Key Insights

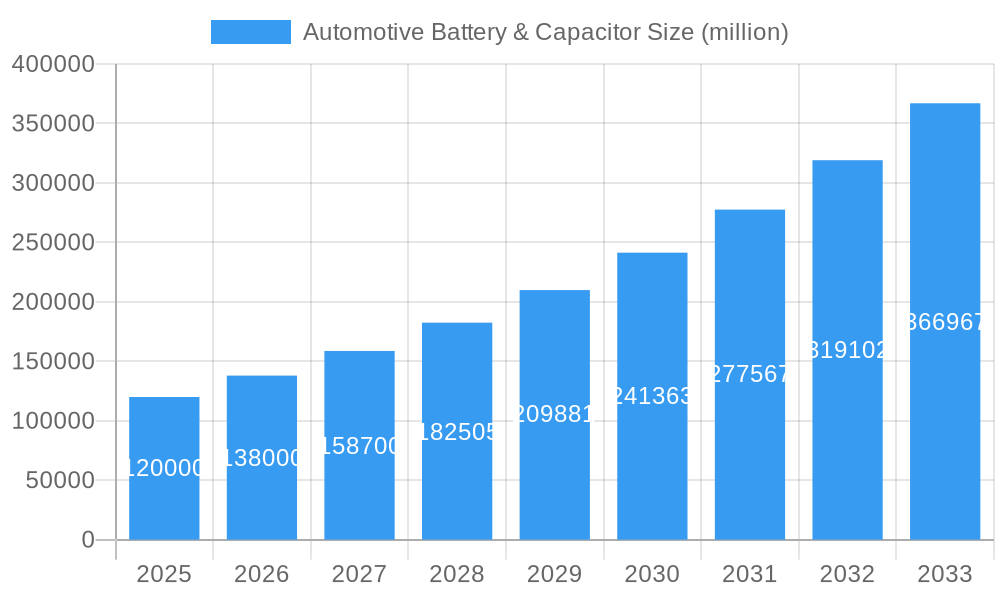

The global automotive battery and capacitor market is projected for significant expansion, reaching an estimated size of 630.6 million by 2025, with a projected Compound Annual Growth Rate (CAGR) of 5.7% from 2025 to 2033. This growth is driven by the accelerating adoption of electric vehicles (EVs) and hybrid vehicles, necessitating advanced battery and capacitor solutions. Increasing environmental regulations and government incentives for sustainable transportation further bolster demand for these critical components. The market is segmented by application into Electric Vehicle, Hybrid Vehicle, and Fuel Cell Vehicle, with electric vehicles emerging as the largest and fastest-growing segment. By type, batteries dominate, fueled by lithium-ion technology advancements, while supercapacitors are gaining traction for their rapid charging and longevity, particularly in hybrid applications.

Automotive Battery & Capacitor Market Size (In Million)

Key growth drivers for the automotive battery and capacitor market include decreasing battery costs, enhanced energy density, and expanding charging infrastructure. However, challenges such as the high initial cost of EVs, raw material availability for battery production, and battery recycling complexities persist. Geographically, the Asia Pacific region, led by China, is expected to dominate due to its robust manufacturing capabilities and rapid EV uptake. North America and Europe are also significant markets, supported by strong governmental backing and consumer interest in sustainable mobility. Industry leaders are investing in research and development to meet evolving market demands. Emerging trends include the innovation of solid-state batteries, next-generation capacitor technologies, and integrated battery management systems for improved performance and safety.

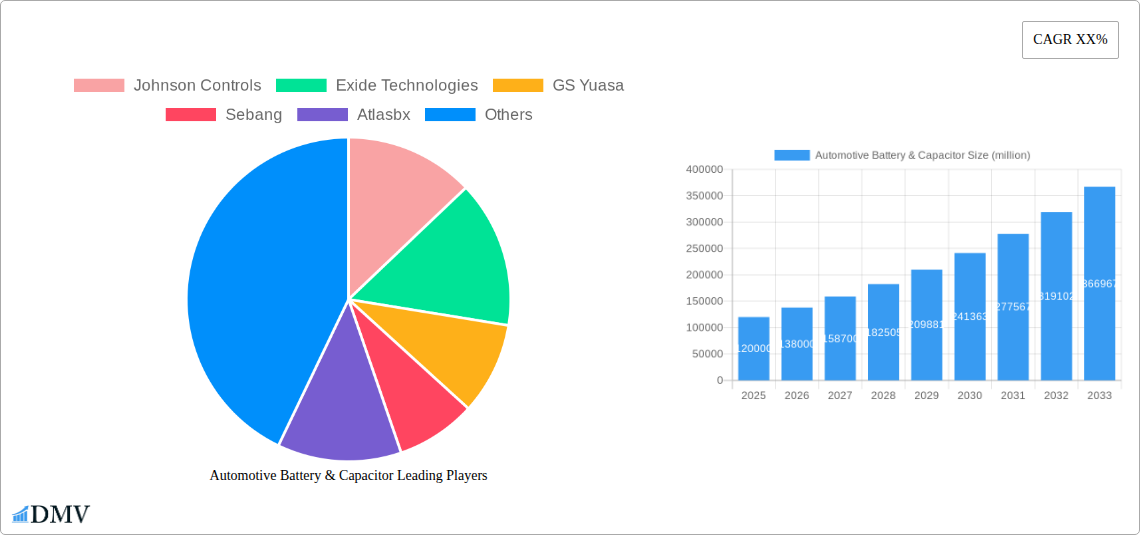

Automotive Battery & Capacitor Company Market Share

Automotive Battery & Capacitor Market Composition & Trends

The global automotive battery and capacitor market is characterized by a dynamic interplay of established players and emerging innovators, with a significant concentration in key regions. Market share distribution is heavily influenced by advancements in electric vehicle (EV) battery technology, with companies like Johnson Controls, Exide Technologies, and GS Yuasa maintaining substantial footprints. The increasing demand for higher energy density, faster charging capabilities, and enhanced safety features fuels continuous innovation, driven by substantial R&D investments. Regulatory landscapes, including stringent emission standards and government incentives for EV adoption, act as powerful catalysts, shaping market direction. The threat of substitute products, while present, is largely mitigated by the unique performance advantages offered by advanced battery and capacitor solutions for electrified powertrains. End-user profiles are evolving, with a growing segment of environmentally conscious consumers and fleet operators prioritizing sustainable transportation. Mergers and acquisitions (M&A) activity remains robust, with significant deal values, as larger entities seek to consolidate market share, acquire cutting-edge technologies, and expand their global reach. For instance, strategic partnerships and acquisitions valued in the hundreds of millions are reshaping the competitive landscape, aiming to secure supply chains and accelerate market penetration.

- Market Share Distribution: Dominated by key players with diversified product portfolios.

- Innovation Catalysts: Driven by EV battery technology advancements and R&D investments.

- Regulatory Landscapes: Stringent emission standards and EV adoption incentives are key drivers.

- Substitute Products: Limited threat due to unique performance advantages in electrified applications.

- End-User Profiles: Shifting towards environmentally conscious consumers and fleet operators.

- M&A Activities: Significant deal values and strategic consolidations are prevalent.

Automotive Battery & Capacitor Industry Evolution

The automotive battery and capacitor industry has undergone a transformative evolution, transitioning from primarily supporting internal combustion engines to becoming the cornerstone of the burgeoning electric vehicle revolution. Over the study period of 2019–2033, with a base year of 2025, the market has witnessed exponential growth trajectories, largely fueled by the rapid adoption of electric and hybrid vehicles. Technological advancements have been at the forefront of this evolution, with a relentless pursuit of higher energy densities, improved power outputs, longer lifespans, and faster charging times for batteries. Simultaneously, supercapacitors are gaining traction for their ability to provide rapid energy bursts for acceleration and regenerative braking, complementing battery performance in applications like Electric Vehicle and Hybrid Vehicle powertrains.

Consumer demand has shifted dramatically, with a growing preference for sustainable mobility solutions, driven by environmental concerns, fluctuating fuel prices, and increasing government mandates. This shift has directly translated into an increased demand for advanced battery and capacitor technologies. The historical period from 2019–2024 saw initial market growth, primarily driven by early EV adopters and pilot programs. The estimated year of 2025 marks a pivotal point, where EV sales are projected to reach significant milestones, further accelerating market expansion. The forecast period of 2025–2033 is anticipated to witness sustained double-digit growth rates, driven by a confluence of factors including decreasing battery costs, expanding charging infrastructure, and a wider array of EV models across various vehicle segments.

Specific data points highlight this dynamic growth. For example, the adoption rate of EVs has seen a compounded annual growth rate (CAGR) exceeding 25% in recent years. Battery energy density has increased by over 15% annually, while charging times have been reduced by an average of 20% through technological innovations. The market for automotive capacitors, though smaller than batteries, is also experiencing robust growth, with a projected CAGR of over 10%, as manufacturers increasingly integrate them for improved energy management and performance in both traditional and electrified vehicles. The industry is witnessing a paradigm shift, with a focus on next-generation battery chemistries, such as solid-state batteries, and advanced capacitor materials to unlock further performance gains and cost reductions, ensuring a sustainable and electrified automotive future.

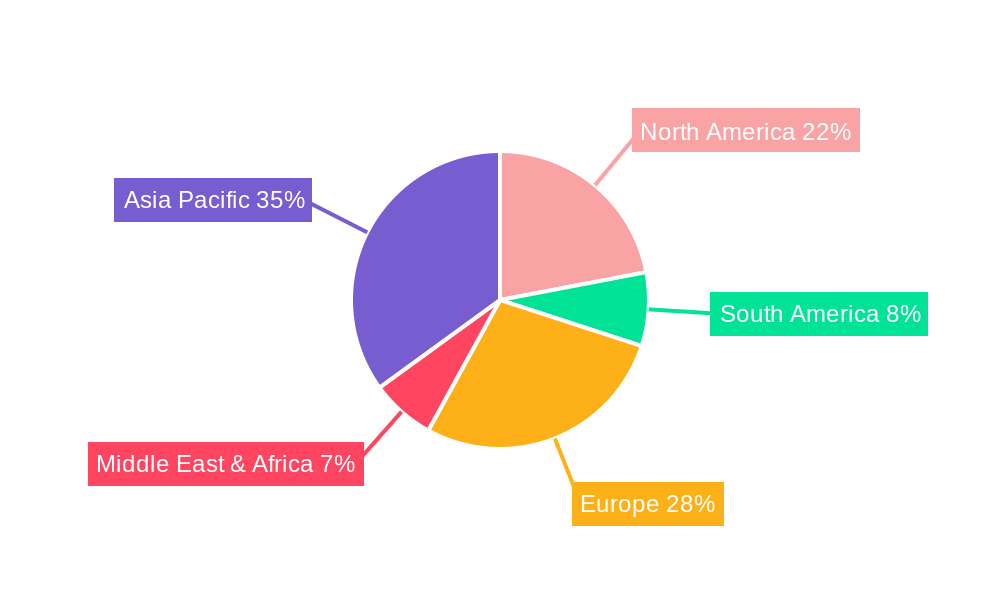

Leading Regions, Countries, or Segments in Automotive Battery & Capacitor

The global automotive battery and capacitor market is currently experiencing significant dominance by specific regions and application segments, driven by a confluence of strategic investments, robust regulatory support, and burgeoning consumer demand. Among the applications, Electric Vehicle (EV) stands out as the primary growth engine, captivating over 70% of the market share, followed by Hybrid Vehicle (HV), which commands approximately 25%. The Fuel Cell Vehicle (FCV) segment, while nascent, is demonstrating promising growth potential, projected to capture a growing niche in the coming years.

Geographically, Asia-Pacific, particularly China, has emerged as the undisputed leader in both production and consumption of automotive batteries and capacitors. This dominance is attributed to several key drivers:

- Government Support and Policy Frameworks: China's aggressive policies to promote EV adoption, including substantial subsidies, tax incentives, and stringent fuel economy regulations, have created a fertile ground for market expansion. Investments in battery manufacturing and charging infrastructure have been monumental, totaling in the hundreds of millions annually.

- Strong Automotive Manufacturing Base: The region hosts a massive automotive manufacturing ecosystem, with a significant portion of global EV production centered here. This proximity to end-users and OEMs facilitates rapid product development and deployment.

- Technological Advancements and Innovation: Leading Asian battery manufacturers are at the forefront of technological innovation, investing billions in research and development for next-generation battery chemistries and manufacturing processes. This includes advancements in Lithium-ion battery technology, solid-state batteries, and energy-dense capacitor solutions.

- Cost Competitiveness: Economies of scale and efficient manufacturing processes have enabled Asian producers to offer batteries and capacitors at competitive price points, making EVs more accessible to a wider consumer base.

North America and Europe follow as significant markets, driven by their own ambitious EV targets, increasing environmental awareness, and technological innovation from global automotive giants. In North America, the US government's focus on domestic battery production and the Inflation Reduction Act are boosting investments. In Europe, stringent CO2 emission standards and the European Green Deal are accelerating the transition to electrified mobility.

Within the types of products, Battery technology overwhelmingly dominates the market, accounting for over 90% of the total market value. This is directly linked to the primary energy storage needs of vehicles. However, Capacitor technology, particularly supercapacitors, is experiencing a surge in adoption for specific applications within EVs and HVs, such as regenerative braking systems, power smoothing, and cold-start assistance, contributing to improved overall vehicle efficiency and performance. The synergy between advanced battery technologies and high-performance capacitors is crucial for the future of automotive electrification, offering enhanced power delivery and energy recovery capabilities.

Automotive Battery & Capacitor Product Innovations

The automotive battery and capacitor market is currently experiencing a wave of groundbreaking product innovations, aimed at enhancing performance, safety, and sustainability in electrified vehicles. A significant focus is on next-generation battery chemistries, moving beyond traditional Lithium-ion. Companies are heavily investing in solid-state battery technology, promising higher energy densities, faster charging times, and improved safety by eliminating flammable liquid electrolytes. This innovation offers a substantial leap in vehicle range and reduced charging downtime, with prototypes demonstrating energy densities exceeding 500 Wh/kg. Furthermore, advancements in battery management systems (BMS) are enabling smarter energy distribution, predictive maintenance, and optimized charging cycles, extending battery lifespan and performance. For capacitors, innovations are centered on increasing power density and capacitance, with new materials allowing for rapid charge and discharge cycles, crucial for regenerative braking systems in Electric Vehicles and Hybrid Vehicles. These advancements are critical for improving the overall efficiency and driving experience of modern automobiles.

Propelling Factors for Automotive Battery & Capacitor Growth

The automotive battery and capacitor market is propelled by a powerful synergy of technological, economic, and regulatory forces. The accelerating global transition towards electric and hybrid vehicles, driven by environmental concerns and a desire for reduced carbon footprints, is the primary catalyst. Government mandates and incentives, such as subsidies for EV purchases and stricter emission standards, are further accelerating this shift, creating substantial market demand. Technological advancements, including the continuous improvement in battery energy density, charging speeds, and lifespan, are making EVs more practical and appealing to consumers. Economic factors, such as decreasing battery production costs due to economies of scale and ongoing R&D, are making electric vehicles more affordable and competitive with traditional internal combustion engine vehicles. For instance, the projected reduction in battery pack costs to under $100 per kWh by 2025 is a significant economic driver.

Obstacles in the Automotive Battery & Capacitor Market

Despite the robust growth, the automotive battery and capacitor market faces several significant obstacles. Supply chain disruptions for critical raw materials like lithium, cobalt, and nickel, exacerbated by geopolitical tensions and increased demand, can lead to price volatility and production delays, impacting the cost and availability of batteries. High upfront costs of electric vehicles, although decreasing, remain a barrier for some consumers compared to conventional vehicles. Limited charging infrastructure in certain regions and the time required for charging can also deter potential buyers. Furthermore, regulatory challenges related to battery recycling, disposal, and evolving safety standards require continuous adaptation and investment from manufacturers. The competitive pressure from established automotive giants and new EV startups also necessitates constant innovation and cost optimization, creating a challenging landscape for market players.

Future Opportunities in Automotive Battery & Capacitor

The future of the automotive battery and capacitor market is brimming with exciting opportunities. The continued exponential growth of the Electric Vehicle market presents the most significant avenue for expansion, with projections indicating EVs will constitute a substantial portion of global vehicle sales by 2030. The development of solid-state batteries holds immense potential to revolutionize the industry by offering enhanced safety, energy density, and faster charging capabilities. Second-life applications for retired EV batteries, such as grid energy storage, present a new revenue stream and a sustainable disposal solution. Emerging markets in developing economies are poised for rapid EV adoption, offering vast untapped potential. Furthermore, the integration of advanced capacitor technologies with battery systems to optimize hybrid vehicle performance and efficiency will continue to drive innovation and market growth.

Major Players in the Automotive Battery & Capacitor Ecosystem

- Johnson Controls

- Exide Technologies

- GS Yuasa

- Sebang

- Atlasbx

- East Penn

- Amara Raja

- FIAMM

- ACDelco

- Bosch

- Hitachi

- Banner

- MOLL

- Camel

- Fengfan

- Chuanxi

- Ruiyu

- Jujiang

- Leoch

- Wanli

Key Developments in Automotive Battery & Capacitor Industry

- 2023/11: Major automotive OEM announces significant investment in solid-state battery research, aiming for commercialization by 2027.

- 2024/01: Battery manufacturer announces a breakthrough in lithium-ion cathode material, promising a 20% increase in energy density and reduced reliance on cobalt.

- 2024/03: Leading capacitor supplier unveils a new supercapacitor technology with twice the power density for automotive applications.

- 2024/07: Government announces new regulations mandating increased recycled material content in automotive batteries by 2030.

- 2025/02: Joint venture formed between a battery producer and an automotive company to establish a gigafactory in North America.

- 2025/05: Major automotive component supplier acquires a specialized battery management system (BMS) developer to enhance its EV offering.

- 2025/09: New global standard for EV battery charging protocols is ratified, aiming to improve interoperability and charging speed.

Strategic Automotive Battery & Capacitor Market Forecast

The strategic automotive battery and capacitor market forecast indicates a period of sustained and robust growth, driven by the irreversible shift towards vehicle electrification. Key growth catalysts include continued technological advancements in battery chemistries, such as the anticipated commercialization of solid-state batteries, which will unlock significant improvements in range and charging times, projected to exceed 500 miles on a single charge for many EVs. The increasing adoption of electric and hybrid vehicles, fueled by stringent emission regulations and a growing consumer preference for sustainable mobility, will continue to be the primary demand driver. Furthermore, strategic investments in battery manufacturing capacity and the development of a comprehensive charging infrastructure across major global markets will facilitate wider EV adoption. The market potential is immense, with projections suggesting the global automotive battery market alone could reach hundreds of billions of dollars by 2033.

Automotive Battery & Capacitor Segmentation

-

1. Application

- 1.1. Electric Vehicle

- 1.2. Hybrid Vehicle

- 1.3. Fuel Cell Vehicle

-

2. Types

- 2.1. Battery

- 2.2. Capacitor

Automotive Battery & Capacitor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Battery & Capacitor Regional Market Share

Geographic Coverage of Automotive Battery & Capacitor

Automotive Battery & Capacitor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Battery & Capacitor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electric Vehicle

- 5.1.2. Hybrid Vehicle

- 5.1.3. Fuel Cell Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Battery

- 5.2.2. Capacitor

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Battery & Capacitor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electric Vehicle

- 6.1.2. Hybrid Vehicle

- 6.1.3. Fuel Cell Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Battery

- 6.2.2. Capacitor

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Battery & Capacitor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electric Vehicle

- 7.1.2. Hybrid Vehicle

- 7.1.3. Fuel Cell Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Battery

- 7.2.2. Capacitor

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Battery & Capacitor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electric Vehicle

- 8.1.2. Hybrid Vehicle

- 8.1.3. Fuel Cell Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Battery

- 8.2.2. Capacitor

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Battery & Capacitor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electric Vehicle

- 9.1.2. Hybrid Vehicle

- 9.1.3. Fuel Cell Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Battery

- 9.2.2. Capacitor

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Battery & Capacitor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electric Vehicle

- 10.1.2. Hybrid Vehicle

- 10.1.3. Fuel Cell Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Battery

- 10.2.2. Capacitor

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Johnson Controls

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Exide Technologies

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 GS Yuasa

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Sebang

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Atlasbx

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 East Penn

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Amara Raja

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 FIAMM

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 ACDelco

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Bosch

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Hitachi

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Banner

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 MOLL

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Camel

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Fengfan

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Chuanxi

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Ruiyu

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Jujiang

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Leoch

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Wanli

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Johnson Controls

List of Figures

- Figure 1: Global Automotive Battery & Capacitor Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Battery & Capacitor Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Battery & Capacitor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Battery & Capacitor Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Battery & Capacitor Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Battery & Capacitor Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Battery & Capacitor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Battery & Capacitor Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Battery & Capacitor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Battery & Capacitor Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Battery & Capacitor Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Battery & Capacitor Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Battery & Capacitor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Battery & Capacitor Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Battery & Capacitor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Battery & Capacitor Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Battery & Capacitor Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Battery & Capacitor Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Battery & Capacitor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Battery & Capacitor Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Battery & Capacitor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Battery & Capacitor Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Battery & Capacitor Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Battery & Capacitor Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Battery & Capacitor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Battery & Capacitor Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Battery & Capacitor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Battery & Capacitor Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Battery & Capacitor Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Battery & Capacitor Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Battery & Capacitor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Battery & Capacitor Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Battery & Capacitor Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Battery & Capacitor Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Battery & Capacitor Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Battery & Capacitor Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Battery & Capacitor Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Battery & Capacitor Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Battery & Capacitor Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Battery & Capacitor Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Battery & Capacitor Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Battery & Capacitor Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Battery & Capacitor Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Battery & Capacitor Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Battery & Capacitor Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Battery & Capacitor Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Battery & Capacitor Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Battery & Capacitor Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Battery & Capacitor Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Battery & Capacitor Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Battery & Capacitor?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Automotive Battery & Capacitor?

Key companies in the market include Johnson Controls, Exide Technologies, GS Yuasa, Sebang, Atlasbx, East Penn, Amara Raja, FIAMM, ACDelco, Bosch, Hitachi, Banner, MOLL, Camel, Fengfan, Chuanxi, Ruiyu, Jujiang, Leoch, Wanli.

3. What are the main segments of the Automotive Battery & Capacitor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 630.6 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Battery & Capacitor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Battery & Capacitor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Battery & Capacitor?

To stay informed about further developments, trends, and reports in the Automotive Battery & Capacitor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence