Key Insights

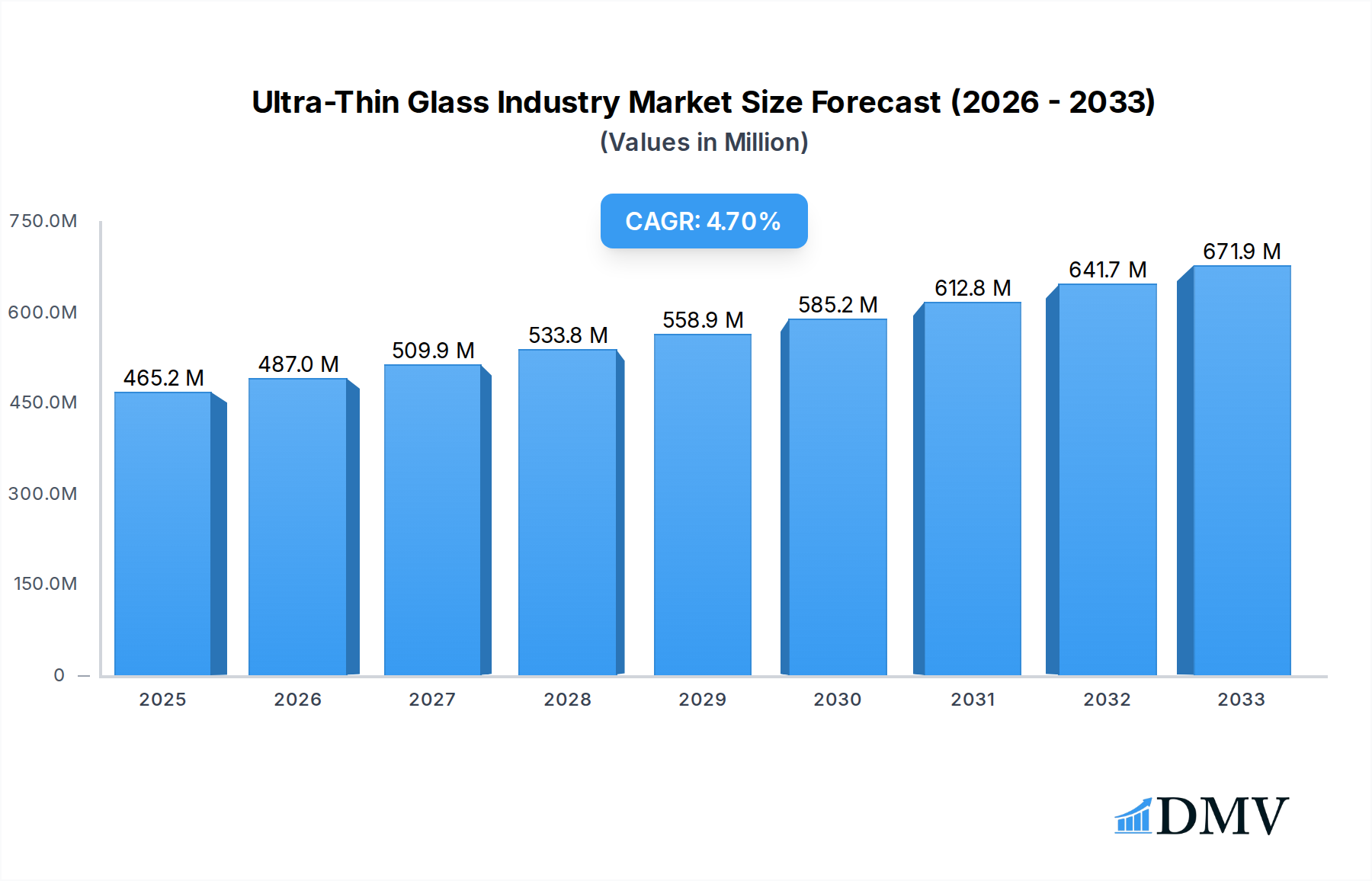

The global Ultra-Thin Glass market is poised for robust expansion, projected to reach an estimated $465.18 million in 2025, driven by an anticipated Compound Annual Growth Rate (CAGR) of 4.64% through 2033. This growth is significantly fueled by the escalating demand for advanced display technologies across various consumer electronics, including smartphones, tablets, and wearables, where ultra-thin glass offers superior aesthetics and durability. Furthermore, the automotive sector's increasing adoption of integrated displays and sophisticated glazing solutions presents a substantial growth avenue. The burgeoning demand for flexible and bendable displays, crucial for next-generation mobile devices and smart textiles, also acts as a primary market stimulant. Innovations in manufacturing processes, leading to thinner, stronger, and more cost-effective ultra-thin glass, will further propel market penetration and adoption across new applications.

Ultra-Thin Glass Industry Market Size (In Million)

Emerging applications such as advanced fingerprint sensors, specialized biotechnology equipment, and innovative architectural glazing are also contributing to the market's upward trajectory. The Asia Pacific region, led by China and South Korea, is expected to dominate the market share due to its strong manufacturing base in electronics and a high concentration of key industry players. Conversely, challenges such as the intricate manufacturing processes requiring specialized equipment and stringent quality control, along with the potential for substitution by alternative materials in certain less demanding applications, represent restraints. However, continuous research and development aimed at enhancing material properties and optimizing production efficiency are expected to mitigate these limitations, ensuring sustained market growth and technological advancement in the ultra-thin glass industry.

Ultra-Thin Glass Industry Company Market Share

This comprehensive report delves deep into the ultra-thin glass industry, a rapidly evolving sector projected to reach millions in market value. We meticulously analyze market composition, key trends, industry evolution, leading regions, product innovations, growth drivers, obstacles, and future opportunities. The report covers the Study Period: 2019–2033, with Base Year: 2025 and Forecast Period: 2025–2033, building upon Historical Period: 2019–2024 data. Discover critical insights for stakeholders in consumer electronics, automotive, and biotechnology sectors.

Ultra-Thin Glass Industry Market Composition & Trends

The global ultra-thin glass market exhibits moderate concentration, with a few dominant players like Corning Incorporated, AGC Glass Europe, and Schott AG holding significant market share. The market is driven by relentless innovation, fueled by advancements in manufacturing techniques and a growing demand for thinner, lighter, and more durable glass solutions. Regulatory landscapes are evolving to support sustainable manufacturing practices and product safety standards, particularly in the automotive and consumer electronics sectors. Substitute products, while present, struggle to match the unique combination of properties offered by ultra-thin glass, including its flexibility, scratch resistance, and excellent optical clarity. End-user profiles are increasingly diverse, encompassing high-end smartphones, advanced displays, flexible OLED screens, and next-generation automotive glazing. Mergers and acquisitions (M&A) activity remains a strategic imperative for market consolidation and expansion, with significant deal values recorded to secure market position and technological expertise. For instance, past M&A deals have collectively amounted to over XXX million in value, signaling strong investor confidence. Market share distribution indicates a strong foothold for companies specializing in high-volume production and cutting-edge R&D.

Ultra-Thin Glass Industry Industry Evolution

The ultra-thin glass industry has witnessed a transformative evolution, marked by substantial growth trajectories and technological breakthroughs over the Historical Period: 2019–2024. From its nascent stages, the industry has rapidly scaled, driven by an insatiable demand for thinner, lighter, and more resilient glass solutions across various applications. Key technological advancements have centered around improved manufacturing processes, enabling higher yields and reduced production costs. Techniques like fusion drawing and chemical strengthening have been pivotal in achieving the desired thinness and enhanced durability. For example, the adoption of advanced chemical strengthening techniques has led to a xx% increase in flexural strength for ultra-thin glass applications, a critical metric for semiconductor substrate and touch panel display durability. Consumer demand has shifted dramatically, prioritizing sleek designs, enhanced portability, and superior visual experiences, directly propelling the adoption of ultra-thin glass in consumer electronics. The automotive industry is increasingly integrating ultra-thin glass for lighter vehicle components and advanced dashboard displays, contributing to fuel efficiency and improved aesthetics. The market experienced a consistent Compound Annual Growth Rate (CAGR) of xx% during the historical period, a testament to its robust expansion. Projections for the Forecast Period: 2025–2033 indicate continued strong growth, fueled by emerging applications in areas like augmented reality (AR) and virtual reality (VR) devices, where weight and optical clarity are paramount. The ongoing research and development in biotechnology for specialized diagnostic equipment also presents a significant growth avenue.

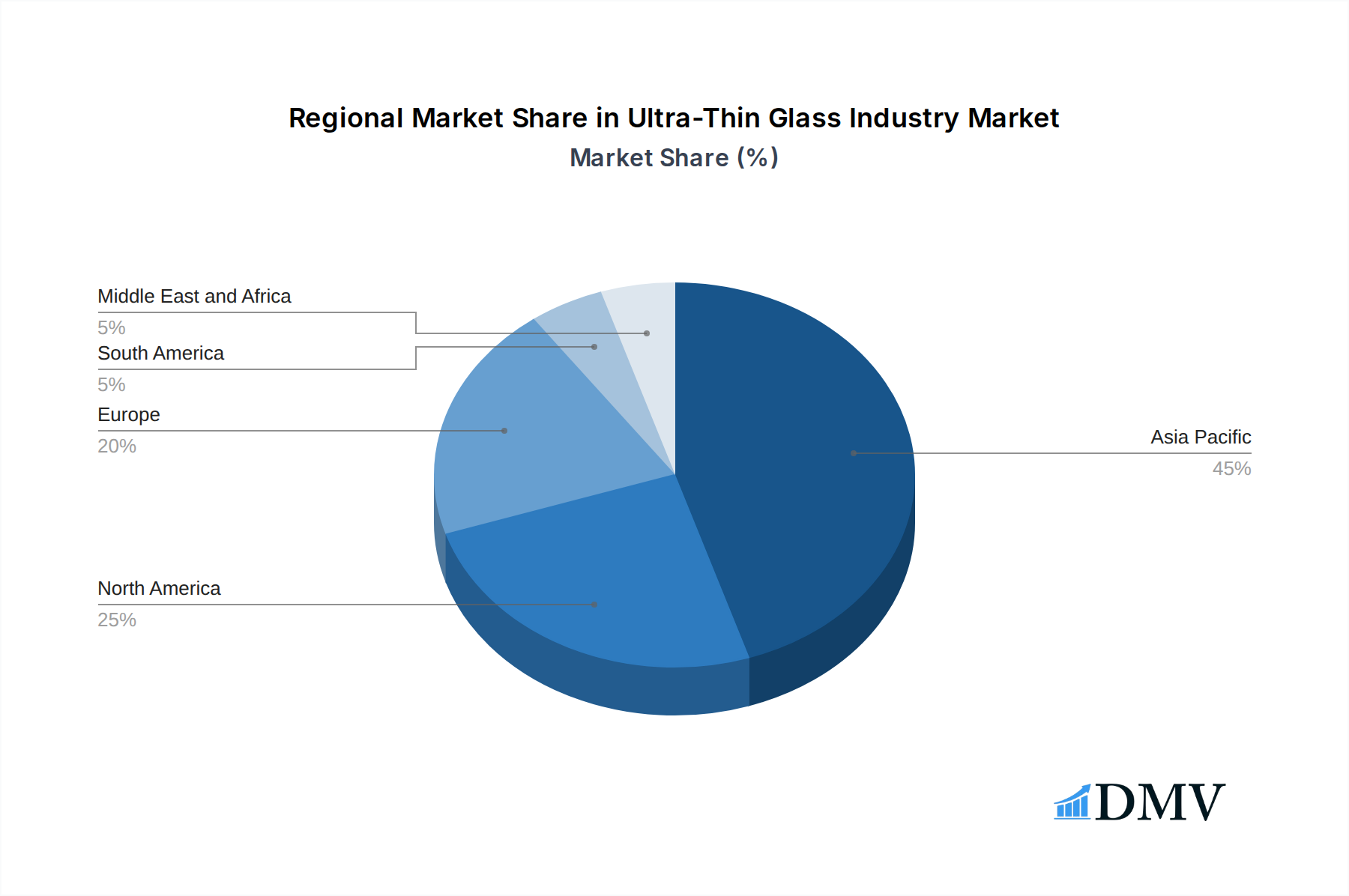

Leading Regions, Countries, or Segments in Ultra-Thin Glass Industry

The ultra-thin glass industry is currently dominated by the Asia-Pacific region, with China leading in both production volume and market demand. This dominance is fueled by a robust manufacturing ecosystem, substantial government support for high-tech industries, and the presence of major global electronics manufacturers. The region's leadership is further solidified by significant investments in research and development, fostering a continuous cycle of innovation.

Application Dominance:

- Touch Panel Displays: This segment is the primary revenue generator, driven by the ubiquitous demand for smartphones, tablets, and other interactive devices. The market for ultra-thin glass in touch panels is valued at over XXX million in the Base Year: 2025.

- Semiconductor Substrate: The increasing complexity and miniaturization of semiconductor components necessitate ultra-thin, high-purity glass substrates for advanced packaging and wafer-level solutions. Investment trends in this segment show a xx% year-on-year increase in R&D spending.

- Automotive Glazing: The growing trend towards advanced driver-assistance systems (ADAS) and integrated displays in vehicles is boosting the adoption of ultra-thin glass for lighter, more durable, and aesthetically pleasing automotive applications. Regulatory support for vehicle safety and emission reduction indirectly benefits this segment.

End-user Industry Dominance:

- Consumer Electronics: This remains the largest end-user industry, with its insatiable demand for thinner, more durable, and visually appealing devices. The sector's growth rate is projected at xx% annually during the forecast period.

- Automotive: The increasing integration of technology in vehicles, from infotainment systems to sensor components, is making ultra-thin glass a critical material. Market penetration in automotive is expected to reach xx% by 2033.

- Biotechnology: While currently a niche segment, the use of ultra-thin glass in microfluidics, diagnostic devices, and advanced imaging technologies is poised for significant growth, driven by innovation and the need for sterile, high-precision materials.

Key drivers of dominance in the Asia-Pacific region include favorable government policies, a skilled workforce, and a strong supply chain network. The region's strategic focus on technological advancement and mass production capabilities provides a competitive edge in meeting the global demand for ultra-thin glass.

Ultra-Thin Glass Industry Product Innovations

Recent product innovations in the ultra-thin glass industry are revolutionizing material capabilities. Companies are developing ultra-thin glass with enhanced flexural strength, superior scratch resistance, and advanced optical properties, making them ideal for curved displays and foldable devices. These innovations include advanced chemical strengthening techniques that impart exceptional durability, enabling applications like flexible OLED displays and fingerprint sensors that require ultra-thin, resilient cover glass. Furthermore, developments in anti-reflective coatings and oleophobic treatments are enhancing user experience in touch panel displays. Performance metrics highlight a xx% improvement in impact resistance and a xx% reduction in light reflection for new product iterations.

Propelling Factors for Ultra-Thin Glass Industry Growth

The ultra-thin glass industry is experiencing robust growth driven by several key factors. Technologically, advancements in manufacturing processes like fusion drawing and chemical strengthening have enabled the production of thinner, more durable, and flexible glass at competitive costs. Economically, the escalating demand for premium smartphones, high-resolution displays, and advanced automotive features directly fuels the need for ultra-thin glass. The growing trend towards miniaturization and lightweighting in electronics and automotive applications also presents a significant advantage. Regulatory influences, such as mandates for improved vehicle safety and energy efficiency, further encourage the adoption of lighter materials like ultra-thin glass in the automotive sector. The increasing investment in consumer electronics R&D, particularly in areas like foldable displays and wearable technology, is a critical catalyst for market expansion, projected to add millions to the market value.

Obstacles in the Ultra-Thin Glass Industry Market

Despite its promising growth, the ultra-thin glass industry faces several obstacles. High production costs associated with specialized manufacturing equipment and complex processes remain a significant barrier, particularly for smaller players. Supply chain disruptions, exacerbated by geopolitical events and raw material availability, can impact production timelines and profitability, with potential cost increases of up to xx%. Furthermore, achieving consistent quality control for extremely thin glass presents technical challenges, leading to potential yield losses. The high initial investment required for advanced manufacturing facilities deters new entrants, contributing to market concentration. Competitive pressures from alternative materials and established glass manufacturers also necessitate continuous innovation and cost optimization to maintain market share.

Future Opportunities in Ultra-Thin Glass Industry

The ultra-thin glass industry is ripe with future opportunities. The burgeoning demand for flexible and foldable displays in consumer electronics presents a significant growth avenue. The increasing integration of advanced driver-assistance systems (ADAS) and augmented reality (AR) displays in the automotive industry will create new markets for ultra-thin glass. Furthermore, the biotechnology sector is increasingly utilizing ultra-thin glass for microfluidic devices, lab-on-a-chip technologies, and advanced medical imaging, offering substantial untapped potential. The development of ultra-thin glass with specialized functionalities, such as enhanced conductivity or thermal resistance, could unlock applications in emerging fields like wearable electronics and smart textiles. Strategic partnerships and collaborations for R&D will be crucial for capitalizing on these opportunities and driving innovation.

Major Players in the Ultra-Thin Glass Industry Ecosystem

- CSG Holding Co Ltd

- Emerge Glass

- Schott AG

- Central Glass Co Ltd

- AGC Glass Europe

- Taiwan Glass Industry Corporation

- Novalglass

- Fraunhofer FEP

- Nitto Boseki Co Ltd

- Changzhou Almaden Co Ltd

- Nippon Electric Glass Co Ltd

- Corning Incorporated

Key Developments in Ultra-Thin Glass Industry Industry

- 2023: Corning Incorporated announced significant advancements in its Willow Glass product line, enhancing flexibility and durability for foldable displays.

- 2023: AGC Glass Europe expanded its production capacity for ultra-thin glass to meet the growing demand from the automotive and consumer electronics sectors.

- 2022: Schott AG introduced a new generation of ultra-thin glass with improved scratch resistance and optical clarity, targeting high-end display applications.

- 2022: Fraunhofer FEP showcased innovative thin-film coatings for ultra-thin glass, enhancing its functionality for various industrial applications.

- 2021: Taiwan Glass Industry Corporation invested in new manufacturing facilities to scale up its production of ultra-thin glass for the electronics market.

- 2020: Emerge Glass secured substantial funding to accelerate the development and commercialization of its novel ultra-thin glass manufacturing technology.

Strategic Ultra-Thin Glass Industry Market Forecast

The strategic outlook for the ultra-thin glass industry is exceptionally promising, driven by continued technological innovation and expanding application horizons. The market is poised for sustained growth, with projected expansion into new high-value segments. Key growth catalysts include the increasing adoption of foldable and flexible displays in consumer electronics, the integration of advanced glass solutions in next-generation automotive designs, and the emerging applications in the biotechnology and healthcare sectors. Investments in R&D, particularly in enhancing material properties like flexibility, strength, and optical performance, will be critical in capturing future market share. The Base Year: 2025 sets a strong foundation for a xx% CAGR during the Forecast Period: 2025–2033, indicating a market projected to reach millions in value by 2033.

Ultra-Thin Glass Industry Segmentation

-

1. Application

- 1.1. Semiconductor Substrate

- 1.2. Touch Panel Displays

- 1.3. Fingerprint Sensors

- 1.4. Automotive Glazing

- 1.5. Other Applications

-

2. End-user Industry

- 2.1. Consumer Electronics

- 2.2. Automotive

- 2.3. Biotechnology

- 2.4. Other End-user Industries

Ultra-Thin Glass Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Ultra-Thin Glass Industry Regional Market Share

Geographic Coverage of Ultra-Thin Glass Industry

Ultra-Thin Glass Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Semiconductor Substrate

- 5.1.2. Touch Panel Displays

- 5.1.3. Fingerprint Sensors

- 5.1.4. Automotive Glazing

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Consumer Electronics

- 5.2.2. Automotive

- 5.2.3. Biotechnology

- 5.2.4. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Ultra-Thin Glass Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Semiconductor Substrate

- 6.1.2. Touch Panel Displays

- 6.1.3. Fingerprint Sensors

- 6.1.4. Automotive Glazing

- 6.1.5. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Consumer Electronics

- 6.2.2. Automotive

- 6.2.3. Biotechnology

- 6.2.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Asia Pacific Ultra-Thin Glass Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Semiconductor Substrate

- 7.1.2. Touch Panel Displays

- 7.1.3. Fingerprint Sensors

- 7.1.4. Automotive Glazing

- 7.1.5. Other Applications

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Consumer Electronics

- 7.2.2. Automotive

- 7.2.3. Biotechnology

- 7.2.4. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. North America Ultra-Thin Glass Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Semiconductor Substrate

- 8.1.2. Touch Panel Displays

- 8.1.3. Fingerprint Sensors

- 8.1.4. Automotive Glazing

- 8.1.5. Other Applications

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Consumer Electronics

- 8.2.2. Automotive

- 8.2.3. Biotechnology

- 8.2.4. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Ultra-Thin Glass Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Semiconductor Substrate

- 9.1.2. Touch Panel Displays

- 9.1.3. Fingerprint Sensors

- 9.1.4. Automotive Glazing

- 9.1.5. Other Applications

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Consumer Electronics

- 9.2.2. Automotive

- 9.2.3. Biotechnology

- 9.2.4. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. South America Ultra-Thin Glass Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Semiconductor Substrate

- 10.1.2. Touch Panel Displays

- 10.1.3. Fingerprint Sensors

- 10.1.4. Automotive Glazing

- 10.1.5. Other Applications

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Consumer Electronics

- 10.2.2. Automotive

- 10.2.3. Biotechnology

- 10.2.4. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Middle East and Africa Ultra-Thin Glass Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Semiconductor Substrate

- 11.1.2. Touch Panel Displays

- 11.1.3. Fingerprint Sensors

- 11.1.4. Automotive Glazing

- 11.1.5. Other Applications

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Consumer Electronics

- 11.2.2. Automotive

- 11.2.3. Biotechnology

- 11.2.4. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CSG Holding Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Emerge Glass

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Schott AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Central Glass Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 AGC Glass Europe

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Taiwan Glass Industry Corporation*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Novalglass

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Fraunhofer FEP

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nitto Boseki Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Changzhou Almaden Co Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nippon Electric Glass Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Corning Incorporated

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 CSG Holding Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ultra-Thin Glass Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Ultra-Thin Glass Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: Asia Pacific Ultra-Thin Glass Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: Asia Pacific Ultra-Thin Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Ultra-Thin Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Ultra-Thin Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Ultra-Thin Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Ultra-Thin Glass Industry Revenue (billion), by Application 2025 & 2033

- Figure 9: North America Ultra-Thin Glass Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Ultra-Thin Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Ultra-Thin Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Ultra-Thin Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Ultra-Thin Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ultra-Thin Glass Industry Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Ultra-Thin Glass Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ultra-Thin Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Ultra-Thin Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Ultra-Thin Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Ultra-Thin Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Ultra-Thin Glass Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: South America Ultra-Thin Glass Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: South America Ultra-Thin Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: South America Ultra-Thin Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Ultra-Thin Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Ultra-Thin Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Ultra-Thin Glass Industry Revenue (billion), by Application 2025 & 2033

- Figure 27: Middle East and Africa Ultra-Thin Glass Industry Revenue Share (%), by Application 2025 & 2033

- Figure 28: Middle East and Africa Ultra-Thin Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Ultra-Thin Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Ultra-Thin Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Ultra-Thin Glass Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Ultra-Thin Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Ultra-Thin Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 13: Global Ultra-Thin Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Global Ultra-Thin Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 27: Global Ultra-Thin Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 33: Global Ultra-Thin Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Ultra-Thin Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Ultra-Thin Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ultra-Thin Glass Industry?

The projected CAGR is approximately 9.7%.

2. Which companies are prominent players in the Ultra-Thin Glass Industry?

Key companies in the market include CSG Holding Co Ltd, Emerge Glass, Schott AG, Central Glass Co Ltd, AGC Glass Europe, Taiwan Glass Industry Corporation*List Not Exhaustive, Novalglass, Fraunhofer FEP, Nitto Boseki Co Ltd, Changzhou Almaden Co Ltd, Nippon Electric Glass Co Ltd, Corning Incorporated.

3. What are the main segments of the Ultra-Thin Glass Industry?

The market segments include Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.7 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand from Consumer Electronics; Other Drivers.

6. What are the notable trends driving market growth?

Growing Demand from Consumer Electronics.

7. Are there any restraints impacting market growth?

; High Cost of Raw Materials; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ultra-Thin Glass Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ultra-Thin Glass Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ultra-Thin Glass Industry?

To stay informed about further developments, trends, and reports in the Ultra-Thin Glass Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence