propelling Factors for TPS Industry Growth

The TPS Industry is experiencing robust growth propelled by a potent combination of technological advancements, economic incentives, and supportive regulatory policies.

- Technological Advancements: Innovations in bio-polymer science are yielding TPS materials with improved performance characteristics, such as enhanced strength, flexibility, and barrier properties, making them viable alternatives to conventional plastics across a wider range of applications.

- Economic Influences: Growing consumer demand for sustainable products, coupled with increasing corporate sustainability goals, is creating a significant market pull for TPS. Price parity with conventional plastics is becoming more achievable as production scales up and raw material costs decrease, driven by increased investment in the billions.

- Regulatory Tailwinds: Government regulations worldwide, including bans on single-use plastics and incentives for bio-based materials, are creating a favorable market environment, driving adoption and innovation in the TPS sector.

Obstacles in the TPS Industry Market

Despite its promising growth, the TPS Industry faces several significant obstacles that temper its expansion.

- Cost Competitiveness: While improving, the production cost of TPS materials can still be higher than that of conventional petroleum-based plastics, impacting adoption rates, particularly in price-sensitive markets where billions of units are concerned.

- Performance Limitations: For certain high-performance applications, existing TPS materials may not yet fully match the stringent requirements of traditional plastics in terms of heat resistance, durability, or chemical inertness.

- Infrastructure Challenges: The development of widespread composting and anaerobic digestion infrastructure is crucial for the effective end-of-life management of compostable TPS, and its current limitations hinder widespread adoption.

- Consumer Education and Misconceptions: Clearer communication is needed to differentiate between biodegradable, compostable, and other eco-friendly claims to avoid consumer confusion and ensure proper disposal.

Future Opportunities in TPS Industry

The TPS Industry is ripe with future opportunities, driven by evolving market dynamics and technological frontiers.

- Expanding Applications: The development of advanced TPS grades will unlock new applications in sectors like automotive, construction, and healthcare, where durability and sustainability are paramount, leading to billions in new market penetration.

- Circular Economy Integration: Increased focus on the circular economy will drive innovation in chemical recycling and bio-refinery processes for TPS, creating closed-loop systems and reducing reliance on virgin feedstocks.

- Emerging Markets: Growth in developing economies, coupled with rising environmental awareness, presents significant untapped potential for TPS adoption, creating new markets valued in the billions.

- Technological Synergies: Integration with emerging technologies like AI-driven material design and advanced manufacturing processes will accelerate the development and customization of TPS solutions.

Major Players in the TPS Industry Ecosystem

- Kuraray Co Ltd

- Rodenburg Biopolymers

- Versalis SpA

- Biologiq Inc.

- AGRANA Beteiligungs-AG

- Biotec Biologische Naturverpackungen GmbH & Co KG

- Cardia Bioplastics

- Grupa Azoty SA

- Biome Bioplastics Limited

- Great Wrap

Key Developments in TPS Industry Industry

- October 2023: Versalis announced its acquisition of Novamont SpA. Through this acquisition, Versalis aimed to strengthen its bio-based product portfolio significantly.

- March 2023: Great Wrap announced the launch of the world's first compostable pallet wrap manufactured using food waste. The company completed commercial trials and is expected to establish the largest stretch wrap manufacturing facility in the country. The 10,000-sq. m plant located in Tullamarine is equipped with a state-of-the-art cast extruding line for the film. Currently, the facility is running at a capacity of 5,000 tons. The company has confirmed that by year-end, its capacity is expected to double to 10,000 tons and is expected to reach 20,000 tons by 2025.

Strategic TPS Industry Market Forecast

The TPS Industry is strategically positioned for substantial growth, projected to reach hundreds of billions in market value by 2033. This expansion will be fueled by an increasing global commitment to sustainability, driving demand for eco-friendly alternatives to conventional plastics. Key growth catalysts include ongoing advancements in material science, leading to improved performance and cost-effectiveness of bio-based polymers. Furthermore, supportive government policies and evolving consumer preferences for environmentally responsible products will continue to accelerate adoption across diverse applications, from packaging to additive manufacturing. The strategic forecast anticipates continued innovation in processing technologies and a growing emphasis on circular economy principles, creating a resilient and dynamic market landscape for TPS.

TPS Industry Segmentation

-

1. Manufacturing Type

- 1.1. Extrusion Molding

-

2. Application

- 2.1. Bags

- 2.2. Films

- 2.3. 3D Print

- 2.4. Other Applications

TPS Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. ASEAN Countries

- 1.6. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. NORDIC Countries

- 3.6. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

TPS Industry Regional Market Share

Geographic Coverage of TPS Industry

TPS Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 5.1.1. Extrusion Molding

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Bags

- 5.2.2. Films

- 5.2.3. 3D Print

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 6. Global TPS Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 6.1.1. Extrusion Molding

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Bags

- 6.2.2. Films

- 6.2.3. 3D Print

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 7. Asia Pacific TPS Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 7.1.1. Extrusion Molding

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Bags

- 7.2.2. Films

- 7.2.3. 3D Print

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 8. North America TPS Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 8.1.1. Extrusion Molding

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Bags

- 8.2.2. Films

- 8.2.3. 3D Print

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 9. Europe TPS Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 9.1.1. Extrusion Molding

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Bags

- 9.2.2. Films

- 9.2.3. 3D Print

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 10. Rest of the World TPS Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 10.1.1. Extrusion Molding

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Bags

- 10.2.2. Films

- 10.2.3. 3D Print

- 10.2.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Manufacturing Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Kuraray Co Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Rodenburg Biopolymers

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Versalis SpA *List Not Exhaustive

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Biologiq Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 AGRANA Beteiligungs-AG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Biotec Biologische Naturverpackungen GmbH & Co KG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Cardia Bioplastics

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Grupa Azoty SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Biome Bioplastics Limited

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Great Wrap

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Kuraray Co Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global TPS Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global TPS Industry Volume Breakdown (kilotons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific TPS Industry Revenue (million), by Manufacturing Type 2025 & 2033

- Figure 4: Asia Pacific TPS Industry Volume (kilotons), by Manufacturing Type 2025 & 2033

- Figure 5: Asia Pacific TPS Industry Revenue Share (%), by Manufacturing Type 2025 & 2033

- Figure 6: Asia Pacific TPS Industry Volume Share (%), by Manufacturing Type 2025 & 2033

- Figure 7: Asia Pacific TPS Industry Revenue (million), by Application 2025 & 2033

- Figure 8: Asia Pacific TPS Industry Volume (kilotons), by Application 2025 & 2033

- Figure 9: Asia Pacific TPS Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: Asia Pacific TPS Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: Asia Pacific TPS Industry Revenue (million), by Country 2025 & 2033

- Figure 12: Asia Pacific TPS Industry Volume (kilotons), by Country 2025 & 2033

- Figure 13: Asia Pacific TPS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific TPS Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America TPS Industry Revenue (million), by Manufacturing Type 2025 & 2033

- Figure 16: North America TPS Industry Volume (kilotons), by Manufacturing Type 2025 & 2033

- Figure 17: North America TPS Industry Revenue Share (%), by Manufacturing Type 2025 & 2033

- Figure 18: North America TPS Industry Volume Share (%), by Manufacturing Type 2025 & 2033

- Figure 19: North America TPS Industry Revenue (million), by Application 2025 & 2033

- Figure 20: North America TPS Industry Volume (kilotons), by Application 2025 & 2033

- Figure 21: North America TPS Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: North America TPS Industry Volume Share (%), by Application 2025 & 2033

- Figure 23: North America TPS Industry Revenue (million), by Country 2025 & 2033

- Figure 24: North America TPS Industry Volume (kilotons), by Country 2025 & 2033

- Figure 25: North America TPS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America TPS Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe TPS Industry Revenue (million), by Manufacturing Type 2025 & 2033

- Figure 28: Europe TPS Industry Volume (kilotons), by Manufacturing Type 2025 & 2033

- Figure 29: Europe TPS Industry Revenue Share (%), by Manufacturing Type 2025 & 2033

- Figure 30: Europe TPS Industry Volume Share (%), by Manufacturing Type 2025 & 2033

- Figure 31: Europe TPS Industry Revenue (million), by Application 2025 & 2033

- Figure 32: Europe TPS Industry Volume (kilotons), by Application 2025 & 2033

- Figure 33: Europe TPS Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Europe TPS Industry Volume Share (%), by Application 2025 & 2033

- Figure 35: Europe TPS Industry Revenue (million), by Country 2025 & 2033

- Figure 36: Europe TPS Industry Volume (kilotons), by Country 2025 & 2033

- Figure 37: Europe TPS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe TPS Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Rest of the World TPS Industry Revenue (million), by Manufacturing Type 2025 & 2033

- Figure 40: Rest of the World TPS Industry Volume (kilotons), by Manufacturing Type 2025 & 2033

- Figure 41: Rest of the World TPS Industry Revenue Share (%), by Manufacturing Type 2025 & 2033

- Figure 42: Rest of the World TPS Industry Volume Share (%), by Manufacturing Type 2025 & 2033

- Figure 43: Rest of the World TPS Industry Revenue (million), by Application 2025 & 2033

- Figure 44: Rest of the World TPS Industry Volume (kilotons), by Application 2025 & 2033

- Figure 45: Rest of the World TPS Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Rest of the World TPS Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Rest of the World TPS Industry Revenue (million), by Country 2025 & 2033

- Figure 48: Rest of the World TPS Industry Volume (kilotons), by Country 2025 & 2033

- Figure 49: Rest of the World TPS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Rest of the World TPS Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global TPS Industry Revenue million Forecast, by Manufacturing Type 2020 & 2033

- Table 2: Global TPS Industry Volume kilotons Forecast, by Manufacturing Type 2020 & 2033

- Table 3: Global TPS Industry Revenue million Forecast, by Application 2020 & 2033

- Table 4: Global TPS Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 5: Global TPS Industry Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global TPS Industry Volume kilotons Forecast, by Region 2020 & 2033

- Table 7: Global TPS Industry Revenue million Forecast, by Manufacturing Type 2020 & 2033

- Table 8: Global TPS Industry Volume kilotons Forecast, by Manufacturing Type 2020 & 2033

- Table 9: Global TPS Industry Revenue million Forecast, by Application 2020 & 2033

- Table 10: Global TPS Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 11: Global TPS Industry Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global TPS Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 13: China TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: China TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 15: India TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: India TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 17: Japan TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Japan TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 19: South Korea TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: South Korea TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 21: ASEAN Countries TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: ASEAN Countries TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 23: Rest of Asia Pacific TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Rest of Asia Pacific TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 25: Global TPS Industry Revenue million Forecast, by Manufacturing Type 2020 & 2033

- Table 26: Global TPS Industry Volume kilotons Forecast, by Manufacturing Type 2020 & 2033

- Table 27: Global TPS Industry Revenue million Forecast, by Application 2020 & 2033

- Table 28: Global TPS Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 29: Global TPS Industry Revenue million Forecast, by Country 2020 & 2033

- Table 30: Global TPS Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 31: United States TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: United States TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 33: Canada TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Canada TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 35: Mexico TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Mexico TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 37: Global TPS Industry Revenue million Forecast, by Manufacturing Type 2020 & 2033

- Table 38: Global TPS Industry Volume kilotons Forecast, by Manufacturing Type 2020 & 2033

- Table 39: Global TPS Industry Revenue million Forecast, by Application 2020 & 2033

- Table 40: Global TPS Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 41: Global TPS Industry Revenue million Forecast, by Country 2020 & 2033

- Table 42: Global TPS Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 43: Germany TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Germany TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 45: United Kingdom TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: United Kingdom TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 47: Italy TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Italy TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 49: France TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: France TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 51: NORDIC Countries TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: NORDIC Countries TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 55: Global TPS Industry Revenue million Forecast, by Manufacturing Type 2020 & 2033

- Table 56: Global TPS Industry Volume kilotons Forecast, by Manufacturing Type 2020 & 2033

- Table 57: Global TPS Industry Revenue million Forecast, by Application 2020 & 2033

- Table 58: Global TPS Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 59: Global TPS Industry Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global TPS Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 61: South America TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: South America TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 63: Middle East and Africa TPS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Middle East and Africa TPS Industry Volume (kilotons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the TPS Industry?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the TPS Industry?

Key companies in the market include Kuraray Co Ltd, Rodenburg Biopolymers, Versalis SpA *List Not Exhaustive, Biologiq Inc, AGRANA Beteiligungs-AG, Biotec Biologische Naturverpackungen GmbH & Co KG, Cardia Bioplastics, Grupa Azoty SA, Biome Bioplastics Limited, Great Wrap.

3. What are the main segments of the TPS Industry?

The market segments include Manufacturing Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 556.7 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand from the Packaging Industry; Favorable Government Policies Promoting Bio-plastics.

6. What are the notable trends driving market growth?

Films Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Multiple Technical Constrains Associated with TPS.

8. Can you provide examples of recent developments in the market?

October 2023: Versalis announced its acquisition of Novamont SpA. Through this acquisition, Versalis aimed to strengthen its bio-based product portfolio significantly.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in kilotons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "TPS Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the TPS Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the TPS Industry?

To stay informed about further developments, trends, and reports in the TPS Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence