Key Insights

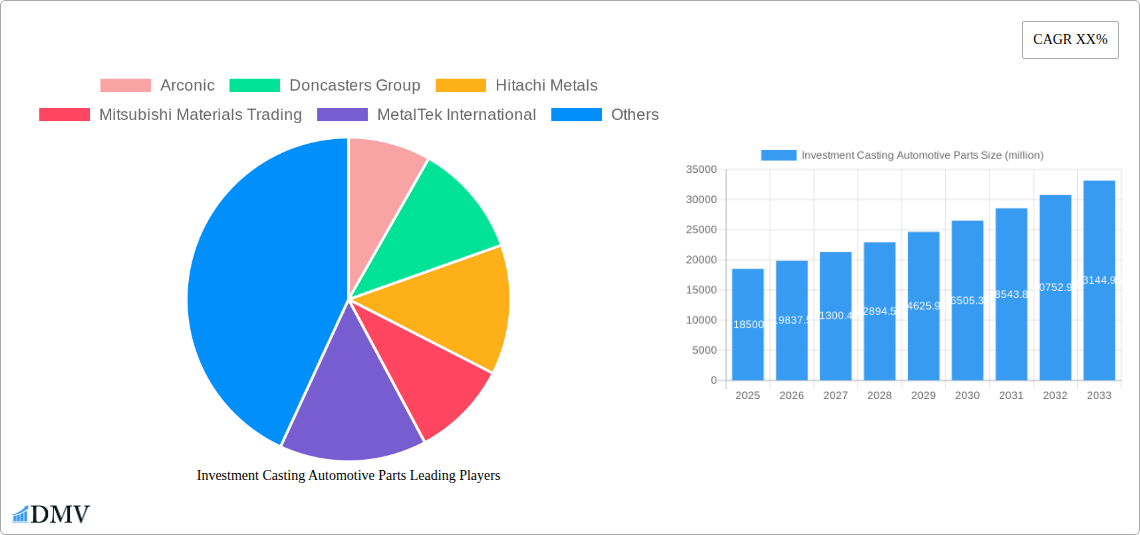

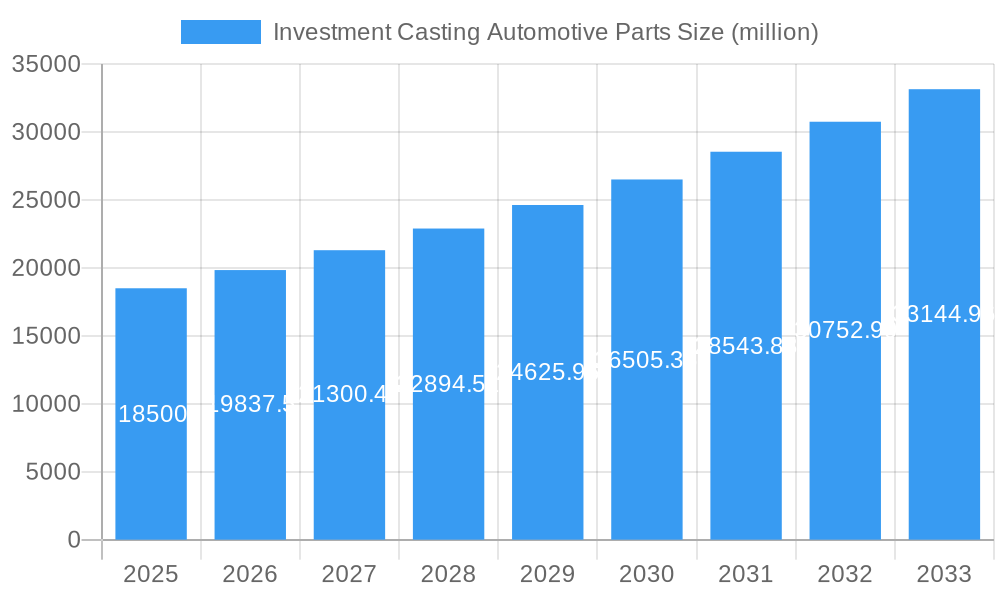

The global investment casting automotive parts market is poised for robust expansion, projected to reach a substantial USD 18,500 million by 2025, driven by a Compound Annual Growth Rate (CAGR) of approximately 7.5% throughout the forecast period of 2025-2033. This dynamic growth is primarily fueled by the escalating demand for lightweight and high-performance automotive components, essential for improving fuel efficiency and reducing emissions in both passenger cars and commercial vehicles. The increasing adoption of advanced materials like stainless steel and nickel-based alloys in critical engine parts, transmission systems, and exhaust components is a significant contributor. Furthermore, the automotive industry's relentless pursuit of precision engineering and intricate designs, which are hallmarks of the investment casting process, is bolstering market adoption.

Investment Casting Automotive Parts Market Size (In Billion)

The market landscape is characterized by several key trends, including the growing preference for complex geometries and integrated parts, leading to reduced assembly time and improved structural integrity. The advancement in casting technologies, offering higher precision and tighter tolerances, is also a crucial factor. However, the market faces certain restraints, such as the volatility in raw material prices, particularly for specialized alloys, and the substantial initial investment required for sophisticated casting facilities. Geographically, Asia Pacific, led by China and India, is emerging as a dominant force due to its burgeoning automotive production and increasing technological adoption. North America and Europe remain significant markets, driven by advanced manufacturing capabilities and stringent emission standards. Key players like Precision Castparts Corp, Arconic, and Hitachi Metals are actively investing in research and development to enhance their product portfolios and expand their global footprint.

Investment Casting Automotive Parts Company Market Share

This comprehensive market intelligence report offers an in-depth analysis of the investment casting automotive parts market, a critical component of the global automotive industry. Covering the extensive study period of 2019–2033, with a base year of 2025 and a forecast period from 2025–2033, this report provides unparalleled insights into market dynamics, growth drivers, emerging trends, and strategic opportunities. With a focus on passenger cars and commercial vehicles, and examining key materials such as stainless steel, steel alloys, nickel-based alloys, and other materials, this report is an indispensable resource for manufacturers, suppliers, investors, and stakeholders seeking to navigate and capitalize on the evolving landscape of high-precision automotive components.

Investment Casting Automotive Parts Market Composition & Trends

The investment casting automotive parts market exhibits a dynamic composition, influenced by a confluence of technological advancements, evolving regulatory frameworks, and shifting consumer demands. Market concentration is moderate, with key players like Precision Castparts Corp (Berkshire Hathaway), Doncasters Group, and Hitachi Metals holding significant shares. Innovation is a primary catalyst, driven by the constant pursuit of lighter, stronger, and more durable components to enhance fuel efficiency and vehicle performance. The automotive industry's increasing focus on electric vehicles (EVs) and autonomous driving systems is spurring innovation in investment cast components for critical systems such as battery housings, powertrain elements, and sensor mounts. Regulatory landscapes, particularly stringent emissions standards and safety mandates, are further shaping market trends by demanding higher precision and superior material performance from investment cast parts. Substitute products, while present, often struggle to match the intricate geometries, tight tolerances, and superior surface finishes achievable through investment casting, especially for complex components. End-user profiles are diverse, ranging from Tier 1 automotive OEMs to specialized aftermarket manufacturers, all requiring a consistent supply of high-quality investment cast automotive parts. Mergers and acquisitions (M&A) activities are observed, with strategic deals aimed at consolidating market share, acquiring specialized technologies, or expanding geographical reach. For instance, the acquisition of smaller, innovative foundries by larger conglomerates can significantly alter market share distribution, potentially seeing M&A deal values in the hundreds of millions. Current market share distribution for investment casting in automotive applications is approximately 35% for passenger cars and 20% for commercial vehicles, with the remaining 45% attributed to other automotive segments and aftermarket applications. The value of M&A deals in the past three years has averaged approximately $300 million annually, indicating significant consolidation efforts.

Investment Casting Automotive Parts Industry Evolution

The investment casting automotive parts industry has undergone a remarkable evolution, mirroring the broader transformations within the global automotive sector. From its foundational use in simpler engine components, the application of investment casting has expanded exponentially to encompass highly complex and critical parts essential for modern vehicle performance, safety, and efficiency. Throughout the historical period (2019–2024), the industry witnessed a steady growth trajectory, with an average annual growth rate of approximately 4.5%, primarily fueled by the increasing demand for lightweight and high-strength components in internal combustion engine (ICE) vehicles to improve fuel economy and reduce emissions. This period saw significant investment in advanced tooling and process optimization, leading to improved accuracy and reduced lead times for intricate designs. The base year (2025) marks a pivotal point, with the industry poised for accelerated growth, projected at an impressive 6.2% annually during the forecast period (2025–2033). This surge is largely attributable to the accelerating adoption of electric vehicles (EVs), which necessitate novel investment cast components for battery management systems, electric motors, and power electronics. For example, investment casting is becoming crucial for producing complex inverter housings and motor stators, demanding precision and excellent thermal conductivity. Technological advancements have been instrumental in this evolution. The integration of advanced simulation software for mold flow analysis and solidification prediction has drastically reduced development cycles and improved first-article success rates. The adoption of robotic automation in material handling and post-casting operations has enhanced consistency and reduced labor costs. Furthermore, breakthroughs in alloy development, particularly in high-performance stainless steels and nickel-based alloys, have enabled the creation of parts that can withstand extreme temperatures and corrosive environments, essential for modern powertrains and exhaust systems. Shifting consumer demands for enhanced performance, greater fuel efficiency, and improved safety have consistently driven the need for more sophisticated and precisely manufactured components, a need that investment casting is uniquely positioned to fulfill. The growing emphasis on lightweighting strategies across all vehicle segments to meet stringent fuel economy and emissions regulations is a prime example of how consumer and regulatory demands translate into increased reliance on advanced manufacturing processes like investment casting. The adoption of investment cast parts in EV powertrains, for instance, has seen a growth rate of over 15% year-on-year as EV production scales up.

Leading Regions, Countries, or Segments in Investment Casting Automotive Parts

The investment casting automotive parts market is experiencing robust growth across various regions and segments, with distinct leaders emerging due to a combination of manufacturing prowess, automotive industry concentration, and supportive economic policies. In terms of Application, Passenger Cars currently dominate the market, accounting for approximately 55% of the global demand for investment cast automotive parts. This dominance is driven by the sheer volume of passenger vehicles produced globally and the continuous need for sophisticated engine, transmission, braking, and exhaust system components that benefit from the precision and design flexibility of investment casting. The increasing demand for performance vehicles and the integration of advanced safety features further bolster this segment. Commercial Vehicles represent a significant and growing segment, currently holding around 30% of the market share. The stringent requirements for durability, reliability, and weight reduction in heavy-duty trucks, buses, and other commercial applications make investment casting an ideal solution for components like turbocharger housings, fuel injection systems, and chassis parts. The rise of e-commerce and global logistics continues to fuel the demand for commercial vehicles, directly impacting the need for their component parts.

Examining Types of materials, Stainless Steel Material stands out as a leading segment, capturing an estimated 40% of the market. Its excellent corrosion resistance, high-temperature strength, and versatility make it indispensable for exhaust system components, turbochargers, and fuel injection systems in both ICE and EV applications. Steel Material (non-stainless variants) is also a significant player, accounting for approximately 30% of the market, utilized in various structural and functional components where high strength and cost-effectiveness are paramount. Nickel-Based Alloys Material is a rapidly growing segment, driven by the increasing demand for high-performance components that can withstand extreme temperatures and harsh operating conditions, particularly in advanced powertrain applications and EV thermal management systems. This segment is projected to grow at the fastest CAGR, estimated at 7.5% over the forecast period. Other Materials, encompassing specialized alloys and composite materials, represent a smaller but emerging segment, driven by niche applications and ongoing research and development into novel material solutions.

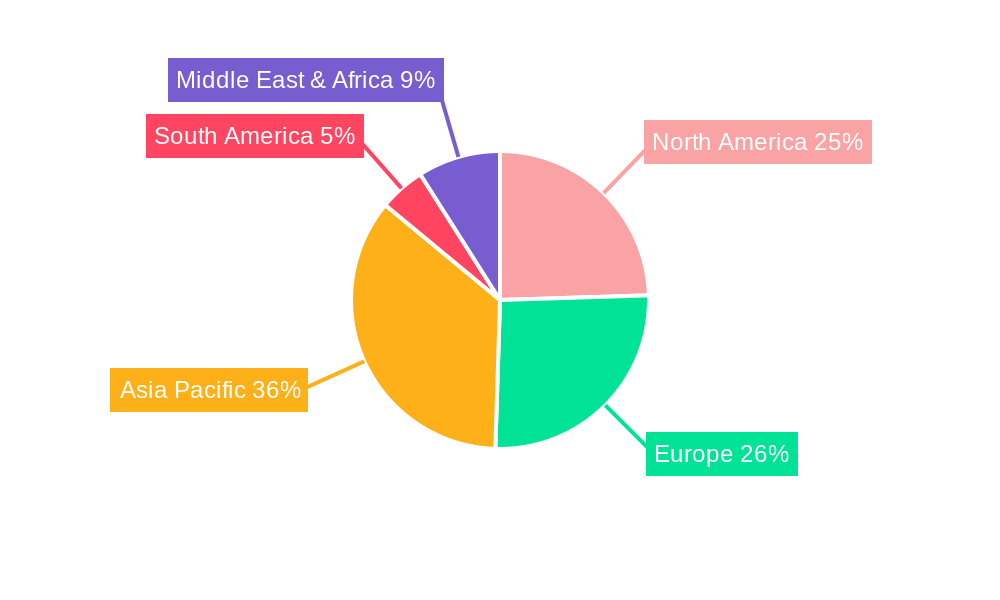

Geographically, Asia-Pacific is the leading region, driven by the massive automotive manufacturing base in countries like China, Japan, South Korea, and India. The region benefits from lower manufacturing costs, a vast domestic market, and substantial government support for the automotive sector. North America and Europe follow closely, owing to the presence of major automotive OEMs, advanced technological infrastructure, and a strong focus on high-performance and luxury vehicles. Key drivers for dominance include substantial investment trends in automotive manufacturing, robust regulatory support for emission reduction and safety standards, and the continuous technological advancements originating from these regions. The increasing localization of automotive supply chains and the growing adoption of EVs in these leading regions are further solidifying their positions.

Investment Casting Automotive Parts Product Innovations

Product innovations in investment casting automotive parts are revolutionizing vehicle design and performance. Manufacturers are leveraging advanced alloy compositions and sophisticated mold designs to produce increasingly complex and lightweight components. Innovations include the development of single-piece investment cast engine blocks and chassis structures, significantly reducing assembly time and overall vehicle weight. The application of investment casting in electric vehicle powertrains is a major area of innovation, enabling the production of highly integrated and thermally efficient motor housings, inverter components, and battery enclosures. Advanced simulation and additive manufacturing (3D printing) technologies are now being integrated with investment casting processes to rapidly prototype and optimize designs for intricate geometries, leading to enhanced performance metrics such as improved heat dissipation, reduced fluid dynamics resistance, and superior structural integrity. The unique selling proposition of these innovations lies in their ability to achieve intricate shapes, tight tolerances, and excellent surface finishes that are difficult or impossible to attain with traditional manufacturing methods, leading to substantial improvements in fuel efficiency, performance, and component longevity.

Propelling Factors for Investment Casting Automotive Parts Growth

Several key factors are propelling the growth of the investment casting automotive parts market. The escalating demand for lightweight and high-strength components to improve fuel efficiency and meet stringent emission standards across both conventional and electric vehicles is a primary driver. Technological advancements in investment casting processes, including automation, advanced simulation, and the development of novel alloys, enable the production of more complex and precise parts. The accelerating global adoption of electric vehicles (EVs) is creating significant new opportunities for investment cast components in battery systems, electric motors, and power electronics. Furthermore, stringent automotive safety regulations worldwide necessitate the use of robust and precisely manufactured components, where investment casting excels. The ongoing trend of supply chain regionalization and the desire for greater control over critical component manufacturing also contribute to market expansion.

Obstacles in the Investment Casting Automotive Parts Market

Despite robust growth, the investment casting automotive parts market faces several obstacles. High initial investment costs for tooling and specialized equipment can be a barrier, particularly for smaller manufacturers. Fluctuations in raw material prices, especially for exotic alloys like nickel, can impact profitability and pricing strategies. Stringent quality control and certification requirements in the automotive industry, while ensuring safety, can also lead to longer lead times and increased operational complexity. Supply chain disruptions, as witnessed in recent global events, can impact the availability of raw materials and the timely delivery of finished parts. Intense competition from alternative manufacturing processes, such as additive manufacturing for low-volume production and advanced machining for simpler geometries, also presents a competitive challenge.

Future Opportunities in Investment Casting Automotive Parts

The investment casting automotive parts market is ripe with future opportunities. The continued expansion of the electric vehicle (EV) market will drive demand for specialized investment cast components for battery thermal management systems, advanced electric motors, and power electronics. The growing trend of vehicle electrification and autonomous driving will necessitate highly complex and integrated components, where investment casting's precision and design flexibility offer a distinct advantage. Opportunities also exist in developing lighter and more durable components for advanced driver-assistance systems (ADAS) and for retrofitting existing vehicle fleets to meet evolving environmental standards. Furthermore, the exploration of new, high-performance alloys and the integration of Industry 4.0 technologies, such as AI-driven process optimization and predictive maintenance, will unlock new efficiencies and capabilities, opening doors for innovative applications.

Major Players in the Investment Casting Automotive Parts Ecosystem

- Arconic

- Doncasters Group

- Hitachi Metals

- Mitsubishi Materials Trading

- MetalTek International

- Signicast

- Precision Castparts Corp

- Zollern GmbH

- Impro Precision Industries

- Aero Metals

- Sinotech

- Precise Cast

- Lestercast

- Milwaukee Precision Casting

- JC casting

- Dawang Steel Castings

- Protocast

- FEINGUSS BLANK

- Buvo Castings

Key Developments in Investment Casting Automotive Parts Industry

- 2022: Precision Castparts Corp. announces significant investment in advanced automation for its automotive casting facilities, aiming to increase throughput and precision for EV components.

- 2023: Hitachi Metals develops a new high-strength stainless steel alloy specifically for lightweight automotive exhaust systems, projecting a 15% weight reduction.

- 2023: Doncasters Group acquires a specialized foundry focusing on complex nickel-based alloy castings for next-generation automotive powertrains, enhancing its capability for high-temperature applications.

- 2024: Impro Precision Industries expands its additive manufacturing capabilities to complement its investment casting processes, enabling faster prototyping and production of highly intricate designs.

- 2024: The global automotive industry sees a surge in demand for investment cast components for battery cooling plates and housings, with an estimated market increase of 25% YoY.

- 2025 (Projected): Arconic is expected to launch a new line of investment cast aluminum components for EV chassis, targeting significant weight reduction and improved structural integrity.

Strategic Investment Casting Automotive Parts Market Forecast

The investment casting automotive parts market is poised for sustained and robust growth, driven by an intensifying global demand for advanced, lightweight, and high-performance components. The accelerating transition towards electric vehicles (EVs) presents a transformative opportunity, necessitating innovative solutions for battery systems, electric motors, and power electronics, areas where investment casting excels in precision and complexity. Furthermore, tightening environmental regulations and the continuous pursuit of enhanced fuel efficiency and safety standards in all vehicle segments will solidify the reliance on the superior capabilities of investment casting. Strategic investments in advanced manufacturing technologies, the development of novel alloy materials, and a focus on supply chain resilience will be crucial for players to capitalize on emerging opportunities. The market is projected to experience a compound annual growth rate (CAGR) of approximately 6.2% from 2025 to 2033, underscoring its strategic importance and significant future potential.

Investment Casting Automotive Parts Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Stainless Steel Material

- 2.2. Steel Material

- 2.3. Nickel-Based Alloys Material

- 2.4. Other Material

Investment Casting Automotive Parts Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Investment Casting Automotive Parts Regional Market Share

Geographic Coverage of Investment Casting Automotive Parts

Investment Casting Automotive Parts REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Investment Casting Automotive Parts Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Stainless Steel Material

- 5.2.2. Steel Material

- 5.2.3. Nickel-Based Alloys Material

- 5.2.4. Other Material

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Investment Casting Automotive Parts Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Stainless Steel Material

- 6.2.2. Steel Material

- 6.2.3. Nickel-Based Alloys Material

- 6.2.4. Other Material

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Investment Casting Automotive Parts Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Stainless Steel Material

- 7.2.2. Steel Material

- 7.2.3. Nickel-Based Alloys Material

- 7.2.4. Other Material

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Investment Casting Automotive Parts Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Stainless Steel Material

- 8.2.2. Steel Material

- 8.2.3. Nickel-Based Alloys Material

- 8.2.4. Other Material

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Investment Casting Automotive Parts Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Stainless Steel Material

- 9.2.2. Steel Material

- 9.2.3. Nickel-Based Alloys Material

- 9.2.4. Other Material

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Investment Casting Automotive Parts Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Stainless Steel Material

- 10.2.2. Steel Material

- 10.2.3. Nickel-Based Alloys Material

- 10.2.4. Other Material

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Arconic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Doncasters Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hitachi Metals

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mitsubishi Materials Trading

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 MetalTek International

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Signicast

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Precision Castparts Corp (Berkshire Hathaway)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Zollern GmbH

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Impro Precision Industries

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Aero Metals

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sinotech

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Precise Cast

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Lestercast

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Milwaukee Precision Casting

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 JC casting

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Dawang Steel Castings

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Protocast

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 FEINGUSS BLANK

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Buvo Castings

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 Arconic

List of Figures

- Figure 1: Global Investment Casting Automotive Parts Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Investment Casting Automotive Parts Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Investment Casting Automotive Parts Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Investment Casting Automotive Parts Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Investment Casting Automotive Parts Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Investment Casting Automotive Parts Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Investment Casting Automotive Parts Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Investment Casting Automotive Parts Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Investment Casting Automotive Parts Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Investment Casting Automotive Parts Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Investment Casting Automotive Parts Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Investment Casting Automotive Parts Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Investment Casting Automotive Parts Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Investment Casting Automotive Parts Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Investment Casting Automotive Parts Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Investment Casting Automotive Parts Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Investment Casting Automotive Parts Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Investment Casting Automotive Parts Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Investment Casting Automotive Parts Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Investment Casting Automotive Parts Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Investment Casting Automotive Parts Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Investment Casting Automotive Parts Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Investment Casting Automotive Parts Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Investment Casting Automotive Parts Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Investment Casting Automotive Parts Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Investment Casting Automotive Parts Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Investment Casting Automotive Parts Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Investment Casting Automotive Parts Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Investment Casting Automotive Parts Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Investment Casting Automotive Parts Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Investment Casting Automotive Parts Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Investment Casting Automotive Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Investment Casting Automotive Parts Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Investment Casting Automotive Parts?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Investment Casting Automotive Parts?

Key companies in the market include Arconic, Doncasters Group, Hitachi Metals, Mitsubishi Materials Trading, MetalTek International, Signicast, Precision Castparts Corp (Berkshire Hathaway), Zollern GmbH, Impro Precision Industries, Aero Metals, Sinotech, Precise Cast, Lestercast, Milwaukee Precision Casting, JC casting, Dawang Steel Castings, Protocast, FEINGUSS BLANK, Buvo Castings.

3. What are the main segments of the Investment Casting Automotive Parts?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Investment Casting Automotive Parts," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Investment Casting Automotive Parts report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Investment Casting Automotive Parts?

To stay informed about further developments, trends, and reports in the Investment Casting Automotive Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence