Key Insights

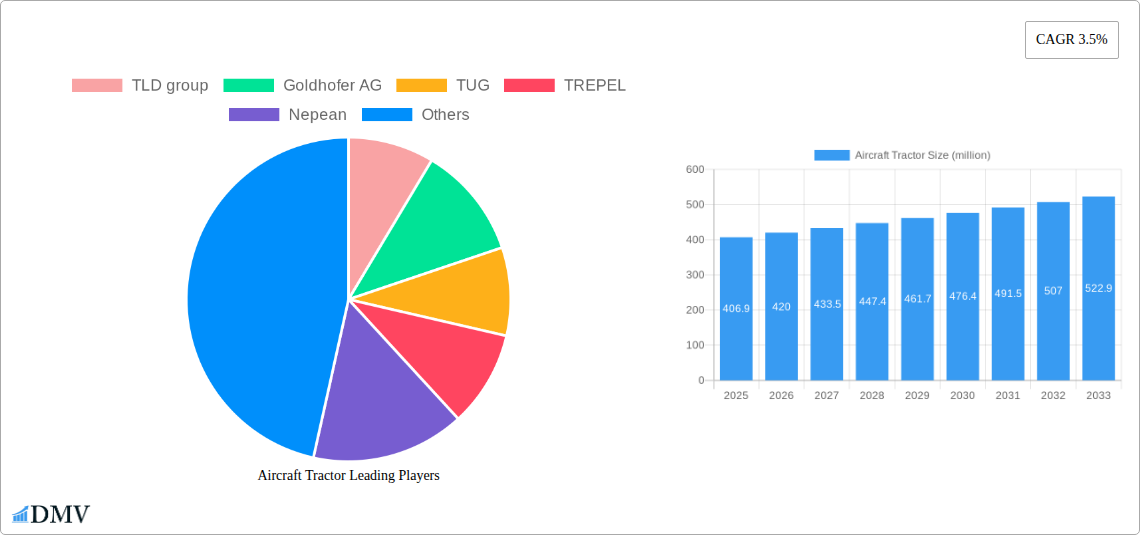

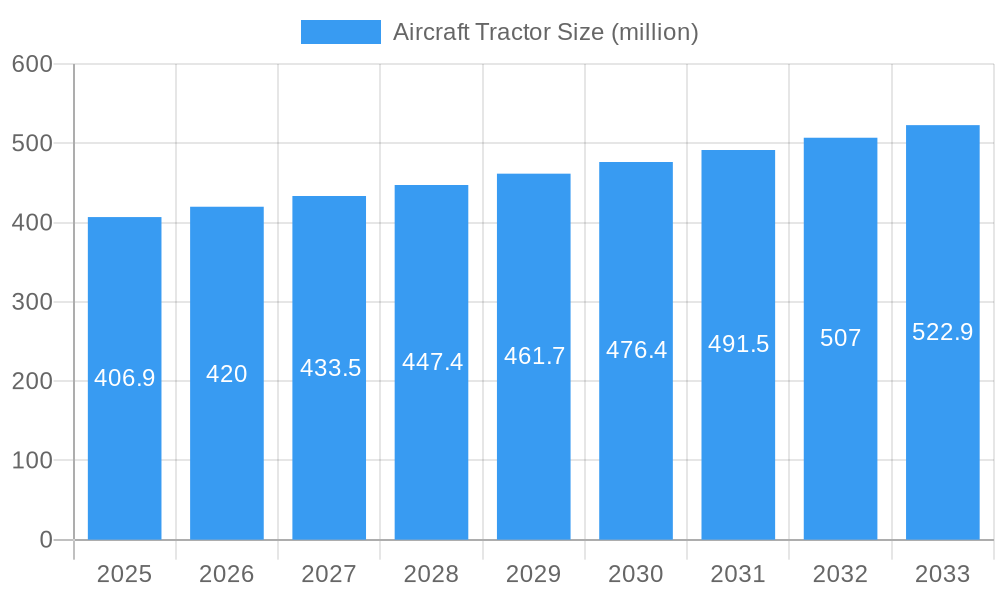

The global Aircraft Tractor market is projected for robust expansion, estimated at USD 406.9 million in 2025, with a projected Compound Annual Growth Rate (CAGR) of 3.5% through 2033. This sustained growth is underpinned by a confluence of escalating air traffic, particularly within civil aviation, and the ongoing modernization of military aviation fleets. The increasing demand for efficient aircraft ground handling solutions, crucial for minimizing turnaround times and enhancing operational safety at airports worldwide, is a primary driver. Advancements in tractor technology, including the development of more powerful, fuel-efficient, and increasingly automated towbarless models, are further stimulating market uptake. These innovations address critical industry needs for reduced operational costs, improved maneuverability in congested apron areas, and enhanced driver ergonomics. The shift towards electric and hybrid aircraft tractors also presents a significant growth avenue, driven by environmental regulations and a broader industry commitment to sustainability.

Aircraft Tractor Market Size (In Million)

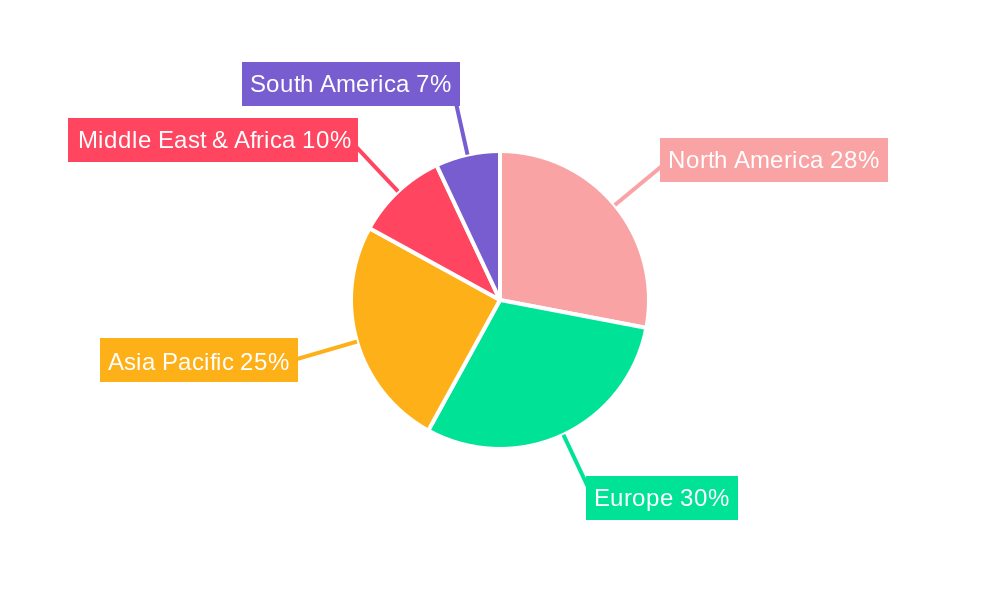

The market's trajectory will be shaped by strategic investments in airport infrastructure and the introduction of new aircraft models requiring specialized ground support equipment. While the demand for conventional tractors remains significant, the superior maneuverability and efficiency of towbarless tractors are expected to drive their adoption, especially in high-traffic commercial airports. Geographically, regions with burgeoning aviation sectors, such as Asia Pacific and the Middle East, are anticipated to witness substantial growth due to increasing passenger and cargo volumes. Conversely, mature markets like North America and Europe will continue to be key revenue generators, driven by fleet upgrades and the adoption of advanced technologies. Challenges such as the high initial cost of sophisticated towbarless tractors and the need for skilled personnel to operate them might pose moderate restraints, but the overarching benefits in operational efficiency and safety are expected to outweigh these concerns, ensuring a positive market outlook.

Aircraft Tractor Company Market Share

Aircraft Tractor Market Composition & Trends

The global aircraft tractor market is characterized by a moderate concentration of key players, with established manufacturers like Goldhofer AG, JBT Aero, and TLD group holding significant market shares. Innovation is primarily driven by the demand for increased efficiency, reduced turnaround times, and enhanced safety in airport operations. Regulatory landscapes, including environmental standards and operational safety protocols, are increasingly influencing product development and market entry. Substitute products, such as specialized tow vehicles and automated guided vehicles, present a growing competitive challenge, particularly in specific niche applications. End-user profiles range from major international airlines and cargo handlers to military air forces and smaller regional airports, each with distinct operational needs and purchasing power. Mergers and acquisitions (M&A) activity, while not at an extreme level, plays a role in market consolidation. For instance, recent M&A deals, valued in the hundreds of millions, have reshaped competitive dynamics and expanded the product portfolios of acquiring entities. Market share distribution sees established players controlling approximately 60% of the global market, with the remaining 40% fragmented among smaller manufacturers and emerging regional players. The focus is shifting towards electric and hybrid aircraft tractors to meet sustainability goals, a trend expected to gain further traction.

- Market Concentration: Moderate, dominated by a few key global manufacturers.

- Innovation Catalysts: Operational efficiency, safety enhancements, sustainability, automation.

- Regulatory Landscapes: Environmental mandates, safety certifications, airport operational guidelines.

- Substitute Products: Specialized tow vehicles, automated guided vehicles (AGVs).

- End-User Profiles: Airlines (major and regional), cargo handlers, military, airport authorities.

- M&A Activities: Strategic acquisitions for market consolidation and portfolio expansion.

- Market Share Distribution: Top 3-5 players hold approximately 60%, with 40% fragmented.

- M&A Deal Values: Estimated in the hundreds of millions, impacting market structure.

Aircraft Tractor Industry Evolution

The aircraft tractor industry has undergone significant evolution, driven by advancements in technology, shifting operational demands, and a growing emphasis on sustainability. Over the historical period of 2019-2024, the market witnessed steady growth, fueled by increasing air traffic and the need for efficient ground support equipment. The base year of 2025 marks a pivotal point where technological integration and electrification are becoming mainstream. The forecast period of 2025-2033 is projected to see accelerated growth, with an estimated Compound Annual Growth Rate (CAGR) of approximately 5.5% to 6.5%. This surge is attributable to the continuous expansion of global aviation, the retirement of older, less efficient aircraft tractor fleets, and the increasing adoption of sophisticated, user-friendly models.

Technological advancements have been a primary catalyst for this evolution. Early aircraft tractors were predominantly mechanical, focusing on brute force for towing. However, modern iterations incorporate advanced hydraulics, sophisticated control systems, and increasingly, electric powertrains. The emergence of towbarless tractors, which eliminate the need for a towbar and thus reduce aircraft stress and turnaround time, has been a disruptive innovation, leading to wider adoption by airlines prioritizing speed and operational flexibility. The industry has also seen a significant push towards automation and semi-automation, with manufacturers developing tractors capable of autonomous movement within apron areas, further enhancing efficiency and safety.

Consumer demand has shifted from basic functionality to comprehensive solutions that offer lower total cost of ownership, reduced environmental impact, and improved driver ergonomics. Airlines and ground handling companies are prioritizing electric aircraft tractors due to their lower operating costs (electricity versus fuel), reduced noise pollution at airports, and compliance with stringent environmental regulations. The adoption metric for electric aircraft tractors has seen a substantial increase, projected to reach over 30% of new sales by 2033. This transition is not merely driven by environmental concerns but also by a proactive approach to future-proofing operations against potential carbon taxes and stricter emissions standards. The overall market growth trajectory is robust, with the global aircraft tractor market size projected to grow from approximately $1.5 billion in 2024 to an estimated $2.5 billion by 2033. This growth is underpinned by consistent demand from both civil aviation and military sectors, with civil aviation segments expected to dominate the market share due to higher volume requirements.

Leading Regions, Countries, or Segments in Aircraft Tractor

The Civil Aviation segment stands as the dominant force within the global aircraft tractor market, accounting for an estimated 75% of the total market share. This dominance is driven by the sheer volume of commercial air traffic worldwide and the continuous need for efficient ground handling operations at airports. Within civil aviation, the Conventional Tractors segment historically held the largest share; however, the Towbarless Tractors segment is experiencing rapid growth and is projected to significantly challenge and eventually surpass conventional tractors in market penetration by 2030. This shift is fueled by the inherent advantages of towbarless technology, including reduced aircraft ground time, minimized risk of ground damage to aircraft, and enhanced operational flexibility for ground crews.

Geographically, North America and Europe currently lead the aircraft tractor market, driven by highly developed aviation infrastructure, substantial airline operations, and stringent safety and environmental regulations that encourage investment in modern ground support equipment. These regions represent over 50% of the global market. Key drivers for this dominance include:

- Investment Trends: Significant capital expenditure by major airlines and airport authorities on fleet modernization and expansion. For instance, North American airlines alone are estimated to invest upwards of $500 million annually in ground support equipment renewals.

- Regulatory Support: Proactive environmental policies promoting the adoption of electric and low-emission vehicles, alongside robust aviation safety regulations that necessitate advanced towing solutions. European Union directives on emissions reduction, for example, are a major impetus for adopting electric aircraft tractors.

- Technological Adoption: Early and widespread adoption of advanced technologies like towbarless tractors and increasing interest in automated ground handling solutions.

The Military segment, while smaller in overall market size compared to civil aviation, remains a critical and consistent consumer of aircraft tractors. Military applications often demand highly robust, all-terrain capable, and specialized tractors for rapid deployment and operation in diverse environmental conditions. The demand here is driven by national defense budgets and strategic readiness initiatives.

Within the Types of aircraft tractors, the Towbarless Tractors segment is poised for the most significant growth. Its market share is projected to expand from approximately 35% in 2025 to an estimated 60% by 2033. This surge is directly correlated with the increasing operational tempo at major airports and the airline industry's focus on reducing aircraft turnaround times to optimize flight schedules and profitability. Conventional tractors will continue to be relevant, especially for smaller aircraft and in regions where the initial investment for towbarless technology might be a barrier, but their market share is expected to gradually decline.

Aircraft Tractor Product Innovations

Product innovation in the aircraft tractor market is rapidly advancing, focusing on enhanced efficiency, sustainability, and operator experience. Key developments include the widespread integration of electric powertrains, offering zero emissions and reduced operational noise, with battery capacities now supporting extended operational cycles. Advanced driver-assistance systems (ADAS) are being incorporated, providing features like obstacle detection and automatic braking, significantly improving safety. Furthermore, manufacturers are developing more compact and agile designs, particularly for towbarless tractors, to navigate crowded airport aprons with greater ease. The integration of telematics and IoT capabilities allows for real-time monitoring of tractor performance, predictive maintenance, and optimized fleet management, enhancing overall operational efficiency for stakeholders. These innovations are crucial for meeting the evolving demands of the aviation industry.

Propelling Factors for Aircraft Tractor Growth

The aircraft tractor market's growth is propelled by several interconnected factors. Increased global air travel and cargo volumes necessitate a larger and more efficient fleet of ground support equipment. Technological advancements, particularly the shift towards electric and automated tractors, are driving fleet modernization and offering improved operational economics and environmental compliance. Stringent airport safety regulations and the drive to reduce aircraft turnaround times also favor the adoption of advanced towing solutions like towbarless tractors. Furthermore, government initiatives promoting sustainable aviation and reduced emissions are creating a favorable environment for the adoption of electric aircraft tractors.

Obstacles in the Aircraft Tractor Market

Despite robust growth prospects, the aircraft tractor market faces several obstacles. The high initial capital investment required for advanced electric and towbarless tractors can be a barrier, particularly for smaller airlines and operators in emerging economies. The ongoing transition to electric powertrains necessitates significant investment in charging infrastructure at airports, which is still developing in many regions. Supply chain disruptions and raw material price volatility can impact manufacturing costs and lead times. Finally, the need for specialized training for operators and maintenance personnel for new technologies presents a logistical challenge for fleet operators.

Future Opportunities in Aircraft Tractor

Emerging opportunities in the aircraft tractor market are abundant. The growing demand for sustainable aviation presents a significant opportunity for electric and hydrogen-powered aircraft tractors. The increasing adoption of automation and artificial intelligence in aviation is paving the way for fully autonomous ground handling vehicles. Expansion into new and developing aviation markets, particularly in Asia and Africa, offers significant growth potential. Furthermore, the development of specialized tractors for emerging aircraft types, such as eVTOLs (electric Vertical Take-Off and Landing) aircraft, represents a nascent but promising opportunity.

Major Players in the Aircraft Tractor Ecosystem

- TLD group

- Goldhofer AG

- TUG

- TREPEL

- Nepean

- Eagle Tugs

- Douglas

- Fresia SpA

- JBT Aero

- Kalmar Motor AB

- Lektro

- Weihai Guangtai

- Charlatte Manutention

Key Developments in Aircraft Tractor Industry

- 2023: Launch of new generation electric towbarless tractors with enhanced battery life and charging capabilities by several leading manufacturers.

- 2023: Increased investment in research and development for autonomous aircraft tractor technology, with pilot programs initiated at major international airports.

- 2022: Acquisition of smaller specialized ground support equipment manufacturers by larger players to expand product portfolios and market reach.

- 2022: Growing adoption of smart connectivity features in aircraft tractors for fleet management and predictive maintenance.

- 2021: Introduction of hybrid-electric aircraft tractors as a transitional solution towards full electrification.

- 2020: Impact of the COVID-19 pandemic on air travel led to temporary slowdowns in fleet upgrades, but recovery has since spurred renewed demand.

- 2019: Increased regulatory pressure globally to reduce airport emissions, driving greater interest in electric ground support equipment.

Strategic Aircraft Tractor Market Forecast

The strategic forecast for the aircraft tractor market indicates a period of substantial and sustained growth, primarily driven by the global aviation industry's recovery and expansion. The increasing emphasis on operational efficiency, safety, and environmental sustainability will continue to be key growth catalysts. The transition towards electric and towbarless tractor technologies is set to accelerate, supported by ongoing technological innovations and favorable regulatory frameworks. Emerging markets and the potential for autonomous ground handling solutions present significant opportunities for market players to expand their reach and revenue streams, ensuring a dynamic and evolving landscape.

Aircraft Tractor Segmentation

-

1. Application

- 1.1. Civil Aviation

- 1.2. Military

-

2. Types

- 2.1. Conventional Tractors

- 2.2. Towbarless Tractors

Aircraft Tractor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aircraft Tractor Regional Market Share

Geographic Coverage of Aircraft Tractor

Aircraft Tractor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Aircraft Tractor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Civil Aviation

- 5.1.2. Military

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Conventional Tractors

- 5.2.2. Towbarless Tractors

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Aircraft Tractor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Civil Aviation

- 6.1.2. Military

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Conventional Tractors

- 6.2.2. Towbarless Tractors

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Aircraft Tractor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Civil Aviation

- 7.1.2. Military

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Conventional Tractors

- 7.2.2. Towbarless Tractors

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Aircraft Tractor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Civil Aviation

- 8.1.2. Military

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Conventional Tractors

- 8.2.2. Towbarless Tractors

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Aircraft Tractor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Civil Aviation

- 9.1.2. Military

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Conventional Tractors

- 9.2.2. Towbarless Tractors

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Aircraft Tractor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Civil Aviation

- 10.1.2. Military

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Conventional Tractors

- 10.2.2. Towbarless Tractors

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 TLD group

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Goldhofer AG

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 TUG

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 TREPEL

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Nepean

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Eagle Tugs

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Douglas

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Fresia SpA

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 JBT Aero

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Kalmar Motor AB

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Lektro

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Weihai Guangtai

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Charlatte Manutention

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 TLD group

List of Figures

- Figure 1: Global Aircraft Tractor Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Aircraft Tractor Revenue (million), by Application 2025 & 2033

- Figure 3: North America Aircraft Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aircraft Tractor Revenue (million), by Types 2025 & 2033

- Figure 5: North America Aircraft Tractor Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aircraft Tractor Revenue (million), by Country 2025 & 2033

- Figure 7: North America Aircraft Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aircraft Tractor Revenue (million), by Application 2025 & 2033

- Figure 9: South America Aircraft Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aircraft Tractor Revenue (million), by Types 2025 & 2033

- Figure 11: South America Aircraft Tractor Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aircraft Tractor Revenue (million), by Country 2025 & 2033

- Figure 13: South America Aircraft Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aircraft Tractor Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Aircraft Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aircraft Tractor Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Aircraft Tractor Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aircraft Tractor Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Aircraft Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aircraft Tractor Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aircraft Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aircraft Tractor Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aircraft Tractor Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aircraft Tractor Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aircraft Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aircraft Tractor Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Aircraft Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aircraft Tractor Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Aircraft Tractor Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aircraft Tractor Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Aircraft Tractor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aircraft Tractor Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Aircraft Tractor Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Aircraft Tractor Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Aircraft Tractor Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Aircraft Tractor Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Aircraft Tractor Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Aircraft Tractor Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Aircraft Tractor Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Aircraft Tractor Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Aircraft Tractor Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Aircraft Tractor Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Aircraft Tractor Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Aircraft Tractor Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Aircraft Tractor Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Aircraft Tractor Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Aircraft Tractor Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Aircraft Tractor Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Aircraft Tractor Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aircraft Tractor Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aircraft Tractor?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the Aircraft Tractor?

Key companies in the market include TLD group, Goldhofer AG, TUG, TREPEL, Nepean, Eagle Tugs, Douglas, Fresia SpA, JBT Aero, Kalmar Motor AB, Lektro, Weihai Guangtai, Charlatte Manutention.

3. What are the main segments of the Aircraft Tractor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 406.9 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aircraft Tractor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aircraft Tractor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aircraft Tractor?

To stay informed about further developments, trends, and reports in the Aircraft Tractor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence