Key Insights

The global Mobile Satellite Communication System market is poised for significant expansion, projected to reach an estimated market size of approximately $25,000 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of around 12% projected through 2033. This growth is largely fueled by increasing demand for reliable and pervasive connectivity across remote and underserved regions, critical for both government and defense operations, as well as burgeoning commercial applications. Key drivers include the escalating need for real-time data transmission in defense scenarios, enhanced maritime operations for safety and efficiency, and the expanding reach of commercial enterprises into areas where terrestrial infrastructure is limited. The adoption of advanced technologies such as high-throughput satellites (HTS) and the integration of LEO (Low Earth Orbit) and MEO (Medium Earth Orbit) constellations are further accelerating market penetration, offering lower latency and higher bandwidth capabilities crucial for applications like real-time video surveillance, IoT connectivity, and seamless voice communication.

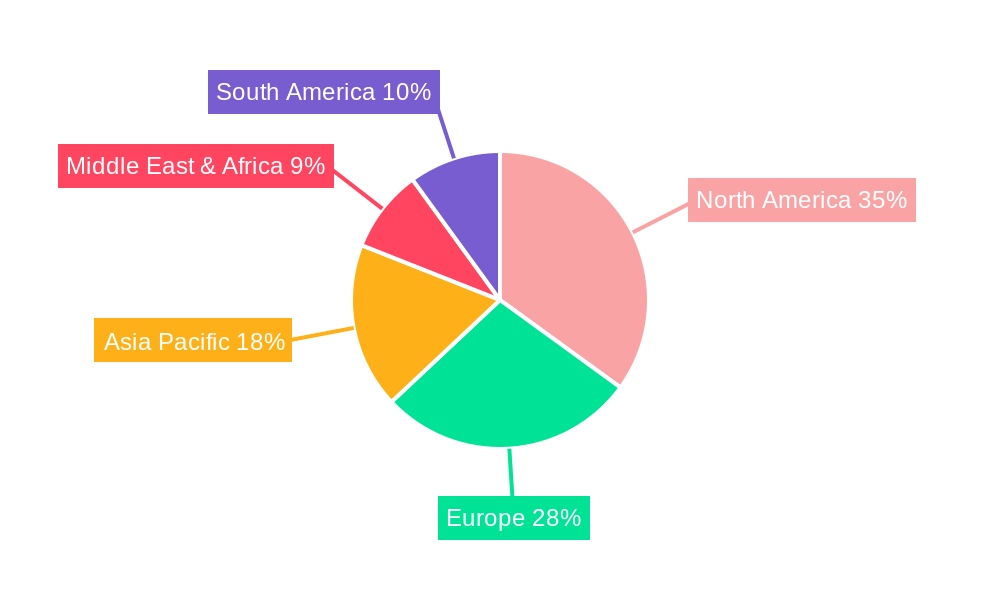

The market is segmented by application into Government and Defense, and Commercial, with the former historically dominating due to critical national security and emergency response needs. However, the Commercial segment is experiencing rapid growth, driven by industries such as agriculture, mining, logistics, and broadcasting seeking uninterrupted connectivity. By type, the Maritime Mobile Satellite System and Aeronautical Mobile Satellite System are vital for global transportation and logistics, while the Land Mobile Satellite System caters to remote workforces, disaster relief efforts, and individual users requiring connectivity on the go. Restraints such as high initial investment costs for satellite infrastructure and the increasing complexity of managing satellite networks are present, yet the persistent need for resilient communication solutions in an increasingly connected world, especially in the face of geopolitical uncertainties and natural disasters, will continue to propel market expansion and innovation, with North America and Europe currently leading in adoption due to established defense and commercial sectors, while the Asia Pacific region is anticipated to witness the fastest growth.

Mobile Satellite Communication System Market Composition & Trends

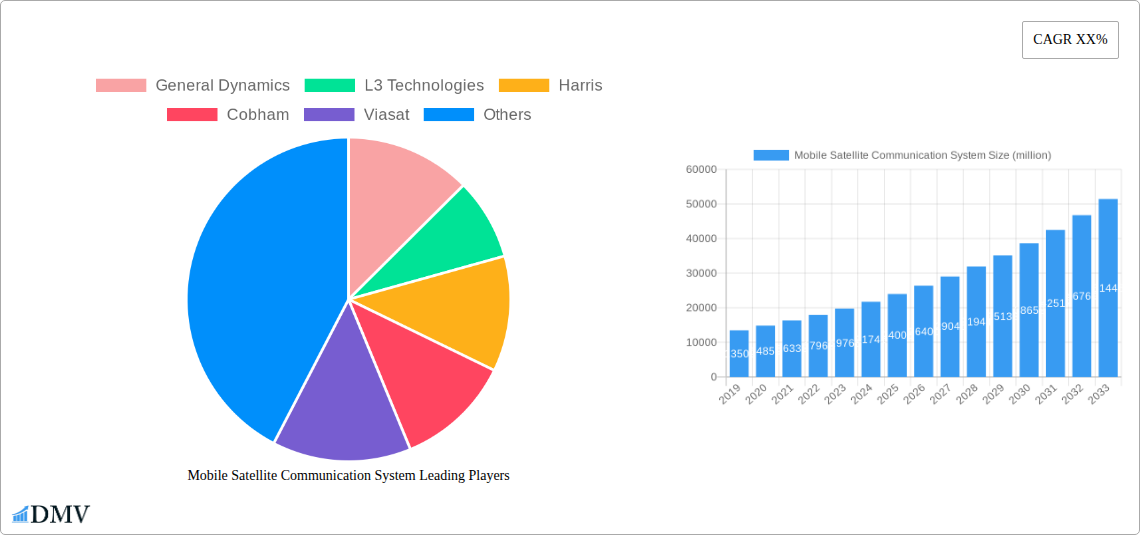

The global Mobile Satellite Communication System market is characterized by robust growth driven by increasing demand for ubiquitous connectivity, particularly within the Government and Defense and Commercial sectors. Market concentration is moderate, with key players like General Dynamics, L3 Technologies, Harris, Cobham, and Viasat holding significant shares. Innovation catalysts include the proliferation of Low Earth Orbit (LEO) satellite constellations, advancements in phased-array antennas, and the integration of AI for enhanced network management. Regulatory landscapes, while evolving, generally favor the expansion of satellite services, especially for critical infrastructure and remote operations. Substitute products, such as terrestrial cellular networks, continue to be a factor, but their limitations in remote or disaster-stricken areas underscore the unique value proposition of mobile satellite communications. End-user profiles range from military units requiring secure, reliable communication in austere environments to commercial enterprises seeking continuous connectivity for remote operations, maritime vessels, and aviation. Mergers and acquisitions (M&A) are shaping the competitive landscape, with significant deal values of approximately XXX million dollars recorded, fostering consolidation and synergistic growth.

- Market Share Distribution: Major players collectively command over 60% of the market, with regional variations in dominance.

- M&A Deal Values: Historical M&A activity has reached an estimated XXX million dollars, signaling strategic consolidation.

- Innovation Focus: LEO constellations, advanced antenna technologies, and integrated network solutions are key areas of innovation.

- End-User Segments: Government and Defense applications represent a substantial market share, followed by Commercial segments including maritime and aeronautical.

Mobile Satellite Communication System Industry Evolution

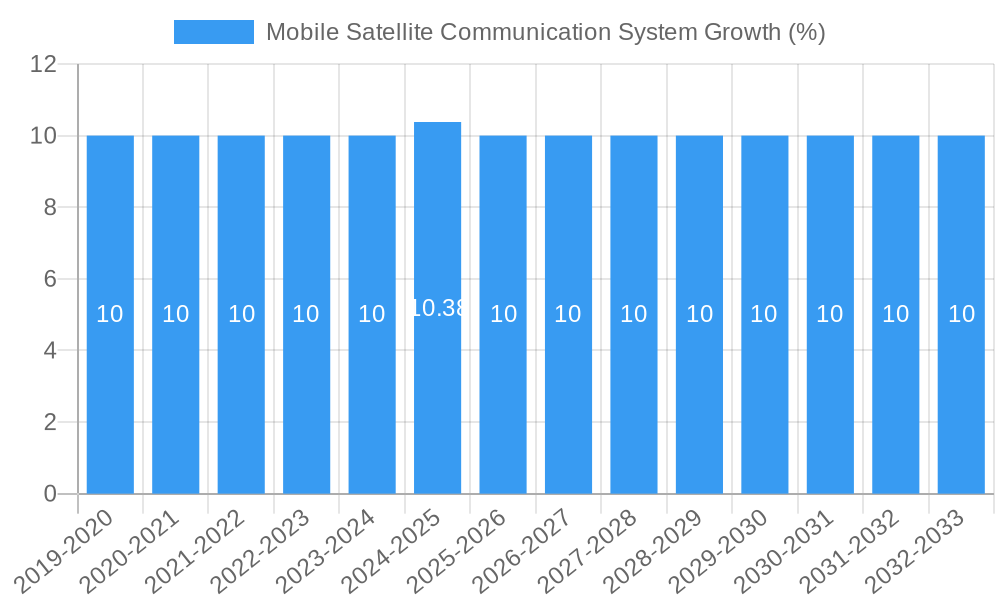

The Mobile Satellite Communication System industry has witnessed a dramatic evolution from its inception, marked by consistent market growth trajectories and significant technological advancements that have fundamentally reshaped connectivity paradigms. Over the historical period of 2019-2024, the market experienced a compound annual growth rate (CAGR) of approximately 8.5%, driven by increasing governmental investments in defense and security communications, alongside a burgeoning demand for high-speed, reliable internet access in remote commercial sectors. The base year of 2025 serves as a critical juncture, with projected growth rates of around 10.2% expected to accelerate through the forecast period of 2025-2033. This surge is largely attributable to the successful deployment and expansion of next-generation satellite constellations, particularly LEO and Medium Earth Orbit (MEO) systems, which offer significantly reduced latency and increased bandwidth compared to traditional Geostationary (GEO) satellites.

Shifting consumer and enterprise demands have played a pivotal role in this evolution. The need for seamless, always-on connectivity for critical applications such as remote sensing, IoT deployments, autonomous vehicle operations, and global maritime and aeronautical operations has become paramount. This has led to a greater adoption of mobile satellite communication systems beyond their traditional defense roles. Technological advancements have not only focused on satellite capabilities but also on user terminals and ground infrastructure. The development of smaller, more power-efficient, and higher-gain antennas, coupled with sophisticated modems and software-defined radio (SDR) technologies, has made mobile satellite communication systems more accessible and versatile. For instance, the adoption of flat-panel antennas and electronically steered arrays has revolutionized the ease of installation and use on mobile platforms. Furthermore, the integration of satellite communication with existing terrestrial networks, through hybrid solutions, is enhancing overall network resilience and coverage. The study period of 2019-2033 encompasses this transformative phase, highlighting how technological leaps and evolving market needs have propelled mobile satellite communications into a vital component of global communication infrastructure.

Leading Regions, Countries, or Segments in Mobile Satellite Communication System

The Government and Defense segment stands as a dominant force within the Mobile Satellite Communication System market, demonstrating consistent leadership throughout the study period of 2019–2033. This dominance is underpinned by substantial and sustained investments in national security, defense modernization programs, and the imperative for secure, resilient, and pervasive communication capabilities for military operations across the globe. Governments worldwide recognize the strategic importance of mobile satellite communications for battlefield awareness, command and control, intelligence gathering, and logistical support, particularly in regions where terrestrial infrastructure is absent, compromised, or non-existent. The inherent ability of satellite systems to provide global coverage, irrespective of geographical terrain or political boundaries, makes them indispensable for defense forces engaged in expeditionary operations, counter-terrorism efforts, and humanitarian assistance missions.

The Maritime Mobile Satellite System is another key segment experiencing robust growth, driven by the expansion of global trade, the increasing sophistication of offshore industries (such as oil and gas exploration), and the growing demand for connectivity among cruise liners and private yachts. Regulatory mandates for maritime safety and communication also contribute significantly to this segment’s expansion. Companies like Cobham and Satcom Global are at the forefront of providing specialized solutions for this sector.

The Aeronautical Mobile Satellite System segment, while currently smaller, is poised for significant expansion. The increasing adoption of inflight connectivity (IFC) by airlines, driven by passenger demand for internet access and the operational needs of airlines for real-time data transmission, is a major growth catalyst. Hughes Network Systems and Viasat are key players here, investing heavily in advanced antenna technologies and satellite capacity to support high-bandwidth IFC services.

The Land Mobile Satellite System segment serves a diverse range of users, including emergency responders, remote industrial workers, and consumers in underserved areas. Campbell Scientific’s focus on environmental monitoring and data collection, as well as the broader application in disaster relief and remote enterprise connectivity, highlights the critical role of this segment. The growth in this area is fueled by the proliferation of IoT devices and the need for reliable communication in rugged and remote environments.

Key Drivers for Government and Defense Dominance:

- National Security Imperatives: Continuous investment in defense modernization and global operational readiness.

- Resilience and Survivability: Satellite systems offer critical redundancy and survivability in contested or disrupted environments.

- Global Reach: Unparalleled coverage for deployed forces in remote or austere locations.

- Secure Communication: Advanced encryption and secure networking protocols are essential.

Growth Factors in Maritime and Aeronautical Segments:

- IFC Demand: Passenger expectation for internet connectivity on flights.

- Commercial Vessel Connectivity: Enhanced operational efficiency, crew welfare, and real-time data for shipping and logistics.

- Offshore Industry Needs: Reliable communication for exploration, drilling, and production platforms.

Mobile Satellite Communication System Product Innovations

The Mobile Satellite Communication System market is witnessing a wave of groundbreaking product innovations designed to enhance performance, reduce size and cost, and expand application reach. Key advancements include the development of highly efficient, low-profile phased-array antennas by companies like Intellian Technologies and Gilat Satellite Networks, enabling seamless, beam-switching connectivity for moving vehicles, vessels, and aircraft. These antennas offer superior tracking capabilities and faster acquisition times, crucial for maintaining continuous communication. Furthermore, the integration of software-defined networking (SDN) and artificial intelligence (AI) into satellite terminals and network management systems is optimizing bandwidth utilization, predicting network congestion, and automating troubleshooting, thereby improving overall user experience and operational efficiency. The increasing affordability and miniaturization of satellite modems and transceivers are also democratizing access to mobile satellite services, paving the way for new applications in the Internet of Things (IoT) and remote sensing.

Propelling Factors for Mobile Satellite Communication System Growth

The growth of the Mobile Satellite Communication System market is propelled by several interconnected factors. Technologically, the proliferation of Low Earth Orbit (LEO) satellite constellations by companies like Iridium is drastically reducing latency and increasing bandwidth, making satellite communication more competitive with terrestrial options. Economically, the increasing demand for remote operations in sectors like energy, mining, and agriculture, coupled with the growing adoption of inflight connectivity, provides substantial market opportunities. Regulatory support, particularly in the defense sector and for critical infrastructure, further fuels investment and deployment.

- Technological Advancements: LEO constellations, improved antenna technology, and integrated network solutions.

- Economic Demand: Growth in remote industries, global trade, and inflight connectivity.

- Regulatory Support: Government investment in defense and critical infrastructure communications.

Obstacles in the Mobile Satellite Communication System Market

Despite its robust growth, the Mobile Satellite Communication System market faces several obstacles. Regulatory hurdles and spectrum licensing complexities in different countries can hinder seamless global deployment and increase operational costs for service providers. The high initial capital investment required for satellite infrastructure and ground terminals, although decreasing, remains a significant barrier for smaller players and certain commercial applications. Supply chain disruptions, particularly for critical electronic components, can impact production timelines and costs, as seen in recent global manufacturing challenges. Competitive pressures from increasingly capable terrestrial networks, especially 5G, also pose a threat in densely populated areas where satellite communication may be perceived as a more expensive alternative.

- Regulatory Complexity: Spectrum allocation and licensing across diverse jurisdictions.

- High Capital Expenditure: Significant upfront investment for satellite and ground segment development.

- Supply Chain Vulnerabilities: Potential disruptions in the availability of key components.

- Terrestrial Network Competition: 5G and other terrestrial technologies in areas with established infrastructure.

Future Opportunities in Mobile Satellite Communication System

Emerging opportunities in the Mobile Satellite Communication System market are abundant and diverse. The expansion of IoT networks in remote industrial settings, smart agriculture, and environmental monitoring presents a vast untapped market. The increasing demand for high-speed, reliable inflight connectivity for both passengers and operational data will continue to drive innovation in the aeronautical segment. The development of integrated satellite-terrestrial networks (e.g., satellite-to-phone technology) promises to expand coverage to previously unconnected areas, offering new service models. Furthermore, advancements in edge computing and artificial intelligence, when combined with satellite connectivity, will unlock new applications in autonomous systems and real-time data analytics in remote locations.

- IoT Expansion: Connecting devices for remote monitoring and industrial applications.

- Advanced IFC: Enhancing passenger and airline operational connectivity.

- Satellite-to-Device Communication: Bridging connectivity gaps for personal devices.

- AI & Edge Computing Integration: Enabling intelligent remote operations and data processing.

Major Players in the Mobile Satellite Communication System Ecosystem

- General Dynamics

- L3 Technologies

- Harris

- Cobham

- Viasat

- Iridium

- Gilat Satellite Networks

- Aselsan

- Intellian Technologies

- Hughes Network Systems

- Newtec

- Campbell Scientific

- Nd Satcom

- Satcom Global

- Holkirk Communications

- Network Innovations

- Avl Technologies

- ST Engineering

Key Developments in Mobile Satellite Communication System Industry

- 2019: Iridium launched the first phase of its next-generation Iridium Certus service, enhancing broadband capabilities for mobile users.

- 2020: Viasat announced the successful launch of its Viasat-3 constellation, promising unprecedented satellite broadband capacity.

- 2021: Gilat Satellite Networks secured significant contracts for deploying satellite networks for governmental and defense applications.

- 2022: L3 Technologies showcased advanced antenna solutions for aeronautical and maritime mobile satellite communications.

- 2023: General Dynamics continued to expand its portfolio of secure mobile satellite communication solutions for defense.

- 2024: Intellian Technologies introduced new compact, high-performance VSAT terminals for various mobile platforms.

- 2024 (Q3): Hughes Network Systems announced advancements in LEO gateway technology, enabling higher throughput for mobile services.

- 2024 (Q4): Cobham integrated advanced satcom solutions with new aircraft models, enhancing inflight connectivity.

Strategic Mobile Satellite Communication System Market Forecast

The Mobile Satellite Communication System market is poised for sustained and accelerated growth through 2033, driven by an unwavering demand for global, resilient connectivity. The continued expansion of LEO satellite constellations, coupled with significant technological advancements in terminal design and network integration, will unlock new market segments and enhance existing service offerings. Strategic investments in defense modernization and the increasing reliance on satellite communications for critical infrastructure and remote enterprise operations will remain foundational growth catalysts. Emerging opportunities in the IoT, autonomous systems, and direct-to-device communication further underscore the expansive potential of this dynamic market.

Mobile Satellite Communication System Segmentation

-

1. Application

- 1.1. Government and Defense

- 1.2. Commercial

-

2. Types

- 2.1. Maritime Mobile Satellite System

- 2.2. Aeronautical Mobile Satellite System

- 2.3. Land Mobile Satellite System

Mobile Satellite Communication System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Mobile Satellite Communication System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mobile Satellite Communication System Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Government and Defense

- 5.1.2. Commercial

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Maritime Mobile Satellite System

- 5.2.2. Aeronautical Mobile Satellite System

- 5.2.3. Land Mobile Satellite System

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Mobile Satellite Communication System Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Government and Defense

- 6.1.2. Commercial

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Maritime Mobile Satellite System

- 6.2.2. Aeronautical Mobile Satellite System

- 6.2.3. Land Mobile Satellite System

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Mobile Satellite Communication System Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Government and Defense

- 7.1.2. Commercial

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Maritime Mobile Satellite System

- 7.2.2. Aeronautical Mobile Satellite System

- 7.2.3. Land Mobile Satellite System

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Mobile Satellite Communication System Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Government and Defense

- 8.1.2. Commercial

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Maritime Mobile Satellite System

- 8.2.2. Aeronautical Mobile Satellite System

- 8.2.3. Land Mobile Satellite System

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Mobile Satellite Communication System Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Government and Defense

- 9.1.2. Commercial

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Maritime Mobile Satellite System

- 9.2.2. Aeronautical Mobile Satellite System

- 9.2.3. Land Mobile Satellite System

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Mobile Satellite Communication System Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Government and Defense

- 10.1.2. Commercial

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Maritime Mobile Satellite System

- 10.2.2. Aeronautical Mobile Satellite System

- 10.2.3. Land Mobile Satellite System

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 General Dynamics

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 L3 Technologies

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Harris

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cobham

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Viasat

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Iridium

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Gilat Satellite Networks

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Aselsan

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Intellian Technologies

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Hughes Network Systems

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Newtec

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Campbell Scientific

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Nd Satcom

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Satcom Global

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Holkirk Communications

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Network Innovations

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Avl Technologies

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 ST Engineering

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 General Dynamics

List of Figures

- Figure 1: Global Mobile Satellite Communication System Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Mobile Satellite Communication System Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Mobile Satellite Communication System Revenue (million), by Application 2024 & 2032

- Figure 4: North America Mobile Satellite Communication System Volume (K), by Application 2024 & 2032

- Figure 5: North America Mobile Satellite Communication System Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Mobile Satellite Communication System Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Mobile Satellite Communication System Revenue (million), by Types 2024 & 2032

- Figure 8: North America Mobile Satellite Communication System Volume (K), by Types 2024 & 2032

- Figure 9: North America Mobile Satellite Communication System Revenue Share (%), by Types 2024 & 2032

- Figure 10: North America Mobile Satellite Communication System Volume Share (%), by Types 2024 & 2032

- Figure 11: North America Mobile Satellite Communication System Revenue (million), by Country 2024 & 2032

- Figure 12: North America Mobile Satellite Communication System Volume (K), by Country 2024 & 2032

- Figure 13: North America Mobile Satellite Communication System Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Mobile Satellite Communication System Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Mobile Satellite Communication System Revenue (million), by Application 2024 & 2032

- Figure 16: South America Mobile Satellite Communication System Volume (K), by Application 2024 & 2032

- Figure 17: South America Mobile Satellite Communication System Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Mobile Satellite Communication System Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Mobile Satellite Communication System Revenue (million), by Types 2024 & 2032

- Figure 20: South America Mobile Satellite Communication System Volume (K), by Types 2024 & 2032

- Figure 21: South America Mobile Satellite Communication System Revenue Share (%), by Types 2024 & 2032

- Figure 22: South America Mobile Satellite Communication System Volume Share (%), by Types 2024 & 2032

- Figure 23: South America Mobile Satellite Communication System Revenue (million), by Country 2024 & 2032

- Figure 24: South America Mobile Satellite Communication System Volume (K), by Country 2024 & 2032

- Figure 25: South America Mobile Satellite Communication System Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Mobile Satellite Communication System Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Mobile Satellite Communication System Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Mobile Satellite Communication System Volume (K), by Application 2024 & 2032

- Figure 29: Europe Mobile Satellite Communication System Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Mobile Satellite Communication System Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Mobile Satellite Communication System Revenue (million), by Types 2024 & 2032

- Figure 32: Europe Mobile Satellite Communication System Volume (K), by Types 2024 & 2032

- Figure 33: Europe Mobile Satellite Communication System Revenue Share (%), by Types 2024 & 2032

- Figure 34: Europe Mobile Satellite Communication System Volume Share (%), by Types 2024 & 2032

- Figure 35: Europe Mobile Satellite Communication System Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Mobile Satellite Communication System Volume (K), by Country 2024 & 2032

- Figure 37: Europe Mobile Satellite Communication System Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Mobile Satellite Communication System Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Mobile Satellite Communication System Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Mobile Satellite Communication System Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Mobile Satellite Communication System Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Mobile Satellite Communication System Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Mobile Satellite Communication System Revenue (million), by Types 2024 & 2032

- Figure 44: Middle East & Africa Mobile Satellite Communication System Volume (K), by Types 2024 & 2032

- Figure 45: Middle East & Africa Mobile Satellite Communication System Revenue Share (%), by Types 2024 & 2032

- Figure 46: Middle East & Africa Mobile Satellite Communication System Volume Share (%), by Types 2024 & 2032

- Figure 47: Middle East & Africa Mobile Satellite Communication System Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Mobile Satellite Communication System Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Mobile Satellite Communication System Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Mobile Satellite Communication System Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Mobile Satellite Communication System Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Mobile Satellite Communication System Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Mobile Satellite Communication System Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Mobile Satellite Communication System Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Mobile Satellite Communication System Revenue (million), by Types 2024 & 2032

- Figure 56: Asia Pacific Mobile Satellite Communication System Volume (K), by Types 2024 & 2032

- Figure 57: Asia Pacific Mobile Satellite Communication System Revenue Share (%), by Types 2024 & 2032

- Figure 58: Asia Pacific Mobile Satellite Communication System Volume Share (%), by Types 2024 & 2032

- Figure 59: Asia Pacific Mobile Satellite Communication System Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Mobile Satellite Communication System Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Mobile Satellite Communication System Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Mobile Satellite Communication System Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Mobile Satellite Communication System Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Mobile Satellite Communication System Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Mobile Satellite Communication System Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Mobile Satellite Communication System Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Mobile Satellite Communication System Revenue million Forecast, by Types 2019 & 2032

- Table 6: Global Mobile Satellite Communication System Volume K Forecast, by Types 2019 & 2032

- Table 7: Global Mobile Satellite Communication System Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Mobile Satellite Communication System Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Mobile Satellite Communication System Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Mobile Satellite Communication System Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Mobile Satellite Communication System Revenue million Forecast, by Types 2019 & 2032

- Table 12: Global Mobile Satellite Communication System Volume K Forecast, by Types 2019 & 2032

- Table 13: Global Mobile Satellite Communication System Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Mobile Satellite Communication System Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Mobile Satellite Communication System Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Mobile Satellite Communication System Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Mobile Satellite Communication System Revenue million Forecast, by Types 2019 & 2032

- Table 24: Global Mobile Satellite Communication System Volume K Forecast, by Types 2019 & 2032

- Table 25: Global Mobile Satellite Communication System Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Mobile Satellite Communication System Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Mobile Satellite Communication System Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Mobile Satellite Communication System Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Mobile Satellite Communication System Revenue million Forecast, by Types 2019 & 2032

- Table 36: Global Mobile Satellite Communication System Volume K Forecast, by Types 2019 & 2032

- Table 37: Global Mobile Satellite Communication System Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Mobile Satellite Communication System Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Mobile Satellite Communication System Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Mobile Satellite Communication System Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Mobile Satellite Communication System Revenue million Forecast, by Types 2019 & 2032

- Table 60: Global Mobile Satellite Communication System Volume K Forecast, by Types 2019 & 2032

- Table 61: Global Mobile Satellite Communication System Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Mobile Satellite Communication System Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Mobile Satellite Communication System Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Mobile Satellite Communication System Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Mobile Satellite Communication System Revenue million Forecast, by Types 2019 & 2032

- Table 78: Global Mobile Satellite Communication System Volume K Forecast, by Types 2019 & 2032

- Table 79: Global Mobile Satellite Communication System Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Mobile Satellite Communication System Volume K Forecast, by Country 2019 & 2032

- Table 81: China Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Mobile Satellite Communication System Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Mobile Satellite Communication System Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Satellite Communication System?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Mobile Satellite Communication System?

Key companies in the market include General Dynamics, L3 Technologies, Harris, Cobham, Viasat, Iridium, Gilat Satellite Networks, Aselsan, Intellian Technologies, Hughes Network Systems, Newtec, Campbell Scientific, Nd Satcom, Satcom Global, Holkirk Communications, Network Innovations, Avl Technologies, ST Engineering.

3. What are the main segments of the Mobile Satellite Communication System?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Satellite Communication System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Satellite Communication System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Satellite Communication System?

To stay informed about further developments, trends, and reports in the Mobile Satellite Communication System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence