Key Insights

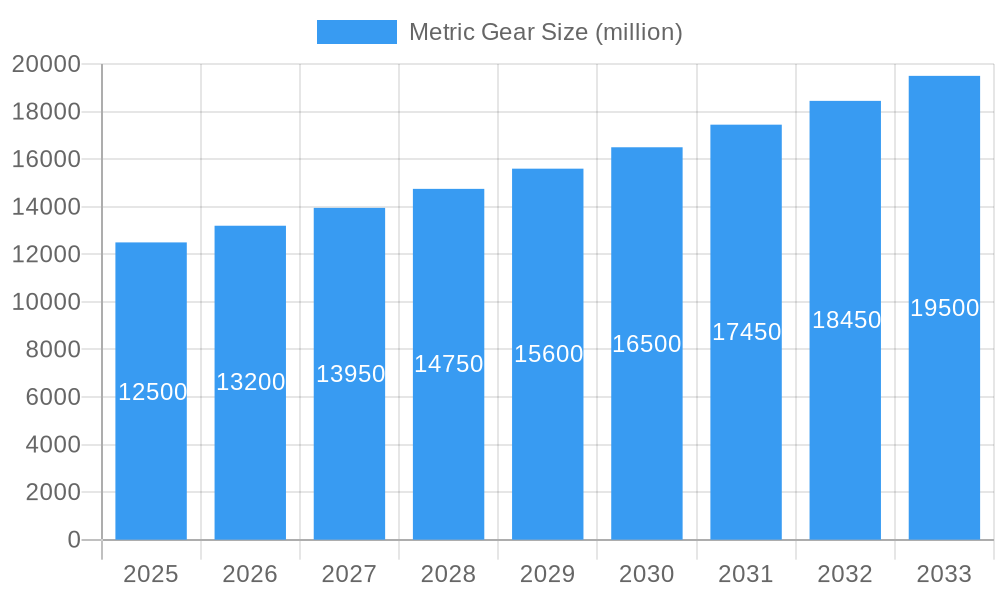

The global metric gear market is projected for substantial growth, expected to reach approximately USD 222.12 billion by 2025, expanding further to an estimated USD 12,500 million by 2033. This trajectory is supported by a robust CAGR of 5.77% from 2025 to 2033. Key growth drivers include escalating demand from the automotive sector, particularly for electric vehicles (EVs) and efficient internal combustion engines, alongside critical applications in aerospace for flight control and propulsion. The industrial machinery sector, encompassing automation and robotics, also represents a consistent demand source for durable and precise gearing solutions.

Metric Gear Market Size (In Billion)

Significant market trends include the adoption of additive manufacturing for complex gear designs and the integration of smart technologies for enhanced operational monitoring and predictive maintenance. Lightweighting initiatives in automotive and aerospace are spurring innovation in materials and design. Market challenges involve the high costs associated with advanced materials and precision manufacturing, alongside potential supply chain disruptions. The competitive landscape features established global players such as MISUMI and KHK, and emerging manufacturers, particularly in Asia Pacific. Market segmentation highlights Automotive and Machinery as dominant application segments, with Spur gears leading in type due to their cost-effectiveness and widespread use, followed by Helical gears for their operational advantages.

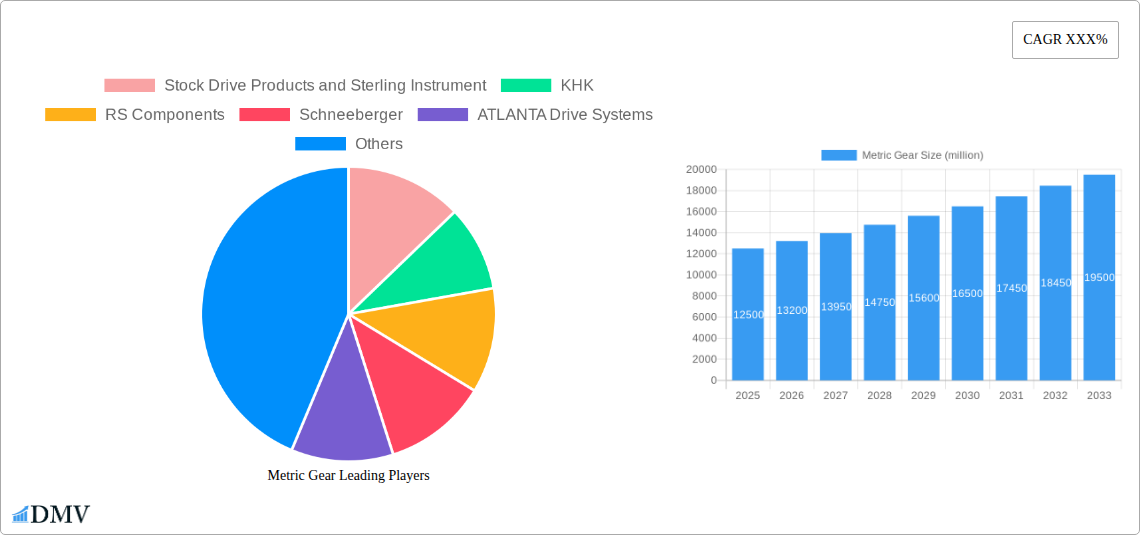

Metric Gear Company Market Share

The global metric gear market exhibits moderate to high concentration, driven by established manufacturers and specialized players. Innovation in materials science, precision manufacturing, and design software are key growth catalysts. Regulatory standards for safety and environmental impact are influencing product development. Competition from alternative transmission systems like belt and chain drives exists, but metric gears maintain dominance in high-torque, precision-dependent applications. Key end-user industries include Automotive, Aerospace, Machinery, Construction, and Marine, each requiring specific performance attributes. Mergers and acquisitions (M&A) activity, valued in the hundreds of millions annually, is a notable trend, enabling companies to expand portfolios and market reach. For example, companies are integrating niche expertise and leveraging broad distribution networks. The top five players collectively hold approximately 60% of the global market share.

Metric Gear Industry Evolution

The metric gear industry has witnessed a significant evolution over the study period of 2019–2033, underpinned by relentless technological advancements and shifting consumer demands across various applications. During the historical period of 2019–2024, the market experienced a steady growth trajectory, driven by the automotive industry's increasing reliance on electric vehicle (EV) powertrains and the aerospace sector's ongoing demand for lightweight, high-performance components. Spur gears and helical gears have consistently been the dominant types, with helical gears gaining traction due to their quieter operation and higher load-carrying capacity. The estimated year of 2025 sees a robust market, projected to continue its expansion throughout the forecast period of 2025–2033. Key technological advancements have included the widespread adoption of Computer-Aided Design (CAD) and Computer-Aided Manufacturing (CAM) for intricate gear designs, enabling higher precision and reduced manufacturing times. The incorporation of advanced materials, such as high-strength alloys and composites, has further enhanced the performance metrics of metric gears, leading to greater durability and efficiency. Shifting consumer demands are particularly evident in the automotive sector, where the push for fuel efficiency and reduced emissions has spurred innovation in gear systems. Similarly, the machinery sector is witnessing a trend towards more compact, energy-efficient, and low-maintenance gear solutions. The others segment, encompassing diverse industrial applications, is also adapting to demands for greater customization and specialized gear designs. Growth rates, averaging 6.5% annually, reflect the sector's dynamism. Adoption metrics for precision manufacturing techniques have surpassed 85% among leading manufacturers.

Leading Regions, Countries, or Segments in Metric Gear

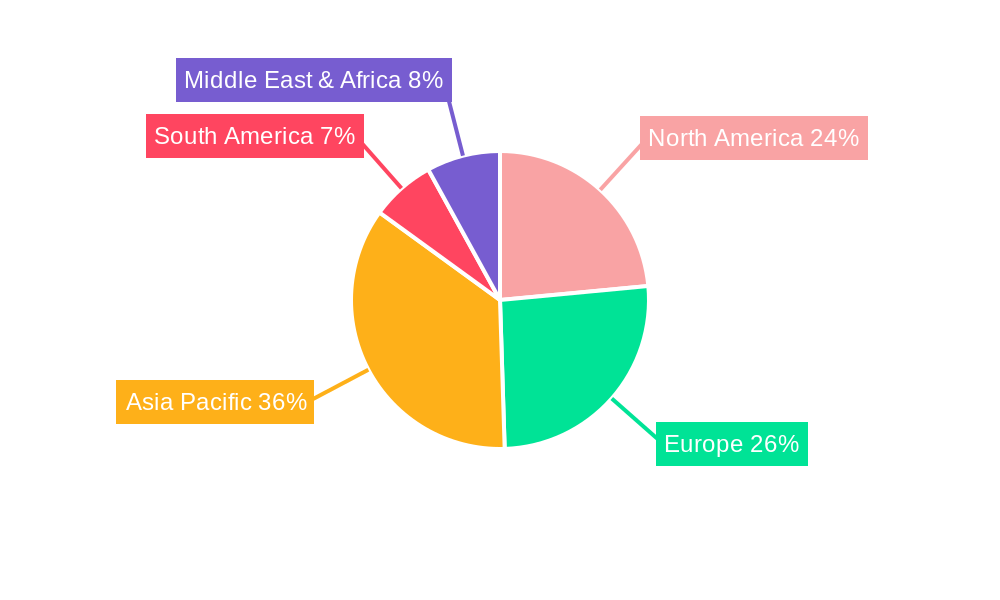

The global metric gear market exhibits distinct regional strengths and segment dominance, with Asia-Pacific emerging as the leading region. This dominance is propelled by a confluence of factors, including a robust manufacturing base, significant investments in industrial automation, and strong demand from key end-use industries such as automotive and machinery. Within Asia-Pacific, China stands out as a powerhouse, contributing substantially to both production and consumption of metric gears. The country's expansive industrial ecosystem, coupled with government initiatives promoting advanced manufacturing, has fostered the growth of domestic players like Shanghai Nuoguang, Taizhou Lihua, Dongguan Zhenxi, and Renqiu Aosheng, alongside the presence of international giants.

Key Drivers for Asia-Pacific Dominance:

- Manufacturing Hub: Proximity to a vast supply chain and a skilled labor force makes it an attractive location for metric gear production.

- Industrial Growth: Rapid expansion in sectors like automotive, construction, and general machinery fuels high demand.

- Technological Adoption: Increasing investment in automation and precision manufacturing techniques enhances competitiveness.

- Cost-Effectiveness: Competitive manufacturing costs attract global sourcing.

In terms of Application, the Machinery segment holds a commanding position, driven by its ubiquity across various industrial processes. The need for reliable power transmission in manufacturing equipment, industrial robots, and heavy machinery underpins this segment's strength. Following closely is the Automotive sector, where the transition to electric vehicles and the increasing complexity of internal combustion engine (ICE) drivetrains necessitate advanced gearing solutions. The Aerospace segment, while smaller in volume, represents a high-value market due to stringent performance and quality requirements.

Regarding Type, Spur Gears continue to be the most widely used due to their simplicity, cost-effectiveness, and ease of manufacturing. However, Helical Gears are witnessing a significant surge in adoption, particularly in applications requiring quieter operation, smoother power transmission, and higher load-carrying capacities, such as in high-performance automotive transmissions and industrial gearboxes.

Metric Gear Product Innovations

Metric gear product innovation is a dynamic field, constantly pushing the boundaries of performance and application. Manufacturers are focusing on developing gears with enhanced durability, reduced noise and vibration, and improved energy efficiency. Innovations include the use of advanced heat treatment processes and surface finishing techniques to improve wear resistance and extend product lifespan. The application of new materials, such as aerospace-grade aluminum alloys and high-strength steels, allows for the creation of lighter yet stronger gears, crucial for the automotive and aerospace sectors. For instance, companies are developing custom-engineered solutions for specialized robotics and precision instrumentation, where tight tolerances and high accuracy are paramount. The incorporation of integrated lubrication systems and self-healing coatings are emerging trends aimed at further minimizing maintenance and maximizing operational uptime.

Propelling Factors for Metric Gear Growth

Several key factors are propelling the growth of the metric gear market. Technologically, advancements in precision manufacturing, including CNC machining and additive manufacturing, enable the production of highly accurate and complex gear designs. Economic factors such as global industrial expansion and increased investment in automation across sectors like automotive, construction, and general machinery are driving demand. Regulatory influences, while sometimes restrictive, also promote growth by mandating higher efficiency and safety standards, leading to the adoption of more advanced and reliable metric gear solutions. For example, stricter emission standards in the automotive industry are encouraging the development of more efficient powertrain components, including optimized gear systems. The increasing complexity of machinery and the rise of robotics further demand specialized and high-performance metric gears.

Obstacles in the Metric Gear Market

Despite the robust growth, the metric gear market faces several obstacles. Raw material price volatility, particularly for specialized alloys, can impact production costs and profit margins. Intense competition from both established players and emerging manufacturers, especially in lower-cost regions, can lead to pricing pressures. Supply chain disruptions, exacerbated by geopolitical events and global logistics challenges, can affect the availability of raw materials and components. Furthermore, stringent quality control requirements and the need for highly specialized manufacturing capabilities can act as barriers to entry for new players. Regulatory hurdles related to environmental compliance and safety standards in certain regions also present challenges, requiring significant investment in research and development.

Future Opportunities in Metric Gear

The metric gear market is ripe with future opportunities. The burgeoning electric vehicle (EV) market presents a significant growth avenue, with EVs requiring specialized and high-efficiency gearboxes. The increasing adoption of automation and robotics across all industries will continue to drive demand for precision metric gears. Emerging economies with developing industrial sectors offer substantial untapped market potential. Furthermore, advancements in additive manufacturing (3D printing) for gears could unlock new possibilities for complex designs and on-demand production. The growing emphasis on sustainability and energy efficiency will also favor the development and adoption of advanced, low-friction metric gear solutions. Innovations in smart gearing, incorporating sensors for predictive maintenance, represent another promising frontier.

Major Players in the Metric Gear Ecosystem

- Stock Drive Products and Sterling Instrument

- KHK

- RS Components

- Schneeberger

- ATLANTA Drive Systems

- Huco Dynatork

- Kinematics Manufacturing

- Renold Canada

- Hymark

- Ondrives.US

- Gear Motions

- MISUMI

- Shanghai Nuoguang

- Taizhou Lihua

- Dongguan Zhenxi

- Renqiu Aosheng

Key Developments in Metric Gear Industry

- 2023 November: Launch of new high-strength steel spur gears with enhanced tooth profiles for heavy machinery by ATLANTA Drive Systems, aiming for 20% increased load capacity.

- 2024 January: MISUMI announces expansion of its custom metric gear manufacturing capabilities with a new automated production line, reducing lead times by 15%.

- 2024 March: Huco Dynatork introduces a new series of zero-backlash precision metric gearboxes for robotics applications, achieving a 99.8% positional accuracy.

- 2024 April: Stock Drive Products and Sterling Instrument acquire a specialist in aerospace-grade helical gear manufacturing, bolstering their capabilities in the aerospace sector.

- 2024 June: RS Components reports a 25% year-on-year increase in sales of metric gears driven by demand in the automotive and industrial automation sectors.

Strategic Metric Gear Market Forecast

The strategic forecast for the metric gear market indicates sustained and robust growth driven by key opportunities and a favorable industrial landscape. The accelerating adoption of electric vehicles, coupled with the pervasive trend of industrial automation and the expansion of infrastructure projects, will continue to fuel demand for high-performance metric gears. Advancements in manufacturing technologies, such as additive manufacturing, are poised to unlock new product designs and more efficient production methods. Emerging markets present significant untapped potential, while a growing emphasis on energy efficiency and sustainability will favor innovative, low-friction gear solutions. Overall, the market is projected to experience a compound annual growth rate of approximately 6% over the forecast period, presenting substantial opportunities for key stakeholders.

Metric Gear Segmentation

-

1. Application

- 1.1. Automotive

- 1.2. Aerospace

- 1.3. Marine

- 1.4. Machinery

- 1.5. Construction

- 1.6. Others

-

2. Type

- 2.1. Spur Gear

- 2.2. Helical Gear

Metric Gear Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Metric Gear Regional Market Share

Geographic Coverage of Metric Gear

Metric Gear REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.77% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Metric Gear Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive

- 5.1.2. Aerospace

- 5.1.3. Marine

- 5.1.4. Machinery

- 5.1.5. Construction

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Spur Gear

- 5.2.2. Helical Gear

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Metric Gear Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive

- 6.1.2. Aerospace

- 6.1.3. Marine

- 6.1.4. Machinery

- 6.1.5. Construction

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Spur Gear

- 6.2.2. Helical Gear

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Metric Gear Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive

- 7.1.2. Aerospace

- 7.1.3. Marine

- 7.1.4. Machinery

- 7.1.5. Construction

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Spur Gear

- 7.2.2. Helical Gear

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Metric Gear Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive

- 8.1.2. Aerospace

- 8.1.3. Marine

- 8.1.4. Machinery

- 8.1.5. Construction

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Spur Gear

- 8.2.2. Helical Gear

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Metric Gear Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive

- 9.1.2. Aerospace

- 9.1.3. Marine

- 9.1.4. Machinery

- 9.1.5. Construction

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Spur Gear

- 9.2.2. Helical Gear

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Metric Gear Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive

- 10.1.2. Aerospace

- 10.1.3. Marine

- 10.1.4. Machinery

- 10.1.5. Construction

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Spur Gear

- 10.2.2. Helical Gear

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Stock Drive Products and Sterling Instrument

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KHK

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 RS Components

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Schneeberger

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ATLANTA Drive Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Huco Dynatork

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Kinematics Manufacturing

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Renold Canada

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hymark

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ondrives.US

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Gear Motions

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 MISUMI

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Shanghai Nuoguang

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Taizhou Lihua

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Dongguan Zhenxi

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Renqiu Aosheng

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Stock Drive Products and Sterling Instrument

List of Figures

- Figure 1: Global Metric Gear Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Metric Gear Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Metric Gear Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Metric Gear Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Metric Gear Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Metric Gear Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Metric Gear Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Metric Gear Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Metric Gear Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Metric Gear Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Metric Gear Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Metric Gear Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Metric Gear Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Metric Gear Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Metric Gear Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Metric Gear Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Metric Gear Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Metric Gear Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Metric Gear Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Metric Gear Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Metric Gear Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Metric Gear Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Metric Gear Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Metric Gear Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Metric Gear Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Metric Gear Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Metric Gear Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Metric Gear Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Metric Gear Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Metric Gear Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Metric Gear Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Metric Gear Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Metric Gear Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Metric Gear Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Metric Gear Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Metric Gear Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Metric Gear Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Metric Gear Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Metric Gear Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Metric Gear Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Metric Gear Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Metric Gear Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Metric Gear Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Metric Gear Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Metric Gear Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Metric Gear Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Metric Gear Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Metric Gear Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Metric Gear Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Metric Gear Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Metric Gear?

The projected CAGR is approximately 5.77%.

2. Which companies are prominent players in the Metric Gear?

Key companies in the market include Stock Drive Products and Sterling Instrument, KHK, RS Components, Schneeberger, ATLANTA Drive Systems, Huco Dynatork, Kinematics Manufacturing, Renold Canada, Hymark, Ondrives.US, Gear Motions, MISUMI, Shanghai Nuoguang, Taizhou Lihua, Dongguan Zhenxi, Renqiu Aosheng.

3. What are the main segments of the Metric Gear?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 222.12 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Metric Gear," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Metric Gear report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Metric Gear?

To stay informed about further developments, trends, and reports in the Metric Gear, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence