Key Insights

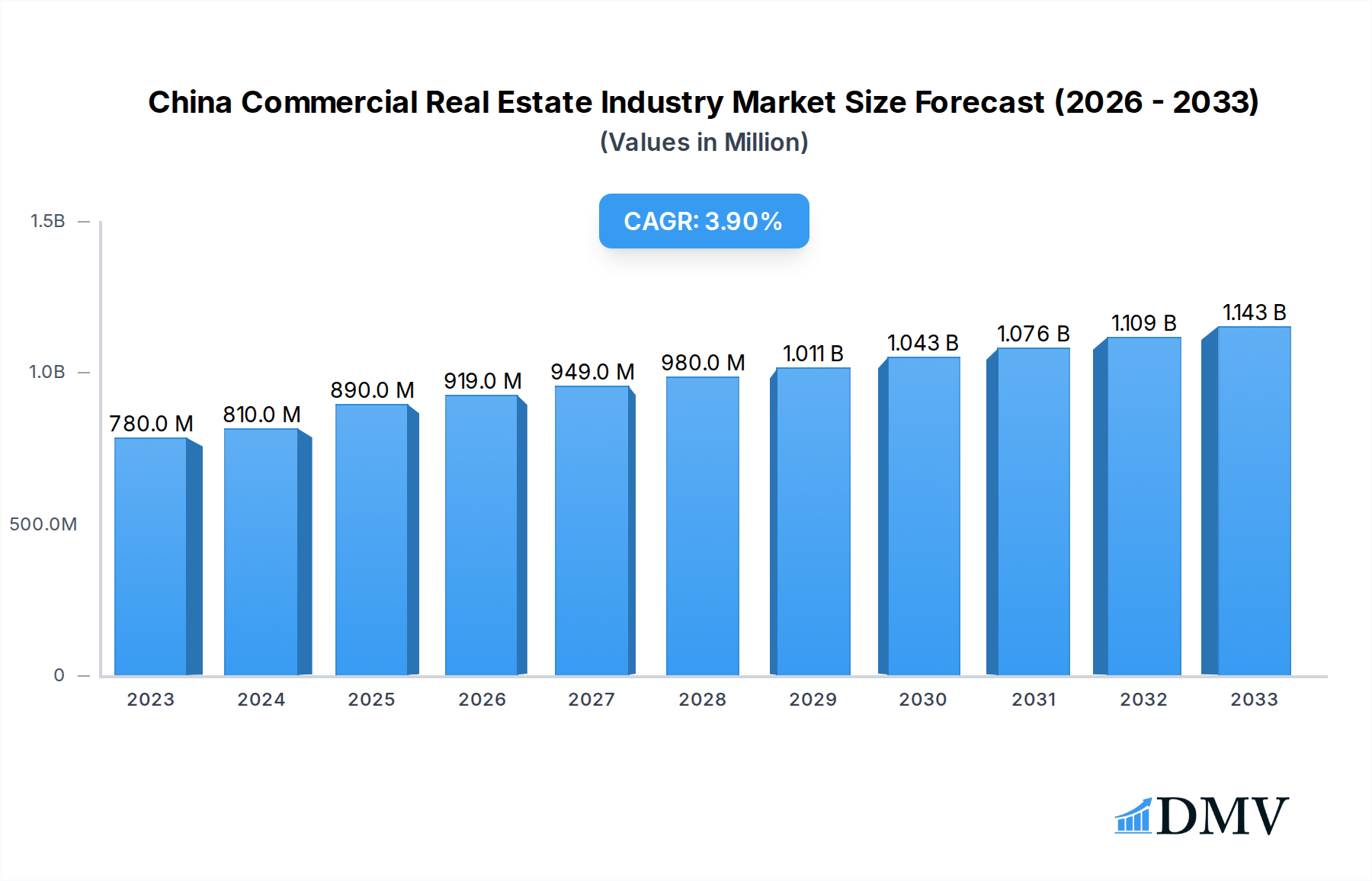

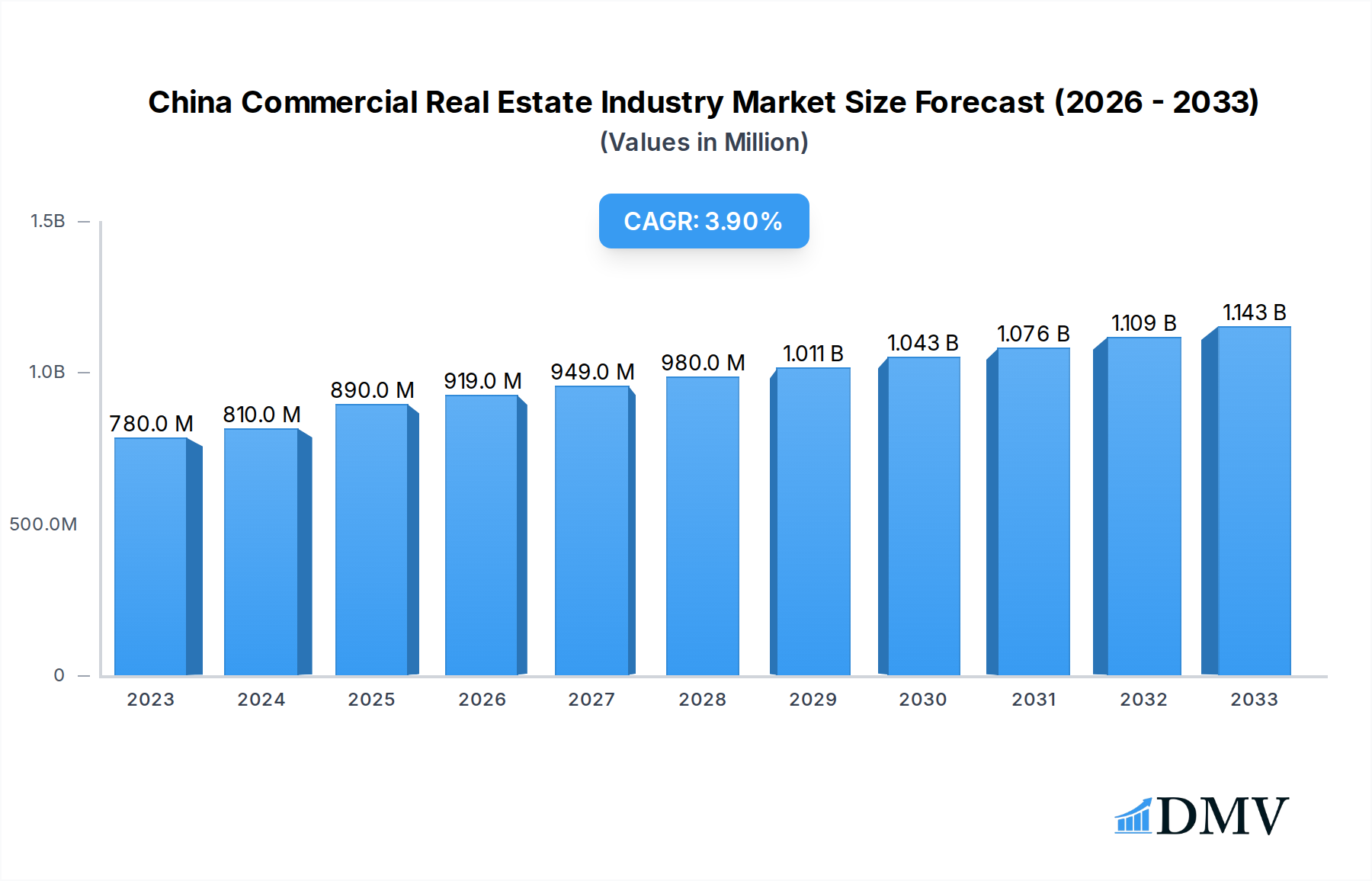

The China Commercial Real Estate Industry is poised for sustained growth, projected to reach USD 0.89 Million by 2025, with a compound annual growth rate (CAGR) of 3.49% expected from 2025 to 2033. This expansion is fueled by robust economic development and increasing urbanization across China, driving demand for modern commercial spaces. Key growth drivers include evolving consumer lifestyles and the burgeoning e-commerce sector, which necessitates sophisticated industrial and logistics facilities. The rapid digitalization of businesses also contributes significantly, increasing the need for advanced office spaces equipped with smart technologies. Furthermore, the recovery and expansion of the hospitality sector, especially in tourist destinations and major economic hubs, are expected to be a substantial contributor to market dynamics. The industry's resilience is further underscored by consistent investment from prominent developers like China Aoyuan Group Ltd, Longfor, and CapitaLand, indicating strong confidence in the sector's future.

China Commercial Real Estate Industry Market Size (In Million)

The market is segmented across critical sectors, with Office, Retail, Industrial (Logistics), and Hospitality properties forming the core of demand. The Industrial (Logistics) segment, in particular, is experiencing accelerated growth due to the persistent rise of online retail and the need for efficient supply chain management. While the overall outlook is positive, potential restraints such as evolving regulatory landscapes and the impact of global economic uncertainties on investment flows require careful navigation by market participants. However, the prevailing trends of digitalization, sustainability, and the demand for flexible workspace solutions are expected to shape the future development of China's commercial real estate, ensuring its continued relevance and growth in the coming years. Leading companies such as Wanda Group, China Resources Land Limited, and Sun Hung Kai Properties Limited are actively investing and innovating within these segments, reinforcing the industry's trajectory.

China Commercial Real Estate Industry Company Market Share

Gain unparalleled insights into the dynamic China Commercial Real Estate Industry with this in-depth report. Spanning the historical period of 2019–2024 and projecting to 2033, this study provides a data-driven roadmap for navigating the complexities and capitalizing on the immense opportunities within China's burgeoning property sector. Focused on the base year 2025 and an estimated year of 2025, this analysis offers actionable intelligence for investors, developers, and stakeholders seeking to understand market composition, industry evolution, leading regions, product innovations, growth drivers, obstacles, and strategic forecasts. This report is your definitive guide to the Chinese property market, including office space, retail properties, industrial logistics, and hospitality assets.

China Commercial Real Estate Industry Market Composition & Trends

The China Commercial Real Estate Industry exhibits a dynamic market composition characterized by evolving concentration levels and significant innovation catalysts. Regulatory landscapes are continuously adapting, influencing market entry and operations for both domestic and international players. Substitute products are emerging, particularly in the digital realm, impacting traditional asset classes like retail properties. End-user profiles are shifting, driven by urbanization and a growing middle class, demanding more sophisticated and sustainable commercial spaces. Mergers and acquisitions (M&A) activities are a key trend, reflecting a consolidation drive and strategic realignment among major entities. For instance, M&A deal values in the China commercial property market are expected to reach hundreds of billions of dollars annually within the forecast period. Key aspects of market composition include:

- Market Share Distribution: Analysis of market share held by leading developers and investors across key segments, including office buildings and industrial logistics.

- Innovation Catalysts: Identification of technological advancements and new business models driving market evolution.

- Regulatory Landscape: Overview of government policies impacting foreign investment, land use, and development.

- End-User Profiles: Detailed segmentation of demand from corporate tenants, retail brands, and institutional investors.

- M&A Activities: Insights into recent and projected merger and acquisition trends, including deal sizes and strategic rationales.

China Commercial Real Estate Industry Industry Evolution

The China Commercial Real Estate Industry is undergoing a profound evolution, shaped by robust market growth trajectories, rapid technological advancements, and significantly shifting consumer demands. Over the study period of 2019–2033, the sector is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 7-9%, fueled by sustained urbanization and economic development. Technological integration, particularly in smart building solutions and proptech, is revolutionizing property management and tenant experience. Adoption metrics for AI-driven property analytics and IoT-enabled building systems are projected to surge by over 50% by 2028. Consumer preferences are increasingly leaning towards flexible workspace solutions, experiential retail environments, and high-efficiency industrial logistics hubs. The Chinese property market is adapting to these changes by embracing sustainable development practices and offering diversified property types. Key aspects of this evolution include:

- Market Growth Trajectories: Detailed analysis of historical and projected growth rates across various commercial real estate segments.

- Technological Advancements: Examination of the impact of digitalization, AI, and IoT on property development, management, and utilization.

- Shifting Consumer Demands: Understanding evolving preferences for flexible office solutions, experiential retail, and e-commerce-driven logistics needs.

- Sustainable Development: The growing importance of ESG (Environmental, Social, and Governance) principles in property development and investment.

- Proptech Adoption: Trends in the adoption of property technology solutions by developers, investors, and end-users.

Leading Regions, Countries, or Segments in China Commercial Real Estate Industry

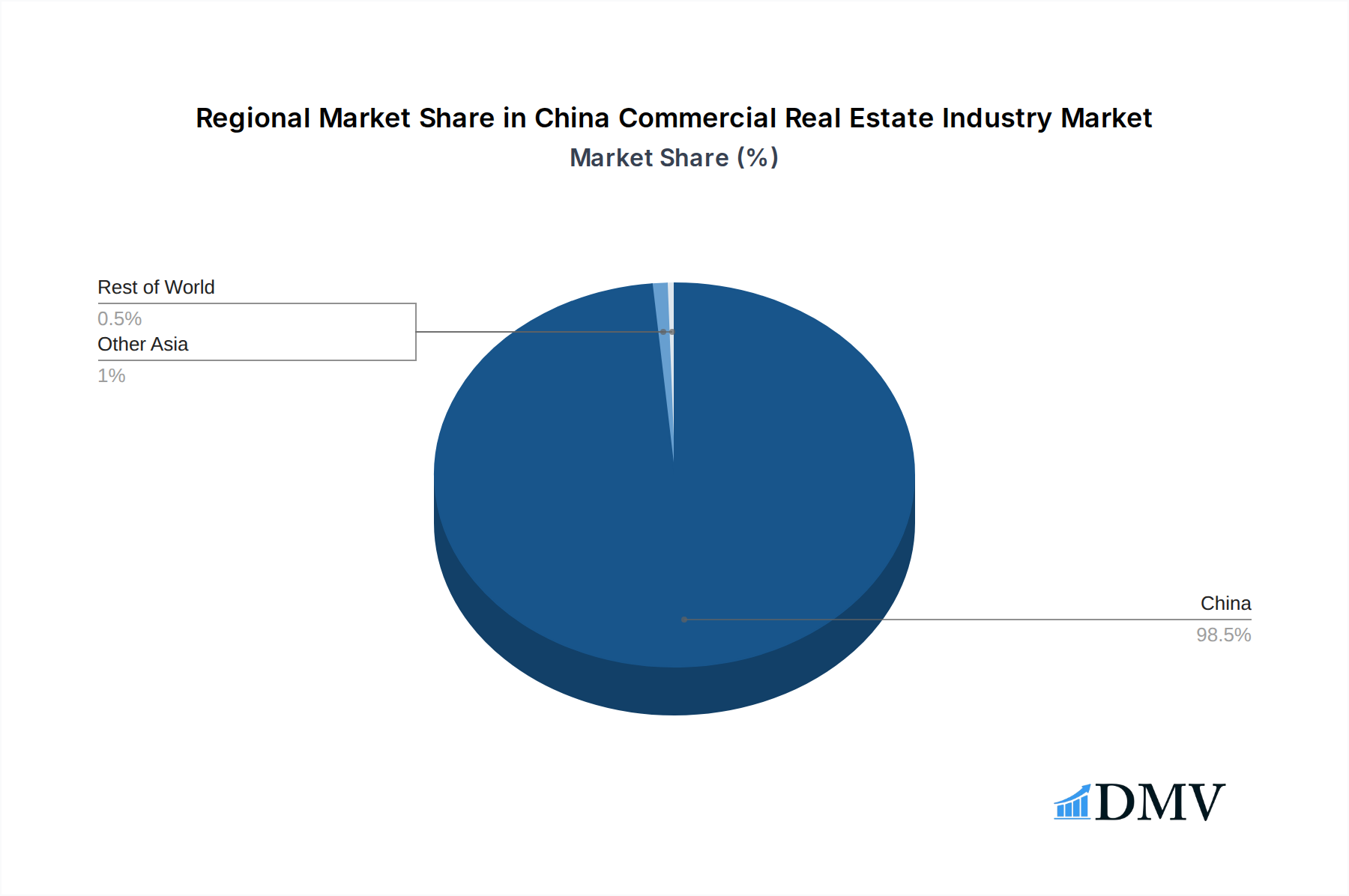

The China Commercial Real Estate Industry is currently dominated by key economic hubs and specific property types, reflecting concentrated investment and development activity. Among the segments, office properties and retail properties have historically commanded significant attention, driven by the expansion of multinational corporations and a burgeoning consumer market. However, the industrial logistics segment is experiencing exponential growth, propelled by the e-commerce boom and the critical need for efficient supply chains. Major drivers for this dominance include robust investment trends, significant regulatory support in designated economic zones, and favorable demographic shifts. For instance, tier-1 cities like Shanghai, Beijing, and Shenzhen continue to attract substantial foreign direct investment due to their established infrastructure and high concentration of businesses. The office market is characterized by increasing demand for premium, green-certified buildings, while the retail sector is adapting to omni-channel strategies, emphasizing experiential retail and mixed-use developments. The industrial logistics segment's rise is further amplified by government initiatives supporting advanced manufacturing and the 'dual circulation' economic strategy.

- Dominant Region: The Yangtze River Delta region, encompassing Shanghai, Jiangsu, and Zhejiang provinces, consistently leads in terms of investment volume and development activity due to its strong economic foundation and connectivity.

- Key Segment Dominance (Office): The office market in major metropolitan areas is driven by the demand for Grade A office spaces, fueled by financial services, technology, and professional services sectors. Investment trends show a preference for high-quality, well-located assets.

- Key Segment Dominance (Retail): The retail sector is undergoing a transformation, with a shift towards experiential retail and mixed-use developments that integrate entertainment, dining, and shopping. Investment is increasingly focused on prime locations and well-managed shopping centers.

- Key Segment Dominance (Industrial Logistics): The industrial logistics segment is experiencing unprecedented growth, driven by the booming e-commerce sector and the need for modern warehousing and distribution facilities. Government support for the manufacturing sector also contributes significantly.

- Key Segment Dominance (Hospitality): The hospitality sector is recovering and adapting to new travel patterns, with increasing demand for business hotels in economic centers and luxury resorts in tourist destinations.

China Commercial Real Estate Industry Product Innovations

Product innovations within the China Commercial Real Estate Industry are largely focused on enhancing sustainability, efficiency, and tenant experience. Developers are increasingly incorporating smart building technologies, such as advanced energy management systems and integrated IoT platforms, to optimize operational costs and reduce environmental impact. For office spaces, the trend is towards flexible and adaptable layouts that cater to evolving work styles, including hot-desking and co-working solutions. In the retail sector, innovations include the integration of augmented reality (AR) for in-store experiences and data analytics to personalize customer journeys. Industrial logistics facilities are seeing advancements in automation, robotics, and temperature-controlled warehousing to meet the demands of rapid e-commerce fulfillment. These innovations aim to create future-ready assets that attract premium tenants and investors.

Propelling Factors for China Commercial Real Estate Industry Growth

The China Commercial Real Estate Industry is propelled by a confluence of powerful factors. Sustained economic growth and ongoing urbanization continue to drive demand for commercial spaces across all segments. Government policies, such as tax incentives for investment in specific sectors and the development of Greater Bay Area, are creating favorable conditions. Technological advancements in construction, property management, and smart building solutions are improving efficiency and creating new value propositions. Furthermore, the increasing affluence of the Chinese population fuels demand for high-quality retail and hospitality experiences, while the booming e-commerce sector directly stimulates growth in industrial logistics. The consistent influx of foreign direct investment also plays a crucial role in the sector's expansion.

Obstacles in the China Commercial Real Estate Industry Market

Despite its growth potential, the China Commercial Real Estate Industry faces several obstacles. Regulatory uncertainties and evolving government policies can create challenges for investors and developers. The potential for economic slowdowns and shifts in global trade dynamics can impact demand and investment sentiment. Intense competition among developers for prime land and tenants can lead to price pressures and affect profitability. Supply chain disruptions, particularly in the construction materials sector, can cause project delays and cost overruns. Furthermore, evolving consumer preferences and the rise of e-commerce pose a challenge for traditional retail properties, requiring significant adaptation.

Future Opportunities in China Commercial Real Estate Industry

Emerging opportunities in the China Commercial Real Estate Industry are diverse and promising. The continued expansion of the e-commerce and logistics sectors presents substantial growth potential for industrial logistics facilities, including cold chain and last-mile delivery hubs. The increasing demand for green and sustainable buildings opens avenues for ESG-focused developments and retrofits. The growth of the digital economy and remote work is creating demand for flexible office solutions and smart-building technologies. Furthermore, the development of emerging cities and regions outside of the traditional tier-1 hubs offers untapped market potential. Investments in healthcare-related real estate and data centers are also projected to rise.

Major Players in the China Commercial Real Estate Industry Ecosystem

- China Aoyuan Group Ltd

- Longfor

- CapitaLand

- Wanda Group

- China Resources Land Limited

- Sun Hung Kai Properties Limited

- Henderson Land Development Company Limited

- Greenland Business Group

- Wharf Real Estate Investment Company Limited

- Prologis

- Seazen Holdings Co Ltd

- Powerlong Real Estate Holdings Limited

Key Developments in China Commercial Real Estate Industry Industry

- May 2023: The Beijing Suning Life Plaza mixed-use complex was purchased for approximately USD 400 Million by CapitaLand Investment Private Fund, with assistance from Cushman & Wakefield's Greater China Capital Markets division, indicating significant investor confidence in prime mixed-use assets.

- April 2023: AIA invested US$1.3 Billion into a Shanghai office-retail complex, and Ping An paid approximately US$7 Billion for industrial and office assets in Shanghai and Beijing. This demonstrates substantial investment from insurers, highlighting their continued belief in mainland China properties as a valuable asset class despite market downturns.

Strategic China Commercial Real Estate Industry Market Forecast

The China Commercial Real Estate Industry is poised for continued strategic growth, driven by ongoing economic development, rapid urbanization, and an increasing focus on sustainability and technology integration. Key growth catalysts include the sustained demand for modern office spaces and experiential retail properties, coupled with the exponential rise of industrial logistics fueled by e-commerce. Government support for innovation and strategic urban development will further bolster market expansion. Opportunities in green building technologies and flexible workspace solutions will shape the future landscape, attracting both domestic and international investment. The market is expected to demonstrate resilience and capitalize on evolving consumer and business needs throughout the forecast period.

China Commercial Real Estate Industry Segmentation

-

1. Type

- 1.1. Office

- 1.2. Retail

- 1.3. Industrial (Logistics)

- 1.4. Hospitality

China Commercial Real Estate Industry Segmentation By Geography

- 1. China

China Commercial Real Estate Industry Regional Market Share

Geographic Coverage of China Commercial Real Estate Industry

China Commercial Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Office

- 5.1.2. Retail

- 5.1.3. Industrial (Logistics)

- 5.1.4. Hospitality

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Commercial Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Office

- 6.1.2. Retail

- 6.1.3. Industrial (Logistics)

- 6.1.4. Hospitality

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Aoyuan Group Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Longfor

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 CapitaLand

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Wanda Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 China Resources Land Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Sun Hung Kai Properties Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Henderson Land Development Company Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Greenland Business Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Wharf Real Estate Investment Company Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Prologis**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Seazen Holdings Co Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Powerlong Real Estate Holdings Limited

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 China Aoyuan Group Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Commercial Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Commercial Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: China Commercial Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: China Commercial Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: China Commercial Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: China Commercial Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Commercial Real Estate Industry?

The projected CAGR is approximately 3.49%.

2. Which companies are prominent players in the China Commercial Real Estate Industry?

Key companies in the market include China Aoyuan Group Ltd, Longfor, CapitaLand, Wanda Group, China Resources Land Limited, Sun Hung Kai Properties Limited, Henderson Land Development Company Limited, Greenland Business Group, Wharf Real Estate Investment Company Limited, Prologis**List Not Exhaustive, Seazen Holdings Co Ltd, Powerlong Real Estate Holdings Limited.

3. What are the main segments of the China Commercial Real Estate Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.89 Million as of 2022.

5. What are some drivers contributing to market growth?

Foreign Investments driving the market; Implementation of government policies driving the market.

6. What are the notable trends driving market growth?

Technology and Innovation Driving the Market.

7. Are there any restraints impacting market growth?

Oversupply of commercial real estate; Increasing property prices affecting the growth of the market.

8. Can you provide examples of recent developments in the market?

May 2023: The Beijing Suning Life Plaza mixed-use complex was recently purchased from Suning for about USD 400 million by CapitaLand Investment Private Fund with the help of Cushman & Wakefield's Greater China Capital Markets division.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Commercial Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Commercial Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Commercial Real Estate Industry?

To stay informed about further developments, trends, and reports in the China Commercial Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence