Key Insights

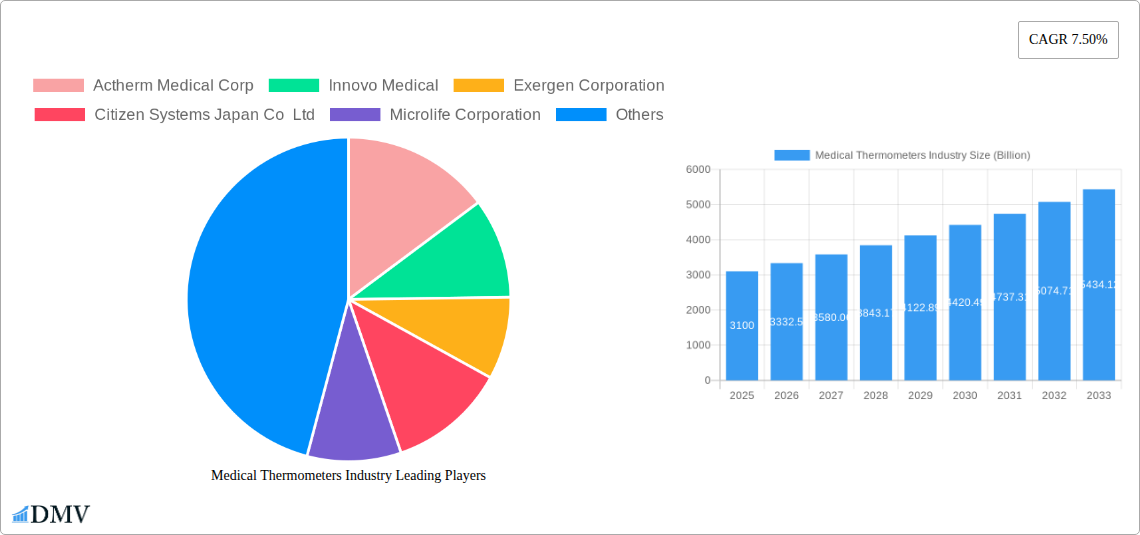

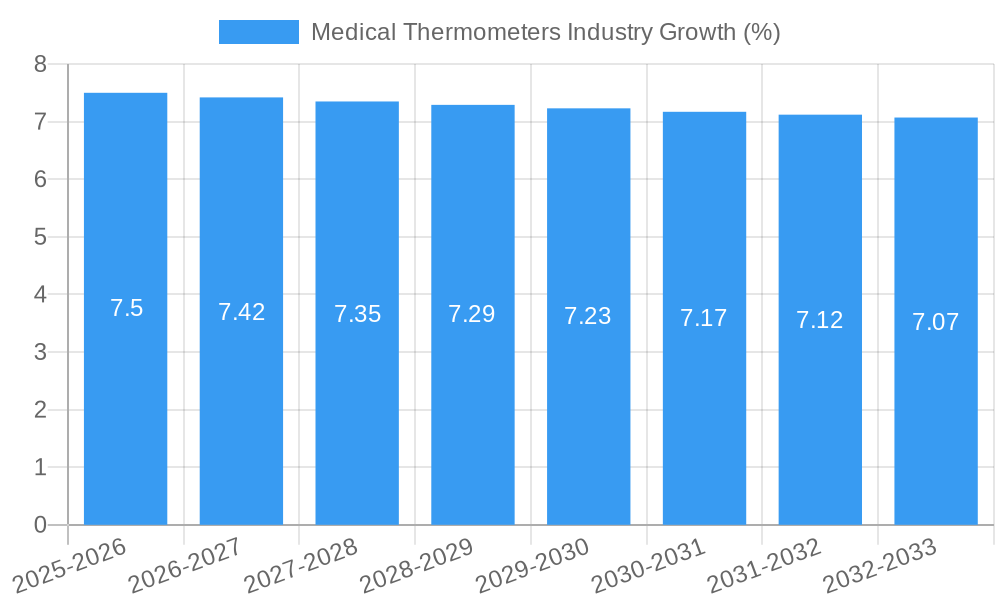

The global Medical Thermometers Market is poised for significant expansion, projected to reach an estimated USD 3.1 billion in 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of 7.50% through 2033. This upward trajectory is largely propelled by the increasing prevalence of infectious diseases and the growing awareness of proactive health monitoring. The demand for accurate and reliable temperature measurement devices is paramount in healthcare settings, from bustling hospitals to specialized clinics, driving innovation and market penetration. Advancements in technology are leading to the development of more sophisticated thermometers, including infrared and digital models that offer faster readings and enhanced user convenience. The shift towards non-mercury-based thermometers is also a significant trend, aligning with environmental concerns and regulatory mandates. The expanding healthcare infrastructure, particularly in emerging economies, coupled with a rising elderly population that requires consistent health surveillance, further bolsters the market's growth prospects.

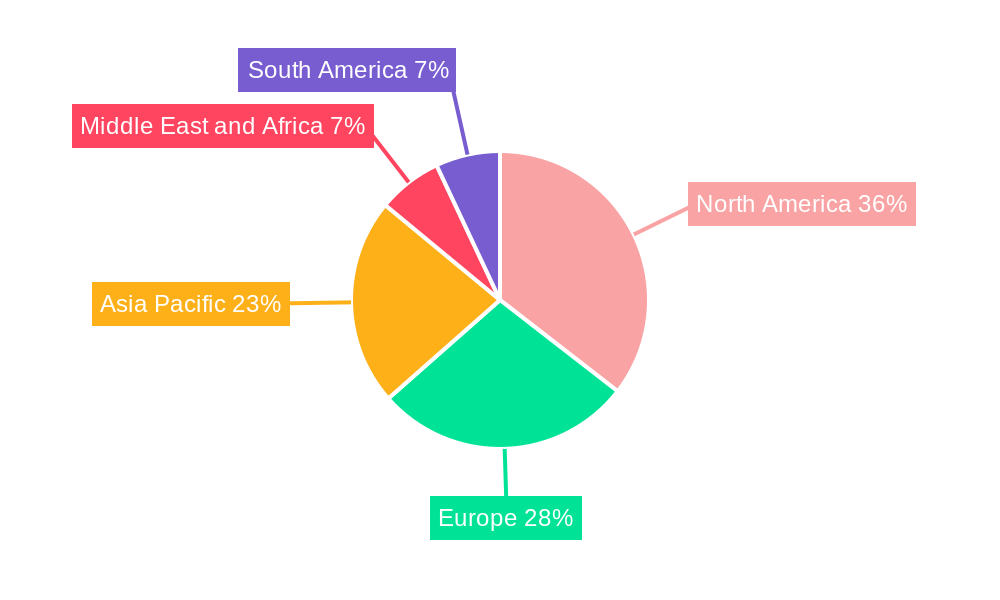

The market's expansion is further fueled by the increasing adoption of home healthcare solutions and the integration of smart devices that allow for remote patient monitoring. While the market is characterized by strong growth drivers, certain restraints, such as the initial cost of advanced digital thermometers and the need for continuous technological upgrades, may present challenges. However, the overwhelming benefits of early disease detection and efficient patient management are expected to outweigh these limitations. Key players are actively investing in research and development to introduce innovative products and expand their geographical reach. The United States and Europe currently dominate the market, but the Asia Pacific region is expected to witness the fastest growth due to its rapidly developing healthcare sector and a large, growing population. The continuous evolution of healthcare practices and the relentless pursuit of improved diagnostic tools will ensure sustained demand for medical thermometers, making it a dynamic and promising sector within the broader medical device industry.

Medical Thermometers Industry Market Composition & Trends

The global Medical Thermometers market is characterized by a dynamic interplay of innovation, regulatory oversight, and evolving end-user needs. Market concentration is moderately consolidated, with a few dominant players like Actherm Medical Corp, Innovo Medical, and Exergen Corporation holding significant market share. However, the landscape is also populated by numerous smaller, specialized manufacturers, particularly in the rapidly growing mercury-free segment. Innovation catalysts are primarily driven by the demand for faster, more accurate, and non-invasive temperature measurement solutions. The regulatory landscape, while stringent to ensure patient safety, also fosters innovation by setting clear performance standards. Substitute products, while not a direct threat to the core function of thermometers, include wearable health trackers with integrated temperature sensing capabilities, albeit with varying levels of clinical validation. End-user profiles are diverse, ranging from acute care settings in hospitals to home healthcare and consumer use, each with distinct purchasing criteria and adoption cycles. Mergers and acquisitions (M&A) activity, while not at an all-time high, remains a strategic tool for market expansion and technology integration. For instance, significant M&A deals in the broader medical devices sector indicate a trend towards consolidation for enhanced R&D and market reach, with estimated deal values in the hundreds of millions of US dollars. The market share distribution sees mercury-free thermometers, especially infrared and digital variants, steadily capturing a larger portion of the revenue pie, reflecting a global shift away from traditional mercury-based devices.

Medical Thermometers Industry Industry Evolution

The Medical Thermometers industry has undergone a significant transformation over the historical period of 2019–2024, driven by technological advancements, a heightened global focus on health monitoring, and increasing regulatory pressure to phase out mercury-based devices. The base year of 2025 marks a pivotal point, with the market poised for substantial growth throughout the forecast period of 2025–2033. Throughout the study period, the industry has witnessed a clear trajectory of increasing market value, projected to reach hundreds of billions of US dollars by 2033. This growth is intrinsically linked to the accelerating adoption of mercury-free thermometer technologies. Infrared thermometers, in particular, have experienced a meteoric rise in demand, propelled by their non-contact nature and rapid measurement capabilities, crucial for infection control and convenience. Digital thermometers have also solidified their position, offering enhanced accuracy and ease of use compared to their mercury predecessors. The COVID-19 pandemic acted as a significant catalyst, dramatically amplifying the demand for accurate and readily available temperature monitoring solutions across all end-user segments, from hospitals and clinics to individual households. This surge in demand not only boosted sales volumes but also spurred innovation in areas such as smart thermometers capable of data logging and remote monitoring, further integrating them into broader digital health ecosystems.

Technological advancements have been central to this evolution. The shift from manual reading to digital displays and subsequently to contactless infrared technology represents a paradigm shift. Miniaturization of components, improved sensor technology, and advancements in battery life have made portable and user-friendly devices more accessible. Furthermore, the integration of Bluetooth and Wi-Fi connectivity in some high-end models is enabling seamless data transfer to smartphones and electronic health records (EHRs), facilitating trend analysis and personalized healthcare. Consumer demand has evolved from basic functionality to a preference for speed, accuracy, ease of use, and increasingly, data connectivity. The widespread availability of information about health and hygiene practices has also empowered consumers to make more informed choices regarding their health monitoring equipment. Regulatory bodies worldwide have played a crucial role by implementing bans or restrictions on mercury-based thermometers, directly influencing manufacturing and market trends towards safer, mercury-free alternatives. This regulatory push, coupled with rising healthcare expenditure and an aging global population that requires more consistent health monitoring, has created a fertile ground for sustained market expansion. The adoption metrics for infrared and digital thermometers have been impressive, with market penetration rates steadily increasing year-on-year. The overall growth rate for the Medical Thermometers market is projected to remain robust, with an anticipated compound annual growth rate (CAGR) of approximately xx% during the forecast period.

Leading Regions, Countries, or Segments in Medical Thermometers Industry

The global Medical Thermometers market is experiencing significant growth and diversification across various regions and product segments. While specific regional dominance can fluctuate, North America and Europe have historically been leading markets due to high healthcare expenditure, advanced healthcare infrastructure, and strong regulatory frameworks encouraging the adoption of advanced medical devices. The Asia-Pacific region, however, is emerging as a powerhouse, driven by a rapidly expanding population, increasing disposable incomes, and a growing awareness of health and hygiene. Within the product type segmentation, the Mercury-free segment, encompassing Infrared and Digital thermometers, is unequivocally dominating market share and growth.

Dominance of Mercury-Free Thermometers: The global shift away from mercury-based thermometers, driven by environmental and health concerns, has cemented the leadership of mercury-free alternatives.

- Infrared Thermometers: These have witnessed exceptional growth, particularly non-contact infrared thermometers. Their ability to provide rapid, hygienic, and accurate readings without physical contact makes them indispensable in clinical settings like hospitals and clinics, as well as in public health screening and home use. The COVID-19 pandemic significantly accelerated their adoption, and this trend is expected to continue. Key drivers include their speed, ease of use, and reduced risk of cross-contamination.

- Digital Thermometers: While not as rapidly growing as infrared in terms of new adoption, digital thermometers continue to hold a substantial market share due to their affordability, accuracy, and widespread availability. They are a staple in households and are commonly found in various healthcare facilities. Their dominance is bolstered by their reliability and ease of understanding for a broad user base.

End-User Dominance: The Hospitals segment represents the largest end-user of medical thermometers.

- Hospitals: The high volume of patient care, stringent infection control protocols, and the need for rapid, accurate temperature monitoring for diagnosis and treatment make hospitals the primary consumers of medical thermometers. They invest in bulk purchases of both infrared and digital thermometers, with a growing preference for advanced, connected devices. The continuous influx of patients and the critical nature of vital sign monitoring ensure a constant demand.

- Clinics: Similar to hospitals, clinics also represent a significant end-user segment, requiring reliable temperature monitoring for routine check-ups, diagnosis, and treatment of various ailments. The increasing number of outpatient procedures and primary care services further fuels demand in this sector.

Key Drivers of Dominance:

- Regulatory Support: Bans and restrictions on mercury-based thermometers in numerous countries create a direct market advantage for mercury-free alternatives.

- Technological Advancements: Continuous innovation in infrared and digital thermometer technology, leading to improved accuracy, speed, and features like data connectivity, drives adoption.

- Infection Control: The emphasis on preventing the spread of infectious diseases, amplified by recent global health crises, strongly favors non-contact and hygienic thermometer solutions.

- Healthcare Expenditure: Rising global healthcare spending and the expansion of healthcare infrastructure, particularly in emerging economies, contribute to increased demand for medical devices, including thermometers.

- Consumer Awareness: Growing consumer awareness regarding health monitoring and the availability of advanced diagnostic tools encourages individuals to invest in reliable home-use thermometers.

Medical Thermometers Industry Product Innovations

The Medical Thermometers industry is abuzz with product innovations focused on enhancing accuracy, speed, and user experience. Advanced infrared sensors are enabling faster, non-contact temperature readings with impressive precision, often within milliseconds. Digital thermometers are integrating smart features, including memory functions for tracking temperature trends, connectivity via Bluetooth or Wi-Fi for data logging to smartphones and EHR systems, and improved ergonomic designs for comfortable handling. Innovations are also emerging in specialized applications, such as ear thermometers with enhanced probe designs for gentler insertion and forehead thermometers that can account for ambient temperature variations. The unique selling propositions often lie in the seamless integration of technology, providing not just a temperature reading but actionable health insights. These advancements are critical in elevating patient care and streamlining diagnostic processes across various healthcare settings.

Propelling Factors for Medical Thermometers Industry Growth

The growth of the Medical Thermometers industry is propelled by a confluence of technological, economic, and regulatory forces. Technological advancements, particularly in infrared and digital thermometer design, are yielding faster, more accurate, and user-friendly devices. The increasing global emphasis on public health and infection control, amplified by recent pandemics, has significantly boosted demand for hygienic and reliable temperature monitoring solutions. Economically, rising healthcare expenditure across both developed and developing nations, coupled with an aging global population requiring more consistent health monitoring, fuels market expansion. Regulatory shifts, such as the global phase-out of mercury-based thermometers, actively promote the adoption of safer, mercury-free alternatives, thereby creating a robust demand environment.

Obstacles in the Medical Thermometers Industry Market

Despite robust growth, the Medical Thermometers industry faces several obstacles. Stringent regulatory approval processes for new medical devices, while crucial for patient safety, can lead to extended product development timelines and increased costs. Supply chain disruptions, as witnessed in recent global events, can impact the availability of critical components and raw materials, leading to production delays and price volatility. Intense competition, especially from numerous manufacturers of generic digital thermometers, can exert downward pressure on pricing, affecting profit margins for some companies. Furthermore, the initial investment cost for advanced, feature-rich thermometers, such as those with connectivity, can be a barrier for smaller healthcare facilities or consumers in price-sensitive markets.

Future Opportunities in Medical Thermometers Industry

Emerging opportunities in the Medical Thermometers industry are vast and span new markets, technologies, and evolving consumer trends. The burgeoning telehealth and remote patient monitoring sectors present a significant avenue for growth, with opportunities for smart thermometers that seamlessly integrate with digital health platforms to provide continuous, data-driven insights. Emerging economies with expanding healthcare infrastructure and increasing health awareness offer untapped market potential for both basic and advanced thermometer solutions. The development of AI-powered diagnostic tools that leverage temperature data for early disease detection and personalized treatment plans is another promising frontier. Furthermore, the growing demand for at-home health monitoring solutions, driven by convenience and a proactive approach to wellness, will continue to fuel the market for user-friendly and technologically advanced consumer thermometers.

Major Players in the Medical Thermometers Industry Ecosystem

- Actherm Medical Corp

- Innovo Medical

- Exergen Corporation

- Citizen Systems Japan Co Ltd

- Microlife Corporation

- Cardinal Health

- Omron Healthcare Inc

- Welch Allyn Inc

- American Diagnostic Corporation

- A&D Company Limited

Key Developments in Medical Thermometers Industry Industry

- November 2022: TriMedika joined the UK Pavilion at MEDICA 2022 to showcase TRITEMP, a non-contact thermometer, highlighting innovative solutions in infection control.

- June 2022: Exergen Corporation launched the TAT-2000 for professionals and TAT-2000C for consumers at the medical fair in Mumbai, India, expanding its product portfolio for both clinical and home use.

Strategic Medical Thermometers Industry Market Forecast

The strategic forecast for the Medical Thermometers industry is exceptionally positive, driven by several key growth catalysts. The ongoing global push for enhanced infection control and public health monitoring will continue to fuel demand for advanced, mercury-free thermometers, particularly infrared and digital variants. Technological innovation, including the integration of smart features and connectivity for remote patient monitoring and telehealth applications, will unlock new revenue streams and market segments. Furthermore, the increasing healthcare expenditure in emerging economies and the persistent need for reliable temperature measurement in hospitals, clinics, and homes globally, ensure a sustained and robust market trajectory. The market potential is significant, with opportunities to capture market share through product differentiation, strategic partnerships, and a focus on emerging healthcare trends.

Medical Thermometers Industry Segmentation

-

1. Product Type

- 1.1. Mercury-based

-

1.2. Mercury-free

- 1.2.1. Infrared

- 1.2.2. Digital

- 1.2.3. Other Product Types

-

2. End User

- 2.1. Hospitals

- 2.2. Clinics

- 2.3. Other End Users

Medical Thermometers Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Medical Thermometers Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Number of Medical Conditions Requiring Accurate Measurement of Body Temperature; Rapid Technological Advancements

- 3.3. Market Restrains

- 3.3.1. Stringent Governing Policies by Regulatory Healthcare Authority; Accuracy Issues With Infrared Thermometers

- 3.4. Market Trends

- 3.4.1. Digital Segment is Expected to Hold a Major Market Share in the Medical Thermometer Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Mercury-based

- 5.1.2. Mercury-free

- 5.1.2.1. Infrared

- 5.1.2.2. Digital

- 5.1.2.3. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Clinics

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. North America Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Mercury-based

- 6.1.2. Mercury-free

- 6.1.2.1. Infrared

- 6.1.2.2. Digital

- 6.1.2.3. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Clinics

- 6.2.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Europe Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Mercury-based

- 7.1.2. Mercury-free

- 7.1.2.1. Infrared

- 7.1.2.2. Digital

- 7.1.2.3. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Clinics

- 7.2.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Asia Pacific Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Mercury-based

- 8.1.2. Mercury-free

- 8.1.2.1. Infrared

- 8.1.2.2. Digital

- 8.1.2.3. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Clinics

- 8.2.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Middle East and Africa Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Mercury-based

- 9.1.2. Mercury-free

- 9.1.2.1. Infrared

- 9.1.2.2. Digital

- 9.1.2.3. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Clinics

- 9.2.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Mercury-based

- 10.1.2. Mercury-free

- 10.1.2.1. Infrared

- 10.1.2.2. Digital

- 10.1.2.3. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Clinics

- 10.2.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. North America Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. South America Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Brazil

- 12.1.2 Mexico

- 12.1.3 Rest of South America

- 13. Europe Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 United Kingdom

- 13.1.2 Germany

- 13.1.3 France

- 13.1.4 Italy

- 13.1.5 Spain

- 13.1.6 Russia

- 13.1.7 Rest of Europe

- 14. Asia Pacific Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 China

- 14.1.2 Japan

- 14.1.3 India

- 14.1.4 South Korea

- 14.1.5 Taiwan

- 14.1.6 Australia

- 14.1.7 Rest of Asia-Pacific

- 15. MEA Medical Thermometers Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Middle East

- 15.1.2 Africa

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Actherm Medical Corp

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Innovo Medical

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Exergen Corporation

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Citizen Systems Japan Co Ltd

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Microlife Corporation

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Cardinal Health

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Omron Healthcare Inc

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Welch Allyn Inc *List Not Exhaustive

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 American Diagnostic Corporation

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 A&D Company Limited

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Actherm Medical Corp

List of Figures

- Figure 1: Global Medical Thermometers Industry Revenue Breakdown (Billion, %) by Region 2024 & 2032

- Figure 2: Global Medical Thermometers Industry Volume Breakdown (K Units, %) by Region 2024 & 2032

- Figure 3: North America Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 4: North America Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 5: North America Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: North America Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 7: South America Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 8: South America Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 9: South America Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 11: Europe Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 12: Europe Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 13: Europe Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 15: Asia Pacific Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 16: Asia Pacific Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 17: Asia Pacific Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Asia Pacific Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 19: MEA Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 20: MEA Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 21: MEA Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: MEA Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 23: North America Medical Thermometers Industry Revenue (Billion), by Product Type 2024 & 2032

- Figure 24: North America Medical Thermometers Industry Volume (K Units), by Product Type 2024 & 2032

- Figure 25: North America Medical Thermometers Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 26: North America Medical Thermometers Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 27: North America Medical Thermometers Industry Revenue (Billion), by End User 2024 & 2032

- Figure 28: North America Medical Thermometers Industry Volume (K Units), by End User 2024 & 2032

- Figure 29: North America Medical Thermometers Industry Revenue Share (%), by End User 2024 & 2032

- Figure 30: North America Medical Thermometers Industry Volume Share (%), by End User 2024 & 2032

- Figure 31: North America Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 32: North America Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 33: North America Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 34: North America Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 35: Europe Medical Thermometers Industry Revenue (Billion), by Product Type 2024 & 2032

- Figure 36: Europe Medical Thermometers Industry Volume (K Units), by Product Type 2024 & 2032

- Figure 37: Europe Medical Thermometers Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 38: Europe Medical Thermometers Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 39: Europe Medical Thermometers Industry Revenue (Billion), by End User 2024 & 2032

- Figure 40: Europe Medical Thermometers Industry Volume (K Units), by End User 2024 & 2032

- Figure 41: Europe Medical Thermometers Industry Revenue Share (%), by End User 2024 & 2032

- Figure 42: Europe Medical Thermometers Industry Volume Share (%), by End User 2024 & 2032

- Figure 43: Europe Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 44: Europe Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 45: Europe Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 46: Europe Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 47: Asia Pacific Medical Thermometers Industry Revenue (Billion), by Product Type 2024 & 2032

- Figure 48: Asia Pacific Medical Thermometers Industry Volume (K Units), by Product Type 2024 & 2032

- Figure 49: Asia Pacific Medical Thermometers Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 50: Asia Pacific Medical Thermometers Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 51: Asia Pacific Medical Thermometers Industry Revenue (Billion), by End User 2024 & 2032

- Figure 52: Asia Pacific Medical Thermometers Industry Volume (K Units), by End User 2024 & 2032

- Figure 53: Asia Pacific Medical Thermometers Industry Revenue Share (%), by End User 2024 & 2032

- Figure 54: Asia Pacific Medical Thermometers Industry Volume Share (%), by End User 2024 & 2032

- Figure 55: Asia Pacific Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 56: Asia Pacific Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 57: Asia Pacific Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 58: Asia Pacific Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 59: Middle East and Africa Medical Thermometers Industry Revenue (Billion), by Product Type 2024 & 2032

- Figure 60: Middle East and Africa Medical Thermometers Industry Volume (K Units), by Product Type 2024 & 2032

- Figure 61: Middle East and Africa Medical Thermometers Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 62: Middle East and Africa Medical Thermometers Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 63: Middle East and Africa Medical Thermometers Industry Revenue (Billion), by End User 2024 & 2032

- Figure 64: Middle East and Africa Medical Thermometers Industry Volume (K Units), by End User 2024 & 2032

- Figure 65: Middle East and Africa Medical Thermometers Industry Revenue Share (%), by End User 2024 & 2032

- Figure 66: Middle East and Africa Medical Thermometers Industry Volume Share (%), by End User 2024 & 2032

- Figure 67: Middle East and Africa Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 68: Middle East and Africa Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 69: Middle East and Africa Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 70: Middle East and Africa Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

- Figure 71: South America Medical Thermometers Industry Revenue (Billion), by Product Type 2024 & 2032

- Figure 72: South America Medical Thermometers Industry Volume (K Units), by Product Type 2024 & 2032

- Figure 73: South America Medical Thermometers Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 74: South America Medical Thermometers Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 75: South America Medical Thermometers Industry Revenue (Billion), by End User 2024 & 2032

- Figure 76: South America Medical Thermometers Industry Volume (K Units), by End User 2024 & 2032

- Figure 77: South America Medical Thermometers Industry Revenue Share (%), by End User 2024 & 2032

- Figure 78: South America Medical Thermometers Industry Volume Share (%), by End User 2024 & 2032

- Figure 79: South America Medical Thermometers Industry Revenue (Billion), by Country 2024 & 2032

- Figure 80: South America Medical Thermometers Industry Volume (K Units), by Country 2024 & 2032

- Figure 81: South America Medical Thermometers Industry Revenue Share (%), by Country 2024 & 2032

- Figure 82: South America Medical Thermometers Industry Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Medical Thermometers Industry Revenue Billion Forecast, by Region 2019 & 2032

- Table 2: Global Medical Thermometers Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 3: Global Medical Thermometers Industry Revenue Billion Forecast, by Product Type 2019 & 2032

- Table 4: Global Medical Thermometers Industry Volume K Units Forecast, by Product Type 2019 & 2032

- Table 5: Global Medical Thermometers Industry Revenue Billion Forecast, by End User 2019 & 2032

- Table 6: Global Medical Thermometers Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 7: Global Medical Thermometers Industry Revenue Billion Forecast, by Region 2019 & 2032

- Table 8: Global Medical Thermometers Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 9: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 10: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 11: United States Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 12: United States Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 13: Canada Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 14: Canada Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 15: Mexico Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 16: Mexico Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 17: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 18: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 19: Brazil Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 20: Brazil Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 21: Mexico Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 22: Mexico Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 23: Rest of South America Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 24: Rest of South America Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 25: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 26: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 27: United Kingdom Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 28: United Kingdom Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 29: Germany Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 30: Germany Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 31: France Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 32: France Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 33: Italy Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 34: Italy Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 35: Spain Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 36: Spain Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 37: Russia Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 38: Russia Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 39: Rest of Europe Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 40: Rest of Europe Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 41: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 42: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 43: China Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 44: China Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 45: Japan Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 46: Japan Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 47: India Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 48: India Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 49: South Korea Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 50: South Korea Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 51: Taiwan Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 52: Taiwan Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 53: Australia Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 54: Australia Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 55: Rest of Asia-Pacific Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 56: Rest of Asia-Pacific Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 57: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 58: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 59: Middle East Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 60: Middle East Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 61: Africa Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 62: Africa Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 63: Global Medical Thermometers Industry Revenue Billion Forecast, by Product Type 2019 & 2032

- Table 64: Global Medical Thermometers Industry Volume K Units Forecast, by Product Type 2019 & 2032

- Table 65: Global Medical Thermometers Industry Revenue Billion Forecast, by End User 2019 & 2032

- Table 66: Global Medical Thermometers Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 67: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 68: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 69: United States Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 70: United States Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 71: Canada Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 72: Canada Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 73: Mexico Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 74: Mexico Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 75: Global Medical Thermometers Industry Revenue Billion Forecast, by Product Type 2019 & 2032

- Table 76: Global Medical Thermometers Industry Volume K Units Forecast, by Product Type 2019 & 2032

- Table 77: Global Medical Thermometers Industry Revenue Billion Forecast, by End User 2019 & 2032

- Table 78: Global Medical Thermometers Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 79: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 80: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 81: Germany Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 82: Germany Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 83: United Kingdom Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 84: United Kingdom Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 85: France Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 86: France Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 87: Italy Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 88: Italy Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 89: Spain Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 90: Spain Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 91: Rest of Europe Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 92: Rest of Europe Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 93: Global Medical Thermometers Industry Revenue Billion Forecast, by Product Type 2019 & 2032

- Table 94: Global Medical Thermometers Industry Volume K Units Forecast, by Product Type 2019 & 2032

- Table 95: Global Medical Thermometers Industry Revenue Billion Forecast, by End User 2019 & 2032

- Table 96: Global Medical Thermometers Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 97: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 98: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 99: China Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 100: China Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 101: Japan Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 102: Japan Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 103: India Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 104: India Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 105: Australia Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 106: Australia Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 107: South Korea Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 108: South Korea Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 109: Rest of Asia Pacific Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 110: Rest of Asia Pacific Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 111: Global Medical Thermometers Industry Revenue Billion Forecast, by Product Type 2019 & 2032

- Table 112: Global Medical Thermometers Industry Volume K Units Forecast, by Product Type 2019 & 2032

- Table 113: Global Medical Thermometers Industry Revenue Billion Forecast, by End User 2019 & 2032

- Table 114: Global Medical Thermometers Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 115: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 116: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 117: GCC Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 118: GCC Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 119: South Africa Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 120: South Africa Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 121: Rest of Middle East and Africa Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 122: Rest of Middle East and Africa Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 123: Global Medical Thermometers Industry Revenue Billion Forecast, by Product Type 2019 & 2032

- Table 124: Global Medical Thermometers Industry Volume K Units Forecast, by Product Type 2019 & 2032

- Table 125: Global Medical Thermometers Industry Revenue Billion Forecast, by End User 2019 & 2032

- Table 126: Global Medical Thermometers Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 127: Global Medical Thermometers Industry Revenue Billion Forecast, by Country 2019 & 2032

- Table 128: Global Medical Thermometers Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 129: Brazil Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 130: Brazil Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 131: Argentina Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 132: Argentina Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 133: Rest of South America Medical Thermometers Industry Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 134: Rest of South America Medical Thermometers Industry Volume (K Units) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Thermometers Industry?

The projected CAGR is approximately 7.50%.

2. Which companies are prominent players in the Medical Thermometers Industry?

Key companies in the market include Actherm Medical Corp, Innovo Medical, Exergen Corporation, Citizen Systems Japan Co Ltd, Microlife Corporation, Cardinal Health, Omron Healthcare Inc, Welch Allyn Inc *List Not Exhaustive, American Diagnostic Corporation, A&D Company Limited.

3. What are the main segments of the Medical Thermometers Industry?

The market segments include Product Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.1 Billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Number of Medical Conditions Requiring Accurate Measurement of Body Temperature; Rapid Technological Advancements.

6. What are the notable trends driving market growth?

Digital Segment is Expected to Hold a Major Market Share in the Medical Thermometer Market.

7. Are there any restraints impacting market growth?

Stringent Governing Policies by Regulatory Healthcare Authority; Accuracy Issues With Infrared Thermometers.

8. Can you provide examples of recent developments in the market?

November 2022: TriMedika joined the UK Pavilion at MEDICA 2022 to showcase TRITEMP, a non-contact thermometer.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Thermometers Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Thermometers Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Thermometers Industry?

To stay informed about further developments, trends, and reports in the Medical Thermometers Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence