Key Insights

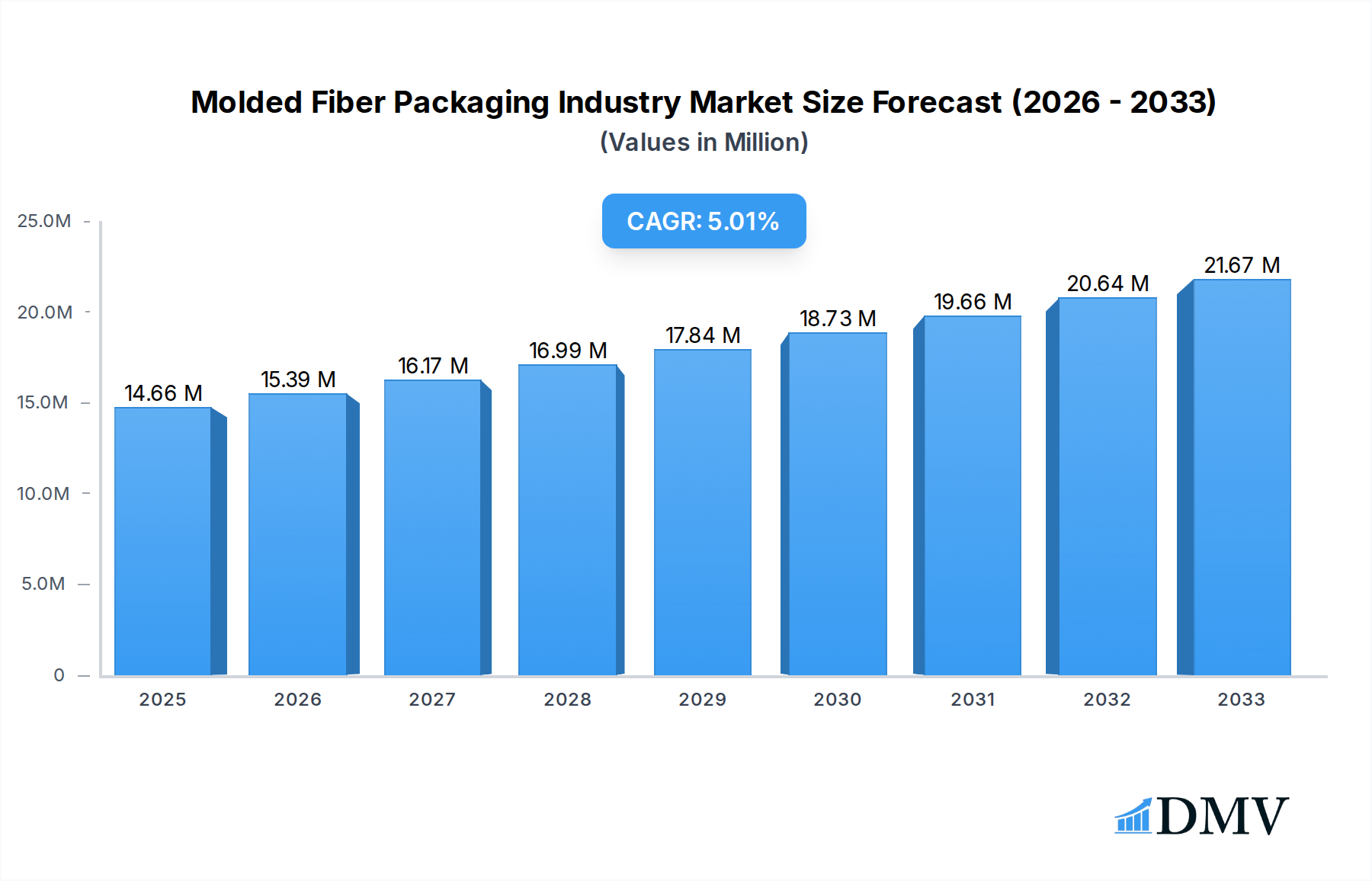

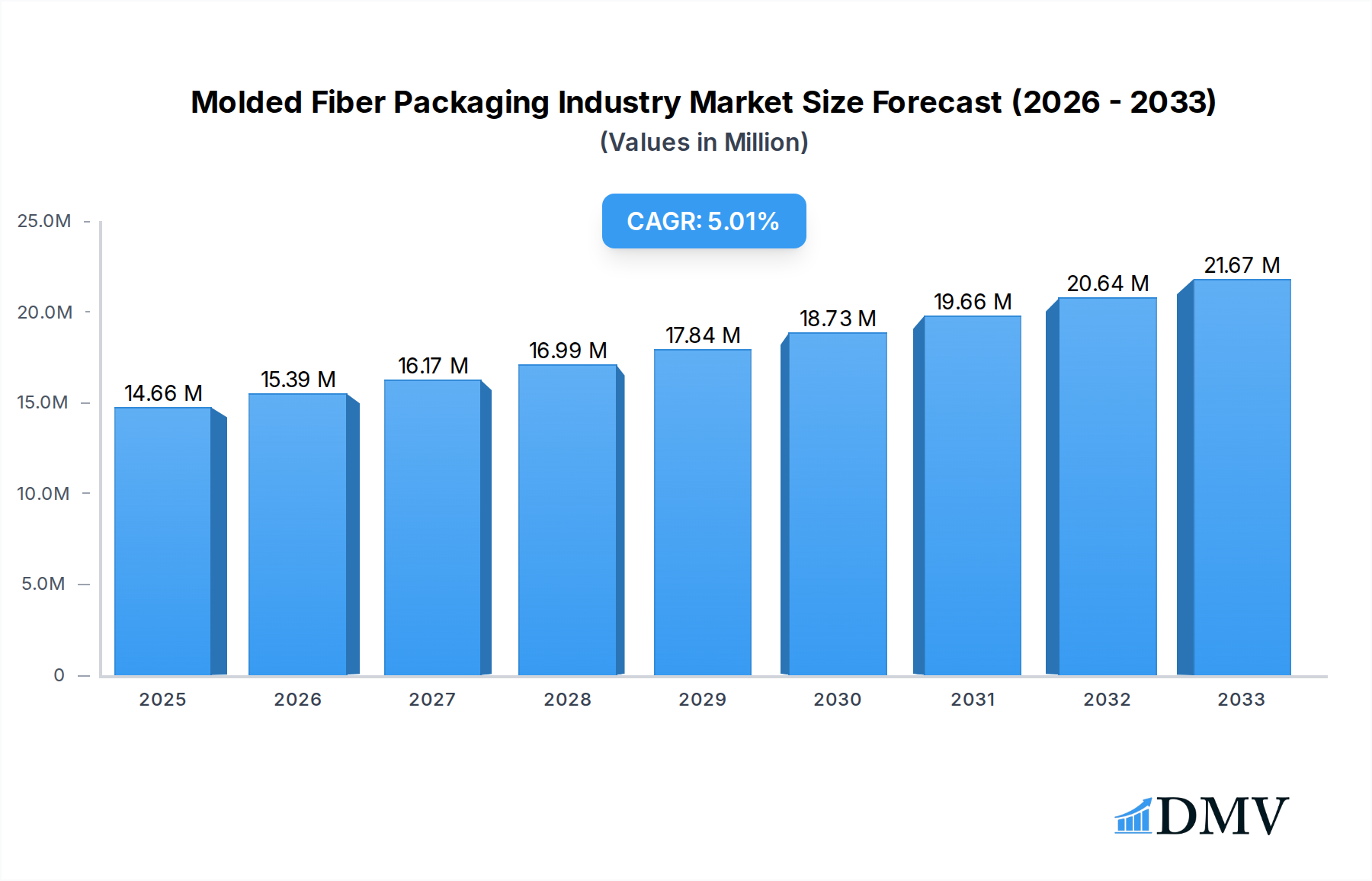

The global Molded Fiber Packaging market is poised for significant expansion, currently valued at an estimated 14.66 million in 2025 and projected to grow at a Compound Annual Growth Rate (CAGR) of 4.96% through 2033. This robust growth is primarily fueled by an escalating demand for sustainable and eco-friendly packaging solutions across various industries. The increasing consumer awareness regarding environmental impact, coupled with stringent government regulations promoting the use of biodegradable and recyclable materials, acts as a powerful catalyst for the molded fiber packaging sector. Furthermore, the inherent properties of molded pulp, such as its durability, shock absorbency, and customizable designs, make it an attractive alternative to traditional plastic and foam packaging, particularly in sectors like food and beverages, electronics, and healthcare where product protection and presentation are paramount. The market's drivers include the shift towards a circular economy, advancements in manufacturing technologies enabling cost-effective production, and the growing adoption of molded fiber for intricate packaging needs.

Molded Fiber Packaging Industry Market Size (In Million)

The market's expansion will be further supported by a widening array of applications and evolving consumer preferences. Innovations in manufacturing processes are enabling the production of thinner, stronger, and more aesthetically pleasing molded fiber packaging, broadening its appeal. The "Formal Type" segment, encompassing both "Wet" and "Dry" molding techniques, offers versatility, allowing for diverse product designs and functionalities to meet specific industry requirements. Key end-user industries like Food and Beverages are increasingly opting for molded fiber for items such as egg cartons, fruit trays, and single-serve containers, driven by both sustainability concerns and the need for effective product protection. The Electronics sector is leveraging molded pulp for protective inserts and packaging, while Healthcare utilizes it for pharmaceutical trays and medical device packaging. While the market enjoys strong growth drivers, potential restraints could include the initial capital investment required for advanced manufacturing equipment and the need for consistent raw material sourcing. However, the overwhelming trend towards sustainable packaging is expected to significantly outweigh these challenges, ensuring a bright future for the molded fiber packaging industry.

Molded Fiber Packaging Industry Company Market Share

Molded Fiber Packaging Industry Market Composition & Trends

The molded fiber packaging market is characterized by a moderate to high concentration, with key players investing heavily in research and development to address growing environmental concerns. Innovation is primarily driven by the demand for sustainable and biodegradable alternatives to conventional plastics. Regulatory landscapes globally are increasingly favoring eco-friendly packaging solutions, impacting material choices and manufacturing processes. Substitute products, such as bioplastics and other compostable materials, pose a competitive threat, though molded fiber's recyclability and cost-effectiveness offer a strong advantage. End-user profiles reveal a significant demand from the Food and Beverages sector, driven by its suitability for food service ware and protective packaging. The Healthcare sector is also showing increasing adoption for medical device packaging and disposables. Mergers and acquisitions (M&A) activity is on the rise as companies seek to expand their production capacity and technological capabilities. M&A deal values are projected to be in the range of several hundred million dollars as the industry consolidates and scales. Market share distribution is currently led by a few dominant manufacturers, but new entrants and strategic partnerships are gradually reshaping the competitive landscape. The market is valued at approximately $3,500 Million in the base year 2025, with a projected CAGR of 6.5% during the forecast period 2025-2033.

Molded Fiber Packaging Industry Industry Evolution

The molded fiber packaging industry has witnessed a remarkable evolution, transitioning from niche applications to a mainstream sustainable packaging solution. The historical period from 2019 to 2024 laid the groundwork for this significant growth, driven by an escalating global awareness of plastic pollution and the urgent need for environmentally responsible alternatives. During this time, the market size grew from approximately $2,800 Million in 2019 to an estimated $3,350 Million by the end of 2024, reflecting an average annual growth rate of roughly 3.5%. Technological advancements have been a crucial catalyst, with innovations in pulping, molding, and finishing processes significantly improving the performance, aesthetics, and cost-effectiveness of molded fiber products. Early adoption of automation and advanced machinery enhanced production efficiency, leading to wider market penetration.

The forecast period, from 2025 to 2033, is expected to see an accelerated growth trajectory, with the market anticipated to reach over $5,500 Million by 2033. This surge is fueled by several factors, including increasingly stringent government regulations phasing out single-use plastics, coupled with growing consumer preference for eco-friendly products across all end-user industries. The base year 2025 stands at an estimated $3,500 Million, with an expected Compound Annual Growth Rate (CAGR) of 6.5% projected through 2033. This robust growth is underpinned by ongoing advancements in material science, leading to stronger, more water-resistant, and aesthetically pleasing molded fiber products. Furthermore, the development of specialized grades for specific applications, such as those resistant to high temperatures or grease, is broadening the market's appeal. The industry's ability to adapt and innovate in response to these evolving demands has cemented its position as a vital component of the global sustainable packaging ecosystem. Consumer demand for products packaged in materials with a lower environmental footprint has become a significant differentiator for brands, further propelling the adoption of molded fiber solutions. The industry's commitment to circular economy principles, including enhanced recyclability and biodegradability, will continue to be a key driver in its sustained evolution.

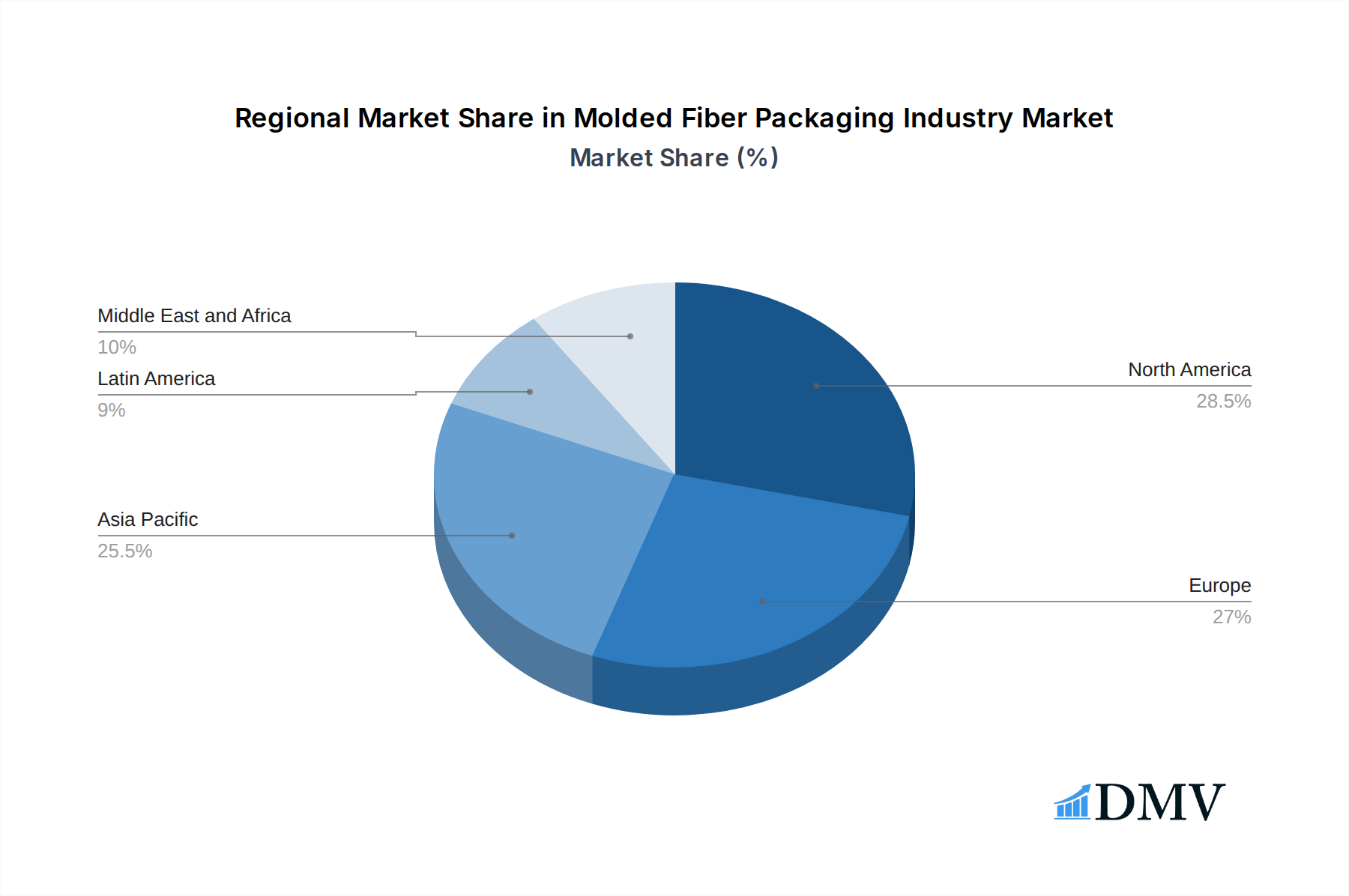

Leading Regions, Countries, or Segments in Molded Fiber Packaging Industry

The Food and Beverages segment stands as the dominant force within the molded fiber packaging industry, driven by its pervasive use in a multitude of applications, from egg cartons and trays to takeout containers and beverage carriers. The North America region is a leading contributor to this dominance, characterized by significant investment trends and robust regulatory support for sustainable packaging. This region's leadership is further amplified by a strong consumer base actively seeking eco-friendly options and a well-established food service industry that relies heavily on disposable packaging.

Key Drivers for Food and Beverages Segment Dominance:

- Consumer Demand for Eco-Friendly Foodware: A growing consciousness about environmental impact has led consumers to favor food and beverage products packaged in sustainable materials. Molded fiber's biodegradability and recyclability align perfectly with these preferences.

- Regulatory Support for Sustainable Packaging: Governments in North America and Europe have implemented policies that restrict single-use plastics, creating a favorable environment for molded fiber alternatives. This includes bans on polystyrene foam containers and mandates for recycled content.

- Versatility and Cost-Effectiveness: Molded fiber packaging offers a high degree of versatility in terms of shape and design, making it suitable for a wide array of food and beverage products. Its production costs are becoming increasingly competitive, especially when compared to the long-term environmental costs of plastic.

- Innovation in Food-Grade Applications: Manufacturers are continuously developing advanced molded fiber solutions with enhanced barrier properties, improved grease resistance, and better thermal insulation, making them ideal for hot and cold food applications.

- Growth of Foodservice and E-commerce: The expansion of the food delivery and takeout market, coupled with the growth of e-commerce for food products, has significantly increased the demand for single-use packaging, with molded fiber emerging as a preferred sustainable option.

The Processed type of molded fiber, which encompasses a wider range of applications beyond basic structural containment, also plays a crucial role in this segment's dominance. Wet molding techniques, in particular, allow for the creation of complex shapes and designs with superior strength and surface finish, further enhancing its appeal for premium food and beverage packaging. The Thermoformed segment is also gaining traction, offering thinner-walled, lighter-weight solutions for specific food packaging needs. While the Dry formal type is experiencing significant innovation, its broader adoption across the Food and Beverages sector is still developing compared to the established wet molding processes. The significant market share held by this segment is further bolstered by strategic investments from major players like Sabert Corporation and Huhtamaki OYJ, who are actively expanding their product portfolios to cater to the escalating demand.

Molded Fiber Packaging Industry Product Innovations

Product innovations in the molded fiber packaging industry are rapidly advancing, focusing on enhancing performance and expanding application possibilities. Manufacturers are developing proprietary blends, such as Sabert Corporation's Pulp Plus and Pulp Max, that are intentionally PFAS-free, addressing a critical health and environmental concern. These advanced formulations offer improved grease and moisture resistance without compromising biodegradability. Furthermore, companies like PulPac are pioneering 'Dry Molded Fiber' technology, enabling the creation of entirely new product formats like fiber bottles designed to replace plastic in sectors such as food, drinks, and consumer health. These innovations aim to deliver superior product protection, shelf appeal, and a significantly reduced environmental footprint, meeting the stringent demands of diverse end-user industries.

Propelling Factors for Molded Fiber Packaging Industry Growth

The molded fiber packaging industry's growth is propelled by a confluence of powerful factors. Environmental consciousness and regulatory mandates are paramount, with governments worldwide implementing stricter regulations against single-use plastics, creating a significant demand for sustainable alternatives. Technological advancements in pulping, molding, and finishing processes are leading to more durable, versatile, and aesthetically pleasing molded fiber products. The growing consumer preference for eco-friendly products across all sectors, particularly Food and Beverages and Healthcare, is a major market driver. Furthermore, the cost-competitiveness and recyclability of molded fiber, compared to some other sustainable materials and the long-term externalities of plastics, make it an increasingly attractive option for businesses aiming to improve their sustainability credentials. The increasing focus on circular economy principles by manufacturers and consumers alike further fuels this positive trajectory.

Obstacles in the Molded Fiber Packaging Industry Market

Despite its robust growth, the molded fiber packaging industry faces several obstacles. Initial investment costs for advanced manufacturing machinery can be substantial, posing a barrier for smaller players. Supply chain disruptions, particularly concerning the availability and cost of raw materials like recycled paper and pulp, can impact production and pricing. While improving, performance limitations such as lower moisture and grease resistance compared to some plastic alternatives still exist for certain applications, requiring ongoing innovation. Regulatory complexities and evolving standards across different regions can also create challenges for widespread adoption. Furthermore, competition from other sustainable packaging materials, including bioplastics and innovative paper-based solutions, intensifies market pressures.

Future Opportunities in Molded Fiber Packaging Industry

Emerging opportunities for the molded fiber packaging industry are abundant and diverse. The development of advanced barrier coatings and treatments will unlock new applications in high-barrier packaging for sensitive food products and pharmaceuticals. The expansion into novel product formats, such as fully compostable fiber bottles for beverages and personal care products, presents significant growth potential. The growing demand for customizable and aesthetically pleasing packaging across various consumer goods sectors offers opportunities for brands to differentiate themselves with unique molded fiber designs. Furthermore, the increasing global focus on circular economy initiatives and sustainable sourcing creates fertile ground for companies that can demonstrate robust recycling and end-of-life solutions. The integration of smart packaging technologies within molded fiber could also unlock new functionalities and consumer engagement avenues.

Major Players in the Molded Fiber Packaging Industry Ecosystem

- Heracles Packaging Company SA

- Omni-Pac Group UK

- Brodrene Hartmann A/S

- PulPac A

- Berkley International

- Sabert Corporation

- Henry Moulded Products Inc

- Huhtamaki OYJ

- Keiding Inc

- EnviroPAK Corporation

- Cullen Packaging Ltd

Key Developments in Molded Fiber Packaging Industry Industry

- June 2023: Sabert Corporation announces the launch of new proprietary molded fiber blends, Pulp Plus and Pulp Max, which are intentionally PFAS-free. As part of its commitment to eliminate all intentionally added perfluoroalkyl and poly-fluoroalkyl substances (PFAS) from its product portfolio by the end of 2023, Sabert's new pulp formulations aim to help customers achieve their sustainability goals.

- February 2023: PulPac, the Swedish company that makes 'Dry Molded Fiber' is teaming up with PA Consulting to create a fiber bottle that's designed to replace plastic bottles in the food, drinks, consumer health, and FMCG sectors. It's based on PulPac's own proprietary technology.

Strategic Molded Fiber Packaging Industry Market Forecast

The strategic market forecast for the molded fiber packaging industry is exceptionally positive, driven by the persistent global imperative for sustainable solutions. Growth catalysts include intensifying regulatory pressure on single-use plastics, which directly favors biodegradable and recyclable alternatives like molded fiber. Technological innovations, particularly in 'Dry Molded Fiber' and advanced barrier properties, are expanding the application scope and performance capabilities, making molded fiber a viable substitute for a broader range of products. Consumer preference for eco-conscious brands further solidifies this trend, creating a robust demand pull. The forecast period 2025-2033 anticipates a significant market expansion, with substantial opportunities arising from sectors like Food and Beverages, Healthcare, and Consumer Goods seeking to align with sustainability goals and circular economy principles. The market is projected to reach over $5,500 Million by 2033, demonstrating a strong CAGR of 6.5% from a base of $3,500 Million in 2025.

Molded Fiber Packaging Industry Segmentation

-

1. Type

- 1.1. Thick wall

- 1.2. Transfer

- 1.3. Thermoformed

- 1.4. Processed

-

2. Formal Type

- 2.1. Wet

- 2.2. Dry

-

3. End-user Industry

- 3.1. Food and Beverages

- 3.2. Electronics

- 3.3. Healthcare

- 3.4. Other End-user Industries

Molded Fiber Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Italy

- 2.5. Spain

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 4. Australia and New Zealand

-

5. Latin America

- 5.1. Brazil

- 5.2. Mexico

-

6. Middle East and Africa

- 6.1. United Arab Emirates

- 6.2. Saudi Arabia

- 6.3. South Africa

Molded Fiber Packaging Industry Regional Market Share

Geographic Coverage of Molded Fiber Packaging Industry

Molded Fiber Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Thick wall

- 5.1.2. Transfer

- 5.1.3. Thermoformed

- 5.1.4. Processed

- 5.2. Market Analysis, Insights and Forecast - by Formal Type

- 5.2.1. Wet

- 5.2.2. Dry

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverages

- 5.3.2. Electronics

- 5.3.3. Healthcare

- 5.3.4. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Thick wall

- 6.1.2. Transfer

- 6.1.3. Thermoformed

- 6.1.4. Processed

- 6.2. Market Analysis, Insights and Forecast - by Formal Type

- 6.2.1. Wet

- 6.2.2. Dry

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverages

- 6.3.2. Electronics

- 6.3.3. Healthcare

- 6.3.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Thick wall

- 7.1.2. Transfer

- 7.1.3. Thermoformed

- 7.1.4. Processed

- 7.2. Market Analysis, Insights and Forecast - by Formal Type

- 7.2.1. Wet

- 7.2.2. Dry

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Food and Beverages

- 7.3.2. Electronics

- 7.3.3. Healthcare

- 7.3.4. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Thick wall

- 8.1.2. Transfer

- 8.1.3. Thermoformed

- 8.1.4. Processed

- 8.2. Market Analysis, Insights and Forecast - by Formal Type

- 8.2.1. Wet

- 8.2.2. Dry

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Food and Beverages

- 8.3.2. Electronics

- 8.3.3. Healthcare

- 8.3.4. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Thick wall

- 9.1.2. Transfer

- 9.1.3. Thermoformed

- 9.1.4. Processed

- 9.2. Market Analysis, Insights and Forecast - by Formal Type

- 9.2.1. Wet

- 9.2.2. Dry

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Food and Beverages

- 9.3.2. Electronics

- 9.3.3. Healthcare

- 9.3.4. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia and New Zealand Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Thick wall

- 10.1.2. Transfer

- 10.1.3. Thermoformed

- 10.1.4. Processed

- 10.2. Market Analysis, Insights and Forecast - by Formal Type

- 10.2.1. Wet

- 10.2.2. Dry

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Food and Beverages

- 10.3.2. Electronics

- 10.3.3. Healthcare

- 10.3.4. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Latin America Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Thick wall

- 11.1.2. Transfer

- 11.1.3. Thermoformed

- 11.1.4. Processed

- 11.2. Market Analysis, Insights and Forecast - by Formal Type

- 11.2.1. Wet

- 11.2.2. Dry

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Food and Beverages

- 11.3.2. Electronics

- 11.3.3. Healthcare

- 11.3.4. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Middle East and Africa Molded Fiber Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Thick wall

- 12.1.2. Transfer

- 12.1.3. Thermoformed

- 12.1.4. Processed

- 12.2. Market Analysis, Insights and Forecast - by Formal Type

- 12.2.1. Wet

- 12.2.2. Dry

- 12.3. Market Analysis, Insights and Forecast - by End-user Industry

- 12.3.1. Food and Beverages

- 12.3.2. Electronics

- 12.3.3. Healthcare

- 12.3.4. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Heracles Packaging Company SA

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Omni-Pac Group UK

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Brodrene Hartmann A/S

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 PulPac A

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Berkley International

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Sabert Corporation

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Henry Moulded Products Inc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Huhtamaki OYJ

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Keiding Inc

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 EnviroPAK Corporation

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Cullen Packaging Ltd

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 Heracles Packaging Company SA

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Molded Fiber Packaging Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Molded Fiber Packaging Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Molded Fiber Packaging Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Molded Fiber Packaging Industry Revenue (Million), by Formal Type 2025 & 2033

- Figure 5: North America Molded Fiber Packaging Industry Revenue Share (%), by Formal Type 2025 & 2033

- Figure 6: North America Molded Fiber Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 7: North America Molded Fiber Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Molded Fiber Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Molded Fiber Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Molded Fiber Packaging Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Europe Molded Fiber Packaging Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Molded Fiber Packaging Industry Revenue (Million), by Formal Type 2025 & 2033

- Figure 13: Europe Molded Fiber Packaging Industry Revenue Share (%), by Formal Type 2025 & 2033

- Figure 14: Europe Molded Fiber Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 15: Europe Molded Fiber Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: Europe Molded Fiber Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Molded Fiber Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Molded Fiber Packaging Industry Revenue (Million), by Type 2025 & 2033

- Figure 19: Asia Pacific Molded Fiber Packaging Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Molded Fiber Packaging Industry Revenue (Million), by Formal Type 2025 & 2033

- Figure 21: Asia Pacific Molded Fiber Packaging Industry Revenue Share (%), by Formal Type 2025 & 2033

- Figure 22: Asia Pacific Molded Fiber Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Asia Pacific Molded Fiber Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Asia Pacific Molded Fiber Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Molded Fiber Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Molded Fiber Packaging Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Australia and New Zealand Molded Fiber Packaging Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Australia and New Zealand Molded Fiber Packaging Industry Revenue (Million), by Formal Type 2025 & 2033

- Figure 29: Australia and New Zealand Molded Fiber Packaging Industry Revenue Share (%), by Formal Type 2025 & 2033

- Figure 30: Australia and New Zealand Molded Fiber Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 31: Australia and New Zealand Molded Fiber Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Australia and New Zealand Molded Fiber Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Molded Fiber Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Molded Fiber Packaging Industry Revenue (Million), by Type 2025 & 2033

- Figure 35: Latin America Molded Fiber Packaging Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: Latin America Molded Fiber Packaging Industry Revenue (Million), by Formal Type 2025 & 2033

- Figure 37: Latin America Molded Fiber Packaging Industry Revenue Share (%), by Formal Type 2025 & 2033

- Figure 38: Latin America Molded Fiber Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 39: Latin America Molded Fiber Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Latin America Molded Fiber Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Molded Fiber Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Molded Fiber Packaging Industry Revenue (Million), by Type 2025 & 2033

- Figure 43: Middle East and Africa Molded Fiber Packaging Industry Revenue Share (%), by Type 2025 & 2033

- Figure 44: Middle East and Africa Molded Fiber Packaging Industry Revenue (Million), by Formal Type 2025 & 2033

- Figure 45: Middle East and Africa Molded Fiber Packaging Industry Revenue Share (%), by Formal Type 2025 & 2033

- Figure 46: Middle East and Africa Molded Fiber Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 47: Middle East and Africa Molded Fiber Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 48: Middle East and Africa Molded Fiber Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Middle East and Africa Molded Fiber Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 3: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 7: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 12: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 13: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: France Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Germany Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 21: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 22: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 23: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: China Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: India Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Japan Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 28: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 29: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 30: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 32: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 33: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: Brazil Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Mexico Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 38: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Formal Type 2020 & 2033

- Table 39: Global Molded Fiber Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 40: Global Molded Fiber Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: United Arab Emirates Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Saudi Arabia Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Africa Molded Fiber Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Molded Fiber Packaging Industry?

The projected CAGR is approximately 4.96%.

2. Which companies are prominent players in the Molded Fiber Packaging Industry?

Key companies in the market include Heracles Packaging Company SA, Omni-Pac Group UK, Brodrene Hartmann A/S, PulPac A, Berkley International, Sabert Corporation, Henry Moulded Products Inc, Huhtamaki OYJ, Keiding Inc, EnviroPAK Corporation, Cullen Packaging Ltd.

3. What are the main segments of the Molded Fiber Packaging Industry?

The market segments include Type, Formal Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.66 Million as of 2022.

5. What are some drivers contributing to market growth?

Shift in Consumer Preferences Toward Recyclable and Eco-friendly Materials; Growing Disposable Income; Augmented Demand for Reusable and Sustainable Packaging From End Users.

6. What are the notable trends driving market growth?

Food and Beverages to be the Largest End-user Industry.

7. Are there any restraints impacting market growth?

Concerns Regarding the Availability of Material.

8. Can you provide examples of recent developments in the market?

June 2023 - Sabert Corporation announces the launch of new proprietary molded fiber blends, Pulp Plus and Pulp Max, which are intentionally PFAS-free. As part of its commitment to eliminate all intentionally added perfluoroalkyl and poly-fluoroalkyl substances (PFAS) from its product portfolio by the end of 2023, Sabert's new pulp formulations aim to help customers achieve their sustainability goals.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Molded Fiber Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Molded Fiber Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Molded Fiber Packaging Industry?

To stay informed about further developments, trends, and reports in the Molded Fiber Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence