Key Insights

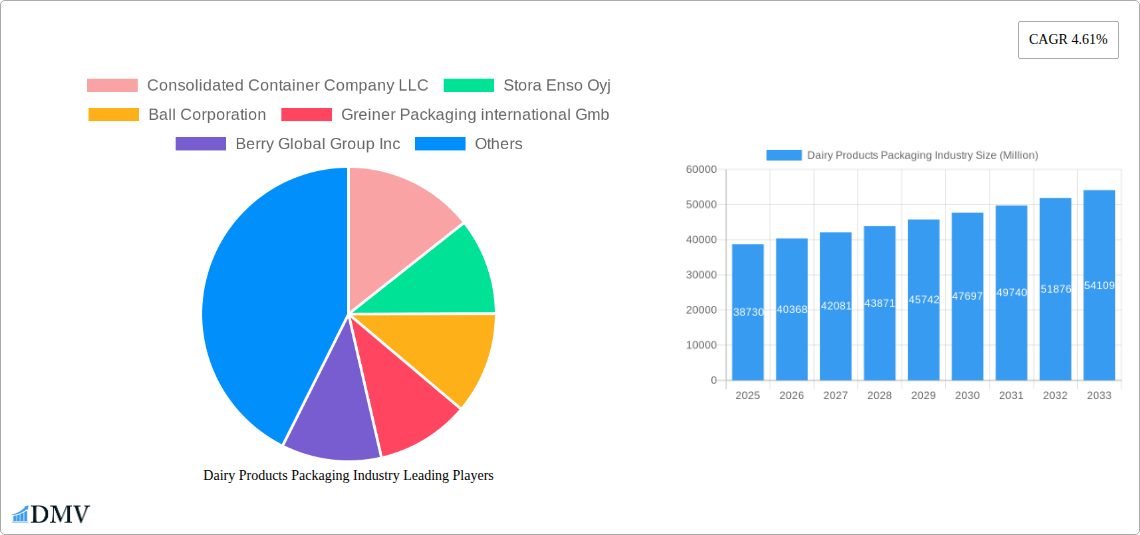

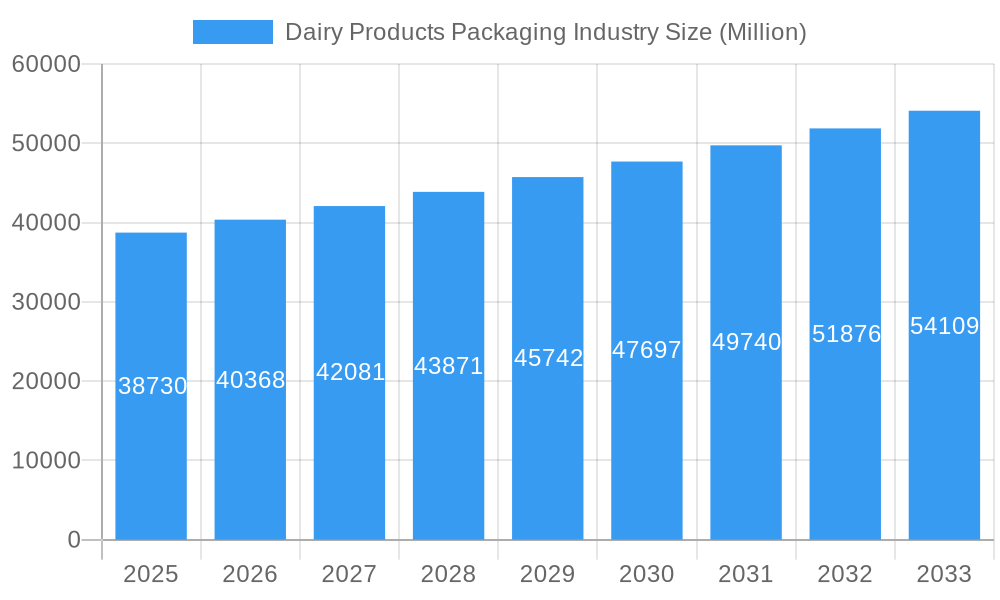

The global Dairy Products Packaging market is poised for significant growth, projected to reach USD 38.73 billion in 2025 and expand at a Compound Annual Growth Rate (CAGR) of 4.3% through 2033. This robust expansion is driven by an increasing global demand for dairy products, stemming from rising disposable incomes, a growing health-conscious population, and the inherent nutritional benefits of dairy. Key trends shaping the market include a strong consumer preference for convenient, sustainable, and aesthetically appealing packaging solutions. The rising awareness about environmental issues is fueling demand for eco-friendly materials like paper and paperboard, alongside advancements in recyclable plastics and lightweight glass. Innovation in packaging design, such as the development of extended shelf-life solutions and smart packaging technologies, will further propel market growth by reducing food waste and enhancing consumer experience.

Dairy Products Packaging Industry Market Size (In Billion)

The market's growth trajectory is further supported by an expanding product portfolio within the dairy sector, encompassing a wider variety of milk, cheese, yogurt, and frozen dairy products. This diversity necessitates a range of packaging formats, with bottles and cartons continuing to dominate due to their established functionality and consumer familiarity. However, pouches and bags are gaining traction for their flexibility, lighter weight, and improved barrier properties, especially for single-serving portions and specialty dairy items. While the market exhibits strong growth potential, certain restraints such as fluctuating raw material prices and stringent regulatory compliance for food contact materials can present challenges. Nevertheless, the industry's ability to adapt to these challenges through technological innovation and a focus on sustainability is expected to ensure continued expansion in the coming years.

Dairy Products Packaging Industry Company Market Share

Dairy Products Packaging Industry Market Composition & Trends

The global dairy products packaging market is a dynamic and evolving sector, projected to reach an estimated market size of XXX billion by 2025. The packaging solutions for dairy are critical for product preservation, shelf-life extension, consumer appeal, and brand differentiation. Market concentration remains moderately fragmented, with key players like Amcor PLC, Berry Global Group Inc, Ball Corporation, and Huhtamaki Group holding significant shares. However, the landscape is continuously reshaped by innovation and strategic alliances. Innovation catalysts are primarily driven by the escalating demand for sustainable and eco-friendly packaging materials, alongside advancements in barrier technologies to enhance food safety and reduce spoilage.

The regulatory landscape is increasingly stringent, pushing manufacturers towards recyclable, compostable, or biodegradable packaging options. Substitute products, such as plant-based alternatives, are indirectly influencing dairy packaging by creating a competitive pressure for enhanced product appeal and convenience. End-user profiles span from large-scale dairy producers to smaller artisanal creameries, each with distinct packaging needs. Mergers and acquisitions (M&A) activities are a significant trend, with deal values in the billions reflecting the strategic importance of this sector. For instance, the acquisition of Elif Holding A.S. by Huhtamaki Group in August 2021 underscores the consolidation aimed at expanding market reach and technological capabilities in flexible packaging for dairy.

- Market Share Distribution: Leading players like Amcor PLC and Berry Global Group Inc. collectively hold approximately XX% of the global market.

- M&A Deal Values: Recent transactions have seen deal values exceeding XXX billion, indicating significant investment and consolidation within the industry.

- Key Innovation Areas: Focus on recycled plastic packaging, paperboard packaging for dairy, and biodegradable dairy containers.

- Regulatory Impact: Growing emphasis on Extended Producer Responsibility (EPR) schemes and single-use plastic bans.

Dairy Products Packaging Industry Industry Evolution

The dairy products packaging industry has witnessed a significant transformation driven by a confluence of technological advancements, shifting consumer preferences, and a global push towards sustainability. The market growth trajectory for dairy packaging materials has been steadily upward, fueled by the consistent global demand for milk, cheese, yogurt, and other dairy-derived products. Historically, the industry relied heavily on traditional materials like glass and basic plastics. However, the forecast period of 2025–2033 is set to be characterized by a rapid adoption of innovative solutions.

Technological advancements have played a pivotal role in shaping the evolution of dairy packaging. Innovations in material science have led to the development of high-barrier plastics that significantly extend the shelf life of dairy products, thereby reducing food waste. The introduction of advanced printing technologies allows for enhanced branding and consumer engagement. Furthermore, the development of smart packaging solutions, incorporating features like temperature indicators, is gaining traction.

Shifting consumer demands are a major impetus for this evolution. There's a pronounced consumer preference for convenient, portable, and single-serving packaging formats, especially for products like yogurt and cultured dairy items. Simultaneously, a heightened awareness of environmental issues has propelled the demand for sustainable dairy packaging. This includes a strong preference for plastic packaging recyclability, the adoption of paper and paperboard solutions, and a growing interest in fiber-based bottles. The industry's response to these demands is evident in the continuous R&D efforts focused on developing eco-friendly dairy packaging.

For example, the study period from 2019–2033 has seen a notable shift from rigid plastic containers to more flexible and lightweight options like pouches and bags for dairy products. The increasing popularity of ready-to-drink dairy beverages has also driven the demand for specialized bottles for dairy. The market's resilience and adaptability are underscored by its capacity to integrate new materials and designs that meet both functional and environmental criteria. The base year of 2025 serves as a critical point for understanding the current market dynamics and projecting future growth, with a projected market size of XXX billion. The estimated year of 2025 further solidifies these projections, anticipating continued growth driven by these multifaceted factors.

- Market Growth Trajectories: Consistent annual growth rates are anticipated, driven by population expansion and rising disposable incomes in emerging economies.

- Technological Advancements: Adoption of chemical recycling for plastics, development of advanced barrier coatings, and integration of digital printing for personalized packaging.

- Shifting Consumer Demands: Increasing demand for convenience, portion control, and aesthetically appealing packaging.

- Sustainability Focus: Growth in demand for recycled content, compostable materials, and lightweighting initiatives across all packaging types.

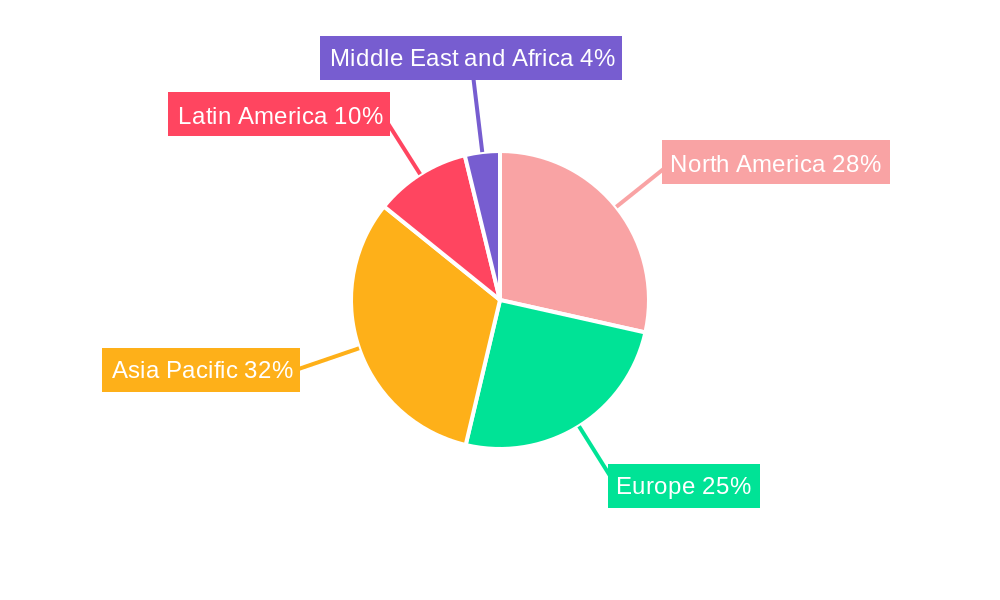

Leading Regions, Countries, or Segments in Dairy Products Packaging Industry

The dairy products packaging industry exhibits distinct regional dominance and segmentation, driven by economic factors, consumer habits, and regulatory frameworks. Globally, Asia Pacific has emerged as a leading region, propelled by its vast population, increasing urbanization, and a rapidly growing middle class with expanding purchasing power for dairy products. Countries like China, India, and Southeast Asian nations are significant contributors to this growth. The rising disposable incomes in these regions directly translate into higher consumption of dairy products, thereby escalating the demand for effective dairy packaging solutions.

Within the material segment, Plastic is the dominant category, accounting for over XX% of the market share. This dominance is attributed to its versatility, cost-effectiveness, and excellent barrier properties, making it ideal for various dairy products like milk, yogurt, and cheese. Paper and Paperboard is experiencing robust growth, driven by the increasing demand for sustainable and recyclable packaging. This segment is particularly strong in the packaging of butter, cheese, and frozen dairy products.

In terms of product segmentation, Milk packaging continues to represent the largest share due to its widespread consumption globally. However, Yogurt and Cultured Products packaging is witnessing significant growth, fueled by the popularity of individual servings and innovative product formulations. The Package Type segment sees Cartons and Boxes as a major contributor, especially for liquid milk and multi-pack cheese. Bottles are crucial for milk, kefir, and some flavored dairy drinks, with a growing trend towards smaller, more convenient sizes.

- Dominant Region: Asia Pacific leads due to a burgeoning middle class and high dairy consumption rates.

- Key Drivers: Rapid urbanization, increasing disposable incomes, supportive government initiatives for food processing and packaging.

- Dominant Material: Plastic continues to hold the largest market share owing to its versatility and cost-effectiveness.

- Key Drivers: Innovations in recycled plastics, development of enhanced barrier properties, cost efficiency compared to alternatives.

- Dominant Product: Milk packaging remains the largest segment due to its staple status in diets worldwide.

- Key Drivers: Consistent demand, availability of various milk types (fresh, UHT, flavored), extensive distribution networks.

- Dominant Package Type: Cartons and Boxes are extensively used for liquid dairy and cheese due to their stackability and protective qualities.

- Key Drivers: Efficiency in logistics, excellent branding opportunities, ability to house various formats (e.g., gable-top cartons for milk).

- Emerging Trends: Significant growth in pouches and bags for yogurt and cultured products, and increasing adoption of fiber-based bottles as a sustainable alternative.

Dairy Products Packaging Industry Product Innovations

Product innovations in the dairy packaging industry are primarily driven by the dual demands for enhanced product preservation and increased sustainability. Manufacturers are actively developing advanced barrier films for plastic milk pouches and yogurt cups that significantly extend shelf life, reducing food waste and improving product quality. The advent of chemically recycled polypropylene is revolutionizing the production of cups for ready-to-drink dairy beverages, offering a viable circular economy solution. Furthermore, the development of fiber-based bottles represents a significant leap towards reducing reliance on virgin plastics and glass. These innovative paper bottles for dairy are designed to offer comparable performance to traditional materials while significantly lowering their environmental footprint.

Propelling Factors for Dairy Products Packaging Industry Growth

The dairy products packaging industry is propelled by several key growth drivers. Increasing global demand for dairy products, driven by population growth and rising disposable incomes in emerging economies, is a primary catalyst. The growing consumer preference for convenient, single-serving, and ready-to-drink dairy options is fostering innovation in flexible packaging and bottles. Furthermore, the escalating emphasis on sustainability and environmental consciousness is a significant driver, pushing manufacturers towards recyclable, compostable, and bio-based packaging solutions. Technological advancements in material science and processing techniques are enabling the development of more efficient, effective, and eco-friendly packaging.

Obstacles in the Dairy Products Packaging Industry Market

Despite robust growth prospects, the dairy products packaging industry faces several obstacles. Stringent and evolving regulatory landscapes, particularly concerning plastic waste and food safety standards, can increase compliance costs and necessitate significant investment in new technologies. Supply chain disruptions, as witnessed in recent years, can lead to material shortages and price volatility, impacting production and profitability. Intense competitive pressures among packaging manufacturers and material suppliers can lead to price wars and squeezed profit margins. Furthermore, the cost of sustainable packaging materials can sometimes be higher than conventional alternatives, posing a challenge for widespread adoption, especially in price-sensitive markets.

Future Opportunities in Dairy Products Packaging Industry

The dairy products packaging industry is ripe with future opportunities. The burgeoning demand for plant-based dairy alternatives will create new avenues for specialized packaging solutions. The continued growth of e-commerce and direct-to-consumer delivery models will necessitate innovative, robust, and temperature-controlled packaging. Further advancements in smart packaging technologies, offering features like traceability and freshness monitoring, will unlock new value propositions for both manufacturers and consumers. The expansion of chemical recycling infrastructure and the development of novel biodegradable materials present significant opportunities for companies investing in circular economy initiatives.

Major Players in the Dairy Products Packaging Industry Ecosystem

- Consolidated Container Company LLC

- Stora Enso Oyj

- Ball Corporation

- Greiner Packaging international Gmb

- Berry Global Group Inc

- Huhtamaki Group

- Winpak Ltd

- Amcor PLC

- International Paper Company

- Sealed Air Corporation

- Saudi Basic Industries Corporation

Key Developments in Dairy Products Packaging Industry Industry

- September 2021 - Greiner Packaging announced Emmi CAFFÈ LATTE, Europe's leading ready-to-drink iced coffee brand, will start incorporating its new chemically recycled polypropylene into packaging. Greiner Packaging makes these cups from chemically recycled material that comes from Borealis.

- August 2021 - Huhtamaki announced the acquisition of Elif Holding A.S., which is a leader in producing and supplying sustainable, flexible packaging to major global FMCG brands in Africa, the Middle East, and Europe. This acquisition helps Huhtamaki to reinforce its position in emerging packaging markets.

- May 2021 - Stora Enso announced a partnership with Pulpex to produce fiber-based bottles. The packaging technology of Pulpex will help to industrialize the production of containers made from wood fiber pulp and eco-friendly paper bottles, offering an alternative to glass and PET plastics bottles.

Strategic Dairy Products Packaging Industry Market Forecast

The strategic dairy products packaging market forecast anticipates sustained growth, driven by an increasing global population and a rising demand for nutritious dairy products. Key growth catalysts include the widespread adoption of sustainable packaging materials, such as chemically recycled plastics and fiber-based alternatives, aligning with global environmental initiatives. The forecast also highlights the significant potential in emerging markets, where urbanization and improved living standards are boosting dairy consumption. Innovations in flexible packaging and convenient formats will continue to cater to evolving consumer lifestyles, ensuring a dynamic and expanding market landscape for the foreseeable future.

Dairy Products Packaging Industry Segmentation

-

1. Material

- 1.1. Plastic

- 1.2. Paper and Paperboard

- 1.3. Glass

- 1.4. Metal

-

2. Product

- 2.1. Milk

- 2.2. Cheese

- 2.3. Frozen Foods

- 2.4. Yogurt

- 2.5. Cultured Products

-

3. Package Type

- 3.1. Bottles

- 3.2. Pouches

- 3.3. Cartons and Boxes

- 3.4. Bags and Wraps

- 3.5. Other Package Types

Dairy Products Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Dairy Products Packaging Industry Regional Market Share

Geographic Coverage of Dairy Products Packaging Industry

Dairy Products Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Plastic

- 5.1.2. Paper and Paperboard

- 5.1.3. Glass

- 5.1.4. Metal

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Milk

- 5.2.2. Cheese

- 5.2.3. Frozen Foods

- 5.2.4. Yogurt

- 5.2.5. Cultured Products

- 5.3. Market Analysis, Insights and Forecast - by Package Type

- 5.3.1. Bottles

- 5.3.2. Pouches

- 5.3.3. Cartons and Boxes

- 5.3.4. Bags and Wraps

- 5.3.5. Other Package Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Dairy Products Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Plastic

- 6.1.2. Paper and Paperboard

- 6.1.3. Glass

- 6.1.4. Metal

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Milk

- 6.2.2. Cheese

- 6.2.3. Frozen Foods

- 6.2.4. Yogurt

- 6.2.5. Cultured Products

- 6.3. Market Analysis, Insights and Forecast - by Package Type

- 6.3.1. Bottles

- 6.3.2. Pouches

- 6.3.3. Cartons and Boxes

- 6.3.4. Bags and Wraps

- 6.3.5. Other Package Types

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. North America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Plastic

- 7.1.2. Paper and Paperboard

- 7.1.3. Glass

- 7.1.4. Metal

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Milk

- 7.2.2. Cheese

- 7.2.3. Frozen Foods

- 7.2.4. Yogurt

- 7.2.5. Cultured Products

- 7.3. Market Analysis, Insights and Forecast - by Package Type

- 7.3.1. Bottles

- 7.3.2. Pouches

- 7.3.3. Cartons and Boxes

- 7.3.4. Bags and Wraps

- 7.3.5. Other Package Types

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Europe Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Plastic

- 8.1.2. Paper and Paperboard

- 8.1.3. Glass

- 8.1.4. Metal

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Milk

- 8.2.2. Cheese

- 8.2.3. Frozen Foods

- 8.2.4. Yogurt

- 8.2.5. Cultured Products

- 8.3. Market Analysis, Insights and Forecast - by Package Type

- 8.3.1. Bottles

- 8.3.2. Pouches

- 8.3.3. Cartons and Boxes

- 8.3.4. Bags and Wraps

- 8.3.5. Other Package Types

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Asia Pacific Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Plastic

- 9.1.2. Paper and Paperboard

- 9.1.3. Glass

- 9.1.4. Metal

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Milk

- 9.2.2. Cheese

- 9.2.3. Frozen Foods

- 9.2.4. Yogurt

- 9.2.5. Cultured Products

- 9.3. Market Analysis, Insights and Forecast - by Package Type

- 9.3.1. Bottles

- 9.3.2. Pouches

- 9.3.3. Cartons and Boxes

- 9.3.4. Bags and Wraps

- 9.3.5. Other Package Types

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Latin America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Plastic

- 10.1.2. Paper and Paperboard

- 10.1.3. Glass

- 10.1.4. Metal

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Milk

- 10.2.2. Cheese

- 10.2.3. Frozen Foods

- 10.2.4. Yogurt

- 10.2.5. Cultured Products

- 10.3. Market Analysis, Insights and Forecast - by Package Type

- 10.3.1. Bottles

- 10.3.2. Pouches

- 10.3.3. Cartons and Boxes

- 10.3.4. Bags and Wraps

- 10.3.5. Other Package Types

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Middle East and Africa Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material

- 11.1.1. Plastic

- 11.1.2. Paper and Paperboard

- 11.1.3. Glass

- 11.1.4. Metal

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Milk

- 11.2.2. Cheese

- 11.2.3. Frozen Foods

- 11.2.4. Yogurt

- 11.2.5. Cultured Products

- 11.3. Market Analysis, Insights and Forecast - by Package Type

- 11.3.1. Bottles

- 11.3.2. Pouches

- 11.3.3. Cartons and Boxes

- 11.3.4. Bags and Wraps

- 11.3.5. Other Package Types

- 11.1. Market Analysis, Insights and Forecast - by Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Consolidated Container Company LLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Stora Enso Oyj

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ball Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Greiner Packaging international Gmb

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Berry Global Group Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Huhtamaki Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Winpak Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Amcor PLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 International Paper Company

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sealed Air Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Saudi Basic Industries Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Consolidated Container Company LLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Dairy Products Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 3: North America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 5: North America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 7: North America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 8: North America Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 11: Europe Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 12: Europe Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 13: Europe Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Europe Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 15: Europe Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 16: Europe Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 19: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 20: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 21: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 23: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 24: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 27: Latin America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 28: Latin America Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 29: Latin America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Latin America Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 31: Latin America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 32: Latin America Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 35: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 36: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 37: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 39: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 40: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 2: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 3: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 4: Global Dairy Products Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 6: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 7: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 8: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 10: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 11: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 12: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 14: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 15: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 16: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 18: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 19: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 20: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 22: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 23: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 24: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dairy Products Packaging Industry?

The projected CAGR is approximately 2.7%.

2. Which companies are prominent players in the Dairy Products Packaging Industry?

Key companies in the market include Consolidated Container Company LLC, Stora Enso Oyj, Ball Corporation, Greiner Packaging international Gmb, Berry Global Group Inc, Huhtamaki Group, Winpak Ltd, Amcor PLC, International Paper Company, Sealed Air Corporation, Saudi Basic Industries Corporation.

3. What are the main segments of the Dairy Products Packaging Industry?

The market segments include Material, Product, Package Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 33.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumer Preference Towards Protein-based Products; Increasing Adoption of Packages Incorporating Small Portion Size.

6. What are the notable trends driving market growth?

Milk Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

; Greenhouse Gas Emission due to Dairy Activities Leading to Legislative Issues.

8. Can you provide examples of recent developments in the market?

September 2021 - Greiner Packaging announced Emmi CAFFÈ LATTE, Europe's leading ready-to-drink iced coffee brand, will start incorporating its new chemically recycled polypropylene into packaging. Greiner Packaging makes these cups from chemically recycled material that comes from Borealis.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dairy Products Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dairy Products Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dairy Products Packaging Industry?

To stay informed about further developments, trends, and reports in the Dairy Products Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence