Key Insights

The global Healthcare Data market is projected for significant expansion, with an estimated market size of 3.1 billion USD by 2024. A robust Compound Annual Growth Rate (CAGR) of 13.36% is anticipated from 2024-2033. This growth is propelled by the exponential increase in healthcare data generation, coupled with the widespread adoption of advanced analytics and AI for actionable insights. Digital transformation, including Electronic Health Records (EHRs), wearables, and telehealth, has created a rich data environment. Key drivers include the demand for personalized medicine, improved patient outcomes, and optimized healthcare operations. The market is shifting towards scalable, cost-effective, and secure cloud-based solutions, enhancing informed decision-making, diagnostics, treatment plans, and proactive population health management.

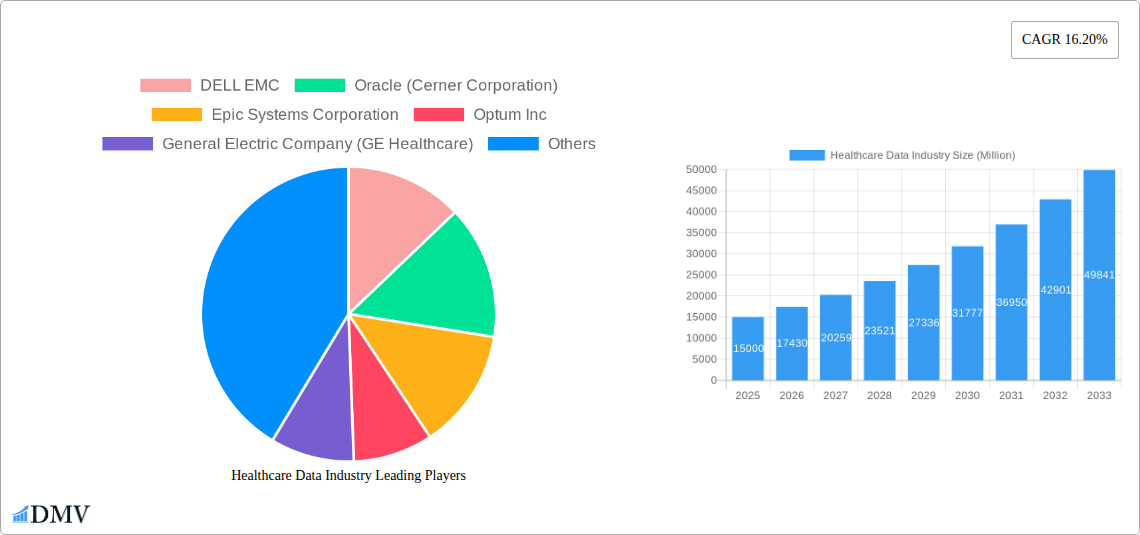

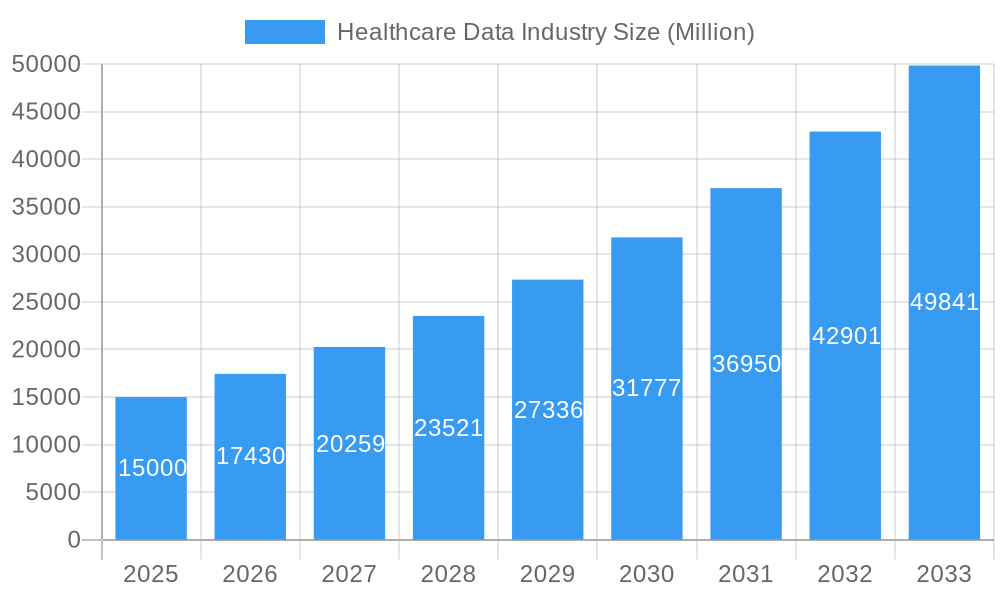

Healthcare Data Industry Market Size (In Billion)

Market segmentation highlights the critical roles of software and services in leveraging healthcare data. Diversifying applications include financial analytics for revenue cycle management, clinical data analytics for patient care quality, operational analytics for workflow streamlining, and population health analytics for preventive care. The competitive landscape features established technology firms and specialized analytics providers offering innovative solutions. Strategic collaborations and M&A activities are expected to consolidate expertise and expand offerings within the global healthcare ecosystem.

Healthcare Data Industry Company Market Share

This report offers an in-depth analysis of the global Healthcare Data Industry, examining its impact on healthcare delivery, operational efficiency, and patient outcomes. Covering the study period of 2019–2033, with a Base Year of 2024, it provides critical insights into market dynamics, key players, emerging trends, and future growth. Explore Software and Services segments, On-premise and Cloud deployment models, and pivotal applications in Financial Analytics, Clinical Data Analytics, Operational Analytics, and Population Health Analytics. The report details how advancements in big data analytics in healthcare, healthcare cloud computing, and clinical data management are reshaping the industry, driving innovation, and creating value.

Healthcare Data Industry Market Composition & Trends

The Healthcare Data Industry exhibits a dynamic market concentration driven by a burgeoning demand for data-driven decision-making and enhanced patient care. Innovation catalysts are abundant, fueled by continuous advancements in artificial intelligence (AI) and machine learning (ML) applied to healthcare. The regulatory landscape, while complex, is progressively adapting to support secure and ethical data utilization. Substitute products are limited as the proprietary nature of healthcare data and the need for specialized analytics create high barriers to entry. End-user profiles span from large hospital networks and integrated delivery networks to payers, pharmaceutical companies, and government health agencies, all seeking to leverage data for improved outcomes and cost reduction. Mergers and acquisitions (M&A) are a significant feature, with deal values in the hundreds of millions of dollars as larger players acquire specialized capabilities or expand their market reach. Key trends include the increasing adoption of cloud-based solutions for scalability and accessibility, and the growing emphasis on interoperability to facilitate seamless data exchange. The market share distribution is evolving, with leading providers consolidating their positions while niche players focus on specialized analytics solutions.

Healthcare Data Industry Industry Evolution

The evolution of the Healthcare Data Industry is marked by a significant market growth trajectory, transitioning from rudimentary data storage to sophisticated AI-powered analytical platforms. Over the historical period of 2019–2024, we witnessed a steady increase in the adoption of electronic health records (EHRs) and a growing awareness of the potential locked within healthcare data. Technological advancements, particularly in cloud computing, big data processing, and advanced analytics, have been the primary enablers of this evolution. The introduction of platform-as-a-service (PaaS) offerings, such as Microsoft's Azure Health Data Services in March 2022, further accelerated cloud adoption by providing secure and scalable environments for protected health information (PHI). Shifting consumer demands, driven by patient empowerment and the pursuit of personalized medicine, are compelling providers to harness data for proactive care and tailored treatment plans. For instance, the increasing utilization of predictive analytics in healthcare has led to a reduction in hospital readmissions and improved chronic disease management, with adoption metrics showing a year-over-year growth of over 15%. The forecast period of 2025–2033 anticipates an exponential rise in the application of real-time data analytics for population health management and precision medicine initiatives, further solidifying the industry's pivotal role in the future of healthcare. Growth rates in specific segments like clinical data analytics are projected to exceed 20% annually as AI algorithms become more adept at identifying patterns and predicting health risks.

Leading Regions, Countries, or Segments in Healthcare Data Industry

The Cloud deployment segment is emerging as the dominant force within the Healthcare Data Industry, driven by its inherent scalability, cost-effectiveness, and enhanced accessibility for remote access and collaboration. This dominance is particularly pronounced in North America, specifically the United States, due to a strong existing digital infrastructure, significant investment in healthcare IT, and favorable regulatory frameworks that encourage data innovation.

- Key Drivers in Cloud Dominance:

- Investment Trends: Substantial investments from venture capital and major technology players in cloud-based healthcare solutions, amounting to billions of dollars annually.

- Regulatory Support: Initiatives and frameworks that, while prioritizing data security, also facilitate the responsible adoption of cloud technologies for healthcare data.

- Technological Advancements: Continuous innovation in cloud security, data storage, and processing power makes cloud solutions increasingly attractive and reliable.

- Interoperability Demands: The growing need for seamless data exchange between disparate healthcare systems strongly favors cloud platforms that can integrate various data sources.

Application-wise, Clinical Data Analytics is experiencing unparalleled growth. This segment is crucial for deriving actionable insights from patient records, medical imaging, and genomic data to improve diagnosis, treatment efficacy, and patient outcomes. The ability to analyze complex clinical data in real-time allows for proactive interventions, personalized treatment plans, and the identification of rare diseases. The growing volume of clinical data generated daily, coupled with the increasing sophistication of AI and ML algorithms, fuels this segment's expansion.

- Dominance Factors for Clinical Data Analytics:

- Improved Patient Outcomes: Direct impact on the quality of care, leading to better diagnoses and more effective treatments.

- Research & Development: Essential for drug discovery, clinical trials, and understanding disease progression.

- Data Volume: The sheer amount of unstructured and structured clinical data generated necessitates advanced analytical capabilities.

- AI/ML Integration: The synergistic integration of AI and ML with clinical data unlocks predictive and prescriptive insights previously unattainable.

The Services component, encompassing consulting, integration, and managed services, also plays a critical role, enabling healthcare organizations to effectively implement and leverage these advanced data solutions.

Healthcare Data Industry Product Innovations

Product innovations in the Healthcare Data Industry are primarily focused on enhancing AI-powered diagnostic tools, predictive analytics platforms for population health, and secure cloud data repositories. Unique selling propositions lie in the ability to process vast datasets with exceptional speed and accuracy, leading to improved diagnostic accuracy, personalized treatment regimens, and proactive disease management. For example, advanced natural language processing (NLP) algorithms are now capable of extracting critical information from unstructured clinical notes, contributing to more comprehensive patient profiles and research. Performance metrics demonstrate significant reductions in diagnostic errors and improved efficiency in operational workflows, with some platforms showing up to a 25% improvement in identifying at-risk patient populations.

Propelling Factors for Healthcare Data Industry Growth

The Healthcare Data Industry's growth is propelled by several key factors. Technologically, advancements in artificial intelligence (AI) and machine learning (ML) are enabling more sophisticated data analysis and predictive capabilities. Economically, the increasing pressure to reduce healthcare costs while improving quality drives demand for efficiency gains through data-driven insights. Regulatory influences, such as the push for data interoperability and the development of value-based care models, further incentivize the adoption of healthcare data solutions. The rising volume of healthcare data itself, generated by EHRs, wearables, and genomic sequencing, provides the raw material for these powerful analytical tools.

Obstacles in the Healthcare Data Industry Market

Despite robust growth, the Healthcare Data Industry faces several obstacles. Regulatory challenges, including stringent data privacy laws like HIPAA and GDPR, necessitate substantial compliance efforts and can slow down data sharing and innovation. Supply chain disruptions, though less direct, can impact the availability of hardware and specialized software components crucial for data infrastructure. Competitive pressures are intense, with established tech giants and specialized startups vying for market share, requiring significant investment in R&D and sales. The initial cost of implementing advanced data solutions and the need for skilled personnel to manage and interpret the data also present significant barriers for smaller organizations.

Future Opportunities in Healthcare Data Industry

Emerging opportunities in the Healthcare Data Industry are vast and multifaceted. The expansion of precision medicine, leveraging genomic and molecular data for highly personalized treatments, presents a significant growth avenue. The increasing adoption of IoT devices and wearables is creating new streams of real-time patient data, opening doors for remote patient monitoring and preventative care. Furthermore, the development of federated learning techniques offers a way to train AI models on decentralized data, addressing privacy concerns and unlocking insights from sensitive patient populations. The growing demand for healthcare AI solutions in emerging economies also represents a substantial untapped market.

Major Players in the Healthcare Data Industry Ecosystem

- DELL EMC

- Oracle (Cerner Corporation)

- Epic Systems Corporation

- Optum Inc

- General Electric Company (GE Healthcare)

- International Business Machines Corporation (IBM)

- ExlService Holdings Inc

- Health Fidelity Inc

- Allscripts Healthcare Solutions Inc

- Flatiron Health

- Apixio

- SAS INSTITUTE INC

- Innovaccer Inc

Key Developments in Healthcare Data Industry Industry

- March 2022: Microsoft launched Azure Health Data Services in the United States. This platform-as-a-service (PaaS) offering is designed exclusively to support protected health information (PHI) in the cloud, enhancing secure data management and accessibility for healthcare organizations.

- March 2022: The government of Thailand launched a big data portal for healthcare facilities. The National Reforms Committee on Public Health joined forces with 12 government agencies to improve the quality of healthcare services by implementing digital technologies, signifying a regional push towards data-driven healthcare.

Strategic Healthcare Data Industry Market Forecast

The strategic healthcare data industry market forecast indicates a period of sustained and accelerated growth driven by the increasing demand for AI-driven insights and cloud-native solutions. Future opportunities in precision medicine, population health management, and the expansion of telehealth services will be key catalysts. The continued integration of advanced analytics, including predictive and prescriptive models, will empower healthcare providers to optimize operational efficiencies, enhance patient care, and reduce overall costs. Investments in data interoperability and secure data sharing frameworks will be crucial for unlocking the full potential of healthcare data, ensuring that the industry moves towards a more proactive, personalized, and equitable healthcare future.

Healthcare Data Industry Segmentation

-

1. Component

- 1.1. Software

- 1.2. Services

-

2. Deployment

- 2.1. On-premise

- 2.2. Cloud

-

3. Application

- 3.1. Financial Analytics

- 3.2. Clinical Data Analytics

- 3.3. Operational Analytics

- 3.4. Population Health Analytics

Healthcare Data Industry Segmentation By Geography

-

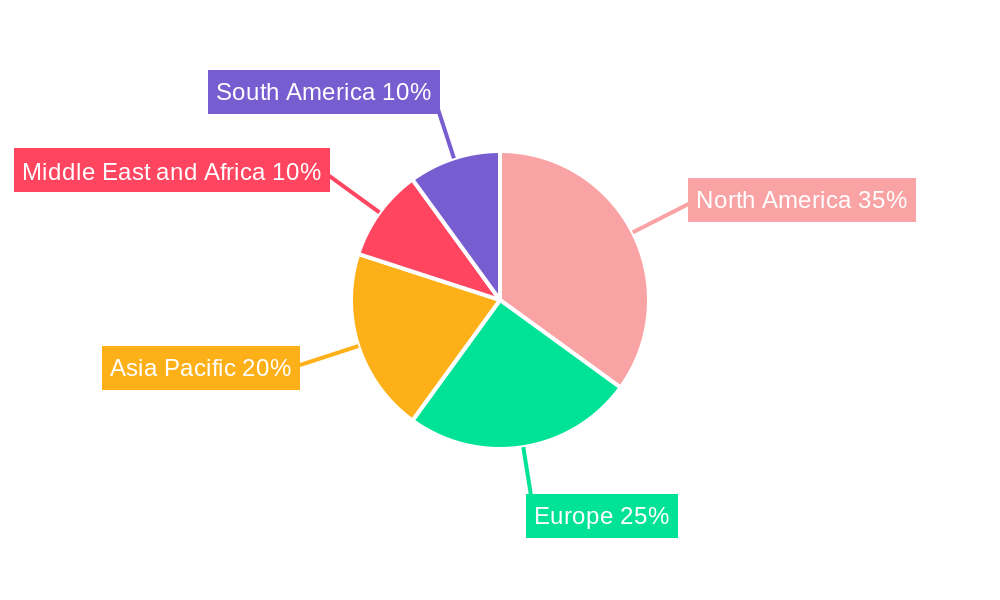

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Healthcare Data Industry Regional Market Share

Geographic Coverage of Healthcare Data Industry

Healthcare Data Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.36% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Software

- 5.1.2. Services

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. On-premise

- 5.2.2. Cloud

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Financial Analytics

- 5.3.2. Clinical Data Analytics

- 5.3.3. Operational Analytics

- 5.3.4. Population Health Analytics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Healthcare Data Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Software

- 6.1.2. Services

- 6.2. Market Analysis, Insights and Forecast - by Deployment

- 6.2.1. On-premise

- 6.2.2. Cloud

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Financial Analytics

- 6.3.2. Clinical Data Analytics

- 6.3.3. Operational Analytics

- 6.3.4. Population Health Analytics

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Software

- 7.1.2. Services

- 7.2. Market Analysis, Insights and Forecast - by Deployment

- 7.2.1. On-premise

- 7.2.2. Cloud

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Financial Analytics

- 7.3.2. Clinical Data Analytics

- 7.3.3. Operational Analytics

- 7.3.4. Population Health Analytics

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Software

- 8.1.2. Services

- 8.2. Market Analysis, Insights and Forecast - by Deployment

- 8.2.1. On-premise

- 8.2.2. Cloud

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Financial Analytics

- 8.3.2. Clinical Data Analytics

- 8.3.3. Operational Analytics

- 8.3.4. Population Health Analytics

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Pacific Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Software

- 9.1.2. Services

- 9.2. Market Analysis, Insights and Forecast - by Deployment

- 9.2.1. On-premise

- 9.2.2. Cloud

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Financial Analytics

- 9.3.2. Clinical Data Analytics

- 9.3.3. Operational Analytics

- 9.3.4. Population Health Analytics

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Middle East and Africa Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Software

- 10.1.2. Services

- 10.2. Market Analysis, Insights and Forecast - by Deployment

- 10.2.1. On-premise

- 10.2.2. Cloud

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Financial Analytics

- 10.3.2. Clinical Data Analytics

- 10.3.3. Operational Analytics

- 10.3.4. Population Health Analytics

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. South America Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Software

- 11.1.2. Services

- 11.2. Market Analysis, Insights and Forecast - by Deployment

- 11.2.1. On-premise

- 11.2.2. Cloud

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Financial Analytics

- 11.3.2. Clinical Data Analytics

- 11.3.3. Operational Analytics

- 11.3.4. Population Health Analytics

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 DELL EMC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Oracle (Cerner Corporation)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Epic Systems Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Optum Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 General Electric Company (GE Healthcare)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 International Business Machines Corporation (IBM)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ExlService Holdings Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Health Fidelity Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Allscripts Healthcare Solutions Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Flatiron Health

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Apixio

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 SAS INSTITUTE INC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Innovaccer Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 DELL EMC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Healthcare Data Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Healthcare Data Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 4: North America Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 5: North America Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 7: North America Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 8: North America Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 9: North America Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 10: North America Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 11: North America Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 12: North America Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 13: North America Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 20: Europe Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 21: Europe Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 22: Europe Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 23: Europe Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 24: Europe Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 25: Europe Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 26: Europe Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 27: Europe Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 29: Europe Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Europe Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 36: Asia Pacific Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 37: Asia Pacific Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 38: Asia Pacific Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 39: Asia Pacific Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 40: Asia Pacific Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 41: Asia Pacific Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 42: Asia Pacific Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 43: Asia Pacific Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 44: Asia Pacific Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Asia Pacific Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Asia Pacific Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Asia Pacific Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Asia Pacific Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 52: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 53: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 54: Middle East and Africa Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 55: Middle East and Africa Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 56: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 57: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 58: Middle East and Africa Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 59: Middle East and Africa Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 60: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 61: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 62: Middle East and Africa Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 63: Middle East and Africa Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 68: South America Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 69: South America Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 70: South America Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 71: South America Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 72: South America Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 73: South America Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 74: South America Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 75: South America Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 76: South America Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 77: South America Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 78: South America Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 79: South America Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 80: South America Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 4: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 5: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Global Healthcare Data Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Healthcare Data Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 10: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 11: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 12: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 13: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United States Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Canada Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Mexico Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 24: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 25: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 26: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 27: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: France Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Spain Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 44: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 45: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 46: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 47: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 48: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 49: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: China Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: India Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Australia Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South Korea Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 64: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 65: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 66: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 67: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 68: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 70: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: GCC Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: South Africa Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 78: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 79: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 80: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 81: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 82: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 83: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 84: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: Brazil Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: Argentina Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Healthcare Data Industry?

The projected CAGR is approximately 13.36%.

2. Which companies are prominent players in the Healthcare Data Industry?

Key companies in the market include DELL EMC, Oracle (Cerner Corporation), Epic Systems Corporation, Optum Inc, General Electric Company (GE Healthcare), International Business Machines Corporation (IBM), ExlService Holdings Inc, Health Fidelity Inc, Allscripts Healthcare Solutions Inc, Flatiron Health, Apixio, SAS INSTITUTE INC, Innovaccer Inc.

3. What are the main segments of the Healthcare Data Industry?

The market segments include Component, Deployment, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Demand for Analytics Solutions for Population Health Management; Rise in Need for Business Intelligence to Optimize Health Administration and Strategy; Surge in Adoption of Big Data in the Healthcare Industry.

6. What are the notable trends driving market growth?

Cloud Segment is Expected to Register a High Growth Rate Over the Forecast Period.

7. Are there any restraints impacting market growth?

Security Concerns Related to Sensitive Patients Medical Data; High Cost of Implementation and Deployment.

8. Can you provide examples of recent developments in the market?

March 2022: Microsoft launched Azure Health Data Services in the United States. It is a platform as a service (PAAS) offering designed exclusively to support protected health information (PHI) in the cloud.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Healthcare Data Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Healthcare Data Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Healthcare Data Industry?

To stay informed about further developments, trends, and reports in the Healthcare Data Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence