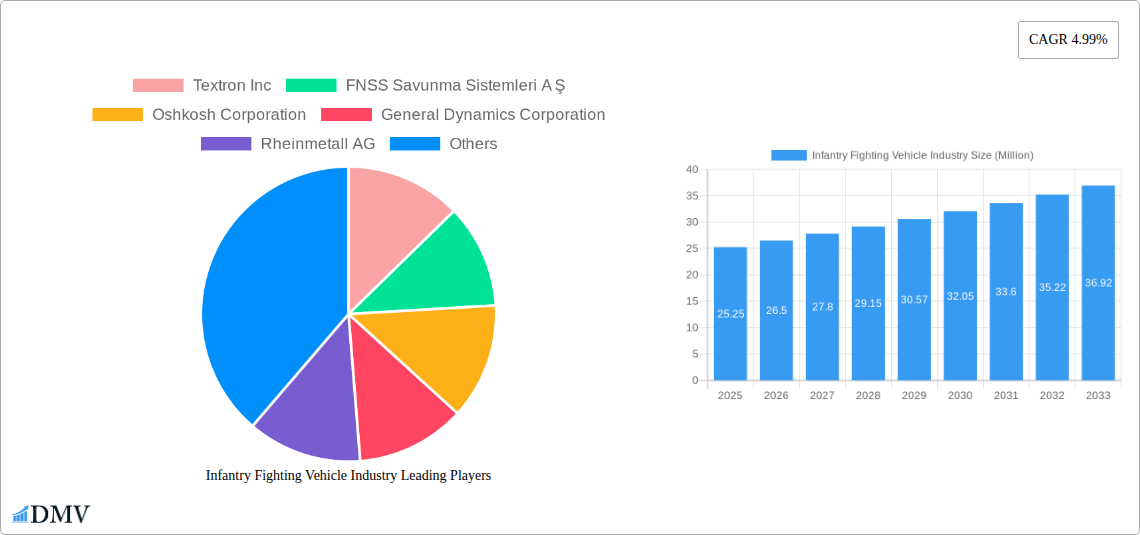

Key Insights

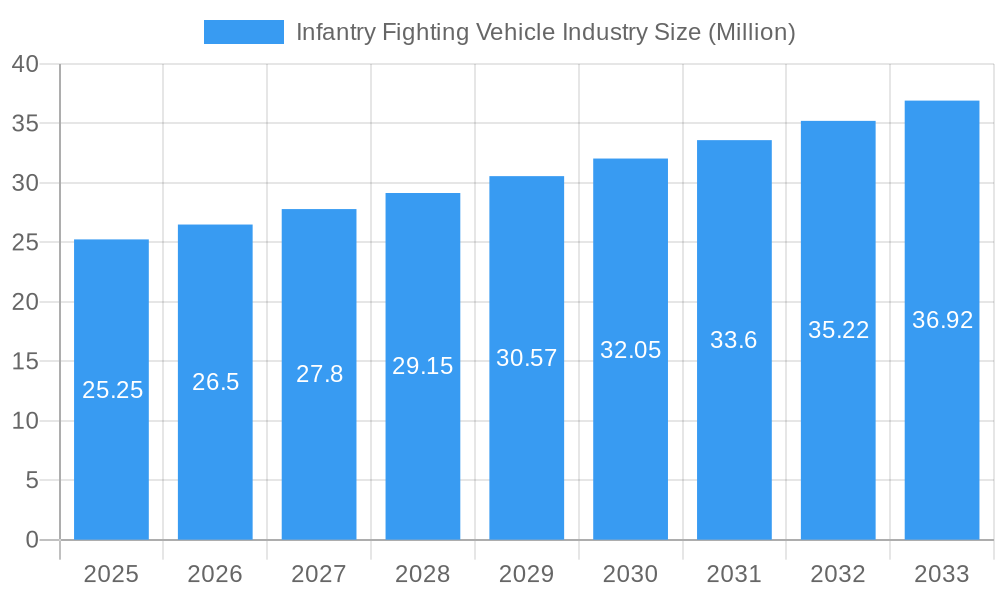

The global Infantry Fighting Vehicle (IFV) market is poised for substantial growth, driven by escalating geopolitical tensions, modernization efforts within defense forces, and the increasing demand for advanced armored protection. The market is projected to reach $25.25 million in 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.99% expected to propel it through 2033. This growth is underpinned by significant investments in next-generation armored platforms designed to enhance troop survivability and combat effectiveness in diverse operational environments. Key drivers include the persistent need to counter emerging threats, such as asymmetric warfare and sophisticated anti-tank weaponry, necessitating vehicles with superior firepower, mobility, and protection. Furthermore, the ongoing modernization of existing fleets by numerous nations, seeking to replace aging armored personnel carriers and older IFV models, is a critical factor fueling market expansion.

Infantry Fighting Vehicle Industry Market Size (In Million)

The IFV market is segmented by vehicle type, with Infantry Fighting Vehicles (IFVs) and Armored Personnel Carriers (APCs) forming the core segments, alongside growing interest in Mine-resistant Ambush Protected (MRAP) vehicles and Main Battle Tanks (MBTs) for specialized roles. Emerging markets in Asia Pacific and the Middle East and Africa are expected to be key growth engines, driven by significant defense budget allocations and regional security concerns. Prominent players like BAE Systems, General Dynamics Corporation, and Rheinmetall AG are at the forefront of innovation, developing advanced IFVs equipped with enhanced sensor suites, active protection systems, and modular designs that can be adapted to specific mission requirements. Despite the positive outlook, challenges such as high procurement costs and the lengthy development cycles for new platforms can act as restraints. However, the continuous evolution of warfare tactics and the imperative for technologically advanced, versatile armored solutions position the IFV market for sustained and significant expansion.

Infantry Fighting Vehicle Industry Company Market Share

Infantry Fighting Vehicle Industry Market Composition & Trends

This comprehensive Infantry Fighting Vehicle (IFV) industry report dissects the global market, projecting a robust expansion from approximately $25,000 Million in 2025 to over $35,000 Million by 2033, at a CAGR of xx%. The analysis delves into market concentration, identifying key players like BAE Systems plc, General Dynamics Corporation, and Rheinmetall AG who collectively hold a significant market share, estimated at around 60% of the global IFV market. Innovation catalysts are prominently explored, with a focus on advancements in modular design, active protection systems, and enhanced survivability features driving the evolution of armored personnel carriers (APC) and infantry fighting vehicles (IFV). The regulatory landscape, while complex, presents opportunities through modernization programs and defense spending across major economies. Substitute products are limited, with the core function of IFVs remaining critical for modern warfare. End-user profiles reveal a strong demand from national defense forces and paramilitary organizations, driven by geopolitical instability and the need for agile, protected ground forces. M&A activities within the historical period (2019-2024) have seen strategic consolidation, with deal values estimated to be in the range of hundreds of millions of dollars, aimed at expanding technological capabilities and market reach.

- Market Share Distribution: Key players like BAE Systems plc (estimated 15% share), General Dynamics Corporation (estimated 12%), and Rheinmetall AG (estimated 10%) dominate the market.

- M&A Deal Values: Historical M&A activities are estimated to have aggregated to over $1,500 Million, focusing on technology acquisition and market consolidation.

- Innovation Focus: Advances in active protection systems (APS), modularity for mission adaptability, and enhanced crew survivability are key innovation drivers.

- Regulatory Impact: Modernization budgets and defense procurement policies in North America and Europe significantly influence market dynamics.

Infantry Fighting Vehicle Industry Industry Evolution

The Infantry Fighting Vehicle (IFV) industry has undergone a significant transformation over the historical period (2019-2024), characterized by escalating global security concerns and a corresponding surge in defense spending. The market growth trajectory for IFVs is projected to maintain a healthy upward trend, with an estimated CAGR of xx% during the forecast period (2025-2033). This growth is underpinned by continuous technological advancements and evolving defense doctrines that prioritize modularity, survivability, and multi-role capabilities in ground combat vehicles. From the base year of 2025, the market is expected to expand significantly as nations across the globe continue to invest in modernizing their land forces.

Technological advancements have been the cornerstone of this evolution. Early iterations of IFVs focused primarily on troop transport and direct fire support. However, the current generation of IFVs integrates sophisticated active protection systems (APS) to counter threats like anti-tank guided missiles (ATGMs) and RPGs, significantly enhancing survivability. Furthermore, the integration of advanced sensor suites, networked communication systems, and artificial intelligence (AI) capabilities allows for superior situational awareness and combat effectiveness. The development of hybrid-electric powertrains is also gaining traction, offering improved operational range, reduced acoustic signature, and enhanced power generation for on-board systems.

Shifting consumer demands, interpreted as the evolving requirements of end-users (national militaries), have driven this technological push. The increasing prevalence of asymmetric warfare and urban combat scenarios has necessitated vehicles that are not only heavily armed and armored but also agile and adaptable to diverse operational environments. This has led to a greater emphasis on modular design, allowing for rapid reconfiguration of weapon systems, sensor packages, and crew configurations to suit specific mission profiles. The demand for Mine-resistant Ambush Protected (MRAP) vehicles, while a distinct segment, has also influenced the overall market by highlighting the critical need for enhanced underbody protection and survivability against IEDs and ambushes, features now being increasingly incorporated into next-generation IFVs. The adoption of wheeled IFVs over tracked variants has also seen a notable increase due to their logistical advantages and operational flexibility for certain types of missions, though tracked vehicles remain dominant in high-intensity combat scenarios. The overall market size, estimated at approximately $25,000 Million in 2025, is poised for substantial growth, reaching an estimated $35,000 Million by 2033, reflecting the continued strategic importance of these platforms in modern defense strategies.

Leading Regions, Countries, or Segments in Infantry Fighting Vehicle Industry

The global Infantry Fighting Vehicle (IFV) industry is experiencing dynamic shifts, with a clear dominance observable across specific regions and vehicle types. In terms of market share and strategic importance, the Infantry Fighting Vehicle (IFV) segment itself stands out as the leading segment, followed closely by the Armored Personnel Carrier (APC) category. These two segments collectively represent the core of modern ground warfare capabilities, driving significant investment and technological innovation within the broader armored vehicle market.

The dominance of the IFV segment is driven by its inherent versatility, combining the protective capabilities of an APC with a more potent direct-fire weapon system, typically a autocannon ranging from 25mm to 57mm. This allows IFVs to engage a wide array of battlefield threats, from enemy infantry and light armored vehicles to even some main battle tanks (MBTs) when employed effectively. Nations worldwide are prioritizing the acquisition and upgrade of IFV fleets to maintain a decisive edge in ground operations. The estimated market share for the IFV segment is approximately 45% of the total armored vehicle market, with Armored Personnel Carriers (APCs) following at around 30%. Mine-resistant Ambush Protected (MRAP) vehicles, while crucial for survivability in specific threat environments, constitute about 15% of the market, and Main Battle Tanks (MBTs) represent a smaller but highly significant 10% due to their specialized heavy armor role. Other Types, encompassing specialized variants, occupy the remaining percentage.

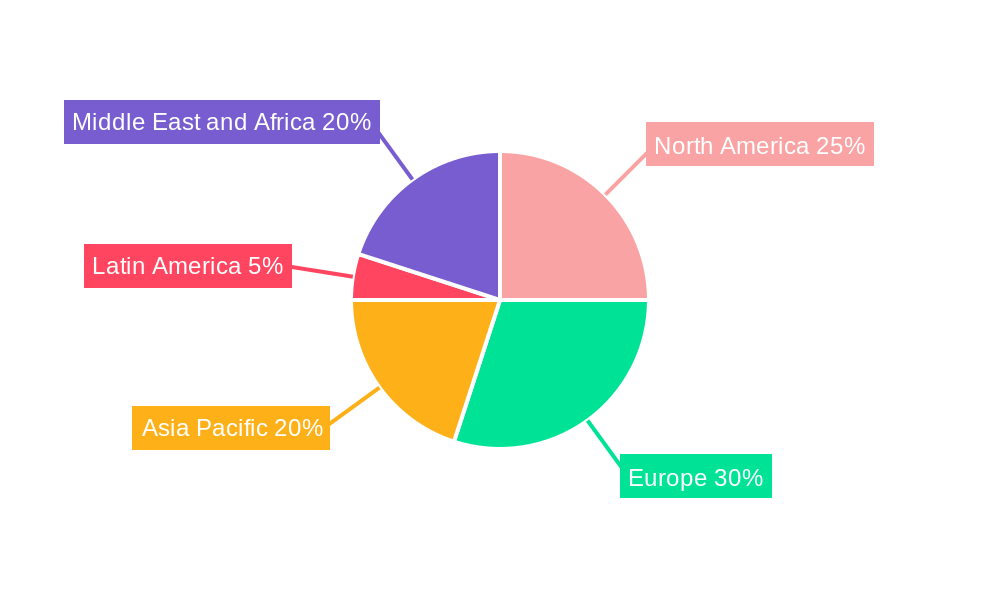

Geographically, North America and Europe collectively emerge as the leading regions for the Infantry Fighting Vehicle industry. This leadership is fueled by substantial defense budgets, ongoing modernization programs, and a sustained focus on technological superiority in land warfare. Countries like the United States, Germany, the United Kingdom, and France are major consumers and developers of advanced IFVs.

Key Drivers for IFV Segment Dominance:

- Versatile Combat Roles: Ability to perform multiple tasks including troop transport, anti-armor, reconnaissance, and fire support.

- Technological Advancements: Integration of advanced sensors, active protection systems (APS), and modular designs enhance battlefield survivability and effectiveness.

- Modernization Programs: Ongoing defense procurement and upgrade initiatives by major global powers to replace aging fleets with modern, capable IFVs.

- Geopolitical Imperatives: Rising regional conflicts and the need for robust ground forces to deter aggression and project power.

Key Drivers for North America & Europe Dominance:

- High Defense Spending: Significant annual defense budgets allocated to acquiring and developing advanced military hardware.

- Technological Leadership: Presence of leading defense manufacturers with advanced research and development capabilities.

- Strategic Alliances: Collaborative defense projects and interoperability requirements within alliances like NATO.

- Active Threat Perception: Sustained geopolitical tensions and a proactive approach to maintaining military readiness.

The continued investment in the IFV segment, coupled with the strategic focus of leading regions on land-based armored capabilities, solidifies their position as the primary drivers of the global Infantry Fighting Vehicle industry.

Infantry Fighting Vehicle Industry Product Innovations

The Infantry Fighting Vehicle (IFV) industry is witnessing rapid innovation, driven by the imperative for enhanced survivability, lethality, and operational flexibility. Product innovations are increasingly focused on integrating advanced digital architectures, enabling seamless communication and data sharing on the battlefield. The development of modular designs allows for rapid mission-specific configurations, incorporating different weapon stations, sensor packages, and protective systems. Next-generation IFVs are featuring advanced active protection systems (APS) capable of detecting, tracking, and neutralizing incoming threats like ATGMs and RPGs in milliseconds, significantly boosting crew survivability. Furthermore, the integration of AI-powered targeting systems and autonomous capabilities is enhancing engagement accuracy and reducing crew workload. Performance metrics are seeing improvements in terms of mobility across varied terrains, reduced acoustic signatures for stealthier operations, and enhanced power generation for sophisticated on-board electronics. Unique selling propositions include the ability to operate in highly contested environments, provide persistent reconnaissance, and offer decisive fire support, all while minimizing crew exposure to enemy fire.

Propelling Factors for Infantry Fighting Vehicle Industry Growth

The Infantry Fighting Vehicle (IFV) industry's growth is propelled by a confluence of critical factors. Geopolitical instability and the resurgence of territorial defense concerns across various regions are driving increased defense spending, leading to the modernization and expansion of armored vehicle fleets. Technological advancements, particularly in areas like active protection systems, modular design, and digital battlefield integration, are creating demand for next-generation IFVs, pushing manufacturers to innovate and upgrade existing platforms. Government initiatives and defense procurement programs, aimed at enhancing national security and maintaining a technological edge, are providing sustained market impetus. Furthermore, the growing emphasis on network-centric warfare and the need for interoperable platforms within allied forces are spurring the development and adoption of advanced IFVs that can seamlessly integrate into joint operations.

Obstacles in the Infantry Fighting Vehicle Industry Market

Despite robust growth prospects, the Infantry Fighting Vehicle (IFV) industry faces significant obstacles. The high cost of research, development, and procurement of advanced IFVs presents a substantial financial burden for many nations, leading to prolonged procurement cycles and potential budget constraints. Stringent regulatory requirements and lengthy certification processes for military hardware can also impede market entry and product deployment. Global supply chain disruptions, particularly for specialized components and raw materials, can impact production timelines and increase manufacturing costs. Moreover, the increasing complexity of IFV systems necessitates highly skilled personnel for operation and maintenance, posing a challenge for armed forces with limited training resources. Intense competition among established defense contractors and emerging players also creates pressure on pricing and market share.

Future Opportunities in Infantry Fighting Vehicle Industry

The future of the Infantry Fighting Vehicle (IFV) industry is rife with opportunities for growth and innovation. The increasing adoption of modular design principles will allow for greater platform versatility and adaptability to a wider range of mission requirements, including urban warfare and peacekeeping operations. The integration of artificial intelligence (AI) and unmanned systems promises to enhance battlefield awareness, automate complex tasks, and improve crew safety. Emerging markets in Asia-Pacific and the Middle East, driven by regional security concerns and modernization efforts, represent significant untapped potential for IFV sales. Furthermore, the development of hybrid-electric and potentially fully electric IFVs offers opportunities for reduced logistical footprints, enhanced stealth capabilities, and lower operational costs. The ongoing evolution of threats also necessitates continuous upgrades to existing fleets, providing a steady stream of aftermarket services and modernization contracts.

Major Players in the Infantry Fighting Vehicle Industry Ecosystem

- Textron Inc

- FNSS Savunma Sistemleri A Ş

- Oshkosh Corporation

- General Dynamics Corporation

- Rheinmetall AG

- Elbit Systems Ltd

- Patria Group

- Denel SOC Ltd

- Saudi Arabian Military Industries (SAMI)

- Nexter Group

- BMC Otomotiv Sanayi ve Ticarest AS

- BAE Systems plc

- Hanwha Corporation

- Mitsubishi Heavy Industries Ltd

Key Developments in Infantry Fighting Vehicle Industry Industry

- March 2023: Australian and German officials signed an agreement to cooperate on the procurement of new combat reconnaissance vehicles, based on the Boxer family of armored fighting vehicles and equipped with a 30-millimeter gun. The deliveries will start in 2025, indicating a significant collaborative procurement effort and the growing importance of advanced wheeled platforms like the Boxer.

- December 2022: Japan selected Patria-built armored modular vehicles (AMV) to replace the Type-96 8X8 wheeled armored personnel carriers of the Japan Ground Self-Defense Force. This selection highlights the increasing preference for modular, wheeled armored vehicles in modern defense forces and demonstrates Patria Group's significant contribution to the IFV market.

Strategic Infantry Fighting Vehicle Industry Market Forecast

The strategic Infantry Fighting Vehicle (IFV) industry forecast anticipates sustained growth, driven by a robust demand for advanced armored platforms. Geopolitical tensions and evolving defense doctrines worldwide are compelling nations to invest in modernizing their land forces, directly translating into increased procurement of IFVs. Technological advancements in areas such as active protection systems, modularity, and digital integration are not only enhancing the capabilities of these vehicles but also creating opportunities for manufacturers to differentiate their offerings. Emerging markets present significant potential, while established players continue to benefit from ongoing modernization programs. The market is poised for expansion, with a projected increase in value driven by the critical role IFVs play in contemporary ground warfare.

Infantry Fighting Vehicle Industry Segmentation

-

1. Type

- 1.1. Armored Personnel Carrier (APC)

- 1.2. Infantry Fighting Vehicle (IFV)

- 1.3. Mine-resistant Ambush Protected (MRAP)

- 1.4. Main Battle Tank (MBT)

- 1.5. Other Types

Infantry Fighting Vehicle Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Rest of Latin America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. United Arab Emirates

- 5.3. Turkey

- 5.4. Rest of Middle East and Africa

Infantry Fighting Vehicle Industry Regional Market Share

Geographic Coverage of Infantry Fighting Vehicle Industry

Infantry Fighting Vehicle Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.99% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Armored Personnel Carrier (APC)

- 5.1.2. Infantry Fighting Vehicle (IFV)

- 5.1.3. Mine-resistant Ambush Protected (MRAP)

- 5.1.4. Main Battle Tank (MBT)

- 5.1.5. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Infantry Fighting Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Armored Personnel Carrier (APC)

- 6.1.2. Infantry Fighting Vehicle (IFV)

- 6.1.3. Mine-resistant Ambush Protected (MRAP)

- 6.1.4. Main Battle Tank (MBT)

- 6.1.5. Other Types

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Infantry Fighting Vehicle Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Armored Personnel Carrier (APC)

- 7.1.2. Infantry Fighting Vehicle (IFV)

- 7.1.3. Mine-resistant Ambush Protected (MRAP)

- 7.1.4. Main Battle Tank (MBT)

- 7.1.5. Other Types

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Infantry Fighting Vehicle Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Armored Personnel Carrier (APC)

- 8.1.2. Infantry Fighting Vehicle (IFV)

- 8.1.3. Mine-resistant Ambush Protected (MRAP)

- 8.1.4. Main Battle Tank (MBT)

- 8.1.5. Other Types

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Infantry Fighting Vehicle Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Armored Personnel Carrier (APC)

- 9.1.2. Infantry Fighting Vehicle (IFV)

- 9.1.3. Mine-resistant Ambush Protected (MRAP)

- 9.1.4. Main Battle Tank (MBT)

- 9.1.5. Other Types

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Infantry Fighting Vehicle Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Armored Personnel Carrier (APC)

- 10.1.2. Infantry Fighting Vehicle (IFV)

- 10.1.3. Mine-resistant Ambush Protected (MRAP)

- 10.1.4. Main Battle Tank (MBT)

- 10.1.5. Other Types

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Infantry Fighting Vehicle Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Armored Personnel Carrier (APC)

- 11.1.2. Infantry Fighting Vehicle (IFV)

- 11.1.3. Mine-resistant Ambush Protected (MRAP)

- 11.1.4. Main Battle Tank (MBT)

- 11.1.5. Other Types

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Textron Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FNSS Savunma Sistemleri A Ş

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Oshkosh Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 General Dynamics Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rheinmetall AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Elbit Systems Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Patria Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Denel SOC Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Saudi Arabian Military Industries (SAMI)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nexter Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 BMC Otomotiv Sanayi ve Ticarest AS

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 BAE Systems plc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Hanwha Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Mitsubishi Heavy Industries Ltd

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Textron Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Infantry Fighting Vehicle Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Infantry Fighting Vehicle Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Infantry Fighting Vehicle Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Infantry Fighting Vehicle Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Infantry Fighting Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Infantry Fighting Vehicle Industry Revenue (Million), by Type 2025 & 2033

- Figure 7: Europe Infantry Fighting Vehicle Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: Europe Infantry Fighting Vehicle Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Infantry Fighting Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Infantry Fighting Vehicle Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Asia Pacific Infantry Fighting Vehicle Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Asia Pacific Infantry Fighting Vehicle Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Infantry Fighting Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Infantry Fighting Vehicle Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Latin America Infantry Fighting Vehicle Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Latin America Infantry Fighting Vehicle Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Latin America Infantry Fighting Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Infantry Fighting Vehicle Industry Revenue (Million), by Type 2025 & 2033

- Figure 19: Middle East and Africa Infantry Fighting Vehicle Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Middle East and Africa Infantry Fighting Vehicle Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Middle East and Africa Infantry Fighting Vehicle Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: France Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Germany Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Russia Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Europe Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 15: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: China Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: India Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Japan Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: South Korea Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Asia Pacific Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 22: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: Brazil Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Rest of Latin America Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 26: Global Infantry Fighting Vehicle Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 27: Saudi Arabia Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Arab Emirates Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Turkey Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Middle East and Africa Infantry Fighting Vehicle Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Infantry Fighting Vehicle Industry?

The projected CAGR is approximately 4.99%.

2. Which companies are prominent players in the Infantry Fighting Vehicle Industry?

Key companies in the market include Textron Inc, FNSS Savunma Sistemleri A Ş, Oshkosh Corporation, General Dynamics Corporation, Rheinmetall AG, Elbit Systems Ltd, Patria Group, Denel SOC Ltd, Saudi Arabian Military Industries (SAMI), Nexter Group, BMC Otomotiv Sanayi ve Ticarest AS, BAE Systems plc, Hanwha Corporation, Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the Infantry Fighting Vehicle Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.25 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Infantry Fighting Vehicle (IFV) to Dominate Market Share.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

March 2023: Australian and German officials signed an agreement to cooperate on the procurement of the new combat reconnaissance vehicles, based on the Boxer family of armored fighting vehicles and equipped with a 30-millimeter gun. The deliveries will start in 2025.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Infantry Fighting Vehicle Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Infantry Fighting Vehicle Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Infantry Fighting Vehicle Industry?

To stay informed about further developments, trends, and reports in the Infantry Fighting Vehicle Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence