Key Insights

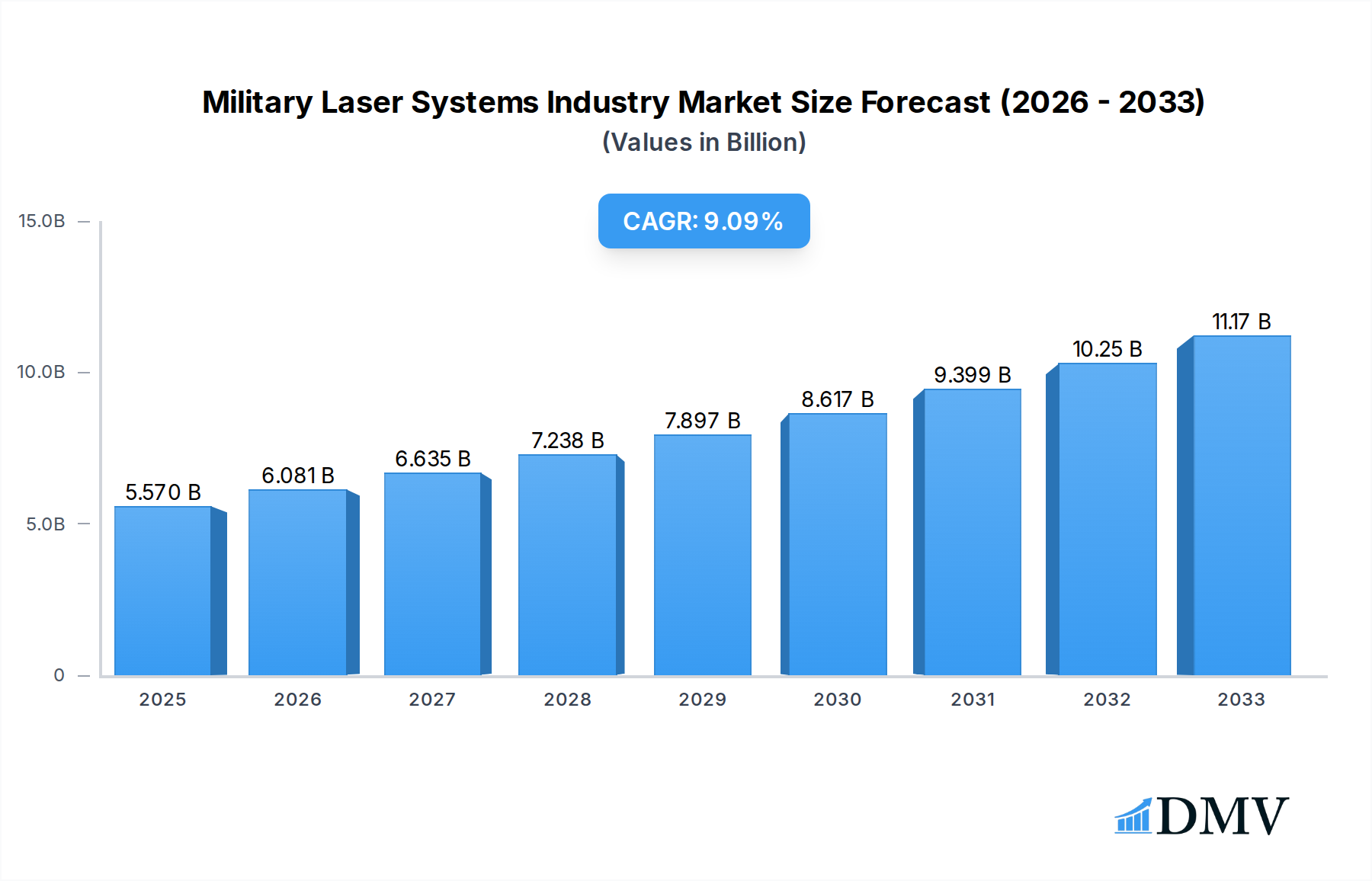

The Military Laser Systems Industry is poised for significant expansion, with a projected market size of 5570 Million in 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 9.09% through 2033. This dynamic growth is fueled by the escalating demand for advanced defense capabilities, including sophisticated directed energy weapons, precision guidance systems, and enhanced laser sighting and rangefinding technologies. Modern military forces are increasingly investing in laser systems to achieve superior battlefield dominance, improve target acquisition, and develop non-lethal or less-lethal engagement options. The ongoing geopolitical tensions and the pursuit of technological superiority by major global powers are central to this upward market trajectory. Furthermore, advancements in laser technology, such as the development of more compact, efficient, and powerful solid-state lasers, are making these systems more deployable and cost-effective, further stimulating market adoption.

Military Laser Systems Industry Market Size (In Billion)

The industry's growth is also influenced by several key trends, including the integration of artificial intelligence and machine learning to enhance laser system autonomy and targeting accuracy, and the growing emphasis on counter-drone capabilities using laser technology. The development of multi-spectrum laser systems that can operate across various environmental conditions and target types also represents a significant trend. However, the market faces certain restraints, such as the high cost of research, development, and deployment of cutting-edge laser technologies, and the complex regulatory frameworks surrounding the use of directed energy weapons. Despite these challenges, the strategic importance of laser systems in modern warfare, coupled with continuous innovation from leading companies like Thales, Lockheed Martin, and Raytheon Technologies, ensures a promising outlook for the Military Laser Systems Industry. The Asia Pacific region, particularly China and India, is emerging as a key growth area due to significant defense modernization efforts.

Military Laser Systems Industry Company Market Share

The global Military Laser Systems industry is characterized by a dynamic and evolving market, driven by escalating geopolitical tensions and rapid advancements in directed energy technologies. Market concentration is moderately high, with a few key players dominating significant portions of the market share. Innovation is primarily fueled by intensive R&D investments in cutting-edge laser technologies and their integration into sophisticated weapon platforms and defense systems. The regulatory landscape is intricate, involving national defense budgets, arms control treaties, and export/import regulations, all of which influence market access and product development. Substitute products, such as traditional projectile-based weaponry, are gradually being challenged by the superior speed-of-light engagement capabilities and reduced logistical footprints offered by laser systems. End-user profiles predominantly consist of national defense ministries and armed forces worldwide, with a growing interest from homeland security agencies. Mergers and acquisitions (M&A) activities are prevalent as established defense contractors seek to expand their capabilities and market reach in this high-growth sector. M&A deal values are projected to reach several hundred million dollars annually, reflecting the strategic importance and commercial potential of military laser systems. Market share distribution sees major players like Lockheed Martin Corporation, RTX Corporation, and Northrop Grumman Corporation holding substantial portions, though emerging players are gaining traction through specialized technological offerings.

Military Laser Systems Industry Industry Evolution

The Military Laser Systems industry has undergone a transformative evolution, charting a trajectory of robust growth and technological sophistication. Over the historical period of 2019-2024, the market witnessed a steady increase in demand, fueled by an increasing recognition of directed energy weapons (DEWs) as a critical component of modern warfare. This period saw significant investments in research and development, leading to substantial technological advancements in laser power, beam quality, and system miniaturization. The adoption of laser-based solutions extended beyond traditional combat roles, encompassing applications like advanced guidance systems, precision targeting, and electronic warfare. Shifting consumer demands, in this context, translated to a growing requirement for scalable, adaptable, and more cost-effective DEW solutions that offer distinct tactical advantages over conventional armaments.

The base year of 2025 marks a significant inflection point, with the market poised for accelerated expansion. Projections indicate a Compound Annual Growth Rate (CAGR) of approximately 8-12% during the forecast period of 2025-2033. This growth is intrinsically linked to ongoing military modernization programs across major nations, particularly the United States, China, and European powers, who are prioritizing the integration of DEWs into their defense arsenals. Technological advancements are focusing on developing higher-power lasers capable of defeating a wider range of threats, including drones, missiles, and even manned aircraft, alongside improvements in sensor fusion and targeting algorithms for enhanced accuracy and reduced collateral damage. Adoption metrics for key technologies, such as solid-state lasers, are expected to rise significantly, eclipsing older gas laser technologies due to their greater efficiency, longevity, and smaller form factors. Furthermore, the increasing emphasis on counter-unmanned aerial system (C-UAS) capabilities is a major catalyst, driving demand for portable and rapidly deployable laser defense systems. The industry's evolution is thus characterized by a relentless pursuit of enhanced performance, greater battlefield utility, and strategic deterrence, solidifying the indispensable role of military laser systems in future defense architectures.

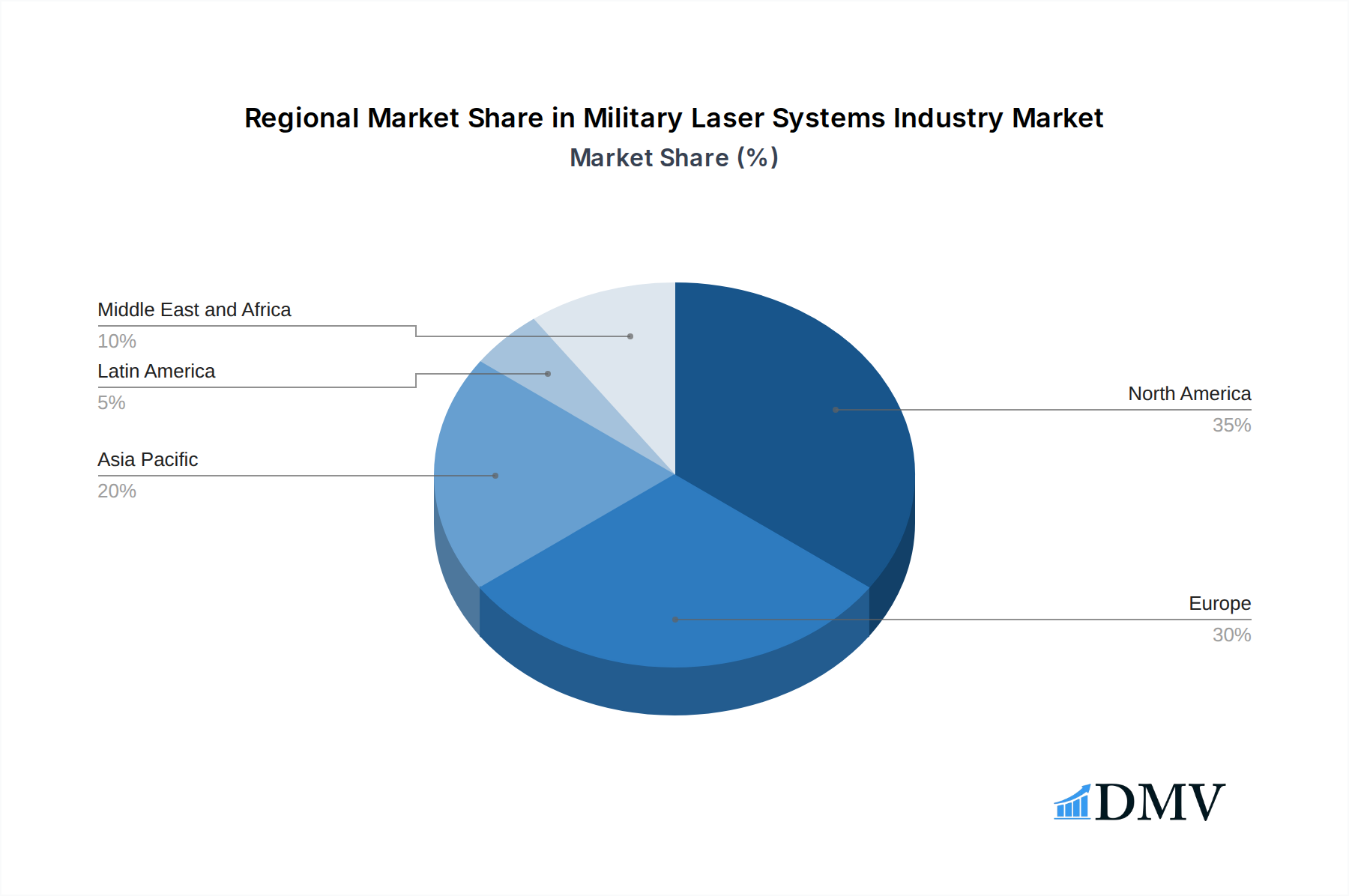

Leading Regions, Countries, or Segments in Military Laser Systems Industry

The global Military Laser Systems industry is heavily influenced by regional investments, technological prowess, and strategic defense priorities. Within the Technology segment, Solid-state Lasers are emerging as the dominant force, surpassing Gas Lasers and Other Technologies due to their superior efficiency, scalability, and reliability. Solid-state laser systems offer faster pulse repetition rates, higher beam quality, and a smaller physical footprint, making them ideal for integration into diverse platforms from man-portable systems to large naval vessels.

In terms of Application, Directed Energy Weapons (DEWs) represent the most significant and rapidly growing segment. This surge is driven by the urgent need for effective counter-drone capabilities, anti-missile systems, and defensive applications against a spectrum of aerial and maritime threats. The speed-of-light engagement offered by DEWs provides a critical tactical advantage, reducing reaction times and enabling precise neutralization of targets.

Geographically, the United States stands out as the leading region and country in the Military Laser Systems industry. This dominance is underpinned by several key drivers:

- Extensive Defense Spending and R&D Investment: The U.S. Department of Defense (DoD) consistently allocates substantial budgets towards advanced weapons systems research and development, with directed energy being a top priority. Significant investment is channeled into programs aimed at developing and fielding high-energy laser (HEL) weapon systems.

- Technological Leadership: American defense contractors like Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, and The Boeing Company are at the forefront of laser technology innovation, possessing advanced manufacturing capabilities and extensive intellectual property in this domain.

- Strategic Imperatives: The U.S. faces a complex and evolving threat landscape, including the proliferation of drones and advanced missile systems, which necessitates the development and deployment of cutting-edge defensive technologies like military laser systems.

Furthermore, the North American region, encompassing the United States and Canada, demonstrates significant market penetration due to strong governmental backing and a robust defense industrial base. Emerging markets in the Asia-Pacific region, particularly China and South Korea, are also exhibiting considerable growth driven by their own military modernization efforts and increasing investments in DEW research.

Military Laser Systems Industry Product Innovations

The Military Laser Systems industry is characterized by a rapid pace of product innovation, focusing on enhancing power, efficiency, and battlefield applicability. Key advancements include the development of kilowatt-class solid-state lasers for directed energy weapon systems, offering superior speed-of-light engagement capabilities against drones and asymmetric threats. Innovations in beam control and targeting systems are improving accuracy and reducing collateral damage, making laser weapons more versatile. For example, RTX Corporation's recent delivery of a 10 KW palletized laser weapon to the US Air Force exemplifies the trend towards modular, deployable systems that can be integrated across various platforms. Applications extend beyond DEWs to advanced laser sights, designators, and rangefinders, providing soldiers with enhanced situational awareness and precision targeting capabilities. Performance metrics are continually being pushed, with a focus on increased range, reduced size, weight, and power (SWaP), and improved operational reliability in diverse environmental conditions.

Propelling Factors for Military Laser Systems Industry Growth

The growth of the Military Laser Systems industry is propelled by several interconnected factors. A primary driver is the escalating global security landscape and the increasing prevalence of asymmetric threats, such as unmanned aerial systems (UAS) and swarm attacks, which traditional kinetic weapons struggle to counter effectively. This has spurred significant government investment in directed energy weapons (DEWs) for their speed-of-light engagement capabilities and precision. Technological advancements in solid-state laser technology, characterized by higher power output, increased efficiency, and smaller form factors, are making these systems more deployable and cost-effective. Furthermore, the strategic imperative for military modernization across major powers, aiming to enhance force protection and maintain technological superiority, is a significant catalyst. Regulatory support and clear defense procurement strategies in key markets further bolster growth.

Obstacles in the Military Laser Systems Industry Market

Despite its robust growth, the Military Laser Systems industry faces several obstacles. A significant restraint is the high cost of research, development, and procurement of advanced laser systems, which can strain defense budgets. Regulatory hurdles and stringent export control policies can also impede market access and international collaboration. The nascent nature of some technologies means that issues with power generation, thermal management, and atmospheric distortion can affect system performance in real-world combat scenarios. Supply chain disruptions, particularly for specialized components and rare earth materials, can also pose challenges. Furthermore, the development of countermeasures by potential adversaries presents a continuous technological race, demanding ongoing innovation and investment.

Future Opportunities in Military Laser Systems Industry

The Military Laser Systems industry is ripe with future opportunities. The growing global demand for robust counter-drone capabilities presents a significant market for compact, scalable laser defense systems. Emerging applications in electronic warfare, directed energy missile defense, and cyber-attack deterrence offer new avenues for innovation and market expansion. The development of even higher-power lasers, capable of neutralizing more resilient targets, is another promising area. Furthermore, the increasing trend towards networked warfare and integrated defense systems creates opportunities for laser systems to be seamlessly incorporated into broader combat architectures. Partnerships and collaborations between defense contractors and technology firms are expected to accelerate advancements and unlock new market segments, particularly in rapidly modernizing defense markets across Asia and the Middle East.

Major Players in the Military Laser Systems Industry Ecosystem

- THALES

- Leidos Inc

- Rheinmetall AG

- Elbit Systems Ltd

- Lockheed Martin Corporation

- MBDA

- IAI

- Rafael Advanced Defense Systems Ltd

- RTX Corporation

- BAE Systems plc

- Northrop Grumman Corporation

- The Boeing Company

Key Developments in Military Laser Systems Industry Industry

- June 2023: RTX Corporation delivered the fourth combat-ready laser weapon to the US Air Force. This new palletized laser weapon was the first 10 KW laser built to US military specifications in a stand-alone configuration that can be moved and mounted anywhere it's needed, significantly enhancing mobile defense capabilities.

- April 2023: The US Department of Defence (DoD) selected NUBURU Inc. of Centennial for a position on the multiple-award indefinite-delivery/indefinite-quantity (IDIQ) contract for the fabrication and delivery of prototypes and equipment in support of solid-state high-energy laser (HEL) weapon systems. NUBURU Inc. conducts research, development, design, and manufacturing of high-power, high-brightness blue lasers, signaling continued investment in cutting-edge laser technologies.

- March 2023: Blighter Surveillance Systems was awarded a contract to supply Raytheon UK with its multi-mode A800 3D e-scan radars as part of a laser weapon project with the UK MoD, highlighting the integration of advanced radar systems with laser weapon platforms for enhanced threat detection and engagement.

Strategic Military Laser Systems Industry Market Forecast

The strategic forecast for the Military Laser Systems industry points towards sustained and accelerated growth, driven by an escalating need for advanced defensive capabilities and continuous technological innovation. The increasing adoption of directed energy weapons, particularly for counter-drone operations, will remain a primary growth catalyst. Significant investments in research and development by major defense powers, coupled with modernization programs, will fuel market expansion throughout the forecast period. Opportunities will emerge in developing more powerful, efficient, and compact laser systems, as well as in integrating these technologies into networked defense architectures. The market is poised to benefit from a growing global emphasis on precision strike capabilities and the deterrence of evolving asymmetric threats, positioning military laser systems as a critical component of future defense strategies.

Military Laser Systems Industry Segmentation

-

1. Technology

- 1.1. Solid-state Lasers

- 1.2. Gas Lasers

- 1.3. Other Technologies

-

2. Application

- 2.1. Directed Energy Weapons

- 2.2. Guidance Systems

- 2.3. Laser Sights, Designators, and Rangefinders

- 2.4. Other Applications

Military Laser Systems Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Russia

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Israel

- 5.4. Rest of Middle East and Africa

Military Laser Systems Industry Regional Market Share

Geographic Coverage of Military Laser Systems Industry

Military Laser Systems Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.09% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Solid-state Lasers

- 5.1.2. Gas Lasers

- 5.1.3. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Directed Energy Weapons

- 5.2.2. Guidance Systems

- 5.2.3. Laser Sights, Designators, and Rangefinders

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Military Laser Systems Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Solid-state Lasers

- 6.1.2. Gas Lasers

- 6.1.3. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Directed Energy Weapons

- 6.2.2. Guidance Systems

- 6.2.3. Laser Sights, Designators, and Rangefinders

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Military Laser Systems Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Solid-state Lasers

- 7.1.2. Gas Lasers

- 7.1.3. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Directed Energy Weapons

- 7.2.2. Guidance Systems

- 7.2.3. Laser Sights, Designators, and Rangefinders

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Military Laser Systems Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Solid-state Lasers

- 8.1.2. Gas Lasers

- 8.1.3. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Directed Energy Weapons

- 8.2.2. Guidance Systems

- 8.2.3. Laser Sights, Designators, and Rangefinders

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Pacific Military Laser Systems Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Solid-state Lasers

- 9.1.2. Gas Lasers

- 9.1.3. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Directed Energy Weapons

- 9.2.2. Guidance Systems

- 9.2.3. Laser Sights, Designators, and Rangefinders

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Latin America Military Laser Systems Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Solid-state Lasers

- 10.1.2. Gas Lasers

- 10.1.3. Other Technologies

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Directed Energy Weapons

- 10.2.2. Guidance Systems

- 10.2.3. Laser Sights, Designators, and Rangefinders

- 10.2.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Middle East and Africa Military Laser Systems Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Solid-state Lasers

- 11.1.2. Gas Lasers

- 11.1.3. Other Technologies

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Directed Energy Weapons

- 11.2.2. Guidance Systems

- 11.2.3. Laser Sights, Designators, and Rangefinders

- 11.2.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 THALES

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Leidos Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Rheinmetall AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Elbit Systems Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Lockheed Martin Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 MBDA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 IAI

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Rafael Advanced Defense Systems Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 RTX Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 BAE Systems plc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Northrop Grumman Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 The Boeing Company

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 THALES

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Military Laser Systems Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Military Laser Systems Industry Revenue (Million), by Technology 2025 & 2033

- Figure 3: North America Military Laser Systems Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Military Laser Systems Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Military Laser Systems Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Military Laser Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Military Laser Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Military Laser Systems Industry Revenue (Million), by Technology 2025 & 2033

- Figure 9: Europe Military Laser Systems Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Europe Military Laser Systems Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: Europe Military Laser Systems Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Military Laser Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Military Laser Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Military Laser Systems Industry Revenue (Million), by Technology 2025 & 2033

- Figure 15: Asia Pacific Military Laser Systems Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Asia Pacific Military Laser Systems Industry Revenue (Million), by Application 2025 & 2033

- Figure 17: Asia Pacific Military Laser Systems Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Military Laser Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Military Laser Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Military Laser Systems Industry Revenue (Million), by Technology 2025 & 2033

- Figure 21: Latin America Military Laser Systems Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Latin America Military Laser Systems Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Latin America Military Laser Systems Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Latin America Military Laser Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Military Laser Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Military Laser Systems Industry Revenue (Million), by Technology 2025 & 2033

- Figure 27: Middle East and Africa Military Laser Systems Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Middle East and Africa Military Laser Systems Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Military Laser Systems Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Military Laser Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Military Laser Systems Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Military Laser Systems Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 2: Global Military Laser Systems Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Military Laser Systems Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Military Laser Systems Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 5: Global Military Laser Systems Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Military Laser Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Military Laser Systems Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 10: Global Military Laser Systems Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 11: Global Military Laser Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Germany Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: France Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Italy Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Russia Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global Military Laser Systems Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 19: Global Military Laser Systems Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Military Laser Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: China Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: India Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: South Korea Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Military Laser Systems Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 27: Global Military Laser Systems Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Military Laser Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: Brazil Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Latin America Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Military Laser Systems Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 32: Global Military Laser Systems Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 33: Global Military Laser Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: United Arab Emirates Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Saudi Arabia Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Israel Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Military Laser Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Military Laser Systems Industry?

The projected CAGR is approximately 9.09%.

2. Which companies are prominent players in the Military Laser Systems Industry?

Key companies in the market include THALES, Leidos Inc, Rheinmetall AG, Elbit Systems Ltd, Lockheed Martin Corporation, MBDA, IAI, Rafael Advanced Defense Systems Ltd, RTX Corporation, BAE Systems plc, Northrop Grumman Corporation, The Boeing Company.

3. What are the main segments of the Military Laser Systems Industry?

The market segments include Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.57 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions.

6. What are the notable trends driving market growth?

Directed Energy Weapons Segment Projected to Exhibit the Highest CAGR During the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data.

8. Can you provide examples of recent developments in the market?

June 2023: RTX Corporation delivered the fourth combat-ready laser weapon to the US Air Force. The new palletized laser weapon was the first 10 KW laser built to US military specifications in a stand-alone configuration that can be moved and mounted anywhere it's needed.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Military Laser Systems Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Military Laser Systems Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Military Laser Systems Industry?

To stay informed about further developments, trends, and reports in the Military Laser Systems Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence