Key Insights

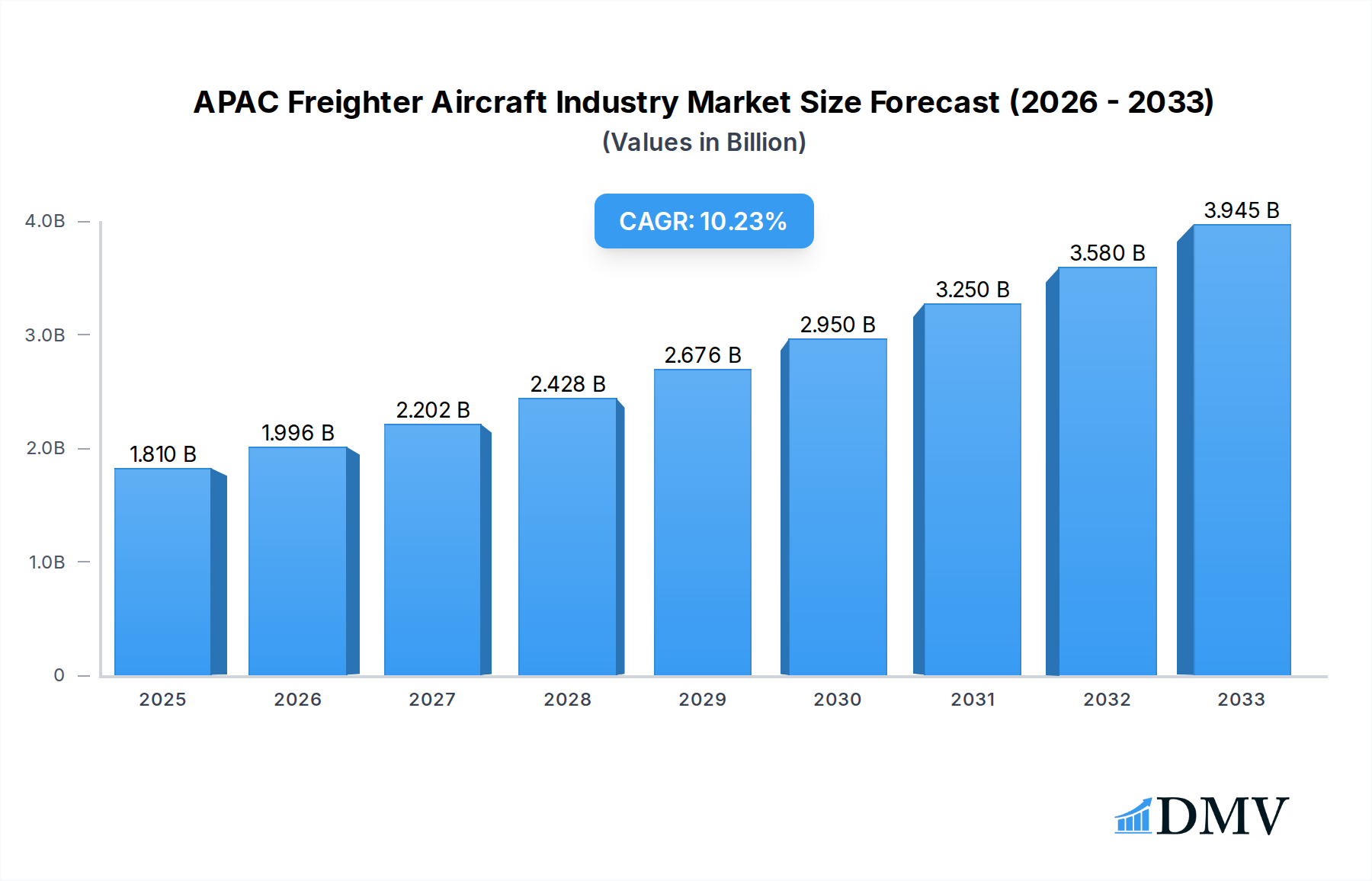

The APAC Freighter Aircraft Industry is poised for substantial growth, projected to reach a market size of 1.81 Billion by 2025, with a remarkable Compound Annual Growth Rate (CAGR) of 10.25% through 2033. This robust expansion is primarily driven by the burgeoning e-commerce sector across the region, demanding increased air cargo capacity to facilitate swift deliveries. Furthermore, the growing manufacturing and export-oriented economies in nations like China, India, and Southeast Asian countries are fueling the need for efficient air freight solutions. The increasing demand for dedicated cargo aircraft, coupled with the strategic conversion of existing passenger aircraft into freighters, highlights the industry's adaptability. Key players are investing in advanced freighter models and expanding their operational capabilities to cater to this escalating demand.

APAC Freighter Aircraft Industry Market Size (In Billion)

The market segmentation reveals a strong preference for turbofan engines due to their power and efficiency in cargo operations, although turboprop aircraft continue to serve niche markets. Geographically, China, India, and Japan are emerging as major hubs for freighter aircraft operations, driven by their extensive trade networks and expanding logistics infrastructure. While the region benefits from significant growth drivers, potential restraints such as fluctuating fuel prices, geopolitical uncertainties, and the need for significant capital investment in fleet modernization could pose challenges. However, the overall outlook remains exceptionally positive, with a consistent upward trajectory anticipated for the APAC freighter aircraft market over the forecast period.

APAC Freighter Aircraft Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the APAC Freighter Aircraft Industry, providing crucial insights into market dynamics, growth trajectories, and future opportunities. Covering a study period from 2019 to 2033, with a base year of 2025, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving landscape of air cargo transportation in the Asia-Pacific region.

APAC Freighter Aircraft Industry Market Composition & Trends

The APAC Freighter Aircraft Industry is characterized by a dynamic market composition, shaped by robust demand for dedicated cargo aircraft and the increasing adoption of derivative of non-cargo aircraft conversions. Market concentration is influenced by the presence of major global players like The Boeing Company and Airbus SE, alongside significant regional contributors such as the Aviation Industry Corporation of China and Singapore Technologies Engineering Ltd. Innovation is primarily driven by advancements in turbofan and turboprop engine technology, enhancing fuel efficiency and payload capacity. The regulatory landscape, while evolving, generally supports fleet expansion and modernization, particularly in key markets like China and India. Substitute products, primarily older freighter models and the expansion of sea and land freight, are closely monitored, but the speed and efficiency of air cargo continue to secure its market position. End-user profiles range from global e-commerce giants and express delivery services to traditional logistics providers and manufacturing firms requiring just-in-time delivery. Merger and acquisition (M&A) activities, though not always publicly disclosed for all segments, are anticipated to continue as companies seek to expand their operational reach and technological capabilities. For instance, the ongoing trend of passenger-to-freighter conversions signifies strategic moves to optimize fleet utilization and respond to market demands, with deal values often significant in the multi-million dollar range for aircraft acquisitions and conversion programs. The market share distribution sees a balanced, yet competitive, landscape with dedicated cargo aircraft holding a substantial portion, while converted freighters are rapidly gaining ground due to their cost-effectiveness.

APAC Freighter Aircraft Industry Industry Evolution

The APAC Freighter Aircraft Industry has undergone a significant evolution, driven by a confluence of technological advancements, shifting economic landscapes, and the burgeoning demand for efficient air cargo solutions across the vast Asia-Pacific region. Over the historical period (2019–2024), the industry witnessed a steady expansion, fueled by the growth of e-commerce, the expansion of manufacturing hubs, and increasing inter-regional trade. The base year (2025) serves as a crucial pivot, reflecting a market poised for accelerated growth. The forecast period (2025–2033) is projected to see robust expansion, with an estimated Compound Annual Growth Rate (CAGR) of xx% in terms of revenue and xx% in terms of fleet numbers. Technological advancements have been a primary catalyst, with a focus on improving fuel efficiency, increasing payload capacity, and enhancing the operational lifespan of aircraft. The development of more advanced turbofan engines by manufacturers like The Boeing Company and Airbus SE has led to significant improvements in speed and range, while innovations in turboprop technology, championed by companies like ATR, have made regional cargo routes more viable and cost-effective. The rise of freighter conversion programs, transforming passenger aircraft into dedicated cargo carriers, has been a pivotal development. This strategy allows for a quicker and more economical way to expand cargo capacity compared to the production of new dedicated freighters. Companies like Guangzhou Aircraft Maintenance Engineering Company Limited (GAMECO) and Israel Aerospace Industries Ltd are at the forefront of these conversion technologies. Shifting consumer demands, particularly the explosion of online retail and the need for faster delivery times, have placed immense pressure on air cargo logistics. This has led to an increased demand for specialized freighter aircraft, including medium-sized and large wide-body freighters, as well as the adaptation of smaller aircraft for niche cargo operations. The strategic importance of air cargo in supporting global supply chains has been further highlighted by recent geopolitical events and the need for rapid and reliable transportation of goods. Adoption metrics for new freighter aircraft and conversion slots are consistently high, indicating strong market confidence. The market's trajectory is also influenced by the increasing focus on sustainability, driving demand for more fuel-efficient aircraft and operational practices.

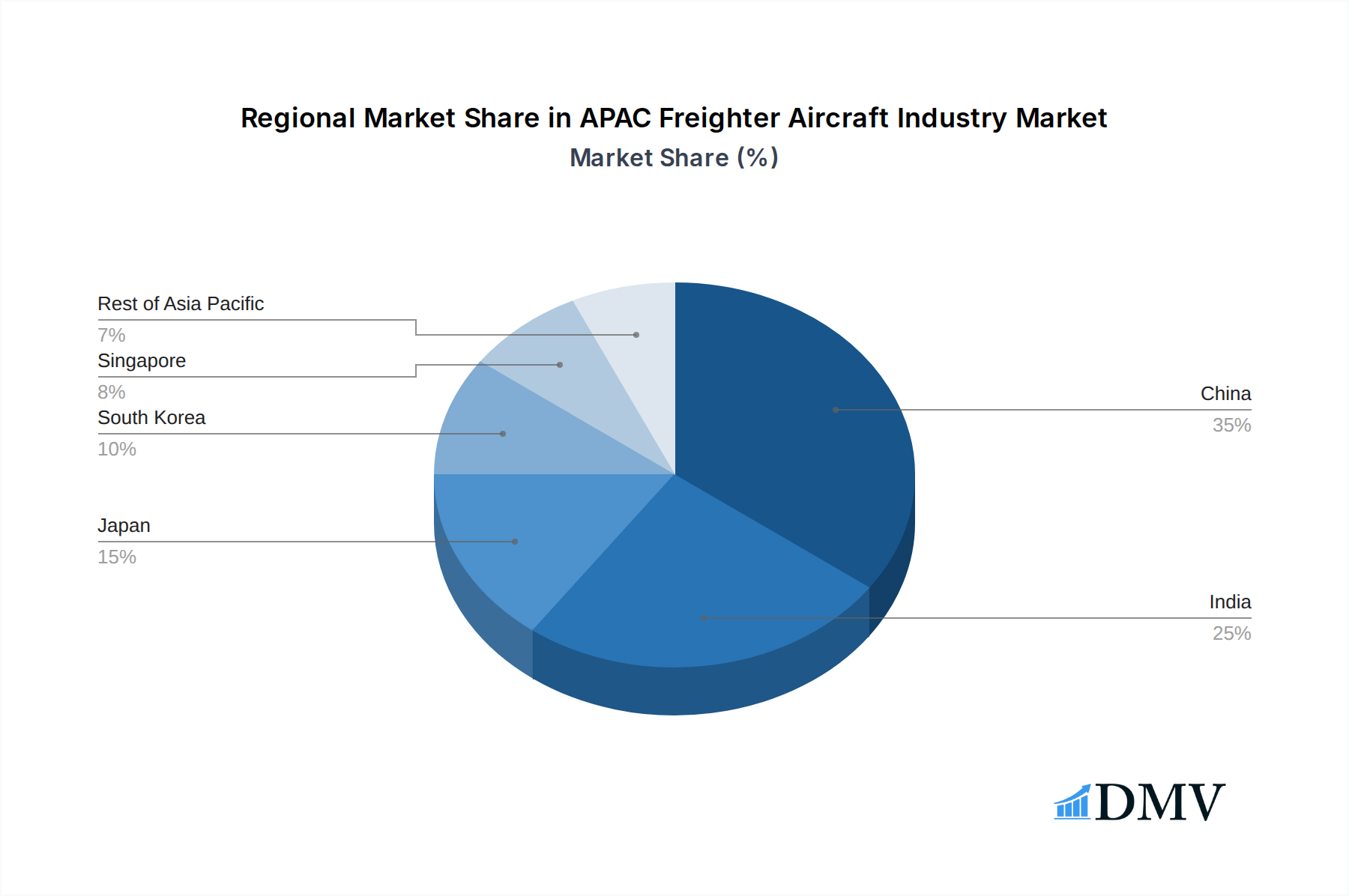

Leading Regions, Countries, or Segments in APAC Freighter Aircraft Industry

The APAC Freighter Aircraft Industry is characterized by distinct regional strengths and segment dominance, with China emerging as a powerhouse, driving significant growth across various facets of the market.

Dominant Geography: China

- Market Size & Growth: China's vast domestic market, coupled with its pivotal role in global manufacturing and trade, positions it as the leading geographical segment. The country's e-commerce boom and the rapid expansion of its logistics infrastructure have created an insatiable demand for freighter aircraft. The Rest of Asia-Pacific also contributes significantly, with India and South Korea showing substantial growth potential.

- Investment Trends: Massive government investment in aviation infrastructure, including new airports and air cargo hubs, coupled with substantial private sector investment in airlines and logistics, underpins China's dominance. This includes significant capital deployed by entities associated with the Aviation Industry Corporation of China.

- Regulatory Support: Favorable government policies promoting air cargo development, tax incentives for aircraft acquisition and operations, and streamlined customs procedures provide a conducive environment for market expansion.

Dominant Aircraft Type: Derivative of Non-Cargo Aircraft

- Cost-Effectiveness & Availability: The conversion of existing passenger aircraft into freighters offers a compelling value proposition, providing a faster and more economical way to increase cargo capacity compared to building new dedicated freighters. This segment is projected to experience substantial growth due to the readily available pool of passenger aircraft suitable for conversion.

- Key Players & Technology: Companies like Precision Aircraft Solution, Israel Aerospace Industries Ltd, and Singapore Technologies Engineering Ltd are key players in the freighter conversion market, offering specialized expertise and innovative conversion technologies. The Boeing Company’s Boeing Converted Freighters (BCF) program is also a significant contributor.

- Market Demand: The growing demand from e-commerce logistics and express delivery services, which often require flexible and rapidly deployable cargo capacity, further fuels the demand for these converted freighters.

Dominant Engine Type: Turbofan

- Performance & Range: Turbofan engines, known for their high thrust, speed, and efficiency over long ranges, remain the preferred choice for larger freighter aircraft and long-haul cargo routes. Major manufacturers like The Boeing Company and Airbus SE heavily rely on advanced turbofan technology for their freighter offerings.

- Technological Advancements: Continuous improvements in turbofan engine technology, focusing on fuel burn reduction, noise abatement, and emissions control, enhance the operational economics and environmental sustainability of freighter operations, making them increasingly attractive.

- Market Penetration: While turboprops have their niche, turbofan-powered freighters dominate the long-haul and high-volume cargo segments, which are critical to the overall growth and structure of the APAC freighter market.

The synergistic interplay between China's robust market demand, the strategic advantage of derivative freighters, and the performance capabilities of turbofan engines creates a powerful growth engine for the APAC Freighter Aircraft Industry. While India shows immense potential, particularly with initiatives like The Boeing Company's freighter conversion facility, and Japan and South Korea contribute with their advanced aviation sectors, China's scale and strategic importance currently place it at the forefront of this dynamic market.

APAC Freighter Aircraft Industry Product Innovations

Product innovation in the APAC Freighter Aircraft Industry is primarily focused on enhancing efficiency, increasing payload capacity, and expanding operational versatility. The development of advanced Boeing Converted Freighters (BCF), such as the Boeing B737-800BCF, represents a significant innovation, effectively transforming existing passenger aircraft into cost-efficient cargo solutions. These conversions offer improved cargo volume and payload, with performance metrics rivaling some dedicated freighters. Similarly, advancements in turboprop technology by manufacturers like ATR are yielding more fuel-efficient and capable regional freighters, suitable for operating from shorter runways and serving less developed airfields. Innovations also extend to cargo handling systems, optimizing loading and unloading times, thereby increasing aircraft utilization. The performance metrics of these innovations are measured by increased tonnes per kilometer, reduced fuel consumption per flight hour, and extended aircraft service life.

Propelling Factors for APAC Freighter Aircraft Industry Growth

Several key factors are propelling the growth of the APAC Freighter Aircraft Industry. The relentless surge in e-commerce, creating unprecedented demand for rapid delivery services, is a primary driver. Government initiatives supporting aviation infrastructure development and air cargo logistics, particularly in China and India, are creating a conducive environment for expansion. Technological advancements, such as the development of fuel-efficient turbofan engines and the highly successful passenger-to-freighter conversion programs offered by companies like The Boeing Company and Precision Aircraft Solution, are enhancing operational economics. Furthermore, the strategic importance of air cargo in bolstering global supply chains and facilitating international trade ensures sustained demand. The growing manufacturing base across the region also necessitates efficient air freight solutions for timely delivery of components and finished goods.

Obstacles in the APAC Freighter Aircraft Industry Market

Despite its strong growth trajectory, the APAC Freighter Aircraft Industry faces several obstacles. Regulatory complexities and varying standards across different APAC nations can hinder seamless cross-border operations and fleet expansion. Supply chain disruptions, as witnessed in recent global events, can impact aircraft production, maintenance, and the availability of spare parts, leading to delays and increased costs. Intense competition among established players like Airbus SE and The Boeing Company, alongside a growing number of regional conversion specialists, can put pressure on pricing and profit margins. Furthermore, rising fuel prices and increasing environmental regulations present ongoing challenges, necessitating continuous investment in fuel-efficient technologies and sustainable operational practices. The limited availability of skilled personnel for aircraft maintenance and operations also poses a potential bottleneck.

Future Opportunities in APAC Freighter Aircraft Industry

The APAC Freighter Aircraft Industry is ripe with future opportunities. The ongoing expansion of e-commerce into less developed regions within APAC presents a significant untapped market for regional freighters and cargo conversion services. Advancements in electric and hybrid-electric propulsion technologies for aircraft, while still in their nascent stages, promise to revolutionize cargo operations with enhanced sustainability and potentially lower operating costs. The increasing demand for specialized cargo, such as pharmaceuticals and temperature-sensitive goods, will drive the need for advanced freighter aircraft with sophisticated climate control systems. Furthermore, the potential for increased trade between APAC nations and other global economic blocs, coupled with the continued growth of the "Belt and Road Initiative," will further boost demand for efficient air cargo solutions, creating opportunities for fleet expansion and new service offerings.

Major Players in the APAC Freighter Aircraft Industry Ecosystem

- Textron Inc

- Airbus SE

- Guangzhou Aircraft Maintenance Engineering Company Limited (GAMECO)

- Aviation Industry Corporation of China

- Israel Aerospace Industries Ltd

- ATR

- Singapore Technologies Engineering Ltd

- KF Aerospace

- Precision Aircraft Solution

- The Boeing Company

Key Developments in APAC Freighter Aircraft Industry Industry

- April 2023: AerCap Holdings N.V. signed lease agreements for two Boeing B737-800BCF (Boeing Converted Freighters) with the newly launched cargo airline PT Rusky Aero Indonesia. The Indonesian carrier, Raindo United Services, will utilize these new Boeing freighters, signaling expansion in Southeast Asian cargo operations.

- March 2023: The Boeing Company announced its plans to establish a facility in India dedicated to converting Boeing B737 passenger planes into freighters. This initiative, a collaboration with GMR Aero Technic, aims to meet the increasing regional and global demand for freighter conversion services and signifies a strategic investment in India's growing aviation sector.

Strategic APAC Freighter Aircraft Industry Market Forecast

The strategic APAC Freighter Aircraft Industry market forecast indicates a robust growth trajectory, primarily fueled by the escalating demand from e-commerce and the increasing imperative for efficient global supply chain integration. The continued success of passenger-to-freighter conversion programs, exemplified by The Boeing Company's initiatives in India, will remain a key growth catalyst, offering cost-effective capacity expansion. Advancements in turbofan and turboprop engine technology will further enhance operational efficiency and sustainability, attracting further investment. Emerging markets within the Rest of Asia-Pacific present significant opportunities for fleet expansion and the development of specialized cargo services. The market's ability to adapt to evolving regulatory landscapes and embrace technological innovation will be crucial for sustained growth and capitalizing on the vast potential of the region's air cargo future.

APAC Freighter Aircraft Industry Segmentation

-

1. Aircraft Type

- 1.1. Dedicated Cargo Aircraft

- 1.2. Derivative of Non-Cargo Aircraft

-

2. Engine Type

- 2.1. Turboprop

- 2.2. Turbofan

-

3. Geography

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Singapore

- 3.6. Rest of Asia-Pacific

APAC Freighter Aircraft Industry Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. South Korea

- 5. Singapore

- 6. Rest of Asia Pacific

APAC Freighter Aircraft Industry Regional Market Share

Geographic Coverage of APAC Freighter Aircraft Industry

APAC Freighter Aircraft Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Dedicated Cargo Aircraft

- 5.1.2. Derivative of Non-Cargo Aircraft

- 5.2. Market Analysis, Insights and Forecast - by Engine Type

- 5.2.1. Turboprop

- 5.2.2. Turbofan

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. South Korea

- 5.3.5. Singapore

- 5.3.6. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. India

- 5.4.3. Japan

- 5.4.4. South Korea

- 5.4.5. Singapore

- 5.4.6. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. Global APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Dedicated Cargo Aircraft

- 6.1.2. Derivative of Non-Cargo Aircraft

- 6.2. Market Analysis, Insights and Forecast - by Engine Type

- 6.2.1. Turboprop

- 6.2.2. Turbofan

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. India

- 6.3.3. Japan

- 6.3.4. South Korea

- 6.3.5. Singapore

- 6.3.6. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. China APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.1.1. Dedicated Cargo Aircraft

- 7.1.2. Derivative of Non-Cargo Aircraft

- 7.2. Market Analysis, Insights and Forecast - by Engine Type

- 7.2.1. Turboprop

- 7.2.2. Turbofan

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. India

- 7.3.3. Japan

- 7.3.4. South Korea

- 7.3.5. Singapore

- 7.3.6. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8. India APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.1.1. Dedicated Cargo Aircraft

- 8.1.2. Derivative of Non-Cargo Aircraft

- 8.2. Market Analysis, Insights and Forecast - by Engine Type

- 8.2.1. Turboprop

- 8.2.2. Turbofan

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. India

- 8.3.3. Japan

- 8.3.4. South Korea

- 8.3.5. Singapore

- 8.3.6. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9. Japan APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.1.1. Dedicated Cargo Aircraft

- 9.1.2. Derivative of Non-Cargo Aircraft

- 9.2. Market Analysis, Insights and Forecast - by Engine Type

- 9.2.1. Turboprop

- 9.2.2. Turbofan

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. India

- 9.3.3. Japan

- 9.3.4. South Korea

- 9.3.5. Singapore

- 9.3.6. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10. South Korea APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10.1.1. Dedicated Cargo Aircraft

- 10.1.2. Derivative of Non-Cargo Aircraft

- 10.2. Market Analysis, Insights and Forecast - by Engine Type

- 10.2.1. Turboprop

- 10.2.2. Turbofan

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. China

- 10.3.2. India

- 10.3.3. Japan

- 10.3.4. South Korea

- 10.3.5. Singapore

- 10.3.6. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11. Singapore APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11.1.1. Dedicated Cargo Aircraft

- 11.1.2. Derivative of Non-Cargo Aircraft

- 11.2. Market Analysis, Insights and Forecast - by Engine Type

- 11.2.1. Turboprop

- 11.2.2. Turbofan

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. China

- 11.3.2. India

- 11.3.3. Japan

- 11.3.4. South Korea

- 11.3.5. Singapore

- 11.3.6. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 12. Rest of Asia Pacific APAC Freighter Aircraft Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 12.1.1. Dedicated Cargo Aircraft

- 12.1.2. Derivative of Non-Cargo Aircraft

- 12.2. Market Analysis, Insights and Forecast - by Engine Type

- 12.2.1. Turboprop

- 12.2.2. Turbofan

- 12.3. Market Analysis, Insights and Forecast - by Geography

- 12.3.1. China

- 12.3.2. India

- 12.3.3. Japan

- 12.3.4. South Korea

- 12.3.5. Singapore

- 12.3.6. Rest of Asia-Pacific

- 12.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Textron Inc

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Airbus SE

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Guangzhou Aircraft Maintenance Engineering Company Limited (GAMECO)

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Aviation Industry Corporation of China

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Israel Aerospace Industries Ltd

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 ATR

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Singapore Technologies Engineering Ltd

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 KF Aerospace

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Precision Aircraft Solution

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 The Boeing Company

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Textron Inc

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global APAC Freighter Aircraft Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: China APAC Freighter Aircraft Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 3: China APAC Freighter Aircraft Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 4: China APAC Freighter Aircraft Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 5: China APAC Freighter Aircraft Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 6: China APAC Freighter Aircraft Industry Revenue (Million), by Geography 2025 & 2033

- Figure 7: China APAC Freighter Aircraft Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: China APAC Freighter Aircraft Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: China APAC Freighter Aircraft Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: India APAC Freighter Aircraft Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 11: India APAC Freighter Aircraft Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 12: India APAC Freighter Aircraft Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 13: India APAC Freighter Aircraft Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 14: India APAC Freighter Aircraft Industry Revenue (Million), by Geography 2025 & 2033

- Figure 15: India APAC Freighter Aircraft Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: India APAC Freighter Aircraft Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: India APAC Freighter Aircraft Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Japan APAC Freighter Aircraft Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 19: Japan APAC Freighter Aircraft Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 20: Japan APAC Freighter Aircraft Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 21: Japan APAC Freighter Aircraft Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 22: Japan APAC Freighter Aircraft Industry Revenue (Million), by Geography 2025 & 2033

- Figure 23: Japan APAC Freighter Aircraft Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Japan APAC Freighter Aircraft Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Japan APAC Freighter Aircraft Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South Korea APAC Freighter Aircraft Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 27: South Korea APAC Freighter Aircraft Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 28: South Korea APAC Freighter Aircraft Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 29: South Korea APAC Freighter Aircraft Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 30: South Korea APAC Freighter Aircraft Industry Revenue (Million), by Geography 2025 & 2033

- Figure 31: South Korea APAC Freighter Aircraft Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 32: South Korea APAC Freighter Aircraft Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: South Korea APAC Freighter Aircraft Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Singapore APAC Freighter Aircraft Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 35: Singapore APAC Freighter Aircraft Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 36: Singapore APAC Freighter Aircraft Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 37: Singapore APAC Freighter Aircraft Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 38: Singapore APAC Freighter Aircraft Industry Revenue (Million), by Geography 2025 & 2033

- Figure 39: Singapore APAC Freighter Aircraft Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 40: Singapore APAC Freighter Aircraft Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Singapore APAC Freighter Aircraft Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 43: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 44: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 45: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 46: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue (Million), by Geography 2025 & 2033

- Figure 47: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 48: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Rest of Asia Pacific APAC Freighter Aircraft Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 2: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 3: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 6: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 7: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 10: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 11: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 14: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 15: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 18: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 19: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 20: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 22: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 23: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 24: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 26: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 27: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 28: Global APAC Freighter Aircraft Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Freighter Aircraft Industry?

The projected CAGR is approximately 10.25%.

2. Which companies are prominent players in the APAC Freighter Aircraft Industry?

Key companies in the market include Textron Inc, Airbus SE, Guangzhou Aircraft Maintenance Engineering Company Limited (GAMECO), Aviation Industry Corporation of China, Israel Aerospace Industries Ltd, ATR, Singapore Technologies Engineering Ltd, KF Aerospace, Precision Aircraft Solution, The Boeing Company.

3. What are the main segments of the APAC Freighter Aircraft Industry?

The market segments include Aircraft Type, Engine Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.81 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Derivative of Non-Cargo Aircraft Segment Will Showcase Significant Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

April 2023: AerCap Holdings N.V. signed lease agreements for two Boeing B737-800BCF (Boeing Converted Freighters) with the newly launched cargo airline PT Rusky Aero Indonesia. The Indonesian carrier, Raindo United Services, will utilize these new Boeing freighters."

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Freighter Aircraft Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Freighter Aircraft Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Freighter Aircraft Industry?

To stay informed about further developments, trends, and reports in the APAC Freighter Aircraft Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence