Key Insights

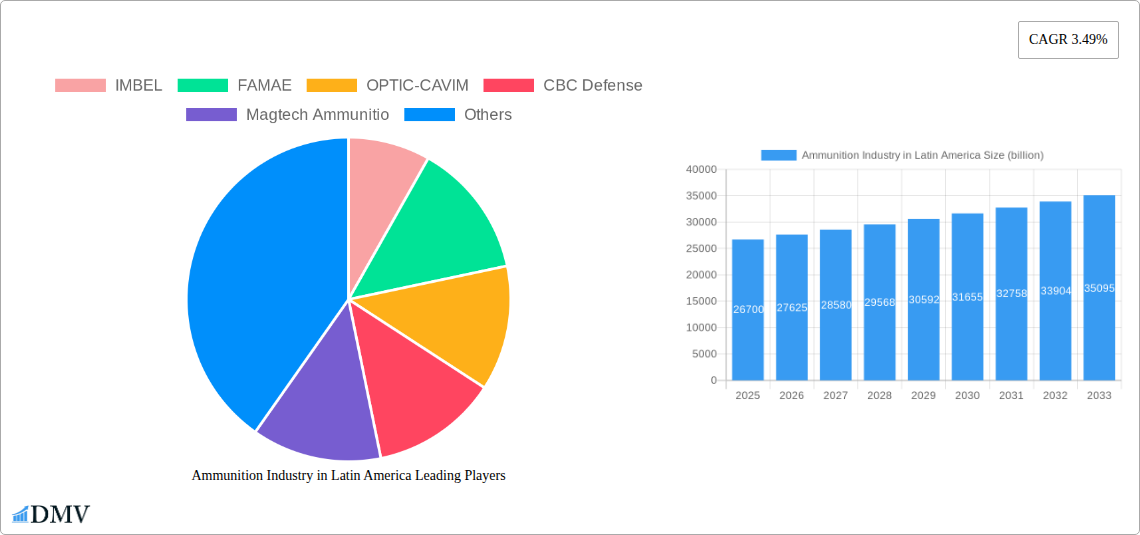

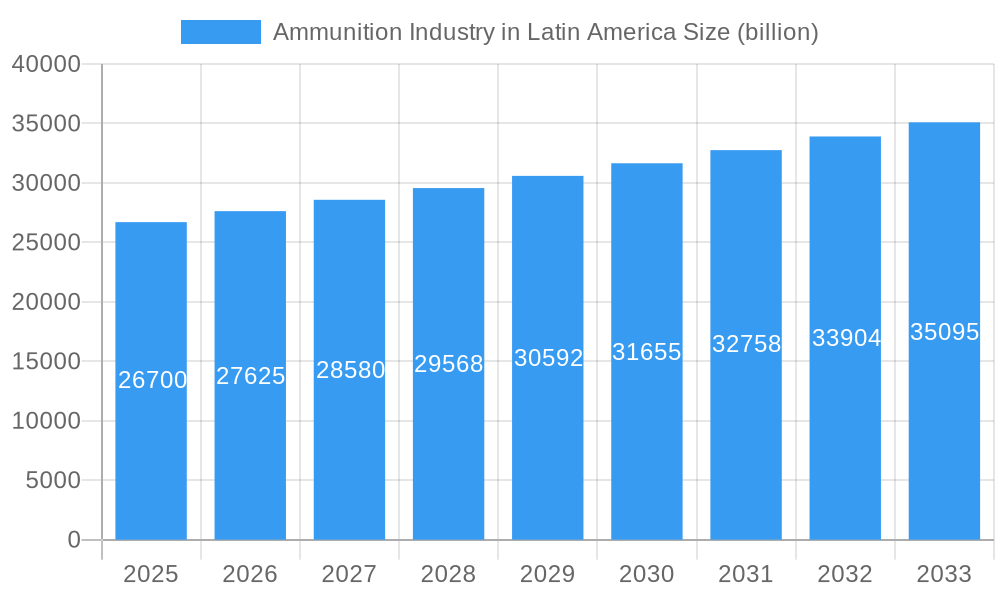

The Latin American ammunition market is poised for steady growth, projecting a market size of $26.7 billion by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 3.49% through 2033. This expansion is primarily fueled by increasing defense budgets across several key nations in the region, driven by a need for enhanced border security and counter-terrorism operations. Furthermore, a growing civilian firearms ownership for sport shooting and self-defense also contributes significantly to market demand. Investments in modernizing military inventories and the procurement of advanced ammunition types, including medium and large caliber rounds, are expected to be key drivers. The presence of established domestic manufacturers and a growing interest in domestic production capabilities further bolster the market's potential.

Ammunition Industry in Latin America Market Size (In Billion)

Despite the positive outlook, the market faces certain restraints. Fluctuations in economic stability within some Latin American countries can impact government defense spending and civilian purchasing power. Additionally, stringent import regulations and the high cost associated with advanced ammunition development and production present challenges. Nevertheless, the increasing demand for specialized ammunition for law enforcement and the sustained growth in small-caliber ammunition for civilian use are expected to offset these limitations. The market is segmented by ammunition type, with small caliber ammunition holding a dominant share, followed by medium, large, and mortar and artillery ammunition. Key end-users include both military and civilian sectors, with the military segment typically exhibiting higher volume procurement.

Ammunition Industry in Latin America Company Market Share

Ammunition Industry in Latin America Market Composition & Trends

The Latin American ammunition market is characterized by a dynamic interplay of factors shaping its composition and future trajectory. Market concentration varies across sub-regions, with established players like CBC Defense and Magtech Ammunition holding significant sway in Brazil and other key economies. Innovation catalysts are primarily driven by evolving defense needs, increasing civilian demand for self-defense, and advancements in manufacturing technologies. The regulatory landscape, while stringent in many nations, presents a complex patchwork of controls and licensing requirements that influence market access and product development. Substitute products, though limited in the core ammunition segment, can emerge in the form of less lethal alternatives or advanced training simulations, particularly impacting the civilian and law enforcement sectors. End-user profiles span the spectrum from civilian sport shooters and personal defense users to sophisticated military and industrial applications, each with distinct purchasing patterns and technical requirements. Merger and acquisition (M&A) activities, while not as prevalent as in more mature markets, are present, driven by consolidation strategies and the pursuit of market share. Recent M&A deals in the region have been valued in the hundreds of millions of dollars, signaling strategic consolidation. The market share distribution for the historical period (2019-2024) shows a projected revenue of over 1.5 billion USD, with leading companies capturing approximately 30-40% of the market collectively.

Ammunition Industry in Latin America Industry Evolution

The ammunition industry in Latin America has undergone significant evolution, marked by consistent market growth trajectories, critical technological advancements, and a palpable shift in consumer demands. Over the study period of 2019–2033, the industry is projected to witness a compound annual growth rate (CAGR) of approximately 5.5%, with the base and estimated year of 2025 alone projecting a market value of over 2.1 billion USD. This growth is underpinned by increasing defense spending across several Latin American nations, driven by geopolitical considerations and internal security concerns. Technological advancements have played a pivotal role, with manufacturers investing in precision engineering, advanced material sciences, and innovative propellant technologies to enhance ammunition performance, reliability, and safety. This is evident in the adoption rates of newer, more efficient ammunition types, which have seen a surge of over 15% in the last five years for small caliber and medium caliber rounds. Consumer demands have also become more sophisticated. The civilian segment, for instance, is increasingly seeking specialized ammunition for self-defense and sport shooting, demanding higher accuracy, consistency, and specialized projectile designs. In the military domain, there's a growing emphasis on interoperability, reduced logistical footprints, and ammunition optimized for modern combat scenarios, including guided munitions and advanced warheads. The historical period of 2019–2024 has seen a steady upward trend, with market revenues growing from an estimated 1.8 billion USD in 2019 to over 2.0 billion USD by 2024, laying a strong foundation for the projected growth in the forecast period of 2025–2033. This evolution reflects a matureing industry adapting to both global trends and regional specificities.

Leading Regions, Countries, or Segments in Ammunition Industry in Latin America

Within the Latin American ammunition industry, Brazil consistently emerges as the dominant country, driven by its robust industrial base, significant defense expenditures, and a burgeoning civilian firearms market. The Small Caliber ammunition segment, encompassing calibers from .22LR to 5.56mm and 9mm, exhibits the most significant market share and growth potential across both civilian and military end-users. This dominance is further amplified by the substantial demand from law enforcement agencies and the substantial civilian population engaged in sport shooting and personal defense. Investment trends in Brazil are heavily tilted towards modernizing domestic production capabilities and research and development for small arms ammunition, with government initiatives often prioritizing national security and self-sufficiency in defense materiel. Regulatory support, though subject to change, generally favors domestic manufacturers and established entities with proven track records.

- Dominant Segment: Small Caliber Ammunition

- Drivers: High demand from civilian self-defense and sport shooting segments, widespread use in military and law enforcement for personal defense weapons and assault rifles, continuous innovation in projectile designs for improved accuracy and terminal ballistics.

- Market Share: Estimated to hold over 45% of the total Latin American ammunition market.

- Investment Trends: Significant private and public investment in advanced manufacturing technologies for small caliber rounds, including advanced metallurgy and propellant compounding.

- Dominant End User: Civilian

- Drivers: Increasing concerns about personal safety, growing participation in recreational shooting sports, availability of licensed firearms for self-defense in several key markets.

- Market Share: Expected to contribute over 35% of the total revenue by 2025.

- Regulatory Support: Evolving regulations in countries like Brazil and Colombia are opening up avenues for responsible civilian ownership and use of firearms and ammunition.

- Key Country: Brazil

- Drivers: Large industrial manufacturing capacity, significant domestic military and police requirements, a substantial civilian firearms market, and proactive government support for the defense industry.

- Market Share: Accounts for an estimated 50% of the total Latin American ammunition market.

- Investment Trends: Government-backed modernization programs for defense companies like IMBEL and EMGEPRON, attracting private sector partnerships and technological collaborations.

While other segments like Medium Caliber and Mortar and Artillery Ammunition are crucial for national defense, their market size and growth rates are comparatively smaller due to specialized applications and higher procurement costs. The Military end-user segment remains a significant driver across all caliber types, with ongoing modernization efforts and regional security dynamics influencing procurement patterns.

Ammunition Industry in Latin America Product Innovations

Product innovations in the Latin American ammunition industry are increasingly focused on enhancing performance and catering to specific user needs. A prime example is the Aguila Ammunition's September 2022 launch of the 9mm, 124-grain Jacketed Hollow Point (JHP). This offering is specifically designed for defense purposes, prioritizing accurate and effective terminal ballistics. This innovation directly addresses the growing civilian demand for reliable self-defense ammunition. In the realm of defense and security, FAMAE's December 2021 unveiling of the technological demonstrator for its 122 mm Rocket Launch System signifies a push towards indigenous development of heavier ordnance, showcasing advancements in rocket propulsion and warhead design. These innovations highlight a trend towards specialized ammunition with superior accuracy, controlled expansion for defense applications, and the development of indigenous capabilities for larger caliber systems.

Propelling Factors for Ammunition Industry in Latin America Growth

Several key factors are propelling the growth of the ammunition industry in Latin America. Increasing Defense Modernization Programs across various nations, driven by evolving geopolitical landscapes and internal security challenges, are a primary driver. Rising Civilian Demand for Firearms and Ammunition, fueled by concerns for personal safety and a growing sporting shooting culture, significantly contributes to market expansion. Technological Advancements in Manufacturing and Ballistics enable the production of more accurate, reliable, and specialized ammunition, attracting both military and civilian consumers. Furthermore, Government Support for Domestic Defense Industries, through incentives and procurement policies, fosters local production and innovation. For instance, initiatives to promote self-sufficiency in defense manufacturing have boosted companies like INDUMIL and OPTIC-CAVIM. The estimated market value for 2025 is projected to exceed 2.1 billion USD, indicative of these robust growth catalysts.

Obstacles in the Ammunition Industry in Latin America Market

Despite robust growth, the ammunition industry in Latin America faces significant obstacles. Stringent and Fragmented Regulatory Frameworks across different countries can complicate market access, import/export procedures, and compliance, leading to increased operational costs and delays. Supply Chain Disruptions, exacerbated by global events and logistical challenges, can impact the availability of raw materials and finished products, leading to price volatility. High Import Tariffs and Taxes in certain nations further inflate the cost of ammunition, potentially hindering sales, especially for civilian consumers. Intensifying Competitive Pressures from both established global players and emerging regional manufacturers necessitate continuous innovation and cost optimization. The illicit arms trade also presents a persistent challenge, often diverting resources and attention from legitimate industry development.

Future Opportunities in Ammunition Industry in Latin America

The future opportunities in the Latin American ammunition industry are diverse and promising. Expansion into Emerging Markets within the region, such as Peru and Chile, presents significant untapped potential for both civilian and military sales. The increasing adoption of Advanced Ammunition Technologies, including guided munitions and less-lethal options, offers avenues for specialized product development and market differentiation. Growing Demand for Training Ammunition and Simulators from military and law enforcement agencies provides a stable recurring revenue stream. Furthermore, Strategic Partnerships and Joint Ventures between local manufacturers and international technology providers can facilitate knowledge transfer and enhance production capabilities. The ongoing focus on Domestic Defense Industrialization will continue to create opportunities for companies like FAMAE and EMGEPRON to expand their product lines and market reach.

Major Players in the Ammunition Industry in Latin America Ecosystem

- IMBEL

- FAMAE

- OPTIC-CAVIM

- CBC Defense

- Magtech Ammunition

- INDUMIL

- Aguila Ammunition

- EMGEPRON

Key Developments in Ammunition Industry in Latin America Industry

- September 2022: Aguila Ammunition launched the 9mm, 124 grain Jacketed Hollow Point (JHP), a product specifically designed for accurate defense purposes, impacting the civilian self-defense ammunition market by offering a specialized and high-performance option.

- December 2021: FAMAE unveiled the technological demonstrator of the 122 mm Rocket Launch System, as part of the project GDD René Echeverría. This development signals significant advancements in indigenous defense technology, particularly in the medium and large caliber segments, enhancing national defense capabilities and potentially opening new export markets for larger ordnance systems.

Strategic Ammunition Industry in Latin America Market Forecast

The strategic forecast for the Latin American ammunition market from 2025 to 2033 indicates sustained robust growth, projected to exceed 3.5 billion USD by the end of the forecast period. This expansion will be driven by ongoing defense modernization initiatives across key nations, coupled with a persistent demand for civilian firearms and ammunition fueled by security concerns and recreational pursuits. Technological innovation will continue to be a critical differentiator, with a growing emphasis on precision, reliability, and specialized applications. Emerging markets within the region, alongside strategic partnerships, are poised to unlock new revenue streams. While regulatory hurdles and supply chain complexities will persist, the overall outlook is positive, supported by increasing investment in domestic manufacturing capabilities and a growing awareness of the strategic importance of a self-sufficient defense industrial base. The market's trajectory is firmly set on an upward trend, driven by a confluence of security needs, evolving consumer preferences, and technological advancements.

Ammunition Industry in Latin America Segmentation

-

1. Ammunition Type

- 1.1. Small Caliber

- 1.2. Medium Caliber

- 1.3. Large Caliber

- 1.4. Mortar and Artillery Ammunition

-

2. End User

- 2.1. Civilian

- 2.2. Military

Ammunition Industry in Latin America Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

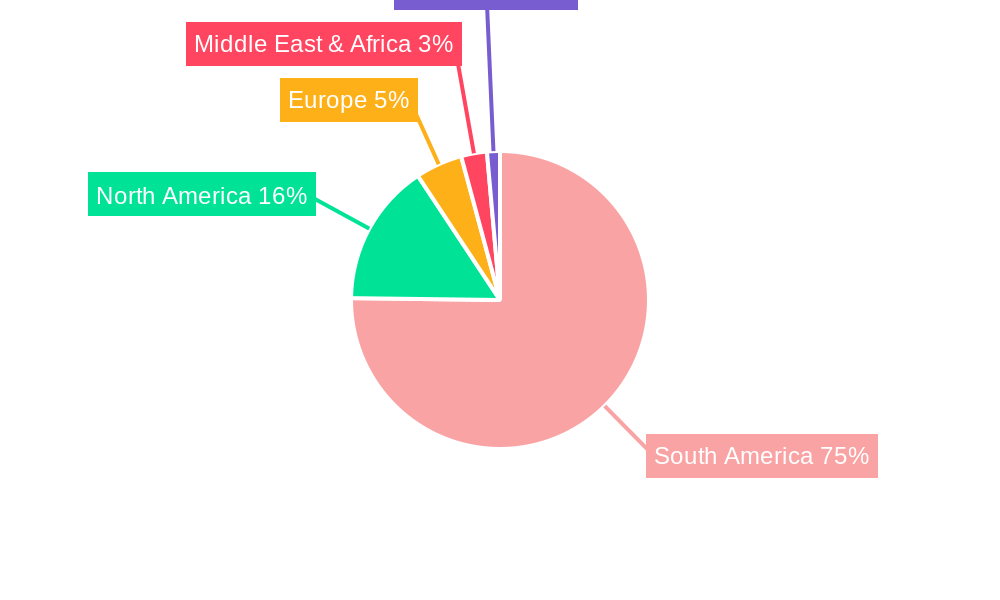

Ammunition Industry in Latin America Regional Market Share

Geographic Coverage of Ammunition Industry in Latin America

Ammunition Industry in Latin America REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 5.1.1. Small Caliber

- 5.1.2. Medium Caliber

- 5.1.3. Large Caliber

- 5.1.4. Mortar and Artillery Ammunition

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Civilian

- 5.2.2. Military

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 6. Global Ammunition Industry in Latin America Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 6.1.1. Small Caliber

- 6.1.2. Medium Caliber

- 6.1.3. Large Caliber

- 6.1.4. Mortar and Artillery Ammunition

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Civilian

- 6.2.2. Military

- 6.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 7. North America Ammunition Industry in Latin America Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 7.1.1. Small Caliber

- 7.1.2. Medium Caliber

- 7.1.3. Large Caliber

- 7.1.4. Mortar and Artillery Ammunition

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Civilian

- 7.2.2. Military

- 7.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 8. South America Ammunition Industry in Latin America Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 8.1.1. Small Caliber

- 8.1.2. Medium Caliber

- 8.1.3. Large Caliber

- 8.1.4. Mortar and Artillery Ammunition

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Civilian

- 8.2.2. Military

- 8.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 9. Europe Ammunition Industry in Latin America Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 9.1.1. Small Caliber

- 9.1.2. Medium Caliber

- 9.1.3. Large Caliber

- 9.1.4. Mortar and Artillery Ammunition

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Civilian

- 9.2.2. Military

- 9.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 10. Middle East & Africa Ammunition Industry in Latin America Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 10.1.1. Small Caliber

- 10.1.2. Medium Caliber

- 10.1.3. Large Caliber

- 10.1.4. Mortar and Artillery Ammunition

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Civilian

- 10.2.2. Military

- 10.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 11. Asia Pacific Ammunition Industry in Latin America Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 11.1.1. Small Caliber

- 11.1.2. Medium Caliber

- 11.1.3. Large Caliber

- 11.1.4. Mortar and Artillery Ammunition

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Civilian

- 11.2.2. Military

- 11.1. Market Analysis, Insights and Forecast - by Ammunition Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 IMBEL

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FAMAE

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 OPTIC-CAVIM

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 CBC Defense

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Magtech Ammunitio

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 INDUMIL

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Aguila Ammunition

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 EMGEPRON

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 IMBEL

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Ammunition Industry in Latin America Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Ammunition Industry in Latin America Revenue (billion), by Ammunition Type 2025 & 2033

- Figure 3: North America Ammunition Industry in Latin America Revenue Share (%), by Ammunition Type 2025 & 2033

- Figure 4: North America Ammunition Industry in Latin America Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Ammunition Industry in Latin America Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Ammunition Industry in Latin America Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Ammunition Industry in Latin America Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ammunition Industry in Latin America Revenue (billion), by Ammunition Type 2025 & 2033

- Figure 9: South America Ammunition Industry in Latin America Revenue Share (%), by Ammunition Type 2025 & 2033

- Figure 10: South America Ammunition Industry in Latin America Revenue (billion), by End User 2025 & 2033

- Figure 11: South America Ammunition Industry in Latin America Revenue Share (%), by End User 2025 & 2033

- Figure 12: South America Ammunition Industry in Latin America Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Ammunition Industry in Latin America Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ammunition Industry in Latin America Revenue (billion), by Ammunition Type 2025 & 2033

- Figure 15: Europe Ammunition Industry in Latin America Revenue Share (%), by Ammunition Type 2025 & 2033

- Figure 16: Europe Ammunition Industry in Latin America Revenue (billion), by End User 2025 & 2033

- Figure 17: Europe Ammunition Industry in Latin America Revenue Share (%), by End User 2025 & 2033

- Figure 18: Europe Ammunition Industry in Latin America Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Ammunition Industry in Latin America Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ammunition Industry in Latin America Revenue (billion), by Ammunition Type 2025 & 2033

- Figure 21: Middle East & Africa Ammunition Industry in Latin America Revenue Share (%), by Ammunition Type 2025 & 2033

- Figure 22: Middle East & Africa Ammunition Industry in Latin America Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East & Africa Ammunition Industry in Latin America Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East & Africa Ammunition Industry in Latin America Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ammunition Industry in Latin America Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ammunition Industry in Latin America Revenue (billion), by Ammunition Type 2025 & 2033

- Figure 27: Asia Pacific Ammunition Industry in Latin America Revenue Share (%), by Ammunition Type 2025 & 2033

- Figure 28: Asia Pacific Ammunition Industry in Latin America Revenue (billion), by End User 2025 & 2033

- Figure 29: Asia Pacific Ammunition Industry in Latin America Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific Ammunition Industry in Latin America Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Ammunition Industry in Latin America Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ammunition Industry in Latin America Revenue billion Forecast, by Ammunition Type 2020 & 2033

- Table 2: Global Ammunition Industry in Latin America Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Ammunition Industry in Latin America Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Ammunition Industry in Latin America Revenue billion Forecast, by Ammunition Type 2020 & 2033

- Table 5: Global Ammunition Industry in Latin America Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Ammunition Industry in Latin America Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Ammunition Industry in Latin America Revenue billion Forecast, by Ammunition Type 2020 & 2033

- Table 11: Global Ammunition Industry in Latin America Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Ammunition Industry in Latin America Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Ammunition Industry in Latin America Revenue billion Forecast, by Ammunition Type 2020 & 2033

- Table 17: Global Ammunition Industry in Latin America Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global Ammunition Industry in Latin America Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Ammunition Industry in Latin America Revenue billion Forecast, by Ammunition Type 2020 & 2033

- Table 29: Global Ammunition Industry in Latin America Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Ammunition Industry in Latin America Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Ammunition Industry in Latin America Revenue billion Forecast, by Ammunition Type 2020 & 2033

- Table 38: Global Ammunition Industry in Latin America Revenue billion Forecast, by End User 2020 & 2033

- Table 39: Global Ammunition Industry in Latin America Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ammunition Industry in Latin America Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ammunition Industry in Latin America?

The projected CAGR is approximately 3.49%.

2. Which companies are prominent players in the Ammunition Industry in Latin America?

Key companies in the market include IMBEL, FAMAE, OPTIC-CAVIM, CBC Defense, Magtech Ammunitio, INDUMIL, Aguila Ammunition, EMGEPRON.

3. What are the main segments of the Ammunition Industry in Latin America?

The market segments include Ammunition Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The Military Segment to Dominate the Market During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In September 2022, Aguila Ammunition launched the 9mm, 124 grain Jacketed Hollow Point (JHP), which claims to be the right choice for those seeking accurate ammunition for defense purposes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ammunition Industry in Latin America," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ammunition Industry in Latin America report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ammunition Industry in Latin America?

To stay informed about further developments, trends, and reports in the Ammunition Industry in Latin America, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence