Key Insights

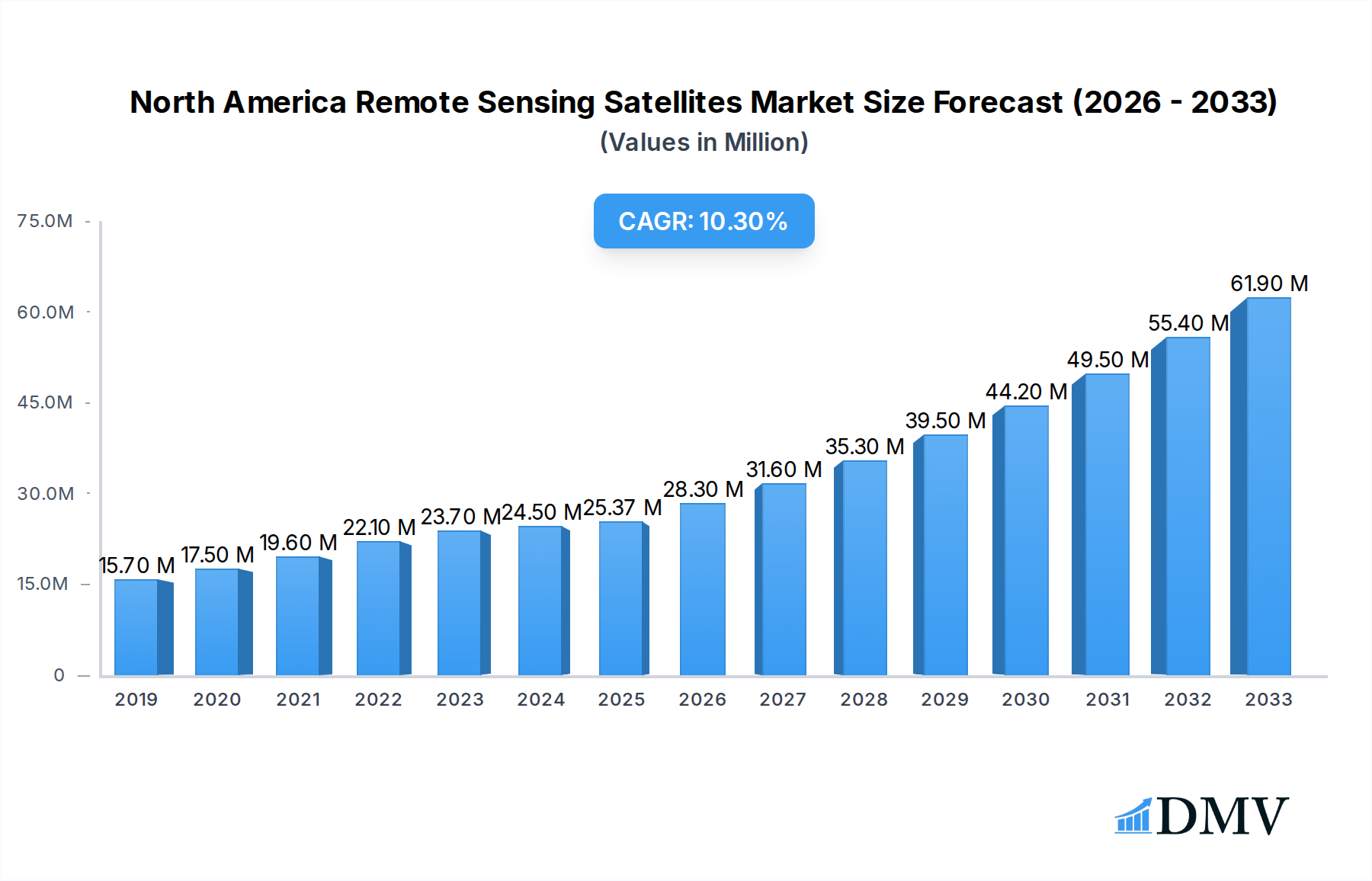

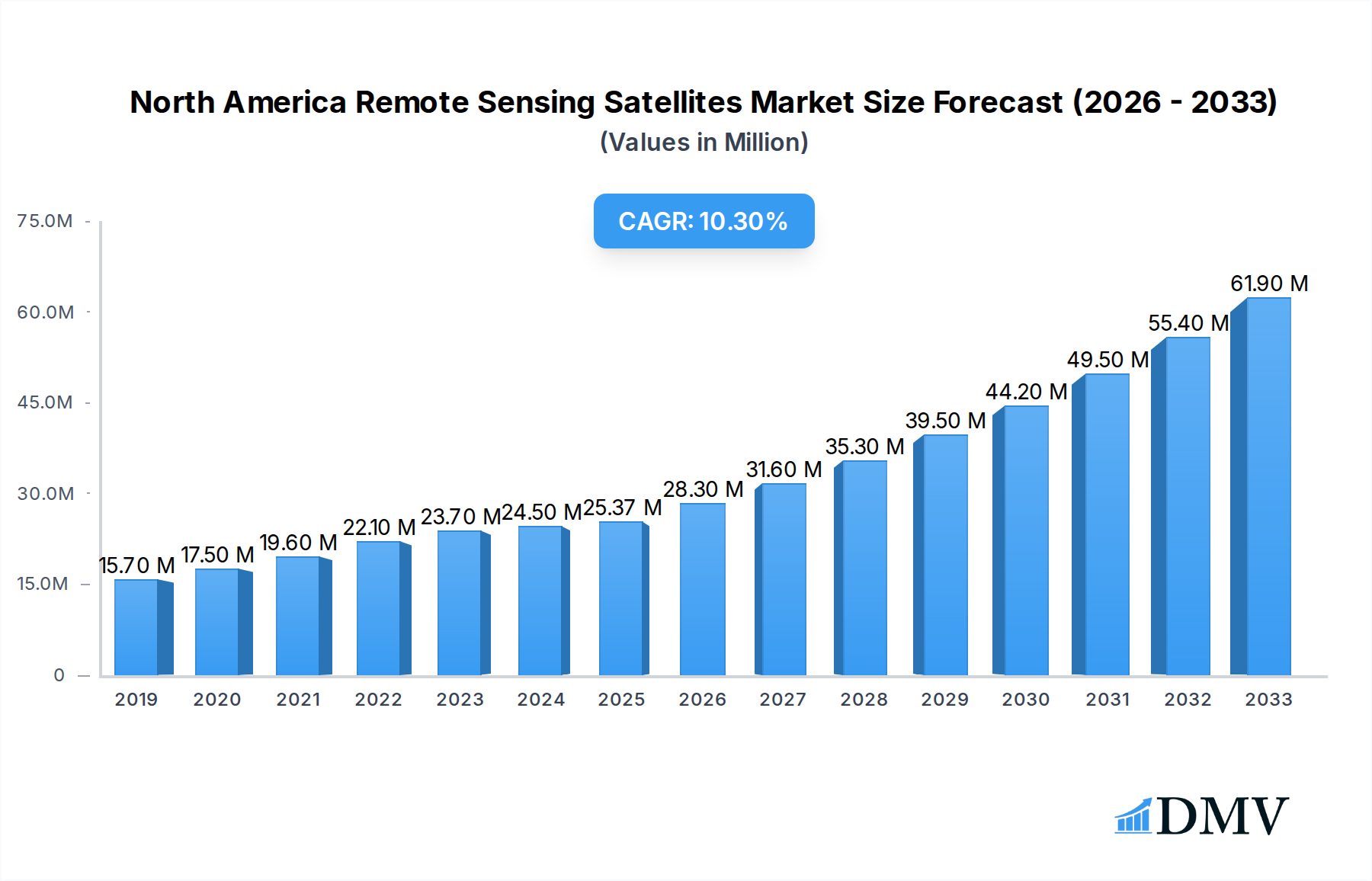

The North America Remote Sensing Satellites Market is poised for significant expansion, projected to reach USD 25.37 billion in 2025 and experience a robust CAGR of 11.59% throughout the forecast period of 2019-2033. This growth is fueled by escalating demand for high-resolution Earth observation data across diverse sectors, particularly in commercial and military applications. Key drivers include the increasing adoption of small satellites for specialized missions, advancements in sensor technology, and the growing need for accurate geospatial intelligence for environmental monitoring, disaster management, urban planning, and national security. The market is segmented across various satellite mass categories, with a notable trend towards smaller, more agile satellite constellations. Propulsion hardware and propellant, along with satellite bus and subsystems, represent critical segments within the overall market due to their essential role in satellite functionality and maneuverability. The sustained investment in space programs by governments and the private sector in North America, coupled with a growing ecosystem of innovative companies, further underpins this positive market outlook.

North America Remote Sensing Satellites Market Market Size (In Million)

The competitive landscape is characterized by the presence of both established aerospace giants and agile new entrants, all vying for market share through technological innovation and strategic collaborations. Companies like Lockheed Martin Corporation, Northrop Grumman Corporation, Maxar Technologies Inc., and Ball Corporation are instrumental in developing sophisticated remote sensing platforms, while newer players such as GomSpace ApS and Spire Global Inc. are driving advancements in the small satellite domain. The market's growth trajectory is also influenced by the increasing deployment of satellites in Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) for applications requiring lower latency and higher revisit rates, such as precision agriculture and real-time imaging. Despite the promising growth, potential restraints could arise from the high initial investment costs associated with satellite development and launch, as well as evolving regulatory frameworks governing space activities. However, the overarching trend of data-driven decision-making and the expanding use cases for remote sensing data strongly suggest a continued upward trajectory for the North America Remote Sensing Satellites Market.

North America Remote Sensing Satellites Market Company Market Share

This in-depth report provides a definitive analysis of the North America Remote Sensing Satellites Market, offering critical insights into its current landscape, historical evolution, and projected trajectory. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this study is essential for stakeholders seeking to capitalize on the burgeoning opportunities within this dynamic sector. We delve into market composition, industry evolution, leading segments, product innovations, growth drivers, obstacles, and future opportunities, complemented by an extensive overview of major players and key industry developments. The North America Remote Sensing Satellites Market is projected to reach XX billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period.

North America Remote Sensing Satellites Market Composition & Trends

The North America Remote Sensing Satellites Market is characterized by a dynamic interplay of innovation and consolidation. Market concentration is moderate, with several key players vying for market share. Innovation is primarily driven by advancements in sensor technology, miniaturization of satellite components, and sophisticated data processing algorithms. The regulatory landscape, while supportive of space exploration and commercialization, presents evolving challenges and opportunities, particularly concerning spectrum allocation and data privacy. Substitute products, such as high-altitude aerial platforms and ground-based sensing, exist but are largely outpaced by the scalability and persistent coverage offered by satellite-based solutions. End-user profiles range from the highly specialized military and government sectors to the rapidly expanding commercial applications in agriculture, environmental monitoring, urban planning, and disaster management. Mergers and acquisitions (M&A) activity has been significant, with deal values reaching into the billions, indicating a trend towards consolidation and strategic partnerships to enhance capabilities and market reach. For instance, the XX billion acquisition of [Company Name] by [Acquiring Company Name] in 2023 significantly reshaped the market landscape.

- Market Share Distribution: Leading companies collectively hold an estimated XX% of the market share.

- M&A Deal Values: The aggregate value of M&A deals in the historical period (2019-2024) is estimated at XX billion.

- Innovation Catalysts: Increased investment in AI for data analysis and enhanced resolution capabilities are key drivers.

- Regulatory Impact: Evolving policies on commercial satellite data utilization are shaping market access and deployment.

North America Remote Sensing Satellites Market Industry Evolution

The North America Remote Sensing Satellites Market has witnessed a transformative evolution driven by rapid technological advancements and an increasing demand for geospatial data. Historically, the industry was dominated by large government-funded programs focused on scientific research and national security. However, the past decade has seen a significant shift towards commercialization, fueled by the miniaturization of satellite technology, the rise of small satellite constellations, and the development of more cost-effective launch services. This evolution has democratized access to space-based data, enabling a wider array of applications across diverse industries. The market growth trajectory has been consistently upward, with an estimated XX% CAGR observed in the historical period (2019-2024). Technological advancements, such as the development of Synthetic Aperture Radar (SAR) with sub-meter resolution and advanced optical sensors capable of hyperspectral imaging, have significantly enhanced data quality and analytical capabilities. Shifting consumer demands have moved from basic imagery to actionable intelligence, necessitating sophisticated data processing, analytics, and cloud-based platforms. The adoption of Earth Observation (EO) data has surged in sectors like precision agriculture, where it aids in crop health monitoring and yield prediction, and in urban planning, where it supports infrastructure development and traffic management. The emergence of private companies launching their own constellations has accelerated this growth, offering more frequent revisits and higher spatial resolutions than previously available. Furthermore, the increasing focus on climate change monitoring, disaster response, and sustainable resource management has further bolstered the demand for remote sensing capabilities. This industry evolution is a testament to the synergistic relationship between technological innovation, market demand, and supportive governmental policies, paving the way for an even more expansive future.

Leading Regions, Countries, or Segments in North America Remote Sensing Satellites Market

Within the North America Remote Sensing Satellites Market, the United States stands out as the dominant country, driven by its robust aerospace industry, significant government investment in space programs, and a thriving commercial sector. The LEO (Low Earth Orbit) class is the leading orbit class, primarily due to the cost-effectiveness and frequent revisit times offered by LEO constellations, crucial for applications requiring up-to-date data. Among the satellite mass segments, 100-500kg satellites represent a significant portion of the market, offering a balance between payload capacity and launch costs, enabling the deployment of sophisticated sensor packages. For satellite subsystems, Satellite Bus & Subsystems are critical, forming the backbone of satellite operations and enabling the integration of various payloads. In terms of end-users, the Commercial segment is experiencing the most rapid expansion, driven by its diverse applications in agriculture, finance, insurance, and logistics.

Dominant Country: United States

- Key Drivers: Extensive R&D funding, presence of major satellite manufacturers and launch providers, strong demand from commercial sectors like agriculture and infrastructure.

- Investment Trends: Significant private investment in satellite constellation development, exceeding XX billion annually.

- Regulatory Support: Favorable policies promoting commercial space activities and data commercialization.

Leading Orbit Class: LEO

- Key Drivers: Reduced launch costs, shorter orbital periods leading to more frequent data acquisition, suitability for Earth observation and communication constellations.

- Adoption Metrics: Over XX% of new satellite launches are destined for LEO.

- Technological Advancements: Miniaturization of components enabling mass deployment of LEO satellites.

Prominent Satellite Mass Segment: 100-500kg

- Key Drivers: Optimal balance of payload capacity, power, and cost-effectiveness for advanced sensors.

- Market Penetration: Constitutes approximately XX% of the current satellite fleet.

- Application Versatility: Supports a wide range of scientific and commercial payloads, including high-resolution optical and SAR sensors.

Critical Satellite Subsystem: Satellite Bus & Subsystems

- Key Drivers: Essential for satellite functionality, providing power, thermal control, attitude determination, and communications.

- Innovation Focus: Development of modular and highly reliable bus architectures to reduce development time and cost.

- Market Impact: The continuous demand for these subsystems underpins the entire satellite manufacturing industry.

Fastest Growing End User: Commercial

- Key Drivers: Growing adoption of geospatial data for business intelligence, risk management, and operational efficiency.

- Application Examples: Precision agriculture, environmental monitoring, disaster response, urban planning, resource exploration.

- Market Potential: Estimated to account for XX% of the market revenue by 2033.

North America Remote Sensing Satellites Market Product Innovations

Product innovations in the North America Remote Sensing Satellites Market are characterized by enhanced resolution, multi-spectral capabilities, and advanced data processing. Companies are developing next-generation SAR satellites capable of all-weather, day-or-night imaging with sub-meter resolution, such as those deployed by Capella Space. Innovations also include miniaturized optical sensors with hyperspectral imaging to discern material composition from orbit. Furthermore, the integration of onboard AI for real-time data analysis and the development of highly agile satellites for targeted observation are transforming the market. These advancements are not only improving data accuracy but also expanding the scope of applications in fields like infrastructure monitoring, agriculture, and defense, offering unique selling propositions through unprecedented levels of detail and actionable insights.

Propelling Factors for North America Remote Sensing Satellites Market Growth

The North America Remote Sensing Satellites Market is propelled by a confluence of powerful factors. Technological advancements, including the development of smaller, more powerful sensors and cost-effective launch vehicles like those from Rocket Lab, are significantly lowering the barrier to entry. Economic drivers include the increasing demand for geospatial data from commercial sectors for applications such as precision agriculture, financial risk assessment, and urban planning, translating into a market value projected to exceed XX billion. Regulatory support from government agencies like NASA, through initiatives like granting wider access to geospatial content, fosters innovation and market growth. The growing awareness and urgent need for climate change monitoring, disaster management, and resource exploration further amplify the demand for remote sensing capabilities.

Obstacles in the North America Remote Sensing Satellites Market Market

Despite its robust growth, the North America Remote Sensing Satellites Market faces several obstacles. Regulatory challenges, particularly concerning spectrum allocation for new satellite constellations and data export restrictions, can impede market expansion. The initial high cost of satellite development and launch, although decreasing, remains a significant investment hurdle for smaller entities. Supply chain disruptions, exacerbated by geopolitical events and the reliance on specialized components, can lead to project delays and increased costs. Intense competitive pressures from established players and emerging startups also necessitate continuous innovation and cost optimization to maintain market share. Quantifiable impacts include potential delays in satellite deployment, estimated at XX months, and increased operational costs of up to XX% due to component shortages.

Future Opportunities in North America Remote Sensing Satellites Market

Emerging opportunities in the North America Remote Sensing Satellites Market are abundant, driven by new technological frontiers and evolving market needs. The expansion of the Internet of Things (IoT) and the demand for real-time, ubiquitous data streams present a significant opportunity for satellite-based IoT connectivity. Advances in AI and machine learning are enabling more sophisticated data analytics, leading to new applications in predictive modeling for climate change, urban resilience, and resource management. The growing focus on sustainable development and ESG (Environmental, Social, and Governance) initiatives will drive demand for satellite data to monitor environmental impact, supply chains, and social indicators. Furthermore, the increasing privatization of space exploration and the potential for in-orbit servicing and manufacturing open up novel avenues for market expansion and revenue generation.

Major Players in the North America Remote Sensing Satellites Market Ecosystem

- ImageSat International

- GomSpace ApS

- LeoStella

- Esri

- Lockheed Martin Corporation

- Ball Corporation

- Maxar Technologies Inc

- IHI Corp

- Thales

- Planet Labs Inc

- Northrop Grumman Corporation

- Spire Global Inc

- Capella Space Corp

Key Developments in North America Remote Sensing Satellites Market Industry

- April 2023: NASA awarded a sole source Blanket Purchase Agreement (BPA) to Capella Space Corporation of San Francisco to provide high-resolution Synthetic Aperture Radar (SAR) (0.5 meter to 1.2 meters) commercial Earth observation data products, significantly boosting Capella's market presence and data accessibility.

- March 2023: Rocket Lab's Electron rocket successfully launched Capella Space's pair of commercial radar imaging satellites into orbit. These satellites are capable of seeing through clouds, in daylight or darkness, to monitor the planet below, enhancing global surveillance and disaster monitoring capabilities.

- February 2023: NASA and geographic information service provider Esri will grant wider access to the space agency's geospatial content for research and exploration purposes through the Space Act Agreement, fostering greater collaboration and innovation in Earth science and planetary exploration.

Strategic North America Remote Sensing Satellites Market Market Forecast

The North America Remote Sensing Satellites Market is poised for substantial growth, driven by an intensified demand for precise, real-time geospatial intelligence across commercial and government sectors. Strategic investments in advanced sensor technology, particularly in SAR and hyperspectral imaging, will continue to fuel product innovation, leading to higher resolution data and expanded application potential. The ongoing trend of small satellite constellation deployment, made more accessible by advancements in launch services and miniaturization, will democratize access to space-based data, fostering new market entrants and innovative business models. Furthermore, the increasing integration of artificial intelligence for data analysis and interpretation will unlock deeper insights, transforming raw satellite imagery into actionable intelligence for critical decision-making in areas such as climate monitoring, disaster response, and resource management, projecting a future market value in the billions.

North America Remote Sensing Satellites Market Segmentation

-

1. Satellite Mass

- 1.1. 10-100kg

- 1.2. 100-500kg

- 1.3. 500-1000kg

- 1.4. Below 10 Kg

- 1.5. above 1000kg

-

2. Orbit Class

- 2.1. GEO

- 2.2. LEO

- 2.3. MEO

-

3. Satellite Subsystem

- 3.1. Propulsion Hardware and Propellant

- 3.2. Satellite Bus & Subsystems

- 3.3. Solar Array & Power Hardware

- 3.4. Structures, Harness & Mechanisms

-

4. End User

- 4.1. Commercial

- 4.2. Military & Government

- 4.3. Other

North America Remote Sensing Satellites Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

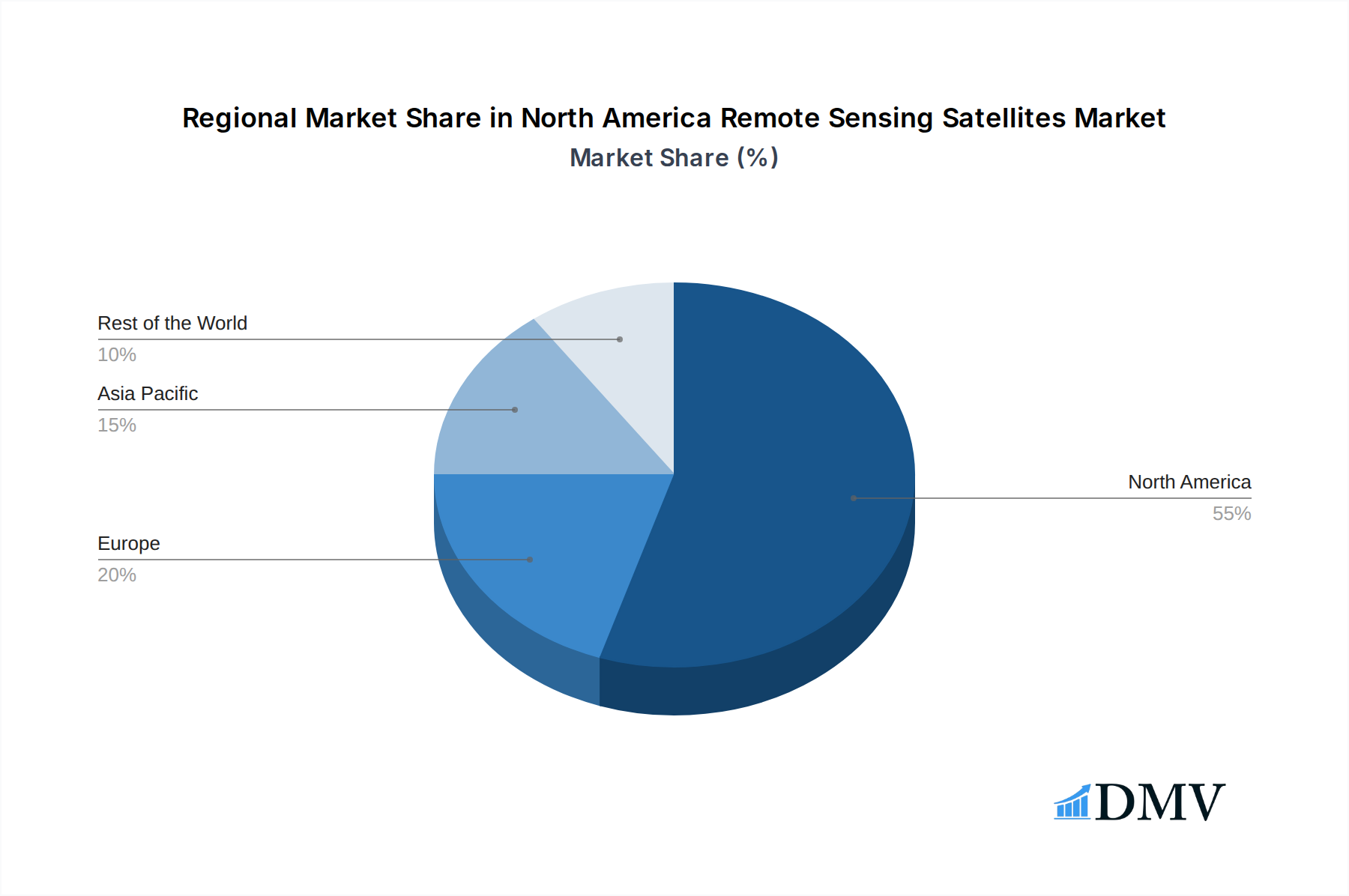

North America Remote Sensing Satellites Market Regional Market Share

Geographic Coverage of North America Remote Sensing Satellites Market

North America Remote Sensing Satellites Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.59% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 5.1.1. 10-100kg

- 5.1.2. 100-500kg

- 5.1.3. 500-1000kg

- 5.1.4. Below 10 Kg

- 5.1.5. above 1000kg

- 5.2. Market Analysis, Insights and Forecast - by Orbit Class

- 5.2.1. GEO

- 5.2.2. LEO

- 5.2.3. MEO

- 5.3. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 5.3.1. Propulsion Hardware and Propellant

- 5.3.2. Satellite Bus & Subsystems

- 5.3.3. Solar Array & Power Hardware

- 5.3.4. Structures, Harness & Mechanisms

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Commercial

- 5.4.2. Military & Government

- 5.4.3. Other

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 6. North America Remote Sensing Satellites Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 6.1.1. 10-100kg

- 6.1.2. 100-500kg

- 6.1.3. 500-1000kg

- 6.1.4. Below 10 Kg

- 6.1.5. above 1000kg

- 6.2. Market Analysis, Insights and Forecast - by Orbit Class

- 6.2.1. GEO

- 6.2.2. LEO

- 6.2.3. MEO

- 6.3. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 6.3.1. Propulsion Hardware and Propellant

- 6.3.2. Satellite Bus & Subsystems

- 6.3.3. Solar Array & Power Hardware

- 6.3.4. Structures, Harness & Mechanisms

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Commercial

- 6.4.2. Military & Government

- 6.4.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ImageSat International

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 GomSpaceApS

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 LeoStella

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Esri

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lockheed Martin Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ball Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Maxar Technologies Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 IHI Corp

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Thale

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Planet Labs Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Northrop Grumman Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Spire Global Inc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Capella Space Corp

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 ImageSat International

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Remote Sensing Satellites Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Remote Sensing Satellites Market Share (%) by Company 2025

List of Tables

- Table 1: North America Remote Sensing Satellites Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 2: North America Remote Sensing Satellites Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 3: North America Remote Sensing Satellites Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 4: North America Remote Sensing Satellites Market Revenue billion Forecast, by End User 2020 & 2033

- Table 5: North America Remote Sensing Satellites Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Remote Sensing Satellites Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 7: North America Remote Sensing Satellites Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 8: North America Remote Sensing Satellites Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 9: North America Remote Sensing Satellites Market Revenue billion Forecast, by End User 2020 & 2033

- Table 10: North America Remote Sensing Satellites Market Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States North America Remote Sensing Satellites Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada North America Remote Sensing Satellites Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico North America Remote Sensing Satellites Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Remote Sensing Satellites Market?

The projected CAGR is approximately 11.59%.

2. Which companies are prominent players in the North America Remote Sensing Satellites Market?

Key companies in the market include ImageSat International, GomSpaceApS, LeoStella, Esri, Lockheed Martin Corporation, Ball Corporation, Maxar Technologies Inc, IHI Corp, Thale, Planet Labs Inc, Northrop Grumman Corporation, Spire Global Inc, Capella Space Corp.

3. What are the main segments of the North America Remote Sensing Satellites Market?

The market segments include Satellite Mass, Orbit Class, Satellite Subsystem, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.37 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

April 2023: NASA has awarded a sole source Blanket Purchase Agreement (BPA) to Capella Space Corporation of San Francisco to provide high-resolution Synthetic Aperture Radar (SAR) (0.5 meter to 1.2 meters) commercial Earth observation data products.March 2023: Rocket Lab's Electron rocket launched CapellaSpace's pair of commercial radar imaging satellites into orbit that are capable of seeing through clouds, in daylight or darkness, to monitor the planet below.February 2023: NASA and geographic information service provider Esri will grant wider access to the space agency's geospatial content for research and exploration purposes through the Space Act Agreement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Remote Sensing Satellites Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Remote Sensing Satellites Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Remote Sensing Satellites Market?

To stay informed about further developments, trends, and reports in the North America Remote Sensing Satellites Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence