Key Insights

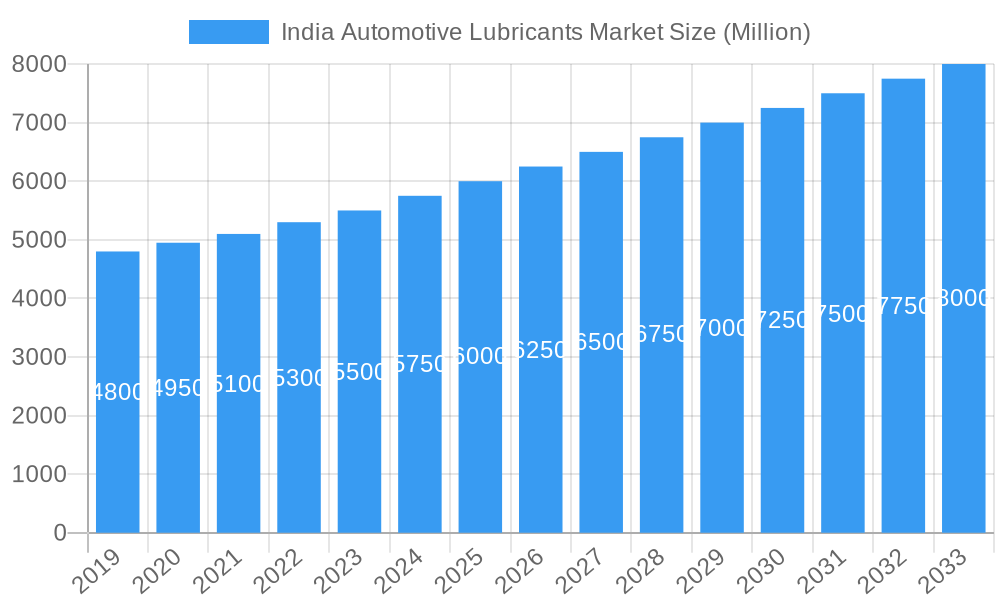

The Indian automotive lubricants market is projected to experience significant growth, reaching a market size of $6.94 billion by 2024. The market is expected to expand at a Compound Annual Growth Rate (CAGR) of 6.61% from the base year 2024 to 2033. This expansion is driven by several key factors. The burgeoning automotive sector, marked by increasing vehicle production and a growing fleet across passenger cars, commercial vehicles, and two-wheelers, forms the primary demand driver. Rising disposable incomes and a growing consumer preference for enhanced vehicle performance and longevity are also contributing to the demand for high-quality lubricants. Furthermore, stricter emission standards and a focus on fuel efficiency are prompting vehicle owners to adopt advanced synthetic and semi-synthetic lubricant formulations, thereby boosting market growth. Infrastructure development and industrialization initiatives across India are indirectly stimulating demand for commercial vehicles and their associated lubricant requirements.

India Automotive Lubricants Market Market Size (In Billion)

The Indian automotive lubricants market is undergoing a significant transformation influenced by technological advancements and shifting consumer behavior. Key trends include a pronounced shift towards synthetic and semi-synthetic lubricants, offering superior performance, extended drain intervals, and improved fuel economy compared to conventional mineral oils. This demand is further amplified by increasingly stringent emission regulations and growing consumer awareness of the environmental and cost benefits of advanced lubricant technologies. The passenger vehicle segment is anticipated to lead, followed by commercial vehicles and motorcycles, each presenting distinct growth opportunities. Among product types, engine oils will continue to command the largest share, with a notable increase expected in greases and transmission fluids due to the growing complexity of modern automotive powertrains. While the market faces intense competition from established global and domestic players, potential challenges may arise from fluctuating raw material prices and the increasing adoption of electric vehicles, which require specialized lubrication solutions. However, the substantial existing fleet of internal combustion engine vehicles and projected growth in conventional vehicle sales in the medium term ensure sustained demand for automotive lubricants.

India Automotive Lubricants Market Company Market Share

This comprehensive report provides a critical analysis of the India automotive lubricants market, a dynamic sector poised for significant expansion driven by robust automotive sales and evolving technological demands. Covering the forecast period from the base year 2024 through 2033, this report offers unparalleled insights into market composition, trends, industry evolution, key segments, product innovations, growth drivers, obstacles, and future opportunities. Leverage this definitive resource for strategic decision-making, investment planning, and competitive intelligence within the Indian lubricant industry.

India Automotive Lubricants Market Market Composition & Trends

The India automotive lubricants market exhibits a competitive landscape with a moderate to high degree of concentration, dominated by established public and private sector players. Innovation catalysts are primarily driven by the demand for higher performance engine oils, eco-friendly lubricants, and specialized fluids for newer vehicle technologies. Regulatory landscapes, guided by emission norms and fuel efficiency standards, are increasingly influencing product development and adoption. Substitute products, such as advanced greases and synthetic fluids, are gaining traction. End-user profiles vary significantly, ranging from individual vehicle owners to large fleet operators and commercial vehicle manufacturers. Mergers & Acquisitions (M&A) activities are anticipated to intensify as companies seek to expand their product portfolios and geographical reach. M&A deal values are projected to increase as consolidation efforts accelerate.

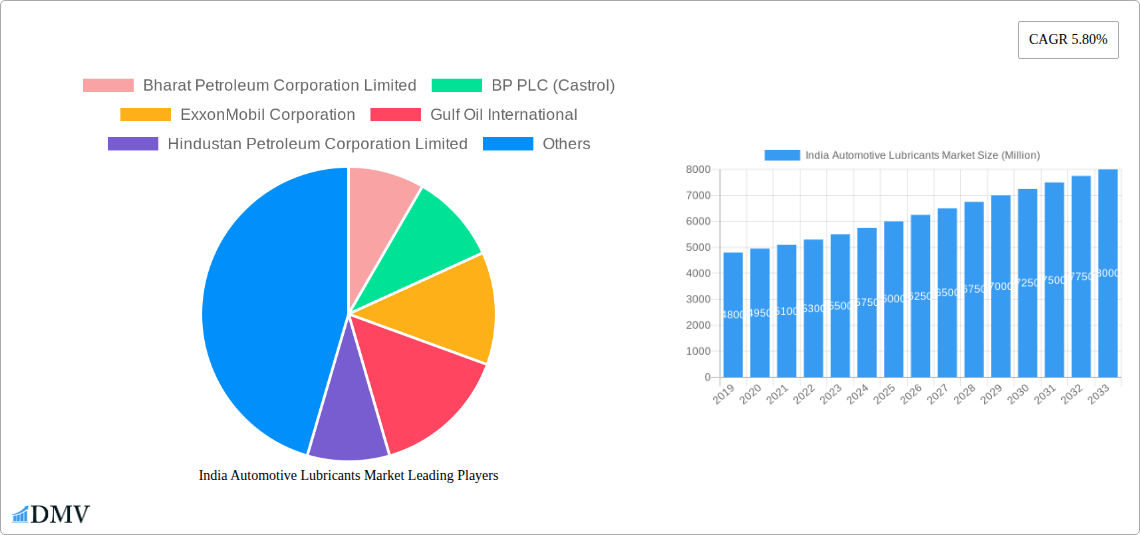

- Market Share Distribution: Key players like Indian Oil Corporation Limited, Bharat Petroleum Corporation Limited, and Hindustan Petroleum Corporation Limited hold significant market shares in the conventional lubricants segment. However, global players such as BP PLC (Castrol), ExxonMobil Corporation, and Royal Dutch Shell Plc are actively increasing their presence, particularly in the synthetic and premium lubricant segments.

- Innovation Focus: Emphasis on Extended Drain Intervals (EDIs), improved fuel economy, and enhanced wear protection are key innovation drivers. The increasing adoption of electric vehicles (EVs) is also beginning to influence the demand for specialized EV fluids, although traditional internal combustion engine (ICE) lubricants will remain dominant throughout the forecast period.

- Regulatory Impact: Stringent BS-VI emission norms are compelling lubricant manufacturers to develop advanced formulations that can withstand higher operating temperatures and offer superior protection to complex engine components.

India Automotive Lubricants Market Industry Evolution

The India automotive lubricants market has witnessed a transformative evolution, marked by consistent growth and increasing sophistication. Historically, the market was primarily driven by the demand for basic mineral-based lubricants for a growing fleet of passenger vehicles and commercial vehicles. However, the past decade has seen a paradigm shift towards high-performance, synthetic, and semi-synthetic lubricants. This evolution is intricately linked to the country's burgeoning automotive sector, which has experienced robust sales growth across all vehicle types. The increasing disposable incomes, coupled with a rising middle class, have fueled the demand for premium vehicles and, consequently, premium lubricants. Technological advancements in engine design, including turbocharging and direct injection, have necessitated the development of lubricants with enhanced thermal stability, oxidative resistance, and detergency. Furthermore, the Indian government's focus on improving fuel efficiency and reducing emissions, exemplified by the adoption of stricter emission standards like BS-VI, has been a significant catalyst for innovation. Lubricant manufacturers are continuously investing in R&D to formulate products that meet these evolving standards, offering improved engine protection, extended drain intervals, and reduced friction, thereby contributing to better fuel economy. The Indian lubricant industry is also experiencing a growing awareness among consumers about the importance of using the right lubricant for optimal vehicle performance and longevity. This awareness is being fostered through extensive marketing campaigns and after-sales services offered by leading players. The increasing complexity of automotive components and the growing adoption of advanced technologies like hybrid powertrains are creating a sustained demand for specialized and technologically superior lubricant solutions, propelling the market towards further growth and sophistication in the coming years. The market growth trajectory is estimated to be around 5-7% CAGR during the forecast period.

Leading Regions, Countries, or Segments in India Automotive Lubricants Market

The India automotive lubricants market is segmented by Vehicle Type and Product Type, with distinct regional and segment-specific dominance factors.

Dominant Vehicle Types:

Commercial Vehicles: This segment is a cornerstone of the Indian automotive lubricants market, propelled by robust economic activity, infrastructure development, and the burgeoning e-commerce sector.

- Key Drivers: Increasing freight movement, government initiatives promoting logistics, and the continuous replacement of older fleets with more fuel-efficient and technologically advanced trucks and buses. The adoption of BS-VI compliant engines in commercial vehicles necessitates the use of high-performance lubricants.

- Dominance Factors: The sheer volume of commercial vehicles operating daily across India, coupled with their demanding operational cycles and the critical role lubricants play in ensuring engine longevity and operational uptime, solidifies this segment's leading position. Fleet operators are increasingly investing in premium lubricants to reduce maintenance costs and minimize breakdowns.

Passenger Vehicles: The passenger vehicle segment contributes significantly to the lubricant market, driven by urbanization, rising disposable incomes, and the expanding middle class.

- Key Drivers: Growing car ownership, a preference for feature-rich and fuel-efficient vehicles, and the increasing popularity of SUVs and compact SUVs. The demand for synthetic and semi-synthetic engine oils is particularly high in this segment.

- Dominance Factors: The large and growing installed base of passenger cars, coupled with a consumer mindset that increasingly values vehicle maintenance and performance, makes this segment a consistent driver of lubricant consumption. Longer warranty periods also encourage the use of manufacturer-approved and high-quality lubricants.

Dominant Product Types:

Engine Oils: As the most critical lubricant for any internal combustion engine, engine oils command the largest market share.

- Key Drivers: Universal application across all vehicle types, the continuous need for engine protection against wear, heat, and contaminants, and the evolution towards more advanced formulations meeting stricter emission and fuel economy standards.

- Dominance Factors: The fundamental requirement of every engine for lubrication, coupled with the rapid pace of technological advancements in engine design, ensures sustained demand for a wide range of engine oils, from conventional mineral oils to high-performance synthetics. The increasing complexity of modern engines, especially those meeting BS-VI norms, further accentuates the need for sophisticated engine oil formulations.

Transmission & Gear Oils: This segment is also crucial, especially for the smooth functioning of transmissions and gearboxes in both manual and automatic vehicles.

- Key Drivers: The increasing complexity of modern transmissions, including automatic and CVT systems, and the demanding operational conditions in heavy-duty applications.

- Dominance Factors: The essential role of transmission and gear oils in reducing friction, preventing wear, and ensuring efficient power transfer across various vehicle types, particularly in commercial vehicles and performance-oriented passenger cars, contributes to its significant market presence.

India Automotive Lubricants Market Product Innovations

The India automotive lubricants market is witnessing a wave of innovation focused on enhancing performance, extending lifespan, and meeting stringent environmental regulations. Key innovations include the development of extended drain interval (EDI) engine oils that allow for longer service periods, reducing maintenance frequency and costs for consumers. Manufacturers are also introducing ultra-low viscosity synthetic engine oils designed to improve fuel efficiency and reduce CO2 emissions, aligning with global sustainability trends and India's emission norms. Furthermore, specialized lubricants for electric vehicles (EVs) are emerging, catering to the unique thermal management and lubrication needs of electric powertrains, including battery cooling and gearbox lubrication. The application of advanced additive technologies, such as nano-particles and friction modifiers, is leading to improved wear protection and reduced operational temperatures.

Propelling Factors for India Automotive Lubricants Market Growth

The India automotive lubricants market is experiencing substantial growth propelled by a confluence of factors. The robust expansion of the Indian automotive industry, characterized by increasing vehicle production and sales across passenger vehicles, commercial vehicles, and two-wheelers, directly translates to higher lubricant demand. Furthermore, the continuous upgrade of automotive technologies, including the widespread adoption of BS-VI emission standards, necessitates the use of advanced, high-performance lubricants that offer superior protection and efficiency. Government initiatives promoting domestic manufacturing and "Make in India" are also fostering local production and innovation in the lubricant sector. Economic growth, rising disposable incomes, and evolving consumer preferences towards premium and technologically advanced vehicles further fuel the demand for higher-quality lubricants. The increasing awareness among vehicle owners regarding the importance of timely maintenance and the use of appropriate lubricants to enhance vehicle lifespan and performance also plays a crucial role.

Obstacles in the India Automotive Lubricants Market Market

Despite the positive growth trajectory, the India automotive lubricants market faces several obstacles. Intense price competition among established and unorganized players can lead to margin pressures and hinder investment in advanced R&D. The presence of a significant unorganized sector selling counterfeit and sub-standard lubricants poses a threat to quality and brand reputation, eroding consumer trust. Fluctuations in crude oil prices, the primary feedstock for lubricants, can impact manufacturing costs and pricing strategies. Supply chain disruptions, exacerbated by logistical challenges and geopolitical factors, can affect the availability and cost of raw materials. Furthermore, evolving vehicle technologies, particularly the gradual transition towards electric vehicles, may eventually reduce the demand for traditional internal combustion engine lubricants, requiring manufacturers to adapt their product portfolios and business models.

Future Opportunities in India Automotive Lubricants Market

The India automotive lubricants market presents numerous future opportunities. The increasing demand for high-performance synthetic and semi-synthetic lubricants, driven by stringent emission norms and the desire for enhanced fuel economy, will continue to be a significant growth avenue. The rapidly expanding EV market in India opens up opportunities for specialized EV fluids, including coolants, transmission fluids, and greases designed for electric powertrains. The growing automotive aftermarket, coupled with the increasing lifespan of vehicles, will sustain demand for reliable and high-quality lubricants. Furthermore, the potential for expansion into Tier 2 and Tier 3 cities, where awareness and adoption of premium lubricants are still nascent, offers considerable untapped market potential. Collaborations and partnerships with automotive OEMs for co-branded lubricants and technological development will also be crucial for capturing future market share.

Major Players in the India Automotive Lubricants Market Ecosystem

- Bharat Petroleum Corporation Limited

- BP PLC (Castrol)

- ExxonMobil Corporation

- Gulf Oil International

- Hindustan Petroleum Corporation Limited

- Idemitsu Kosan Co Ltd

- Indian Oil Corporation Limited

- PETRONAS Lubricants International

- Royal Dutch Shell Plc

- TIDE WATER OIL CO (INDIA) LTD

- TotalEnergies

- Valvoline Inc

Key Developments in India Automotive Lubricants Market Industry

- January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions. This strategic realignment is expected to enhance operational efficiency and focus on evolving market demands, including the lubricant sector.

- December 2021: ExxonMobil introduced a line of synthetic engine oils, i.e., Mobil Super Pro, for SUVs in India, catering to the growing demand for high-performance lubricants in this popular vehicle segment.

- October 2021: Valvoline and Cummins extended their long-standing marketing and technology collaboration agreement for another five years. Cummins will endorse and promote Valvoline's Premium Blue engine oil for its heavy-duty diesel engines and generators and will distribute Valvoline products through its global distribution networks, strengthening Valvoline's position in the heavy-duty lubricant market.

Strategic India Automotive Lubricants Market Market Forecast

The India automotive lubricants market is poised for strategic growth, fueled by the persistent expansion of its automotive sector and the increasing adoption of advanced vehicle technologies. The forecast period is characterized by a rising demand for synthetic and semi-synthetic lubricants, driven by stricter emission standards and a growing consumer consciousness towards fuel efficiency and enhanced engine performance. The significant installed base of commercial vehicles, coupled with ongoing infrastructure development, will continue to be a strong demand driver. Furthermore, the nascent yet rapidly growing electric vehicle (EV) segment presents a novel opportunity for specialized EV fluids, signaling a long-term diversification strategy for lubricant manufacturers. Key players are expected to focus on product innovation, strategic partnerships with OEMs, and expanding their distribution networks to capture a larger market share, positioning the market for sustained value creation and robust growth in the coming years.

India Automotive Lubricants Market Segmentation

-

1. Vehicle Type

- 1.1. Commercial Vehicles

- 1.2. Motorcycles

- 1.3. Passenger Vehicles

-

2. Product Type

- 2.1. Engine Oils

- 2.2. Greases

- 2.3. Hydraulic Fluids

- 2.4. Transmission & Gear Oils

India Automotive Lubricants Market Segmentation By Geography

- 1. India

India Automotive Lubricants Market Regional Market Share

Geographic Coverage of India Automotive Lubricants Market

India Automotive Lubricants Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.61% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Commercial Vehicles

- 5.1.2. Motorcycles

- 5.1.3. Passenger Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Engine Oils

- 5.2.2. Greases

- 5.2.3. Hydraulic Fluids

- 5.2.4. Transmission & Gear Oils

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. India Automotive Lubricants Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Commercial Vehicles

- 6.1.2. Motorcycles

- 6.1.3. Passenger Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Engine Oils

- 6.2.2. Greases

- 6.2.3. Hydraulic Fluids

- 6.2.4. Transmission & Gear Oils

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bharat Petroleum Corporation Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 BP PLC (Castrol)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 ExxonMobil Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gulf Oil International

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Hindustan Petroleum Corporation Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Idemitsu Kosan Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Indian Oil Corporation Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PETRONAS Lubricants International

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Royal Dutch Shell Plc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 TIDE WATER OIL CO (INDIA) LTD

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 TotalEnergies

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Valvoline Inc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Bharat Petroleum Corporation Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Automotive Lubricants Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Automotive Lubricants Market Share (%) by Company 2025

List of Tables

- Table 1: India Automotive Lubricants Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: India Automotive Lubricants Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: India Automotive Lubricants Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: India Automotive Lubricants Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 5: India Automotive Lubricants Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: India Automotive Lubricants Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Automotive Lubricants Market?

The projected CAGR is approximately 6.61%.

2. Which companies are prominent players in the India Automotive Lubricants Market?

Key companies in the market include Bharat Petroleum Corporation Limited, BP PLC (Castrol), ExxonMobil Corporation, Gulf Oil International, Hindustan Petroleum Corporation Limited, Idemitsu Kosan Co Ltd, Indian Oil Corporation Limited, PETRONAS Lubricants International, Royal Dutch Shell Plc, TIDE WATER OIL CO (INDIA) LTD, TotalEnergies, Valvoline Inc.

3. What are the main segments of the India Automotive Lubricants Market?

The market segments include Vehicle Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.94 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Largest Segment By Vehicle Type : Commercial Vehicles.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.December 2021: ExxonMobil introduced a line of synthetic engine oils, i.e., Mobil Super Pro, for SUVs in India.October 2021: Valvoline and Cummins extended their long-standing marketing and technology collaboration agreement for another five years. Cummins will endorse and promote Valvoline's Premium Blue engine oil for its heavy-duty diesel engines and generators and will distribute Valvoline products through its global distribution networks.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Automotive Lubricants Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Automotive Lubricants Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Automotive Lubricants Market?

To stay informed about further developments, trends, and reports in the India Automotive Lubricants Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence