Key Insights

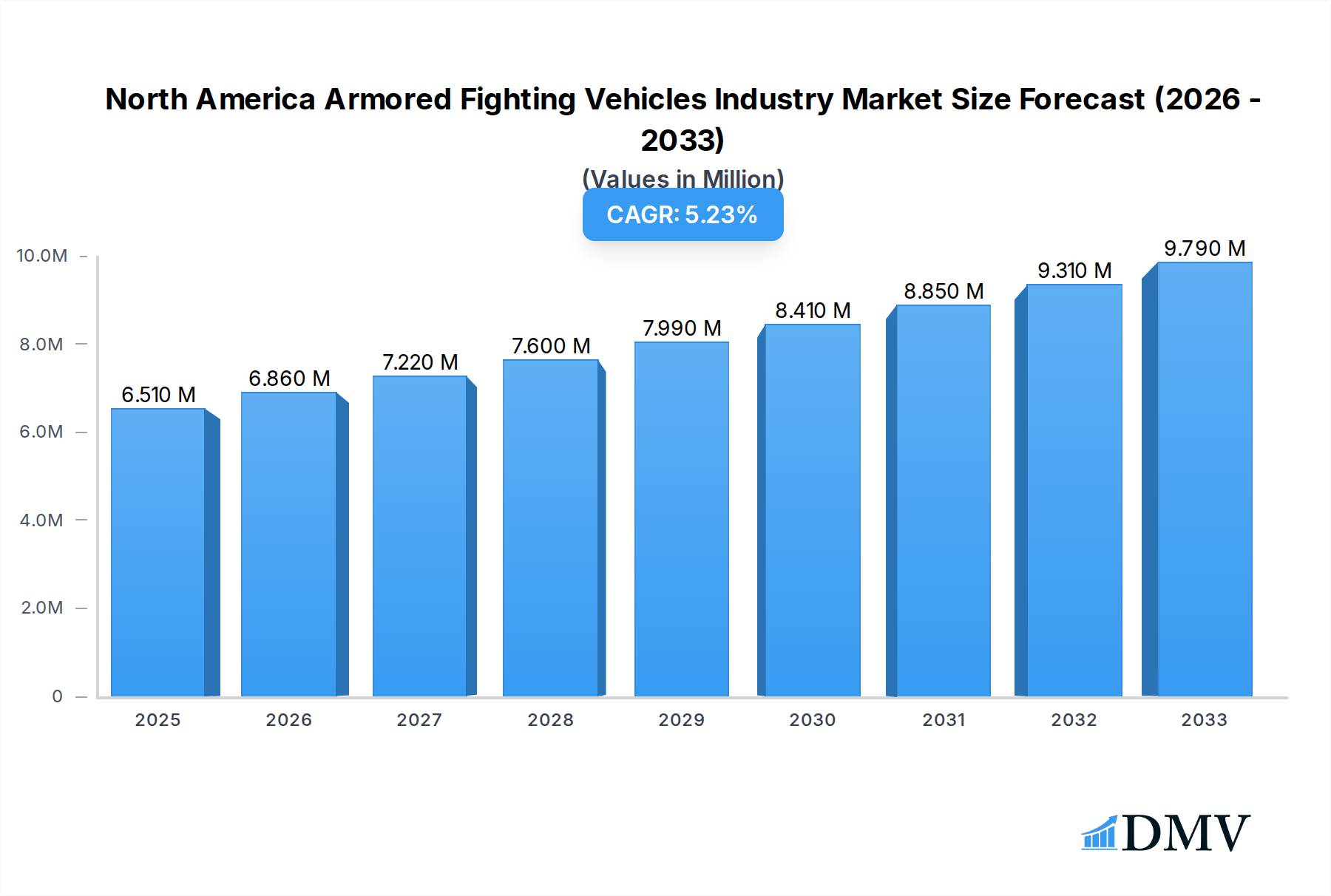

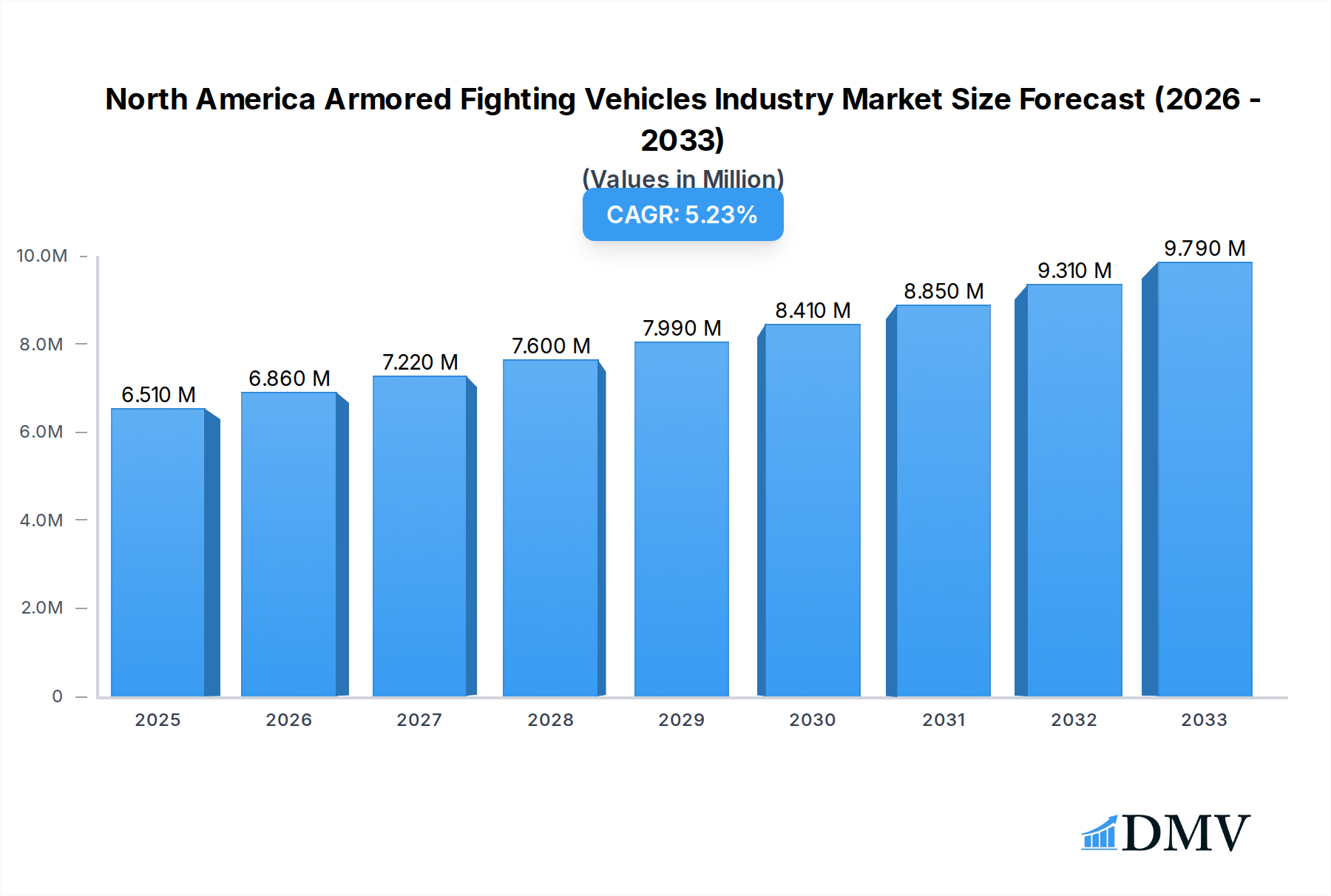

The North American Armored Fighting Vehicles (AFV) market is poised for robust expansion, projected to reach USD 6.51 million by 2025, driven by a CAGR of 5.18% through 2033. This sustained growth is underpinned by escalating geopolitical tensions and the ongoing modernization efforts within the defense sectors of the United States and Canada. The increasing demand for advanced protection and enhanced combat capabilities for military personnel fuels the adoption of sophisticated AFV solutions. Key drivers include the need to counter evolving threats, the replacement of aging vehicle fleets, and significant government defense spending aimed at maintaining technological superiority. The market is witnessing a strong emphasis on developing lighter, more agile, and technologically advanced vehicles that offer superior survivability and operational efficiency across diverse battlefield scenarios.

North America Armored Fighting Vehicles Industry Market Size (In Million)

The AFV market in North America is characterized by a diverse range of product segments, with Armored Personnel Carriers (APC) and Infantry Fighting Vehicles (IFV) likely to dominate due to their critical role in troop transport and direct combat support. Main Battle Tanks (MBT) also represent a significant segment, albeit with longer replacement cycles, catering to heavy armor requirements. Emerging trends include the integration of artificial intelligence, advanced sensor systems, and enhanced network-centric warfare capabilities into these vehicles. Furthermore, a growing focus on modular designs and cost-effective upgrades is influencing procurement strategies. Restraints, such as budget constraints and lengthy procurement cycles, are being addressed through innovative financing models and phased modernization programs, ensuring continued market dynamism. The competitive landscape is marked by major defense contractors like General Dynamics Corporation, BAE Systems plc, and Textron Inc., all vying to secure contracts through technological innovation and strategic partnerships.

North America Armored Fighting Vehicles Industry Company Market Share

North America Armored Fighting Vehicles Industry Market Composition & Trends

The North America Armored Fighting Vehicles (AFVs) industry is characterized by a moderate level of market concentration, driven by a few key players dominating the landscape. Innovation is a continuous catalyst, fueled by evolving geopolitical threats and the relentless pursuit of enhanced survivability and operational effectiveness. Regulatory frameworks, primarily influenced by national defense budgets and international arms control agreements, significantly shape market access and development. Substitute products, while limited in the direct combat role, can emerge in the form of advanced wheeled vehicles or indirect fire support systems. End-user profiles are predominantly governmental defense ministries and military organizations within the United States and Canada, prioritizing advanced protection, firepower, and modularity. Mergers and Acquisitions (M&A) activities are strategic, aimed at consolidating capabilities, expanding product portfolios, and securing market share. For instance, significant M&A deals within the defense sector, estimated to be in the billions of US Dollars annually, often involve acquisitions of specialized AFV component manufacturers or divisions. Market share distribution is closely tied to major defense procurement contracts and technological leadership, with key players like General Dynamics Corporation and BAE Systems plc holding substantial portions.

- Market Concentration: Dominated by a few major defense contractors.

- Innovation Catalysts: Evolving threat landscapes, demand for advanced capabilities.

- Regulatory Landscape: National defense budgets, international agreements.

- Substitute Products: Limited direct combat, but alternative support systems exist.

- End-User Profiles: Government defense ministries and military organizations.

- M&A Activities: Strategic consolidation, portfolio expansion, market share acquisition.

- M&A Deal Values: Estimated in the billions of US Dollars annually.

- Market Share Distribution: Tied to major procurement contracts and technological prowess.

North America Armored Fighting Vehicles Industry Industry Evolution

The North America Armored Fighting Vehicles (AFVs) industry has undergone a significant evolution, driven by a dynamic interplay of technological advancements, shifting geopolitical demands, and evolving military doctrines. Throughout the historical period of 2019–2024, the market witnessed a steady demand for robust and versatile AFVs, with a particular emphasis on upgrading existing fleets and introducing incrementally improved models. The base year of 2025 marks a pivotal point where industry stakeholders are poised for more substantial transformations, anticipating increased investment in next-generation platforms. This evolution is deeply intertwined with the continuous quest for enhanced survivability, superior firepower, and greater operational mobility, directly influenced by the experiences gained in various global theaters of operation. Technological innovation has been a relentless force, with advancements in composite armor, active protection systems (APS), networked warfare capabilities, and hybrid-electric powertrains becoming increasingly critical. These innovations are not merely incremental; they represent a paradigm shift in how armored warfare is conceived and executed, moving towards more intelligent, adaptable, and lethal platforms.

The forecast period of 2025–2033 is projected to witness accelerated growth, with an estimated Compound Annual Growth Rate (CAGR) of approximately 4.5% to 6.0%, reaching a market valuation potentially exceeding tens of billions of US Dollars by the end of the study period. This growth will be underpinned by several factors, including the modernization programs of major North American militaries, the increasing demand for interoperable systems across allied forces, and the growing recognition of the critical role AFVs play in both conventional and asymmetric conflicts. Shifting consumer demands, in this context, refer to the evolving requirements of military end-users, who are increasingly prioritizing platforms that offer modularity for mission-specific configurations, reduced logistical footprints, and advanced situational awareness. The adoption of technologies like artificial intelligence (AI) for battlefield management and autonomous functions, alongside directed-energy weapons and advanced sensor suites, will become more prevalent. Furthermore, the focus on sustainability and reduced environmental impact, while perhaps secondary to immediate combat effectiveness, is slowly emerging as a consideration in the development of future AFVs, pushing for more fuel-efficient designs and alternative power sources. The industry's ability to adapt to these multifaceted demands will be crucial for sustained growth and relevance.

Leading Regions, Countries, or Segments in North America Armored Fighting Vehicles Industry

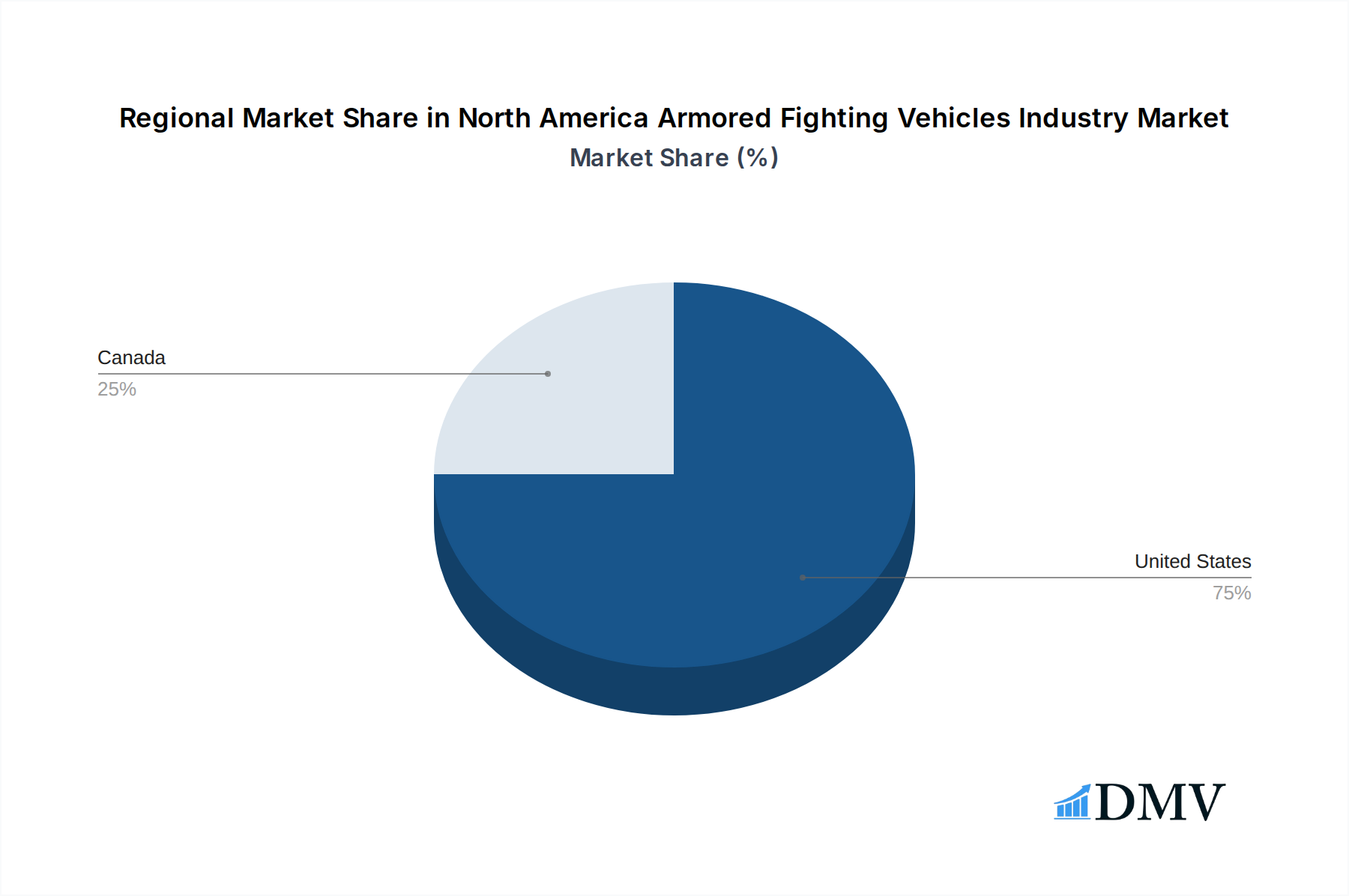

The North America Armored Fighting Vehicles (AFVs) industry is unequivocally dominated by the United States, which serves as the primary market and a global leader in AFV development, production, and procurement. This dominance is driven by a confluence of factors, including the sheer size of the U.S. defense budget, the presence of leading global defense contractors, and the continuous requirement for advanced armored capabilities to maintain military superiority. The U.S. military's extensive operational experience also directly informs the design and evolution of AFVs, pushing the boundaries of innovation.

- Dominant Country: United States

- Investment Trends: The U.S. Department of Defense (DoD) consistently allocates substantial funds towards the acquisition and modernization of armored vehicle fleets. This includes multi-year procurement contracts for main battle tanks, infantry fighting vehicles, and armored personnel carriers, ensuring a sustained demand. The projected annual investment in AFVs within the United States is expected to remain in the range of USD 10,000 million to USD 15,000 million throughout the forecast period.

- Regulatory Support: Favorable governmental policies, including robust research and development (R&D) tax incentives and streamlined procurement processes for defense technologies, further bolster the U.S. market. Domestic production requirements also create a strong incentive for manufacturers to establish and maintain operations within the country.

- Technological Hub: The concentration of leading defense contractors, research institutions, and specialized manufacturing facilities in the U.S. creates a powerful ecosystem for technological innovation in AFVs. This includes advancements in protection systems, weapon platforms, and onboard electronics.

- Geopolitical Influence: The U.S.'s global security role necessitates a highly capable and technologically advanced armored force, driving the demand for cutting-edge AFV solutions.

While the United States stands out, Canada represents a significant, albeit smaller, market segment within North America. The Canadian Armed Forces are actively engaged in modernizing their armored fleet, driven by the need to replace aging equipment and enhance their capabilities for expeditionary operations and homeland defense. Investment in the Canadian AFV market, though lower than in the U.S., is steady, with significant procurements occurring periodically.

In terms of Vehicle Type, the Main Battle Tank (MBT) and Infantry Fighting Vehicle (IFV) segments are historically the most prominent and receive the largest share of investment due to their critical combat roles. However, the demand for Armored Personnel Carriers (APC) remains robust, particularly for troop transport and support roles in various operational environments. The "Other Vehicle Types" category, encompassing reconnaissance vehicles, combat engineering vehicles, and self-propelled artillery, also contributes to market diversity and is subject to evolving battlefield needs. The U.S. Army's ongoing modernization efforts, for example, focus on a balanced portfolio across these types, ensuring a comprehensive armored capability.

North America Armored Fighting Vehicles Industry Product Innovations

The North America Armored Fighting Vehicles (AFVs) industry is witnessing groundbreaking product innovations centered on enhanced survivability, modularity, and networked warfare capabilities. Key advancements include the integration of next-generation composite armor materials and active protection systems (APS) designed to intercept incoming threats, significantly reducing vulnerability on the battlefield. The development of modular designs allows for rapid reconfiguration of AFVs to meet specific mission requirements, from troop transport to direct fire support, enhancing operational flexibility. Furthermore, the incorporation of advanced sensor suites, artificial intelligence (AI) for target recognition and threat assessment, and robust communication systems are creating truly networked platforms that can share real-time battlefield information, leading to improved situational awareness and coordinated operations. These innovations translate into superior performance metrics such as increased protection levels against modern anti-tank weapons, greater agility and speed in varied terrains, and enhanced firepower with advanced cannon and missile systems, positioning these vehicles at the forefront of modern military operations.

Propelling Factors for North America Armored Fighting Vehicles Industry Growth

Several key factors are propelling the growth of the North America Armored Fighting Vehicles (AFVs) industry. Firstly, the persistent and evolving geopolitical tensions globally necessitate continuous modernization and expansion of armored forces by North American nations. Secondly, significant government defense spending, driven by national security strategies and modernization programs, directly translates into substantial procurement contracts for new and upgraded AFVs. Thirdly, technological advancements, particularly in areas like active protection systems, advanced armor, and networked warfare capabilities, are creating demand for next-generation vehicles that offer superior performance and survivability. Finally, the ongoing need to replace aging vehicle fleets with more capable and adaptable platforms ensures a consistent market for manufacturers.

- Geopolitical Instability: Heightened global security concerns drive demand for robust armored capabilities.

- Government Defense Budgets: Increased and sustained military spending by the US and Canada.

- Technological Advancements: Innovation in protection, lethality, and networked systems.

- Fleet Modernization: Requirement to replace aging platforms with advanced alternatives.

Obstacles in the North America Armored Fighting Vehicles Industry Market

The North America Armored Fighting Vehicles (AFVs) industry faces several significant obstacles that can impede growth and market dynamics. Foremost among these are the substantial financial outlays required for the research, development, and procurement of advanced AFVs, often running into billions of US Dollars for major programs, which can strain defense budgets. Regulatory hurdles, including stringent export controls and compliance with evolving international arms trade agreements, can complicate international sales and collaborations. Supply chain disruptions, particularly for specialized components and rare earth materials, can lead to production delays and increased costs, with potential impacts on delivery timelines for critical defense equipment. Furthermore, intense competitive pressures among established defense contractors and the emergence of new technological solutions can create market uncertainty. The lengthy procurement cycles inherent in government defense acquisition processes also pose a challenge, often extending over many years and requiring sustained commitment.

Future Opportunities in North America Armored Fighting Vehicles Industry

The North America Armored Fighting Vehicles (AFVs) industry is poised for significant future opportunities driven by emerging trends and evolving defense requirements. The increasing emphasis on modularity and platform adaptability presents a substantial opportunity for manufacturers to offer versatile vehicles that can be quickly reconfigured for diverse mission sets, reducing the need for specialized fleets. Advancements in unmanned and optionally manned vehicle technologies offer the potential for highly autonomous or semi-autonomous AFVs, enhancing operational safety and efficiency. The growing demand for counter-insurgency and stability operations in various regions necessitates the development of lighter, more agile, yet highly protected AFVs. Furthermore, opportunities exist in upgrading existing vehicle fleets with advanced electronic warfare capabilities, artificial intelligence, and enhanced lethality systems, extending their operational lifespan and combat effectiveness.

- Modular and Adaptable Platforms: Focus on vehicles with reconfigurable systems for varied missions.

- Unmanned and Optionally Manned Technologies: Development of autonomous or semi-autonomous AFVs.

- Lightweight and Agile Designs: Catering to counter-insurgency and rapid deployment needs.

- Fleet Modernization Programs: Opportunities to upgrade existing vehicles with new technologies.

Major Players in the North America Armored Fighting Vehicles Industry Ecosystem

- Textron Inc

- THALES

- Oshkosh Corporation

- General Dynamics Corporation

- Rheinmetall AG

- Elbit Systems Ltd

- QinetiQ Group

- AM General LLC

- Leonardo S p A

- BAE Systems plc

- HDT Global

Key Developments in North America Armored Fighting Vehicles Industry Industry

- November 2022: BAE Systems plc was awarded a contract worth USD 32 million by the US Department of Defense (DoD) to supply M2A4 and M7A4 Bradley fighting vehicles to the US Army. These vehicles are designed to provide mechanized infantry with improved mobility, firepower, and protection. The project is slated to be completed by August 2023.

- November 2022: The Canadian military entered into a contract worth USD 165 million with the General Dynamics Corporation to acquire 39 additional light-armored vehicles. This procurement is part of Canada's effort to replace equipment previously donated to Ukraine.

Strategic North America Armored Fighting Vehicles Industry Market Forecast

The strategic forecast for the North America Armored Fighting Vehicles (AFVs) industry indicates a robust growth trajectory driven by a confluence of factors including escalating geopolitical tensions, consistent government defense investments, and rapid technological innovation. The continued emphasis on fleet modernization, coupled with the demand for enhanced survivability and networked warfare capabilities, will fuel procurement of both new platforms and upgrades of existing assets. Emerging opportunities in modular vehicle designs and the integration of artificial intelligence will also contribute significantly to market expansion. The industry is expected to witness sustained demand throughout the forecast period, with an anticipated market valuation reaching tens of billions of US Dollars, underscoring its strategic importance in maintaining national security and projecting military power across North America.

North America Armored Fighting Vehicles Industry Segmentation

-

1. Vehicle Type

- 1.1. Armored Personnel Carrier (APC)

- 1.2. Infantry Fighting Vehicle (IFV)

- 1.3. Main Battle Tank (MBT)

- 1.4. Other Vehicle Types

-

2. Geography

- 2.1. United States

- 2.2. Canada

North America Armored Fighting Vehicles Industry Segmentation By Geography

- 1. United States

- 2. Canada

North America Armored Fighting Vehicles Industry Regional Market Share

Geographic Coverage of North America Armored Fighting Vehicles Industry

North America Armored Fighting Vehicles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.18% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Armored Personnel Carrier (APC)

- 5.1.2. Infantry Fighting Vehicle (IFV)

- 5.1.3. Main Battle Tank (MBT)

- 5.1.4. Other Vehicle Types

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United States

- 5.2.2. Canada

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.3.2. Canada

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. North America Armored Fighting Vehicles Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Armored Personnel Carrier (APC)

- 6.1.2. Infantry Fighting Vehicle (IFV)

- 6.1.3. Main Battle Tank (MBT)

- 6.1.4. Other Vehicle Types

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United States

- 6.2.2. Canada

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. United States North America Armored Fighting Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Armored Personnel Carrier (APC)

- 7.1.2. Infantry Fighting Vehicle (IFV)

- 7.1.3. Main Battle Tank (MBT)

- 7.1.4. Other Vehicle Types

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United States

- 7.2.2. Canada

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Canada North America Armored Fighting Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Armored Personnel Carrier (APC)

- 8.1.2. Infantry Fighting Vehicle (IFV)

- 8.1.3. Main Battle Tank (MBT)

- 8.1.4. Other Vehicle Types

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United States

- 8.2.2. Canada

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Competitive Analysis

- 9.1. Company Profiles

- 9.1.1 Textron Inc

- 9.1.1.1. Company Overview

- 9.1.1.2. Products

- 9.1.1.3. Company Financials

- 9.1.1.4. SWOT Analysis

- 9.1.2 THALES

- 9.1.2.1. Company Overview

- 9.1.2.2. Products

- 9.1.2.3. Company Financials

- 9.1.2.4. SWOT Analysis

- 9.1.3 Oshkosh Corporation

- 9.1.3.1. Company Overview

- 9.1.3.2. Products

- 9.1.3.3. Company Financials

- 9.1.3.4. SWOT Analysis

- 9.1.4 General Dynamics Corporation

- 9.1.4.1. Company Overview

- 9.1.4.2. Products

- 9.1.4.3. Company Financials

- 9.1.4.4. SWOT Analysis

- 9.1.5 Rheinmetall AG

- 9.1.5.1. Company Overview

- 9.1.5.2. Products

- 9.1.5.3. Company Financials

- 9.1.5.4. SWOT Analysis

- 9.1.6 Elbit Systems Ltd

- 9.1.6.1. Company Overview

- 9.1.6.2. Products

- 9.1.6.3. Company Financials

- 9.1.6.4. SWOT Analysis

- 9.1.7 QinetiQ Group

- 9.1.7.1. Company Overview

- 9.1.7.2. Products

- 9.1.7.3. Company Financials

- 9.1.7.4. SWOT Analysis

- 9.1.8 AM General LLC

- 9.1.8.1. Company Overview

- 9.1.8.2. Products

- 9.1.8.3. Company Financials

- 9.1.8.4. SWOT Analysis

- 9.1.9 Leonardo S p A

- 9.1.9.1. Company Overview

- 9.1.9.2. Products

- 9.1.9.3. Company Financials

- 9.1.9.4. SWOT Analysis

- 9.1.10 BAE Systems plc

- 9.1.10.1. Company Overview

- 9.1.10.2. Products

- 9.1.10.3. Company Financials

- 9.1.10.4. SWOT Analysis

- 9.1.11 HDT Global

- 9.1.11.1. Company Overview

- 9.1.11.2. Products

- 9.1.11.3. Company Financials

- 9.1.11.4. SWOT Analysis

- 9.1.1 Textron Inc

- 9.2. Market Entropy

- 9.2.1 Company's Key Areas Served

- 9.2.2 Recent Developments

- 9.3. Company Market Share Analysis 2025

- 9.3.1 Top 5 Companies Market Share Analysis

- 9.3.2 Top 3 Companies Market Share Analysis

- 9.4. List of Potential Customers

- 10. Research Methodology

List of Figures

- Figure 1: North America Armored Fighting Vehicles Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Armored Fighting Vehicles Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 3: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 5: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 8: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 9: North America Armored Fighting Vehicles Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Armored Fighting Vehicles Industry?

The projected CAGR is approximately 5.18%.

2. Which companies are prominent players in the North America Armored Fighting Vehicles Industry?

Key companies in the market include Textron Inc, THALES, Oshkosh Corporation, General Dynamics Corporation, Rheinmetall AG, Elbit Systems Ltd, QinetiQ Group, AM General LLC, Leonardo S p A, BAE Systems plc, HDT Global.

3. What are the main segments of the North America Armored Fighting Vehicles Industry?

The market segments include Vehicle Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.51 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Main Battle Tanks Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

November 2022: BAE Systems plc was awarded a contract worth USD 32 million by the US Department of Defense (DoD) to supply M2A4 and M7A4 Bradley fighting vehicles to the US Army. These vehicles are designed to provide mechanized infantry with improved mobility, firepower, and protection. The project is slated to be completed by August 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Armored Fighting Vehicles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Armored Fighting Vehicles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Armored Fighting Vehicles Industry?

To stay informed about further developments, trends, and reports in the North America Armored Fighting Vehicles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence