Key Insights

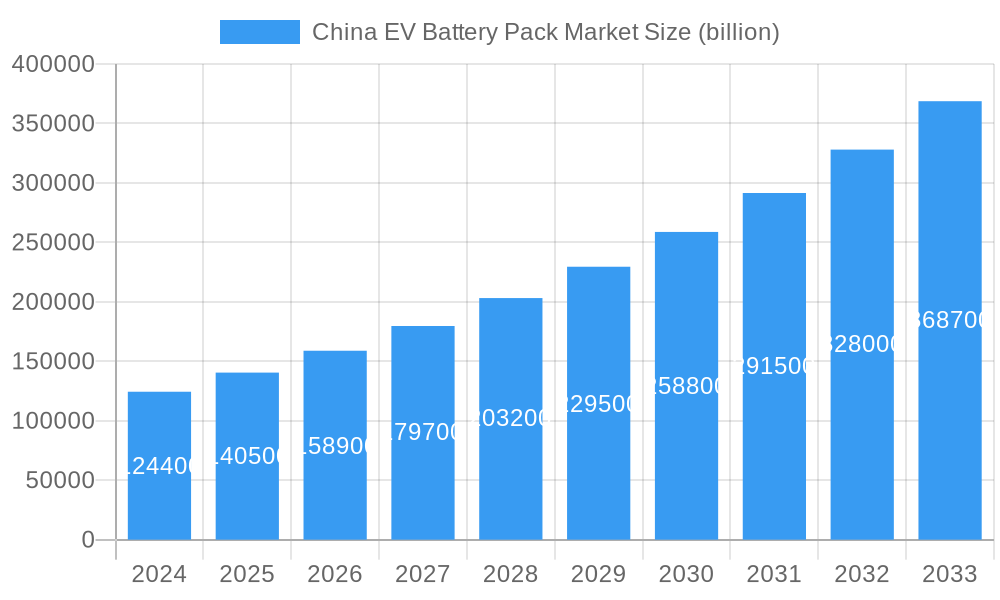

The China Electric Vehicle (EV) Battery Pack Market is experiencing robust expansion, projected to reach an impressive USD 124.4 billion in 2024 and continue its upward trajectory with a Compound Annual Growth Rate (CAGR) of 12.8% through 2033. This significant growth is underpinned by several powerful drivers, most notably the Chinese government's unwavering commitment to promoting electric mobility through substantial subsidies, favorable policies, and the rapid development of charging infrastructure. The increasing consumer demand for environmentally friendly transportation, coupled with the declining cost of EV batteries and advancements in battery technology, further fuels market expansion. The market is witnessing a strong preference for Battery Electric Vehicles (BEVs), which are dominating the propulsion type segment. Within battery chemistry, Lithium Iron Phosphate (LFP) batteries are gaining significant traction due to their cost-effectiveness, safety, and extended lifespan, alongside Nickel Manganese Cobalt (NMC) and Nickel Cobalt Aluminum (NCA) chemistries for higher energy density applications. The capacity segment of 40 kWh to 80 kWh is currently dominant, catering to a wide range of passenger cars and light commercial vehicles, while larger capacity packs are seeing increased adoption for longer-range vehicles.

China EV Battery Pack Market Market Size (In Billion)

The competitive landscape is characterized by the presence of formidable domestic players, including Contemporary Amperex Technology Co. Ltd. (CATL), FinDreams Battery Co. Ltd., and BYD Company Ltd. (through its battery division), who are at the forefront of innovation and production scale. The market is also influenced by ongoing trends such as the development of solid-state batteries, advancements in battery management systems (BMS), and the increasing emphasis on battery recycling and second-life applications to ensure sustainability. However, potential restraints such as fluctuations in raw material prices, particularly for lithium and cobalt, and the need for continuous technological upgrades to meet evolving performance demands, could pose challenges. The dominance of China in this market is undeniable, with the country serving as both a major producer and consumer of EV battery packs. The focus on battery components like cathodes, anodes, and electrolytes, along with material types such as lithium, nickel, and cobalt, highlights the intricate supply chain that underpins this dynamic market.

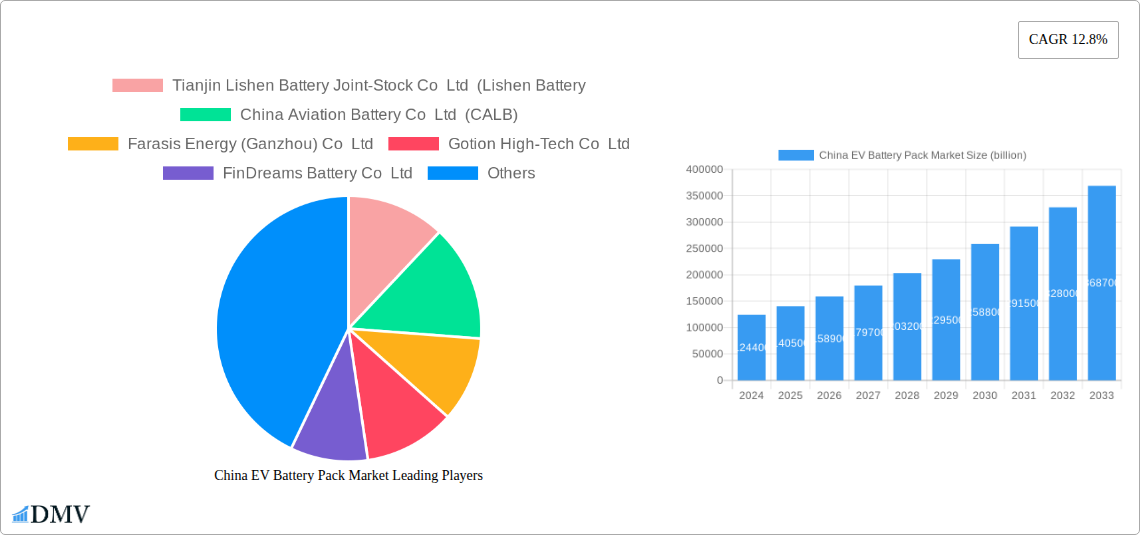

China EV Battery Pack Market Company Market Share

This in-depth report delves into the dynamic China EV battery pack market, providing a granular analysis of its current landscape and projecting its trajectory through 2033. As the global leader in electric vehicle adoption, China's battery pack industry is pivotal, driven by robust government support, technological innovation, and surging consumer demand for electric vehicles (EVs). This report offers critical insights for stakeholders, including manufacturers, suppliers, investors, and policymakers, equipping them with data-driven intelligence to navigate this rapidly evolving sector. We meticulously examine market segmentation, key players, technological advancements, and growth drivers, offering a definitive roadmap to understanding the future of China's EV battery pack market.

China EV Battery Pack Market Market Composition & Trends

The China EV battery pack market exhibits a moderate to high degree of concentration, with a few dominant players holding substantial market share, particularly CATL and BYD (FinDreams Battery). Innovation catalysts are manifold, stemming from intense R&D efforts focused on enhancing energy density, improving safety, reducing costs, and extending battery life. Regulatory landscapes, spearheaded by favorable government policies and stringent emission standards, continue to propel the adoption of EVs and, consequently, the demand for advanced battery packs. Substitute products, such as hydrogen fuel cells, are nascent but do not yet pose a significant threat to the established lithium-ion battery dominance. End-user profiles are increasingly diverse, ranging from individual car owners seeking sustainable transportation to fleet operators and commercial vehicle manufacturers optimizing operational efficiency. Mergers and acquisitions (M&A) activities are prevalent, driven by the pursuit of vertical integration, technological acquisition, and market expansion. For instance, recent M&A deals have been valued in the billions, aiming to consolidate supply chains and secure raw material access. Market share distribution is highly skewed, with the top three players commanding over 60% of the EV battery market share in China. The China EV battery pack market size is projected to reach multi-billion dollar valuations, underscoring its economic significance. The China battery market is characterized by continuous evolution and strategic consolidation.

China EV Battery Pack Market Industry Evolution

The China EV battery pack industry has witnessed an extraordinary evolutionary journey, transforming from a nascent sector to a global powerhouse. Over the historical period (2019-2024), the market experienced exponential growth, fueled by a confluence of government mandates, technological breakthroughs, and a rapidly expanding electric vehicle ecosystem. Early adoption was primarily driven by policy incentives, such as subsidies and tax breaks for EV purchases, which directly translated into a surge in demand for EV batteries in China. This period saw a significant shift in battery chemistry, with Lithium Iron Phosphate (LFP) batteries gaining considerable traction due to their cost-effectiveness, improved safety, and longer lifespan compared to earlier chemistries. The China battery manufacturing sector rapidly scaled up production capacity, leading to economies of scale and further cost reductions.

Technological advancements have been a constant feature of this evolution. From incremental improvements in energy density and charging speeds to the development of more sophisticated battery management systems (BMS), manufacturers have continuously pushed the boundaries of performance. The growth rate of China's EV battery market has consistently outpaced global averages, often exceeding 20% year-on-year. Adoption metrics for EVs, closely mirroring battery pack demand, have seen a similar upward trend, with the penetration rate of electric vehicles in China reaching significant milestones.

As the market matured, consumer demands began to evolve beyond mere affordability and range. Factors such as battery longevity, charging infrastructure accessibility, and the environmental impact of battery production and disposal have become increasingly important. This has spurred further innovation in areas like solid-state batteries and advanced recycling technologies. The China automotive battery market is no longer just about supplying cells; it's about offering integrated battery pack solutions that enhance the overall EV ownership experience. The base year of 2025 marks a crucial juncture, with the market expected to continue its robust growth trajectory, driven by these multifaceted factors. The future forecast period (2025-2033) anticipates sustained expansion, albeit potentially at a more moderated pace as the market matures and faces new challenges and opportunities. The industry's evolution is a testament to China's strategic vision in establishing a dominant position in the global new energy vehicle supply chain. The global EV battery market heavily relies on the innovations and production capabilities emanating from China.

Leading Regions, Countries, or Segments in China EV Battery Pack Market

Within the China EV battery pack market, several segments and regions stand out as dominant forces, shaping the overall market dynamics.

Dominant Propulsion Type: The Battery Electric Vehicle (BEV) segment overwhelmingly dominates the propulsion type landscape. This is a direct consequence of China's aggressive push towards zero-emission transportation and stringent regulations targeting internal combustion engine vehicles. BEVs represent over 85% of the new energy vehicle sales in China, driving substantial demand for high-capacity BEV battery packs. Plug-in Hybrid Electric Vehicles (PHEVs) hold a smaller but significant share, catering to a segment of consumers seeking a transitional solution. The market for PHEV battery packs is expected to grow, but at a slower pace than BEVs.

Dominant Battery Chemistry: Lithium Iron Phosphate (LFP) chemistry has emerged as the undisputed leader in the China EV battery pack market. Its advantages in terms of cost-effectiveness, safety, and thermal stability, coupled with advancements in energy density, have made it the preferred choice for a wide range of EV models, particularly in the mass-market passenger car segment. While Nickel Manganese Cobalt (NMC) and Nickel Cobalt Aluminum (NCA) chemistries still hold a share, especially in performance-oriented vehicles, the trend strongly favors LFP. The cost advantage of LFP batteries is a critical factor in driving down the overall cost of EVs, making them more accessible to a broader consumer base. The dominance of LFP is expected to persist throughout the forecast period.

Dominant Body Type: Passenger Cars constitute the largest segment by body type for EV battery packs in China. The sheer volume of passenger vehicle sales, coupled with government incentives and a growing consumer preference for personal mobility solutions, fuels this dominance. The LCV (Light Commercial Vehicle) and M&HDT (Medium & Heavy Duty Truck) segments are experiencing rapid growth, driven by the electrification of logistics and public transportation, but they still represent a smaller portion of the overall market compared to passenger cars. The bus segment also remains important, especially for public transportation electrification initiatives.

Dominant Battery Capacity Range: The 40 kWh to 80 kWh capacity range is currently the most prevalent for EV battery packs in China, catering to the typical range requirements of most passenger vehicles. However, there is a growing demand for Above 80 kWh capacity packs, driven by longer-range EVs and a desire for increased driving flexibility. The Less than 15 kWh and 15 kWh to 40 kWh segments are more relevant for smaller EVs, PHEVs, and specific commercial applications.

Dominant Battery Form Factor: Prismatic and Pouch battery forms are widely adopted in the China EV battery pack market. Prismatic cells offer good energy density and structural integrity, while pouch cells provide design flexibility and potentially better thermal management. Cylindrical cells are also used, particularly by some major players, but their market share is generally smaller compared to prismatic and pouch formats in passenger vehicles. The choice of form factor often depends on specific vehicle architecture and performance requirements.

Dominant Component & Material Type: The Cathode remains a critical and high-value component within the EV battery pack, with Lithium, Nickel, and Cobalt being key materials, though the emphasis is shifting towards reducing Cobalt content due to cost and ethical concerns. Natural Graphite is the predominant material for anodes. The increasing demand for LFP batteries means that Iron and Phosphate are also crucial materials. The supply chain for these materials, particularly lithium and nickel, is a key focus for ensuring market stability and growth.

Dominant Method: Laser welding is a widely adopted and advanced method for battery pack assembly and interconnection within the China EV battery pack manufacturing ecosystem, offering precision and reliability. Wire bonding is also used, particularly for specific applications and components.

The dominance of these segments is a result of strategic industry development, government policies favoring electrification, and the evolving needs of the Chinese automotive market. Investment trends are heavily focused on LFP technology and battery recycling, while regulatory support continues to be a primary driver of growth.

China EV Battery Pack Market Product Innovations

The China EV battery pack market is a hotbed of innovation, with continuous advancements aimed at improving performance, safety, and sustainability. Key product innovations include the development of higher energy density NCM and NCA chemistries, alongside breakthroughs in LFP battery technology that have significantly narrowed the performance gap with nickel-based chemistries while retaining cost advantages. Innovations in cell design, such as the integration of solid-state electrolytes, promise enhanced safety and faster charging capabilities. Manufacturers are also focusing on advanced battery management systems (BMS) that optimize performance, extend lifespan, and improve thermal management, crucial for the longevity and safety of EV battery packs. Furthermore, the industry is actively pursuing innovations in modular battery pack designs, enabling easier replacement, repair, and the potential for second-life applications. The integration of gigafactories and highly automated production lines is a key innovation in manufacturing, ensuring consistent quality and high output for the burgeoning China EV battery market. These innovations directly translate into enhanced driving range, faster charging times, and improved overall vehicle performance for consumers.

Propelling Factors for China EV Battery Pack Market Growth

Several key factors are propelling the robust growth of the China EV battery pack market. Foremost is the unwavering commitment from the Chinese government, evident through supportive policies, subsidies, and stringent emission standards that strongly favor electric vehicle adoption. Technological advancements in battery chemistry, energy density, and charging infrastructure are making EVs more practical and appealing to consumers. The rapidly expanding EV market in China, driven by both domestic and international manufacturers, directly fuels demand for EV battery packs. Economic factors, including decreasing battery costs due to economies of scale in manufacturing and the growing middle class's increasing purchasing power, further contribute. The development of a comprehensive EV charging network across the country is also a significant catalyst, alleviating range anxiety and encouraging wider EV adoption.

Obstacles in the China EV Battery Pack Market Market

Despite its impressive growth, the China EV battery pack market faces several obstacles. Supply chain disruptions, particularly concerning the availability and price volatility of key raw materials like lithium, nickel, and cobalt, pose a significant challenge. Regulatory shifts or a reduction in government subsidies could impact market growth, although the underlying demand trend remains strong. Intense competition among numerous battery manufacturers in China can lead to price wars and pressure on profit margins. Furthermore, ensuring battery safety and addressing concerns related to thermal runaway and fire risks remain ongoing challenges requiring continuous R&D and stringent quality control. The efficient and sustainable disposal and recycling of used EV batteries also presents a growing logistical and environmental hurdle that needs effective solutions.

Future Opportunities in China EV Battery Pack Market

The China EV battery pack market is ripe with future opportunities. The increasing demand for high-performance, long-range EVs presents a significant opportunity for advancements in battery chemistry and pack design, including the exploration of next-generation technologies like solid-state batteries. The expansion of the EV market into commercial vehicles, including trucks and buses, opens up new avenues for specialized battery solutions. The growing emphasis on sustainability creates opportunities for companies focusing on battery recycling and the development of ethically sourced materials. Furthermore, the global expansion of Chinese battery manufacturers presents opportunities to establish a dominant presence in international markets, leveraging their cost-efficiency and technological expertise. The development of innovative battery swapping solutions also represents a promising growth area, offering a convenient and rapid charging alternative.

Major Players in the China EV Battery Pack Market Ecosystem

- Contemporary Amperex Technology Co Ltd (CATL)

- BYD Co Ltd (FinDreams Battery Co Ltd)

- LG Energy Solution Ltd

- Panasonic Holdings Corporation

- SK On Co Ltd

- Samsung SDI Co Ltd

- EVE Energy Co Ltd

- Sunwoda Electric Vehicle Battery Co Ltd (Sunwoda)

- Gotion High-Tech Co Ltd

- Tianjin Lishen Battery Joint-Stock Co Ltd (Lishen Battery)

- China Aviation Battery Co Ltd (CALB)

- Farasis Energy (Ganzhou) Co Ltd

- SVOLT Energy Technology Co Ltd (SVOLT)

- Ruipu Energy Co Ltd

Key Developments in China EV Battery Pack Market Industry

- June 2023: CATL announced the signing of a strategic cooperation framework agreement with the Shenzhen Municipal People’s Government, focusing on New Energy Vehicle battery swapping, electric ships, new energy storage, green parks, financial services, and trade for all-round cooperation. This signals a deepening integration of battery technology with broader sustainable urban development initiatives.

- May 2023: Changan Auto disclosed that its battery cell joint venture (JV) with CATL will complete registration in the first half of 2023. The JV, primarily engaged in power battery cell production and manufacturing, is expected to be commissioned within 2023 with an impressive annual capacity of 25 GWh, significantly boosting domestic battery cell supply.

- May 2023: CATL announced a bank-enterprise strategic cooperation agreement signing ceremony with the Agricultural Bank of China (ABC). This partnership aims to deepen cooperation and innovate business models in battery swapping, overseas and domestic businesses, and green electricity and energy storage. This highlights the growing financial backing and strategic partnerships supporting the EV battery sector's expansion.

Strategic China EV Battery Pack Market Market Forecast

The China EV battery pack market is poised for continued strategic growth, driven by ongoing policy support and accelerating consumer adoption of electric vehicles. Forecasts indicate sustained demand, particularly for LFP battery packs due to their cost-effectiveness and improving performance, which will continue to make EVs more accessible. The push towards higher energy density and faster charging will fuel innovation in NCM/NCA chemistries and the nascent exploration of solid-state batteries. Significant opportunities lie in the electrification of commercial fleets and the development of advanced battery recycling infrastructure, addressing sustainability concerns. Strategic alliances and consolidation among major players, such as CATL and BYD, are expected to shape the market landscape, ensuring stable supply chains and driving technological advancements. The market's robust trajectory through 2033 is underpinned by a clear vision for a greener transportation future, with EV battery packs at its core.

China EV Battery Pack Market Segmentation

-

1. Body Type

- 1.1. Bus

- 1.2. LCV

- 1.3. M&HDT

- 1.4. Passenger Car

-

2. Propulsion Type

- 2.1. BEV

- 2.2. PHEV

-

3. Battery Chemistry

- 3.1. LFP

- 3.2. NCA

- 3.3. NCM

- 3.4. NMC

- 3.5. Others

-

4. Capacity

- 4.1. 15 kWh to 40 kWh

- 4.2. 40 kWh to 80 kWh

- 4.3. Above 80 kWh

- 4.4. Less than 15 kWh

-

5. Battery Form

- 5.1. Cylindrical

- 5.2. Pouch

- 5.3. Prismatic

-

6. Method

- 6.1. Laser

- 6.2. Wire

-

7. Component

- 7.1. Anode

- 7.2. Cathode

- 7.3. Electrolyte

- 7.4. Separator

-

8. Material Type

- 8.1. Cobalt

- 8.2. Lithium

- 8.3. Manganese

- 8.4. Natural Graphite

- 8.5. Nickel

- 8.6. Other Materials

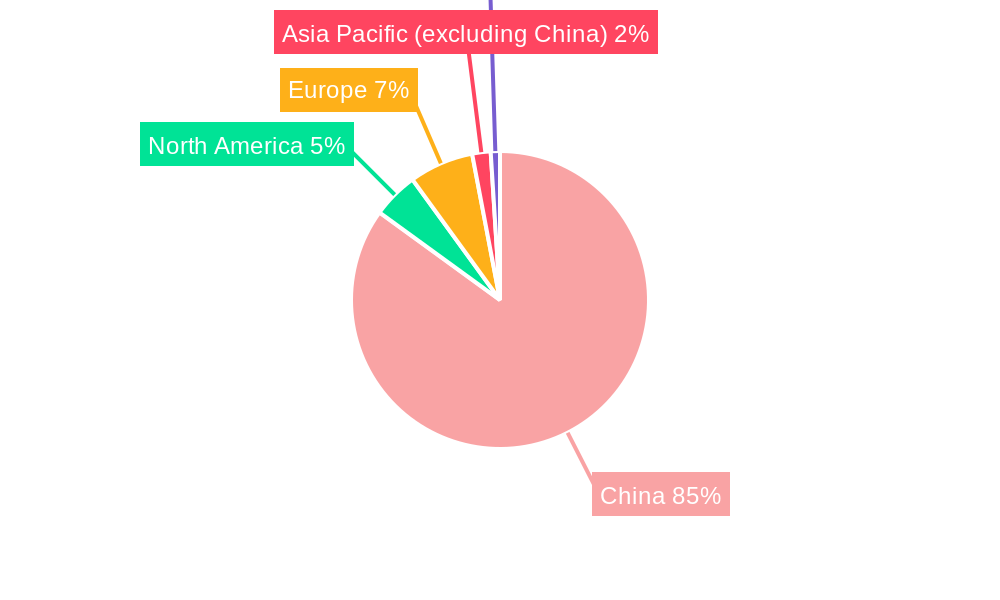

China EV Battery Pack Market Segmentation By Geography

- 1. China

China EV Battery Pack Market Regional Market Share

Geographic Coverage of China EV Battery Pack Market

China EV Battery Pack Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Body Type

- 5.1.1. Bus

- 5.1.2. LCV

- 5.1.3. M&HDT

- 5.1.4. Passenger Car

- 5.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.2.1. BEV

- 5.2.2. PHEV

- 5.3. Market Analysis, Insights and Forecast - by Battery Chemistry

- 5.3.1. LFP

- 5.3.2. NCA

- 5.3.3. NCM

- 5.3.4. NMC

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Capacity

- 5.4.1. 15 kWh to 40 kWh

- 5.4.2. 40 kWh to 80 kWh

- 5.4.3. Above 80 kWh

- 5.4.4. Less than 15 kWh

- 5.5. Market Analysis, Insights and Forecast - by Battery Form

- 5.5.1. Cylindrical

- 5.5.2. Pouch

- 5.5.3. Prismatic

- 5.6. Market Analysis, Insights and Forecast - by Method

- 5.6.1. Laser

- 5.6.2. Wire

- 5.7. Market Analysis, Insights and Forecast - by Component

- 5.7.1. Anode

- 5.7.2. Cathode

- 5.7.3. Electrolyte

- 5.7.4. Separator

- 5.8. Market Analysis, Insights and Forecast - by Material Type

- 5.8.1. Cobalt

- 5.8.2. Lithium

- 5.8.3. Manganese

- 5.8.4. Natural Graphite

- 5.8.5. Nickel

- 5.8.6. Other Materials

- 5.9. Market Analysis, Insights and Forecast - by Region

- 5.9.1. China

- 5.1. Market Analysis, Insights and Forecast - by Body Type

- 6. China EV Battery Pack Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Body Type

- 6.1.1. Bus

- 6.1.2. LCV

- 6.1.3. M&HDT

- 6.1.4. Passenger Car

- 6.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 6.2.1. BEV

- 6.2.2. PHEV

- 6.3. Market Analysis, Insights and Forecast - by Battery Chemistry

- 6.3.1. LFP

- 6.3.2. NCA

- 6.3.3. NCM

- 6.3.4. NMC

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by Capacity

- 6.4.1. 15 kWh to 40 kWh

- 6.4.2. 40 kWh to 80 kWh

- 6.4.3. Above 80 kWh

- 6.4.4. Less than 15 kWh

- 6.5. Market Analysis, Insights and Forecast - by Battery Form

- 6.5.1. Cylindrical

- 6.5.2. Pouch

- 6.5.3. Prismatic

- 6.6. Market Analysis, Insights and Forecast - by Method

- 6.6.1. Laser

- 6.6.2. Wire

- 6.7. Market Analysis, Insights and Forecast - by Component

- 6.7.1. Anode

- 6.7.2. Cathode

- 6.7.3. Electrolyte

- 6.7.4. Separator

- 6.8. Market Analysis, Insights and Forecast - by Material Type

- 6.8.1. Cobalt

- 6.8.2. Lithium

- 6.8.3. Manganese

- 6.8.4. Natural Graphite

- 6.8.5. Nickel

- 6.8.6. Other Materials

- 6.1. Market Analysis, Insights and Forecast - by Body Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Tianjin Lishen Battery Joint-Stock Co Ltd (Lishen Battery

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 China Aviation Battery Co Ltd (CALB)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Farasis Energy (Ganzhou) Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gotion High-Tech Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FinDreams Battery Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Contemporary Amperex Technology Co Ltd (CATL)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sunwoda Electric Vehicle Battery Co Ltd (Sunwoda)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 EVE Energy Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ruipu Energy Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 SVOLT Energy Technology Co Ltd (SVOLT)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Tianjin Lishen Battery Joint-Stock Co Ltd (Lishen Battery

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China EV Battery Pack Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China EV Battery Pack Market Share (%) by Company 2025

List of Tables

- Table 1: China EV Battery Pack Market Revenue billion Forecast, by Body Type 2020 & 2033

- Table 2: China EV Battery Pack Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 3: China EV Battery Pack Market Revenue billion Forecast, by Battery Chemistry 2020 & 2033

- Table 4: China EV Battery Pack Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 5: China EV Battery Pack Market Revenue billion Forecast, by Battery Form 2020 & 2033

- Table 6: China EV Battery Pack Market Revenue billion Forecast, by Method 2020 & 2033

- Table 7: China EV Battery Pack Market Revenue billion Forecast, by Component 2020 & 2033

- Table 8: China EV Battery Pack Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 9: China EV Battery Pack Market Revenue billion Forecast, by Region 2020 & 2033

- Table 10: China EV Battery Pack Market Revenue billion Forecast, by Body Type 2020 & 2033

- Table 11: China EV Battery Pack Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 12: China EV Battery Pack Market Revenue billion Forecast, by Battery Chemistry 2020 & 2033

- Table 13: China EV Battery Pack Market Revenue billion Forecast, by Capacity 2020 & 2033

- Table 14: China EV Battery Pack Market Revenue billion Forecast, by Battery Form 2020 & 2033

- Table 15: China EV Battery Pack Market Revenue billion Forecast, by Method 2020 & 2033

- Table 16: China EV Battery Pack Market Revenue billion Forecast, by Component 2020 & 2033

- Table 17: China EV Battery Pack Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 18: China EV Battery Pack Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China EV Battery Pack Market?

The projected CAGR is approximately 12.8%.

2. Which companies are prominent players in the China EV Battery Pack Market?

Key companies in the market include Tianjin Lishen Battery Joint-Stock Co Ltd (Lishen Battery, China Aviation Battery Co Ltd (CALB), Farasis Energy (Ganzhou) Co Ltd, Gotion High-Tech Co Ltd, FinDreams Battery Co Ltd, Contemporary Amperex Technology Co Ltd (CATL), Sunwoda Electric Vehicle Battery Co Ltd (Sunwoda), EVE Energy Co Ltd, Ruipu Energy Co Ltd, SVOLT Energy Technology Co Ltd (SVOLT).

3. What are the main segments of the China EV Battery Pack Market?

The market segments include Body Type, Propulsion Type, Battery Chemistry, Capacity, Battery Form, Method, Component, Material Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 124.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Travel and Tourism Industry is Driving the Car Rental Market.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Increasing Popularity of Ride-Sharing Services Pose Challenges for the Conventional Car Rental Market.

8. Can you provide examples of recent developments in the market?

June 2023: CATL announced the signing of a strategic cooperation framework agreement with the Shenzhen Municipal People’s Government. The two parties will focus on such key fields as New Energy Vehicle battery swapping, electric ships, new energy storage, green parks, financial services, and trade for all-round cooperation.May 2023: Changan Auto recently disclosed that the battery cell joint venture (JV) between it and CATL will complete registration in the first half of 2023. The JV will mainly be engaged in the production and manufacturing of power battery cells and is expected to be commissioned within 2023, with an annual capacity as high as 25 GWh.May 2023: CATL announced the holding of a bank-enterprise strategic cooperation agreement signing ceremony with the Agricultural Bank of China (ABC). With the agreement signed, the two parties will deepen cooperation to continuously innovate cooperation models in such fields as battery swapping business, overseas and domestic businesses, and green electricity and energy storage businesses.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China EV Battery Pack Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China EV Battery Pack Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China EV Battery Pack Market?

To stay informed about further developments, trends, and reports in the China EV Battery Pack Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence