Key Insights

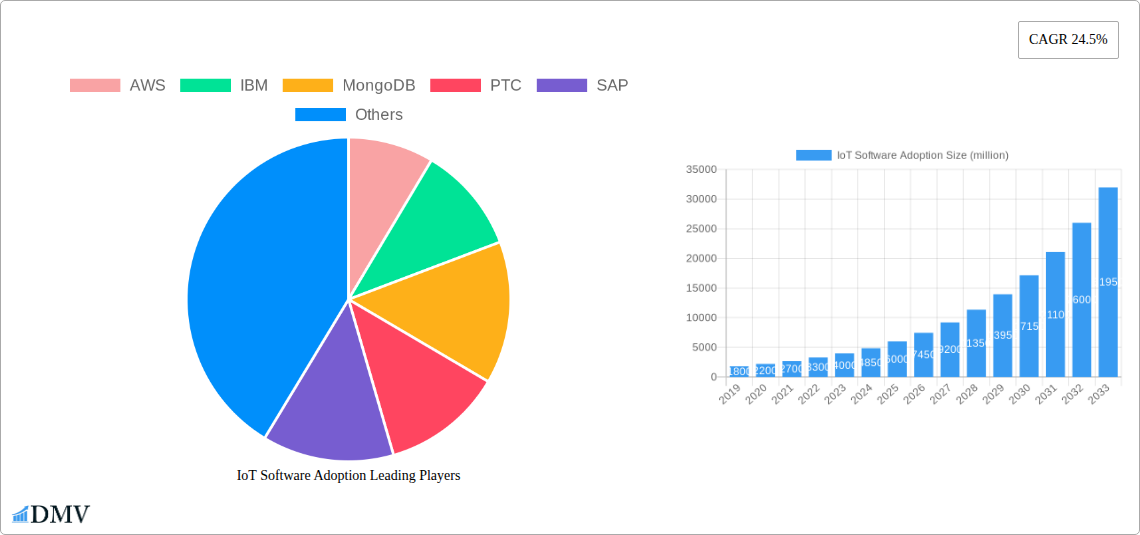

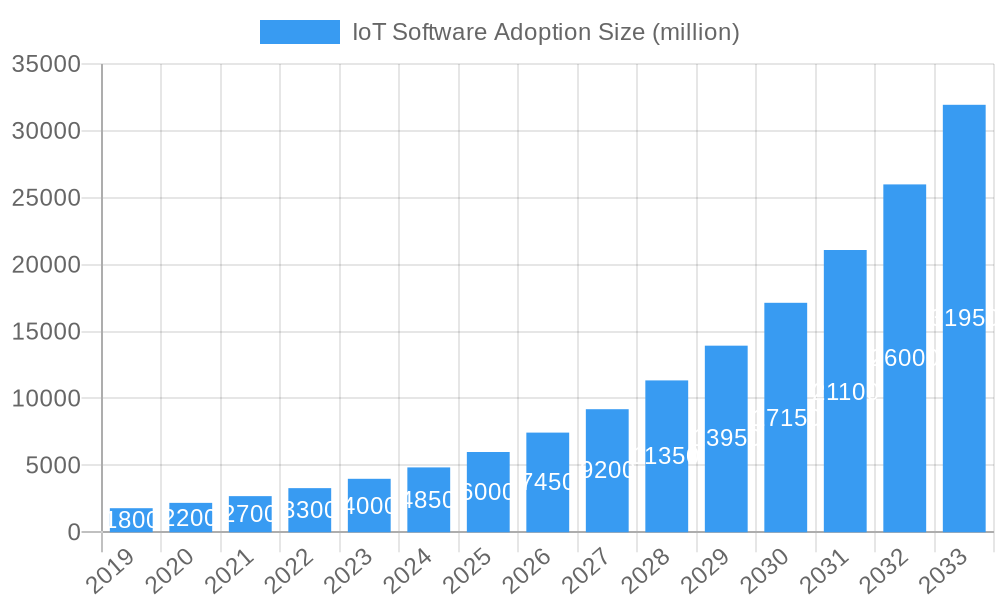

The global IoT Software Adoption market is poised for substantial expansion, projected to reach USD 6000 million by 2025, driven by a remarkable Compound Annual Growth Rate (CAGR) of 24.5% over the forecast period of 2025-2033. This robust growth is fueled by the increasing integration of IoT solutions across diverse industries, from smart manufacturing and healthcare to smart cities and connected vehicles. The escalating demand for real-time data analytics, predictive maintenance, and enhanced operational efficiency are key accelerators. Furthermore, the proliferation of connected devices and the growing need for sophisticated platforms to manage and analyze this vast amount of data are creating significant opportunities for IoT software providers. Small and Medium-sized Enterprises (SMEs) are increasingly adopting IoT solutions to gain a competitive edge, while large enterprises are leveraging them for large-scale digital transformation initiatives.

IoT Software Adoption Market Size (In Billion)

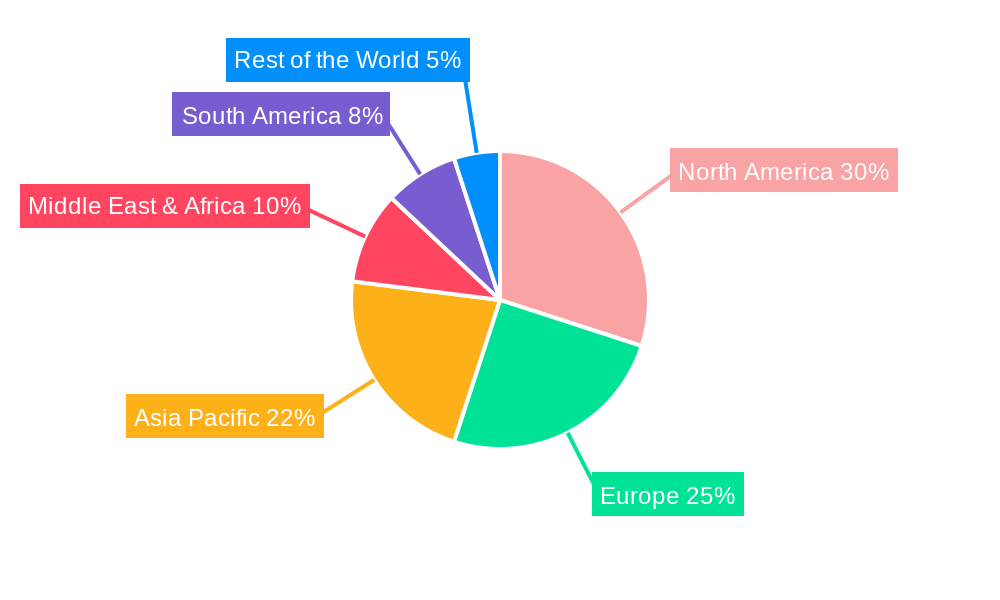

The market dynamics are further shaped by the prevailing trends in cloud-based IoT solutions, offering scalability, flexibility, and cost-effectiveness. While on-premises deployments continue to cater to specific security and regulatory requirements, the cloud segment is expected to dominate. However, certain restraints, such as data security and privacy concerns, the high initial investment costs for some organizations, and the need for skilled personnel to implement and manage IoT solutions, could temper the growth trajectory. Geographically, North America and Europe are leading the adoption, with Asia Pacific showing immense potential due to rapid industrialization and government initiatives promoting smart technologies. The competitive landscape is characterized by the presence of major technology giants like Microsoft, Google, AWS, and IBM, alongside specialized IoT software vendors, all vying for market share through innovation and strategic partnerships.

IoT Software Adoption Company Market Share

This in-depth IoT software adoption market analysis report provides an indispensable roadmap for understanding the dynamic landscape of the Internet of Things (IoT) software ecosystem. Delve into critical trends, strategic investments, and the competitive forces shaping IoT solutions adoption across diverse industries and company sizes. With a study period spanning 2019 to 2033, a base year of 2025, and a forecast period of 2025–2033, this report offers unparalleled foresight into market evolution. Discover how leading players like AWS, IBM, MongoDB, PTC, SAP, Cisco, Google, Microsoft, Oracle, and Siemens are innovating and expanding their IoT platform offerings.

IoT Software Adoption Market Composition & Trends

The IoT software adoption market exhibits a dynamic concentration, driven by continuous innovation and evolving regulatory frameworks. Key trends include the increasing demand for cloud-based IoT solutions and the strategic integration of edge computing capabilities. Stakeholders can gain valuable insights into market share distribution, with significant contributions from major technology providers. Mergers and acquisitions (M&A) are a prominent feature, with a projected M&A deal value of over $500 million within the forecast period, reflecting consolidation and strategic expansion. The analysis encompasses an evaluation of substitute products, enabling stakeholders to understand competitive alternatives and identify market vulnerabilities. Furthermore, the report details end-user profiles, categorizing adoption patterns between SMEs and Large Enterprises, providing a granular view of market penetration.

- Market Concentration: Driven by major cloud providers and specialized IoT software vendors.

- Innovation Catalysts: AI/ML integration, 5G deployment, and advanced analytics.

- Regulatory Landscapes: Evolving data privacy laws and industry-specific compliance requirements.

- Substitute Products: Traditional software solutions with limited IoT integration capabilities.

- End-User Profiles: Detailed segmentation for SMEs and Large Enterprises.

- M&A Activities: Strategic acquisitions to expand platform capabilities and market reach.

IoT Software Adoption Industry Evolution

The IoT software adoption industry is on a robust growth trajectory, fueled by transformative technological advancements and a palpable shift in consumer and enterprise demands. The historical period from 2019 to 2024 witnessed foundational growth, primarily driven by early adopters in manufacturing and logistics leveraging IoT platforms for operational efficiency. As we move into the forecast period of 2025–2033, the market is projected to accelerate significantly, with an anticipated Compound Annual Growth Rate (CAGR) of approximately 18%. This expansion is underpinned by the increasing ubiquity of connected devices, the maturation of IoT security solutions, and the growing need for real-time data analytics to derive actionable insights. Technological breakthroughs, including the widespread implementation of artificial intelligence (AI) and machine learning (ML) within IoT software, are enabling more sophisticated predictive maintenance, enhanced asset tracking, and personalized customer experiences. Enterprises are increasingly recognizing the strategic imperative of embracing IoT solutions to gain a competitive edge, optimize supply chains, and develop innovative revenue streams. The adoption metrics are showing a clear preference for cloud-based IoT software due to its scalability, flexibility, and cost-effectiveness, although on-premises IoT solutions remain relevant for organizations with stringent data sovereignty or security requirements. This evolution signifies a move from basic connectivity to intelligent, data-driven ecosystems that are transforming industries.

Leading Regions, Countries, or Segments in IoT Software Adoption

North America currently leads the IoT software adoption market, driven by a confluence of factors including significant investment in advanced technologies, a robust presence of leading IoT software vendors such as Microsoft, AWS, and IBM, and proactive government initiatives fostering digital transformation. The region's dominance is further amplified by a high adoption rate of cloud-based IoT solutions among both Large Enterprises and an increasingly tech-savvy SME segment. The sheer volume of data generated and the advanced analytical capabilities deployed for insights extraction solidify North America's position as a frontrunner.

Key drivers for this leadership include:

- Investment Trends: Substantial venture capital and corporate R&D investments in IoT technologies, estimated to exceed $80 billion annually in North America by 2025.

- Regulatory Support: Favorable policies and standards promoting IoT deployment and data utilization, encouraging innovation and adoption.

- Technological Infrastructure: Widespread availability of high-speed internet and 5G networks, crucial for seamless IoT operations.

- Enterprise Digitization Push: A strong emphasis on digital transformation across industries, with IoT software seen as a critical enabler.

While Large Enterprises continue to be major adopters, the SME segment is rapidly expanding its footprint, leveraging accessible cloud IoT platforms to improve operational efficiency and customer engagement. The preference for cloud deployment models is paramount due to their inherent scalability and reduced upfront infrastructure costs, making advanced IoT capabilities accessible to a broader market.

IoT Software Adoption Product Innovations

The IoT software adoption landscape is being reshaped by groundbreaking product innovations focused on enhancing device management, data analytics, and security. Vendors are introducing AI-powered predictive maintenance modules, offering unparalleled uptime and reduced operational costs. Advanced analytics dashboards provide real-time, actionable insights from massive data streams, enabling faster decision-making. Furthermore, robust IoT security solutions are incorporating blockchain and advanced encryption to safeguard connected devices and sensitive data. The unique selling propositions often lie in the seamless integration of these functionalities within comprehensive IoT platforms, catering to diverse industry needs from manufacturing to healthcare.

Propelling Factors for IoT Software Adoption Growth

Several key factors are propelling the growth of the IoT software adoption market. Technologically, the widespread deployment of 5G networks offers enhanced connectivity and reduced latency, crucial for real-time IoT applications. Economically, the increasing realization of ROI through operational efficiency, cost reduction, and new revenue streams is a significant driver. Regulatory shifts, such as government initiatives promoting smart cities and industrial digitalization, also provide a supportive environment. The growing demand for data analytics to derive actionable insights from connected devices further fuels adoption.

Obstacles in the IoT Software Adoption Market

Despite strong growth, the IoT software adoption market faces several obstacles. Security concerns remain paramount, with the increasing number of connected devices creating larger attack surfaces. Data privacy regulations and compliance complexities can hinder deployment in certain regions. Interoperability issues between different IoT platforms and devices continue to pose integration challenges, leading to increased implementation costs and time. Supply chain disruptions, amplified by global events, can impact the availability of hardware components necessary for IoT solutions.

Future Opportunities in IoT Software Adoption

The future of IoT software adoption is rife with opportunities. The expansion of edge computing presents a significant avenue for processing data closer to the source, enabling faster insights and reducing bandwidth requirements. The burgeoning Industrial IoT (IIoT) sector, particularly in smart manufacturing and energy management, offers substantial growth potential. Furthermore, the integration of IoT with emerging technologies like extended reality (XR) will unlock new immersive applications for training, maintenance, and remote assistance. The growing focus on sustainability is also driving demand for IoT solutions that optimize resource management and reduce environmental impact.

Major Players in the IoT Software Adoption Ecosystem

- AWS

- IBM

- MongoDB

- PTC

- SAP

- Cisco

- Microsoft

- Oracle

- Siemens

Key Developments in IoT Software Adoption Industry

- 2023 Q4: Microsoft launches Azure IoT Edge improvements for enhanced edge analytics.

- 2024 Q1: Cisco announces strategic partnerships to bolster IoT security offerings.

- 2024 Q2: SAP integrates AI capabilities into its IoT platform for predictive maintenance.

- 2024 Q3: IBM expands its hybrid cloud IoT solutions for industrial enterprises.

- 2024 Q4: PTC strengthens its ThingWorx platform with new AR and IoT integration features.

- 2025 Q1: Google Cloud introduces new IoT data analytics tools for faster insights.

- 2025 Q2: AWS unveils expanded capabilities for IoT device management and security.

- 2025 Q3: Oracle announces advancements in its cloud-based IoT solutions for supply chain optimization.

- 2025 Q4: Siemens enhances its industrial IoT offerings with a focus on digital twin integration.

- 2026 Q1: MongoDB introduces enhanced IoT database solutions for scalable data management.

Strategic IoT Software Adoption Market Forecast

The IoT software adoption market is poised for substantial growth, driven by increasing digital transformation initiatives and the intrinsic value of connected technologies. The forecast period 2025–2033 predicts a robust expansion, fueled by advancements in AI, 5G, and edge computing. Key growth catalysts include the relentless pursuit of operational efficiency, the creation of new business models, and the imperative for enhanced data-driven decision-making across all sectors. The market's potential is immense, promising to redefine how businesses operate and interact with the physical world.

IoT Software Adoption Segmentation

-

1. Application

- 1.1. SMEs

- 1.2. Large Enterprises

-

2. Types

- 2.1. Cloud

- 2.2. On-premises

IoT Software Adoption Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

IoT Software Adoption Regional Market Share

Geographic Coverage of IoT Software Adoption

IoT Software Adoption REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global IoT Software Adoption Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. SMEs

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America IoT Software Adoption Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. SMEs

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud

- 6.2.2. On-premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America IoT Software Adoption Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. SMEs

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud

- 7.2.2. On-premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe IoT Software Adoption Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. SMEs

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud

- 8.2.2. On-premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa IoT Software Adoption Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. SMEs

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud

- 9.2.2. On-premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific IoT Software Adoption Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. SMEs

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud

- 10.2.2. On-premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 AWS

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 IBM

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 MongoDB

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 PTC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SAP

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 cisco

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Google

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Microsoft

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Oracle

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Siemens

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 AWS

List of Figures

- Figure 1: Global IoT Software Adoption Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America IoT Software Adoption Revenue (million), by Application 2025 & 2033

- Figure 3: North America IoT Software Adoption Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America IoT Software Adoption Revenue (million), by Types 2025 & 2033

- Figure 5: North America IoT Software Adoption Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America IoT Software Adoption Revenue (million), by Country 2025 & 2033

- Figure 7: North America IoT Software Adoption Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America IoT Software Adoption Revenue (million), by Application 2025 & 2033

- Figure 9: South America IoT Software Adoption Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America IoT Software Adoption Revenue (million), by Types 2025 & 2033

- Figure 11: South America IoT Software Adoption Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America IoT Software Adoption Revenue (million), by Country 2025 & 2033

- Figure 13: South America IoT Software Adoption Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe IoT Software Adoption Revenue (million), by Application 2025 & 2033

- Figure 15: Europe IoT Software Adoption Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe IoT Software Adoption Revenue (million), by Types 2025 & 2033

- Figure 17: Europe IoT Software Adoption Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe IoT Software Adoption Revenue (million), by Country 2025 & 2033

- Figure 19: Europe IoT Software Adoption Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa IoT Software Adoption Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa IoT Software Adoption Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa IoT Software Adoption Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa IoT Software Adoption Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa IoT Software Adoption Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa IoT Software Adoption Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific IoT Software Adoption Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific IoT Software Adoption Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific IoT Software Adoption Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific IoT Software Adoption Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific IoT Software Adoption Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific IoT Software Adoption Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global IoT Software Adoption Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global IoT Software Adoption Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global IoT Software Adoption Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global IoT Software Adoption Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global IoT Software Adoption Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global IoT Software Adoption Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global IoT Software Adoption Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global IoT Software Adoption Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global IoT Software Adoption Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global IoT Software Adoption Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global IoT Software Adoption Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global IoT Software Adoption Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global IoT Software Adoption Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global IoT Software Adoption Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global IoT Software Adoption Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global IoT Software Adoption Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global IoT Software Adoption Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global IoT Software Adoption Revenue million Forecast, by Country 2020 & 2033

- Table 40: China IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific IoT Software Adoption Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the IoT Software Adoption?

The projected CAGR is approximately 24.5%.

2. Which companies are prominent players in the IoT Software Adoption?

Key companies in the market include AWS, IBM, MongoDB, PTC, SAP, cisco, Google, Microsoft, Oracle, Siemens.

3. What are the main segments of the IoT Software Adoption?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 6000 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "IoT Software Adoption," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the IoT Software Adoption report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the IoT Software Adoption?

To stay informed about further developments, trends, and reports in the IoT Software Adoption, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence