Key Insights

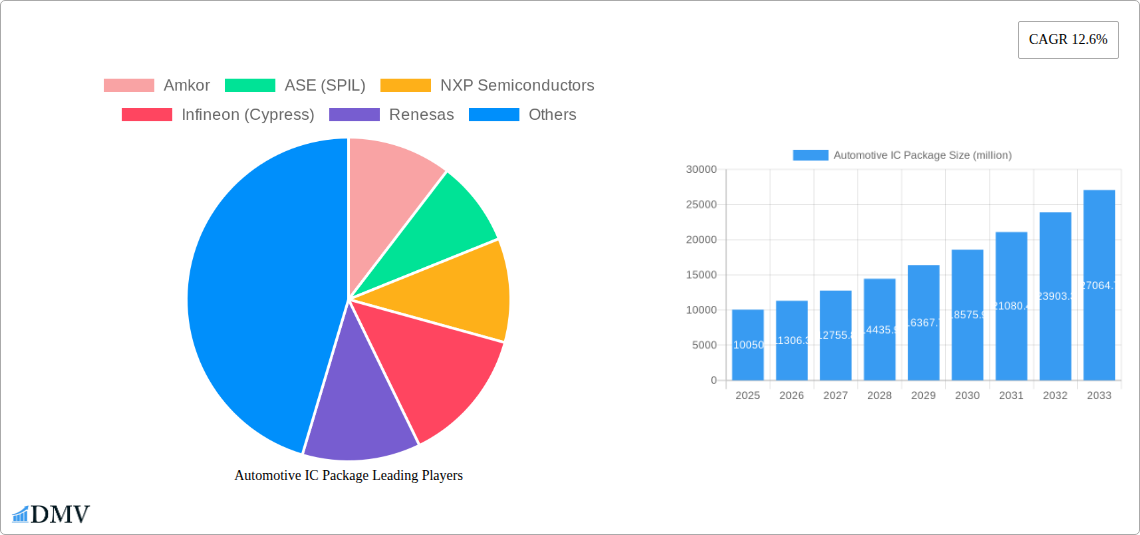

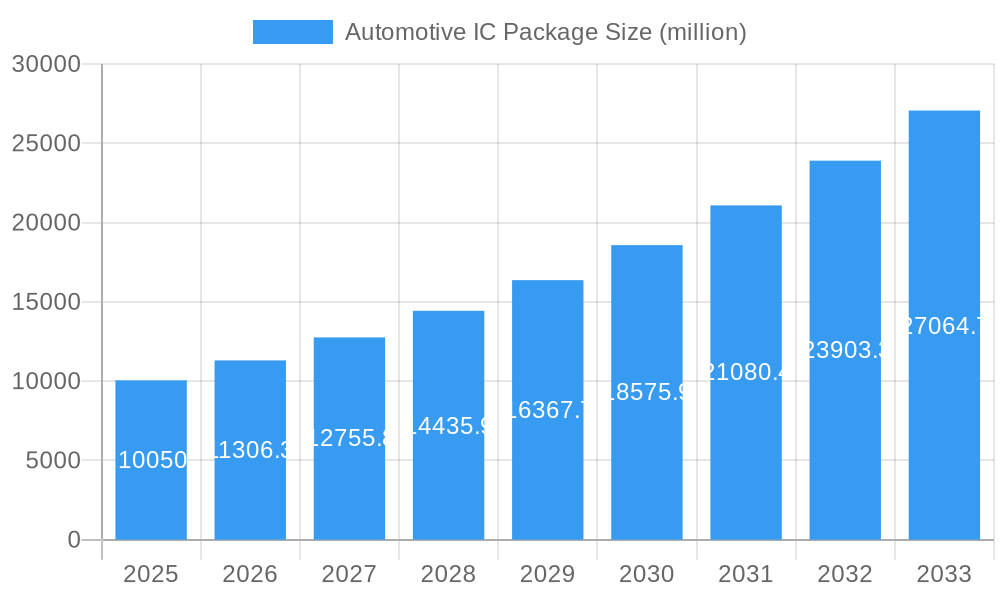

The global Automotive IC Package market is poised for significant expansion, projected to reach $10,050 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 12.6% anticipated from 2025 to 2033. This remarkable growth is propelled by the escalating demand for advanced driver-assistance systems (ADAS), autonomous driving technologies, and the increasing semiconductor content within vehicles. The transition towards electric vehicles (EVs), which inherently require more sophisticated electronic components for battery management, power control, and infotainment, further fuels this market. Key drivers include the relentless pursuit of enhanced vehicle safety features, the growing adoption of connected car technologies, and the miniaturization and higher performance demands for automotive integrated circuits (ICs). Furthermore, the expansion of automotive electronics across mainstream and advanced packaging segments underscores the diverse applications driving market momentum.

Automotive IC Package Market Size (In Billion)

The market is characterized by a dynamic interplay between Original Semiconductor Assembly and Test (OSAT) providers and Integrated Device Manufacturers (IDMs). While OSATs are crucial for handling the increasing complexity and volume of packaging needs, IDMs are heavily invested in developing next-generation solutions. Trends such as the adoption of wafer-level packaging, 3D packaging, and advanced materials are critical for meeting the stringent reliability and performance requirements of the automotive sector. Despite the optimistic outlook, certain restraints may emerge, including potential supply chain disruptions for critical raw materials, escalating manufacturing costs, and the need for continuous innovation to keep pace with rapid technological advancements in the automotive industry. However, the industry's strategic focus on miniaturization, increased functionality, and enhanced thermal management solutions for automotive ICs will likely outweigh these challenges, ensuring sustained market expansion.

Automotive IC Package Company Market Share

Automotive IC Package Market Composition & Trends

The global Automotive IC Package market is characterized by a dynamic concentration of leading players, with significant contributions from both established Integrated Device Manufacturers (IDMs) and specialized Outsourced Semiconductor Assembly and Test (OSAT) providers. Innovation is a key catalyst, driven by the insatiable demand for enhanced automotive functionalities, including advanced driver-assistance systems (ADAS), in-car infotainment, and electrification. The market's growth trajectory is further shaped by evolving regulatory landscapes, particularly concerning vehicle safety standards and emissions, which necessitate increasingly sophisticated semiconductor solutions. Substitute products, while emerging, face substantial hurdles in matching the performance and reliability demanded by the automotive sector. End-user profiles span from Tier-1 automotive suppliers integrating complex electronic modules to original equipment manufacturers (OEMs) demanding high-performance, robust semiconductor components. Mergers and acquisitions (M&A) activities continue to reshape the competitive landscape, with deal values reaching several million dollars as companies strategically consolidate their offerings and expand their market reach. For instance, in the historical period of 2019-2024, a significant number of M&A deals, collectively valued at over $500 million, have occurred. Market share distribution shows a healthy, yet competitive, environment, with the top five players holding approximately 70% of the market in 2025. The increasing complexity of automotive electronics, from autonomous driving to connected car technologies, fuels a continuous push for advanced packaging solutions, driving innovation and strategic collaborations.

Automotive IC Package Industry Evolution

The Automotive IC Package industry has witnessed a profound evolution, transforming from a niche segment to a critical enabler of modern vehicle technology. The study period, spanning from 2019 to 2033, encapsulates a remarkable growth trajectory, propelled by relentless technological advancements and an ever-increasing sophistication in consumer demands for automotive features. In the historical period (2019-2024), the market experienced a compound annual growth rate (CAGR) of approximately 12%, driven by the initial wave of ADAS adoption and the burgeoning electric vehicle (EV) market. As we enter the base year of 2025, the market is estimated to reach over $15,000 million, a testament to its significant expansion. The forecast period (2025-2033) anticipates sustained growth, with projections indicating a CAGR of over 10%, pushing the market value to well over $30,000 million by 2033. This expansion is intrinsically linked to the increasing semiconductor content per vehicle, which is rapidly climbing from an average of over $500 in 2020 to an estimated over $1,000 by 2025, and projected to exceed $2,000 by 2030.

Technological advancements have been the bedrock of this evolution. The shift towards advanced packaging techniques, such as wafer-level packaging (WLP), 2.5D and 3D integration, and system-in-package (SiP) solutions, has been paramount. These innovations enable higher power density, improved thermal management, reduced form factors, and enhanced performance, all critical for automotive applications operating under extreme conditions. For example, the adoption of advanced packaging for automotive microcontrollers (MCUs) has seen a rise from 20% in 2019 to an estimated 50% by 2025, with projections to reach over 75% by 2033.

Shifting consumer demands have acted as a powerful catalyst. The desire for safer, more connected, and more autonomous vehicles has directly translated into a higher demand for sophisticated electronic components. Features like adaptive cruise control, lane-keeping assist, autonomous parking, and advanced infotainment systems rely heavily on powerful processors, sensors, and memory, all requiring specialized and reliable IC packaging. The increasing penetration of EVs, with their complex power management and battery control systems, further amplifies the need for robust and high-performance semiconductor solutions, hence driving the demand for specialized automotive IC packages. The growing emphasis on in-vehicle connectivity, including 5G integration and over-the-air updates, also necessitates advanced packaging to support higher bandwidth and lower latency requirements. The overall market growth is therefore a confluence of technological innovation, evolving regulatory mandates, and the ever-increasing sophistication of automotive electronics driven by consumer preferences.

Leading Regions, Countries, or Segments in Automotive IC Package

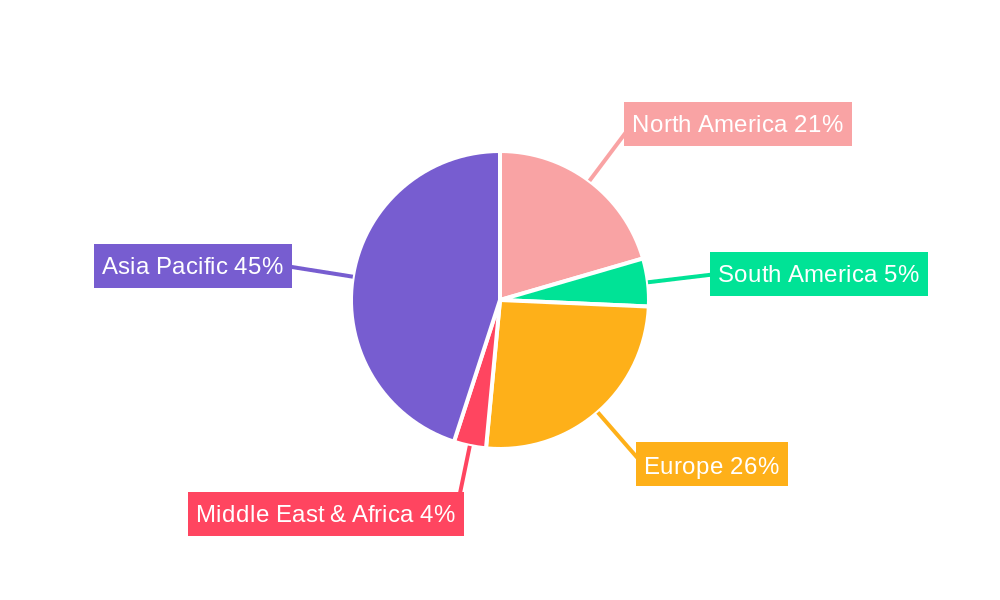

The dominance within the Automotive IC Package market is multifaceted, with key regions, countries, and application segments exhibiting significant influence. Asia-Pacific, particularly China, South Korea, and Taiwan, stands as the leading region, driven by its robust semiconductor manufacturing infrastructure and the presence of major OSAT players. These regions are critical hubs for both advanced and mainstream packaging technologies, catering to the massive automotive production volumes in the vicinity.

Application Segments Dominance:

- Advanced Packaging: This segment is witnessing the most rapid growth and is increasingly becoming the focus for high-performance automotive applications.

- Key Drivers: The relentless pursuit of higher processing power, enhanced thermal performance, and miniaturization for ADAS, autonomous driving, and electric vehicle powertrains are primary drivers.

- Dominance Factors: Regions with strong R&D capabilities and significant investments in advanced manufacturing processes, such as flip-chip, WLP, and 3D IC integration, are leading this segment. Major IDMs and OSATs in East Asia are at the forefront. The market share of advanced packaging is projected to grow from an estimated 40% in 2025 to over 60% by 2033.

- Mainstream Packaging: While advanced packaging garners significant attention, mainstream packaging solutions continue to hold a substantial market share, particularly for less critical but high-volume automotive components.

- Key Drivers: Cost-effectiveness, proven reliability, and widespread availability make mainstream packages suitable for a broad range of automotive applications, including infotainment, body control modules, and basic safety systems.

- Dominance Factors: Regions with a strong manufacturing base for traditional packaging techniques and a large volume of standard automotive component production, such as Southeast Asia and parts of Europe, maintain significant presence. This segment is estimated to hold approximately 60% of the market in 2025, gradually declining as advanced solutions become more accessible.

Types Dominance:

- Automotive OSAT (Outsourced Semiconductor Assembly and Test): OSATs are pivotal to the industry, offering specialized packaging and testing services to a wide array of semiconductor manufacturers.

- Key Drivers: Their flexibility, scalability, and expertise in handling complex packaging requirements for automotive applications make them indispensable. The increasing outsourcing trend by IDMs further bolsters their position.

- Dominance Factors: Companies like ASE (SPIL), Amkor, and JCET (STATS ChipPAC) based in Asia-Pacific hold a commanding market share. Their ability to offer a diverse portfolio of advanced and mainstream packaging solutions tailored for the automotive sector is a key differentiator. The Automotive OSAT segment is projected to account for over 70% of the overall automotive IC packaging market by 2033.

- Automotive IDM (Integrated Device Manufacturer): IDMs, while increasingly outsourcing, continue to play a crucial role by developing and packaging their own high-performance automotive ICs.

- Key Drivers: Control over the entire semiconductor value chain, proprietary technologies, and specialized design expertise enable IDMs to offer integrated solutions.

- Dominance Factors: Major players like NXP Semiconductors, Infineon (Cypress), Renesas, and TI (Texas Instruments) possess strong in-house packaging capabilities for their critical automotive offerings. They often focus on developing cutting-edge packaging solutions for their flagship processors and sensors. While their direct share might be less than OSATs, their influence in driving packaging innovation is substantial.

Geographically, North America and Europe remain significant markets due to their strong automotive R&D presence and stringent safety regulations, driving demand for advanced packaging. However, Asia-Pacific's sheer manufacturing volume and the presence of major semiconductor foundries and OSATs solidify its leading position.

Automotive IC Package Product Innovations

Product innovations in automotive IC packaging are primarily focused on enhancing reliability, thermal management, and miniaturization to meet the stringent demands of in-vehicle environments. Technologies like advanced leadframe packages, flip-chip configurations with underfill, and wafer-level chip-scale packages (WLCSP) are increasingly prevalent. These innovations enable higher power handling capabilities, improved signal integrity, and reduced form factors, crucial for densely populated automotive electronic control units (ECUs). For instance, the development of fan-out wafer-level packaging (FOWLP) allows for the integration of multiple dies into a single package, significantly reducing size and cost for complex automotive processors and sensors used in ADAS. Performance metrics such as operating temperature ranges extending beyond 150°C, enhanced vibration resistance exceeding 50g, and extremely low failure rates (FIT rates in the low single digits) are key selling propositions, ensuring these packages can withstand harsh automotive conditions.

Propelling Factors for Automotive IC Package Growth

Several key factors are propelling the growth of the Automotive IC Package market. The exponential rise in vehicle electrification, with an increasing demand for power-efficient and high-performance semiconductors in electric vehicles (EVs), is a major driver. Advanced Driver-Assistance Systems (ADAS) and the burgeoning trend towards autonomous driving necessitate sophisticated processing power and sensor integration, requiring advanced packaging solutions for enhanced functionality and reliability. Furthermore, stringent automotive safety regulations worldwide mandate increasingly complex electronic systems, thereby fueling the demand for specialized IC packages. The continuous integration of connectivity features, including 5G, in-vehicle infotainment, and the Internet of Things (IoT) applications, also contributes significantly to market expansion.

Obstacles in the Automotive IC Package Market

Despite the robust growth, the Automotive IC Package market faces several obstacles. The highly demanding reliability standards and long qualification cycles for automotive-grade components represent a significant barrier to entry and innovation. Supply chain disruptions, exacerbated by geopolitical tensions and the global semiconductor shortage, continue to pose challenges for material procurement and production output, potentially impacting market availability and pricing. The increasing cost of advanced packaging technologies, while offering performance benefits, can also be a restraint for certain mainstream automotive applications. Furthermore, the intense competition among OSAT providers and IDMs can lead to price pressures, impacting profit margins.

Future Opportunities in Automotive IC Package

Emerging opportunities in the Automotive IC Package market are abundant and diverse. The widespread adoption of Level 3 and Level 4 autonomous driving technologies will spur demand for high-performance computing chips and advanced sensor fusion modules, requiring cutting-edge packaging solutions. The growth of in-vehicle networking and the increasing demand for immersive infotainment experiences will drive the need for high-bandwidth and low-latency communication packages. The continued expansion of the EV market, with its intricate power electronics and battery management systems, presents a substantial opportunity for specialized power IC packaging. Furthermore, the development of new materials and manufacturing techniques, such as heterogeneous integration and advanced thermal management solutions, opens avenues for innovation and market differentiation.

Major Players in the Automotive IC Package Ecosystem

- Amkor

- ASE (SPIL)

- NXP Semiconductors

- Infineon (Cypress)

- Renesas

- TI (Texas Instruments)

- STMicroelectronics

- onsemi

- UTAC

- Bosch

- Rohm

- ADI (Analog Devices, Inc)

- JCET (STATS ChipPAC)

- Mitsubishi Electric

- Carsem

- Tongfu Microelectronics (TFME)

- King Yuan Electronics Corp. (KYEC)

- Powertech Technology Inc. (PTI)

- Microchip (Microsemi)

- Unisem Group

- SFA Semicon

- Forehope Electronic (Ningbo) Co.,Ltd.

- Toshiba

- BYD

- Zhuzhou CRRC Times Electric

- China Resources Microelectronics Limited

- Hangzhou Silan Microelectronics

- Rapidus

Key Developments in Automotive IC Package Industry

- 2023 Q4: Amkor announces expansion of its advanced packaging capabilities for automotive applications, including SiP solutions.

- 2024 Q1: ASE (SPIL) reports significant growth in its automotive packaging segment, driven by demand for ADAS and EV components.

- 2024 Q2: NXP Semiconductors introduces new high-performance processors with integrated advanced packaging for autonomous driving.

- 2024 Q3: Infineon (Cypress) unveils a new range of automotive-grade microcontrollers optimized for advanced packaging solutions.

- 2024 Q4: Renesas expands its partnerships with OSATs to accelerate the development of next-generation automotive IC packages.

- 2025 Q1: TI (Texas Instruments) highlights increased investment in its automotive packaging R&D, focusing on thermal management.

- 2025 Q2: STMicroelectronics announces a strategic collaboration for advanced wafer-level packaging for automotive sensors.

- 2025 Q3: onsemi showcases its latest power IC packaging solutions for electric vehicle powertrains.

- 2025 Q4: UTAC reveals plans to increase its capacity for automotive OSAT services.

Strategic Automotive IC Package Market Forecast

The Automotive IC Package market is poised for robust and sustained growth over the forecast period. Key growth catalysts include the accelerating adoption of electric vehicles, the increasing sophistication of autonomous driving technologies, and the growing demand for advanced connectivity and infotainment systems in vehicles. Strategic investments in advanced packaging technologies by major players, coupled with supportive government regulations promoting automotive safety and emissions standards, will further fuel market expansion. Emerging markets and new automotive trends, such as in-car digital health monitoring, also present significant future opportunities, promising a dynamic and evolving landscape for automotive IC packaging. The market is projected to witness a CAGR of over 10% from 2025 to 2033.

Automotive IC Package Segmentation

-

1. Application

- 1.1. Advanced Packaging

- 1.2. Mainstream Packaging

-

2. Types

- 2.1. Automotive OSAT

- 2.2. Automotive IDM

Automotive IC Package Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive IC Package Regional Market Share

Geographic Coverage of Automotive IC Package

Automotive IC Package REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive IC Package Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Advanced Packaging

- 5.1.2. Mainstream Packaging

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Automotive OSAT

- 5.2.2. Automotive IDM

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive IC Package Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Advanced Packaging

- 6.1.2. Mainstream Packaging

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Automotive OSAT

- 6.2.2. Automotive IDM

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive IC Package Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Advanced Packaging

- 7.1.2. Mainstream Packaging

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Automotive OSAT

- 7.2.2. Automotive IDM

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive IC Package Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Advanced Packaging

- 8.1.2. Mainstream Packaging

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Automotive OSAT

- 8.2.2. Automotive IDM

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive IC Package Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Advanced Packaging

- 9.1.2. Mainstream Packaging

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Automotive OSAT

- 9.2.2. Automotive IDM

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive IC Package Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Advanced Packaging

- 10.1.2. Mainstream Packaging

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Automotive OSAT

- 10.2.2. Automotive IDM

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Amkor

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ASE (SPIL)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 NXP Semiconductors

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Infineon (Cypress)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Renesas

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 TI (Texas Instruments)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 STMicroelectronics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 onsemi

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 UTAC

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Bosch

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Rohm

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ADI (Analog Devices

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Inc)

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 JCET (STATS ChipPAC)

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Mitsubishi Electric

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Carsem

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Tongfu Microelectronics (TFME)

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 King Yuan Electronics Corp. (KYEC)

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Powertech Technology Inc. (PTI)

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Microchip (Microsemi)

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Unisem Group

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 SFA Semicon

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Forehope Electronic (Ningbo) Co.

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Ltd.

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Toshiba

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 BYD

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Zhuzhou CRRC Times Electric

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 China Resources Microelectronics Limited

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Hangzhou Silan Microelectronics

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Rapidus

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.1 Amkor

List of Figures

- Figure 1: Global Automotive IC Package Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive IC Package Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive IC Package Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive IC Package Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive IC Package Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive IC Package Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive IC Package Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive IC Package Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive IC Package Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive IC Package Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive IC Package Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive IC Package Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive IC Package Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive IC Package Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive IC Package Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive IC Package Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive IC Package Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive IC Package Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive IC Package Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive IC Package Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive IC Package Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive IC Package Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive IC Package Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive IC Package Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive IC Package Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive IC Package Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive IC Package Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive IC Package Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive IC Package Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive IC Package Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive IC Package Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive IC Package Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive IC Package Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive IC Package Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive IC Package Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive IC Package Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive IC Package Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive IC Package Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive IC Package Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive IC Package Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive IC Package Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive IC Package Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive IC Package Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive IC Package Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive IC Package Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive IC Package Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive IC Package Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive IC Package Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive IC Package Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive IC Package Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive IC Package?

The projected CAGR is approximately 12.6%.

2. Which companies are prominent players in the Automotive IC Package?

Key companies in the market include Amkor, ASE (SPIL), NXP Semiconductors, Infineon (Cypress), Renesas, TI (Texas Instruments), STMicroelectronics, onsemi, UTAC, Bosch, Rohm, ADI (Analog Devices, Inc), JCET (STATS ChipPAC), Mitsubishi Electric, Carsem, Tongfu Microelectronics (TFME), King Yuan Electronics Corp. (KYEC), Powertech Technology Inc. (PTI), Microchip (Microsemi), Unisem Group, SFA Semicon, Forehope Electronic (Ningbo) Co., Ltd., Toshiba, BYD, Zhuzhou CRRC Times Electric, China Resources Microelectronics Limited, Hangzhou Silan Microelectronics, Rapidus.

3. What are the main segments of the Automotive IC Package?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10050 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive IC Package," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive IC Package report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive IC Package?

To stay informed about further developments, trends, and reports in the Automotive IC Package, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence