Key Insights

The global market for automotive metal pipes is poised for robust expansion, driven by increasing vehicle production and the growing demand for advanced fluid transfer systems. Valued at approximately $15 billion in 2025, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of around 7.5% from 2025 to 2033, reaching an estimated $28 billion by the end of the forecast period. This growth is primarily fueled by the surging automotive industry, particularly in emerging economies, and the increasing adoption of complex engine technologies that necessitate sophisticated and durable fluid conveyance solutions. The rising production of both commercial vehicles and passenger cars, coupled with a sustained focus on enhancing vehicle performance and safety, directly contributes to the sustained demand for metal pipes, including metal hoses and metal hard tubes.

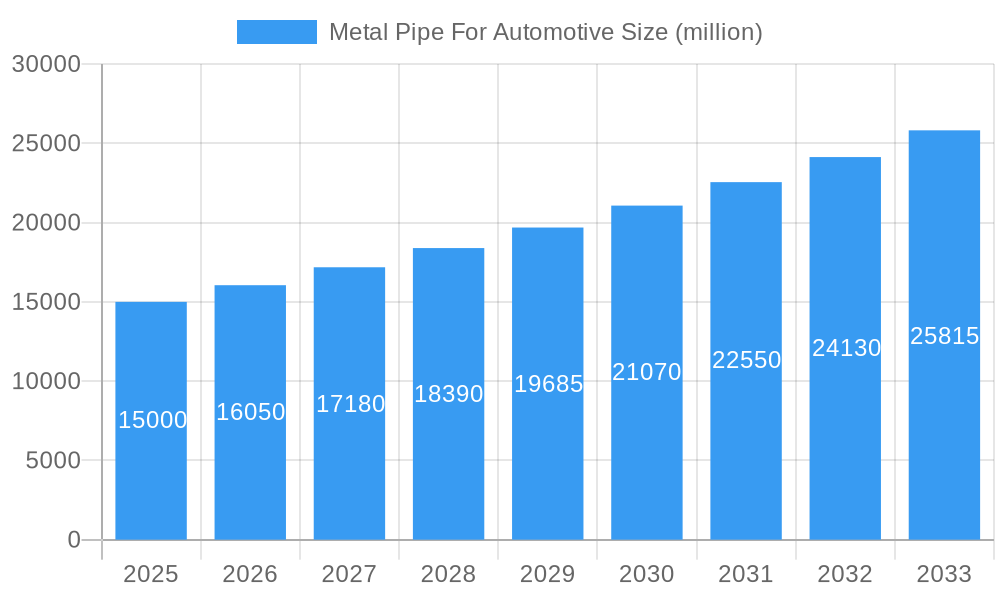

Metal Pipe For Automotive Market Size (In Billion)

The market dynamics are further shaped by several key trends. A significant driver is the ongoing technological evolution in the automotive sector, including the development of electric vehicles (EVs) and hybrid powertrains. While EVs might reduce the need for traditional fuel lines, they introduce new requirements for thermal management systems and battery cooling, which often utilize specialized metal tubing. Furthermore, stringent emission regulations worldwide are pushing automakers to adopt more efficient and reliable exhaust systems, as well as advanced fuel injection and cooling technologies, all of which rely heavily on high-quality metal piping. Despite this positive outlook, the market faces certain restraints. Fluctuations in raw material prices, particularly for stainless steel and aluminum, can impact manufacturing costs. Additionally, the increasing adoption of lightweight materials and alternative fluid transfer solutions, such as advanced polymers, presents a competitive challenge. Nonetheless, the inherent durability, heat resistance, and pressure handling capabilities of metal pipes ensure their continued relevance and dominance in many critical automotive applications. The market is segmented into commercial vehicle and passenger vehicle applications, with metal hoses and metal hard tubes representing the key product types.

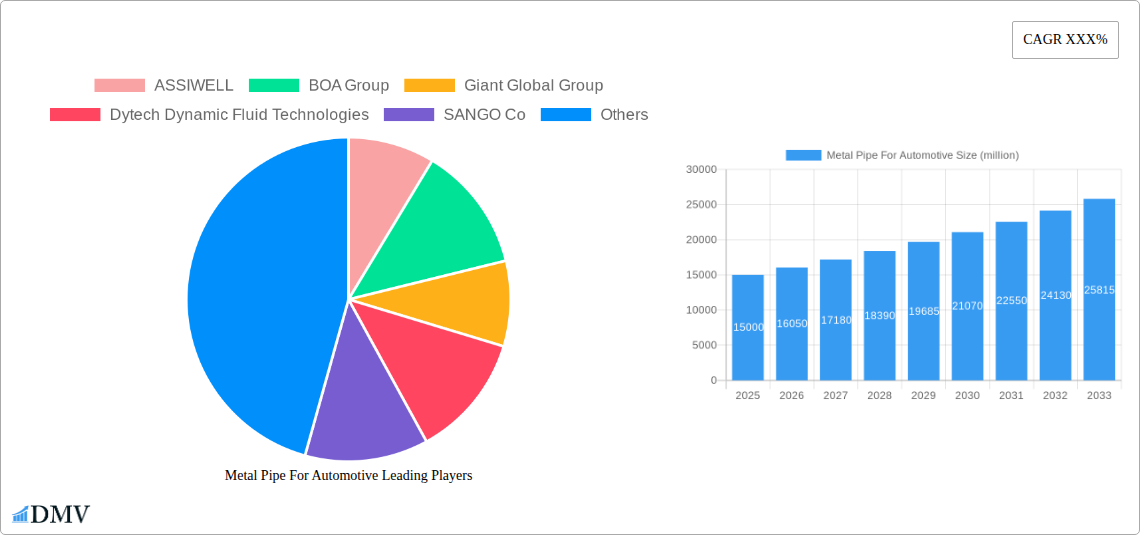

Metal Pipe For Automotive Company Market Share

Metal Pipe For Automotive Market Composition & Trends

The global metal pipe for automotive market is characterized by a moderate concentration of key players, with ASSIWELL, BOA Group, Giant Global Group, Dytech Dynamic Fluid Technologies, SANGO Co, Witzenmann, Usui Co, TI Automotive, Ningbo Felix Auto Parts, Zhejiang Modobacks Technology, Ningbo Fushi Auto Parts, Changzhou Changlian Corrugated Pipe, Guangdong Shuangxing New Materials Group, Jiangsu Oulang Automotive Piping System, Jiangsu Sujia Group, and Zhongshan Hesheng Auto Parts collectively holding a significant market share. Innovation catalysts are primarily driven by the relentless pursuit of lightweight materials, enhanced durability, and improved fluid transfer efficiency, particularly for emission control systems and advanced powertrain technologies. The regulatory landscape is increasingly stringent, with a growing emphasis on environmental compliance, vehicle safety standards, and material recyclability, influencing product development and manufacturing processes. Substitute products, such as high-performance polymers and advanced composites, pose a competitive challenge but often fall short in extreme temperature or high-pressure applications where metal pipes remain indispensable. End-user profiles are diverse, encompassing automotive OEMs, tier-1 and tier-2 suppliers, and aftermarket service providers, all demanding robust and cost-effective solutions. Mergers and acquisitions (M&A) activity is present, albeit strategic rather than consolidative, often focused on acquiring specialized technologies or expanding geographical reach. For instance, a notable M&A deal in 2023 involved a transaction valued at an estimated $500 million, aimed at integrating advanced manufacturing capabilities. The market share distribution sees Metal Hard Tube segments holding approximately 65% of the total market value, while Metal Hose applications account for the remaining 35%.

Metal Pipe For Automotive Industry Evolution

The metal pipe for automotive industry has witnessed a transformative evolution over the historical period of 2019–2024, with a projected compound annual growth rate (CAGR) of approximately 5.2% from the base year of 2025 through to 2033. This sustained growth is intrinsically linked to the burgeoning global automotive production volumes, particularly in emerging economies. The industry has actively embraced technological advancements, transitioning from traditional steel and aluminum alloys to more sophisticated materials like stainless steel, titanium, and advanced high-strength steels (AHSS). These material innovations are crucial for meeting the increasing demand for lightweighting to improve fuel efficiency and reduce emissions in both Commercial Vehicles and Passenger Vehicles. The adoption of advanced manufacturing techniques, such as precision welding, hydroforming, and advanced coating technologies, has significantly enhanced the performance characteristics of automotive metal pipes, leading to improved corrosion resistance, higher pressure handling capabilities, and extended product lifecycles. Furthermore, the industry is responding to shifting consumer demands, with a growing preference for vehicles that are not only fuel-efficient but also equipped with robust and reliable fluid transfer systems that support advanced functionalities like turbocharging, direct injection, and sophisticated exhaust gas recirculation (EGR) systems. The increasing complexity of vehicle architectures necessitates specialized metal piping solutions that can withstand a wider range of operating temperatures and pressures. For example, the adoption rate of advanced stainless steel alloys for exhaust systems has increased by an estimated 15% annually since 2021 due to stricter emission norms. Similarly, the demand for specialized metal hoses for hydraulic braking and power steering systems has seen a consistent growth of around 4% per annum, driven by the increasing prevalence of advanced driver-assistance systems (ADAS) that rely on precise fluid control. The market's trajectory is further influenced by the ongoing electrification trend in the automotive sector; while electric vehicles (EVs) may reduce the demand for certain engine-related fluid transfer components, they introduce new requirements for thermal management systems, battery cooling, and high-voltage cabling protection, areas where specialized metal pipes and hoses are increasingly finding application. The market's overall expansion is underscored by consistent investments in research and development aimed at creating lighter, stronger, and more cost-effective metal piping solutions.

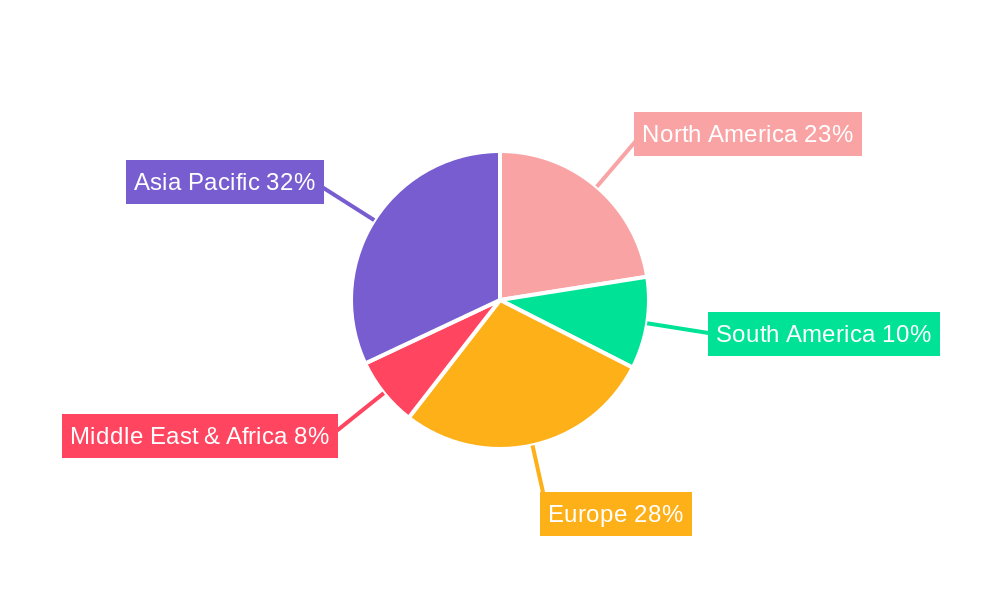

Leading Regions, Countries, or Segments in Metal Pipe For Automotive

The global metal pipe for automotive market exhibits a clear dominance in the Asia-Pacific region, driven by its position as the world's largest automotive manufacturing hub. This dominance is further amplified by the significant presence of key players like Giant Global Group, Ningbo Felix Auto Parts, Zhejiang Modobacks Technology, Ningbo Fushi Auto Parts, Changzhou Changlian Corrugated Pipe, Guangdong Shuangxing New Materials Group, Jiangsu Oulang Automotive Piping System, and Jiangsu Sujia Group, all contributing to the region's robust production and supply capabilities.

Key Drivers of Dominance in Asia-Pacific

- Massive Automotive Production: Asia-Pacific is home to the highest volume of vehicle production globally, encompassing both Commercial Vehicle and Passenger Vehicle segments, creating an insatiable demand for automotive metal pipes.

- Favorable Regulatory Environment: While increasingly stringent, the regulatory frameworks in countries like China and India are often supportive of domestic manufacturing and industrial growth, fostering a conducive environment for local players.

- Cost-Effective Manufacturing: The region offers a competitive cost structure for manufacturing, allowing for the production of high-quality metal pipes at attractive price points, further bolstering its export capabilities.

- Growing Domestic Consumption: A rapidly expanding middle class in countries like China and India is driving domestic demand for new vehicles, directly translating into increased consumption of automotive components.

- Technological Adoption: Local manufacturers are increasingly investing in advanced technologies and R&D to meet global quality standards and develop specialized products for evolving automotive needs.

Within the Asia-Pacific region, China stands out as the undisputed leader, accounting for over 40% of the global market share. Its sheer scale of vehicle production, coupled with a well-developed supply chain and a significant number of domestic metal pipe manufacturers, solidifies its position. This dominance is further fueled by extensive investment trends in the automotive sector, with both domestic and international OEMs establishing and expanding their manufacturing footprints. The country’s strong focus on developing advanced manufacturing capabilities and its pivotal role in global automotive supply chains directly contribute to its leadership in metal pipe production and consumption.

In terms of Application, the Passenger Vehicle segment represents the largest market share, estimated at approximately 70% of the total metal pipe for automotive market value. This is attributed to the sheer volume of passenger cars manufactured globally and the diverse range of fluid transfer systems required, including fuel lines, brake lines, exhaust systems, and cooling systems. The Commercial Vehicle segment, while smaller in volume, represents a significant market due to the higher complexity and more demanding operating conditions of components used in trucks, buses, and other heavy-duty vehicles, leading to a higher average revenue per unit.

Analyzing by Type, Metal Hard Tube holds a dominant position, constituting around 65% of the market. These tubes are critical for applications requiring high structural integrity and precise fluid conveyance, such as fuel delivery, brake systems, and power steering. Metal Hose segments, while smaller at approximately 35%, are essential for applications requiring flexibility and vibration absorption, such as exhaust systems, turbocharger connections, and hydraulic systems, and are experiencing robust growth due to advancements in flexible metal tubing technology.

Metal Pipe For Automotive Product Innovations

Product innovations in the metal pipe for automotive sector are driven by the imperative for enhanced performance, durability, and sustainability. Manufacturers are introducing lightweight alloys, such as advanced aluminum composites and high-strength stainless steels, to reduce vehicle weight and improve fuel efficiency, contributing to an estimated 10% reduction in the weight of exhaust systems. Developments include multi-layer metal pipes with advanced coatings for superior corrosion resistance, extending component life by up to 20% in harsh environments. Innovations in manufacturing processes, such as precision hydroforming, enable the creation of complex geometries for optimized fluid flow and thermal management, critical for modern turbocharged engines and EV battery cooling systems. The integration of sensor-compatible materials and designs is also a growing trend, facilitating real-time performance monitoring.

Propelling Factors for Metal Pipe For Automotive Growth

Several key factors are propelling the growth of the metal pipe for automotive market. Technologically, the increasing demand for lightweighting in vehicles to improve fuel efficiency and reduce emissions is a primary driver, pushing for the adoption of advanced alloys. Economically, the consistent growth in global automotive production, particularly in emerging markets, directly translates to higher demand for these essential components. Regulatory influences, such as stricter emission standards and safety regulations worldwide, necessitate the use of more robust and high-performance metal piping solutions to meet these evolving requirements. For example, the introduction of Euro 7 emission standards in Europe is driving the development of advanced exhaust system piping.

Obstacles in the Metal Pipe For Automotive Market

Despite robust growth, the metal pipe for automotive market faces several obstacles. Regulatory challenges, particularly concerning the sourcing of raw materials and compliance with evolving environmental regulations, can increase operational costs. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can impact production schedules and cost-effectiveness. Competitive pressures from alternative materials like high-performance polymers and composites, especially for less demanding applications, also pose a challenge, although metal pipes retain an advantage in extreme temperature and high-pressure scenarios. Furthermore, the increasing complexity of vehicle architectures can lead to higher tooling and development costs for specialized metal pipe designs.

Future Opportunities in Metal Pipe For Automotive

Emerging opportunities in the metal pipe for automotive market are multifaceted. The rapid growth of electric vehicles (EVs) presents a significant opportunity for specialized metal pipes and hoses used in battery thermal management systems, power electronics cooling, and robust cable protection. The increasing integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies requires sophisticated fluid and sensor conveyance systems, creating demand for specialized metal tubing. Furthermore, the growing aftermarket segment for vehicle repairs and upgrades, particularly in developing economies, offers a sustained revenue stream. The development of bio-based or recycled metal alloys for enhanced sustainability is also an emerging area with significant potential.

Major Players in the Metal Pipe For Automotive Ecosystem

- ASSIWELL

- BOA Group

- Giant Global Group

- Dytech Dynamic Fluid Technologies

- SANGO Co

- Witzenmann

- Usui Co

- TI Automotive

- Ningbo Felix Auto Parts

- Zhejiang Modobacks Technology

- Ningbo Fushi Auto Parts

- Changzhou Changlian Corrugated Pipe

- Guangdong Shuangxing New Materials Group

- Jiangsu Oulang Automotive Piping System

- Jiangsu Sujia Group

- Zhongshan Hesheng Auto Parts

Key Developments in Metal Pipe For Automotive Industry

- 2023/07: TI Automotive expands its North American manufacturing capabilities with a new facility focusing on advanced fuel line systems.

- 2023/04: BOA Group announces a strategic partnership with an EV startup to develop specialized thermal management piping solutions.

- 2023/01: Witzenmann introduces a new generation of lightweight, high-temperature resistant metal hoses for turbocharger applications.

- 2022/11: Giant Global Group acquires a smaller competitor specializing in precision metal tube bending to enhance its product portfolio.

- 2022/08: SANGO Co. launches a new series of corrosion-resistant stainless steel pipes for heavy-duty commercial vehicle exhaust systems.

- 2022/05: Ningbo Felix Auto Parts invests significantly in automated welding technology to improve production efficiency and quality.

- 2022/02: Dytech Dynamic Fluid Technologies showcases innovative flexible metal hose solutions for emerging autonomous vehicle sensor integration.

- 2021/10: Usui Co. receives an award for its groundbreaking lightweight aluminum alloy tubing for passenger vehicles.

- 2021/07: Zhejiang Modobacks Technology announces a breakthrough in plasma-based coating technology for enhanced pipe durability.

Strategic Metal Pipe For Automotive Market Forecast

The strategic metal pipe for automotive market forecast indicates sustained growth driven by the automotive industry's ongoing transition towards electrification, enhanced safety features, and stricter environmental regulations. The increasing demand for lightweighting and high-performance materials will continue to favor advanced metal alloys and innovative manufacturing processes. Opportunities in thermal management systems for EVs and robust fluid conveyance for autonomous driving technologies present significant growth avenues. Regional expansion, particularly in emerging automotive markets, coupled with strategic investments in research and development, will be crucial for stakeholders to capitalize on the evolving landscape and maintain a competitive edge. The market is poised for an estimated market size of over $XX million by 2033.

Metal Pipe For Automotive Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Vehicle

-

2. Type

- 2.1. Metal Hose

- 2.2. Metal Hard Tube

Metal Pipe For Automotive Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Metal Pipe For Automotive Regional Market Share

Geographic Coverage of Metal Pipe For Automotive

Metal Pipe For Automotive REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Metal Pipe For Automotive Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Metal Hose

- 5.2.2. Metal Hard Tube

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Metal Pipe For Automotive Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Metal Hose

- 6.2.2. Metal Hard Tube

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Metal Pipe For Automotive Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Metal Hose

- 7.2.2. Metal Hard Tube

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Metal Pipe For Automotive Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Metal Hose

- 8.2.2. Metal Hard Tube

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Metal Pipe For Automotive Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Metal Hose

- 9.2.2. Metal Hard Tube

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Metal Pipe For Automotive Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Metal Hose

- 10.2.2. Metal Hard Tube

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ASSIWELL

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BOA Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Giant Global Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Dytech Dynamic Fluid Technologies

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SANGO Co

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Witzenmann

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Usui Co

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 TI Automotive

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ningbo Felix Auto Parts

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Zhejiang Modobacks Technology

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Ningbo Fushi Auto Parts

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Changzhou Changlian Corrugated Pipe

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Guangdong Shuangxing New Materials Group

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Jiangsu Oulang Automotive Piping System

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Jiangsu Sujia Group

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Zhongshan Hesheng Auto Parts

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 ASSIWELL

List of Figures

- Figure 1: Global Metal Pipe For Automotive Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Metal Pipe For Automotive Revenue (million), by Application 2025 & 2033

- Figure 3: North America Metal Pipe For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Metal Pipe For Automotive Revenue (million), by Type 2025 & 2033

- Figure 5: North America Metal Pipe For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Metal Pipe For Automotive Revenue (million), by Country 2025 & 2033

- Figure 7: North America Metal Pipe For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Metal Pipe For Automotive Revenue (million), by Application 2025 & 2033

- Figure 9: South America Metal Pipe For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Metal Pipe For Automotive Revenue (million), by Type 2025 & 2033

- Figure 11: South America Metal Pipe For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Metal Pipe For Automotive Revenue (million), by Country 2025 & 2033

- Figure 13: South America Metal Pipe For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Metal Pipe For Automotive Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Metal Pipe For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Metal Pipe For Automotive Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Metal Pipe For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Metal Pipe For Automotive Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Metal Pipe For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Metal Pipe For Automotive Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Metal Pipe For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Metal Pipe For Automotive Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Metal Pipe For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Metal Pipe For Automotive Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Metal Pipe For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Metal Pipe For Automotive Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Metal Pipe For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Metal Pipe For Automotive Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Metal Pipe For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Metal Pipe For Automotive Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Metal Pipe For Automotive Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Metal Pipe For Automotive Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Metal Pipe For Automotive Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Metal Pipe For Automotive Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Metal Pipe For Automotive Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Metal Pipe For Automotive Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Metal Pipe For Automotive Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Metal Pipe For Automotive Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Metal Pipe For Automotive Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Metal Pipe For Automotive Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Metal Pipe For Automotive Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Metal Pipe For Automotive Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Metal Pipe For Automotive Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Metal Pipe For Automotive Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Metal Pipe For Automotive Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Metal Pipe For Automotive Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Metal Pipe For Automotive Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Metal Pipe For Automotive Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Metal Pipe For Automotive Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Metal Pipe For Automotive Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Metal Pipe For Automotive?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Metal Pipe For Automotive?

Key companies in the market include ASSIWELL, BOA Group, Giant Global Group, Dytech Dynamic Fluid Technologies, SANGO Co, Witzenmann, Usui Co, TI Automotive, Ningbo Felix Auto Parts, Zhejiang Modobacks Technology, Ningbo Fushi Auto Parts, Changzhou Changlian Corrugated Pipe, Guangdong Shuangxing New Materials Group, Jiangsu Oulang Automotive Piping System, Jiangsu Sujia Group, Zhongshan Hesheng Auto Parts.

3. What are the main segments of the Metal Pipe For Automotive?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Metal Pipe For Automotive," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Metal Pipe For Automotive report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Metal Pipe For Automotive?

To stay informed about further developments, trends, and reports in the Metal Pipe For Automotive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence