Key Insights

The global Implants for Cosmetic Surgery market is poised for significant expansion, with an estimated market size of $12.1 billion in 2025, projected to grow at a robust Compound Annual Growth Rate (CAGR) of 5.8% through 2033. This upward trajectory is primarily driven by an increasing global demand for aesthetic enhancements, a growing awareness and acceptance of cosmetic procedures, and advancements in implant technology offering safer and more natural-looking results. Key drivers include the rising disposable incomes in emerging economies, allowing a larger segment of the population to afford these elective procedures, and the influence of social media and celebrity culture in normalizing and popularizing cosmetic surgery. Furthermore, the development of innovative implant materials and techniques, such as personalized 3D-printed implants, is enhancing patient satisfaction and expanding the procedural scope.

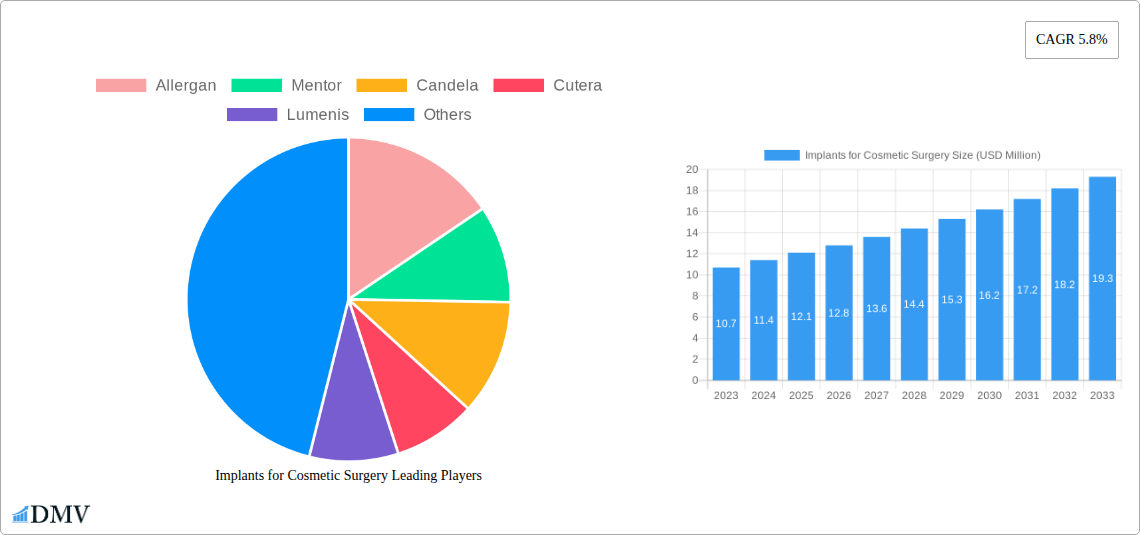

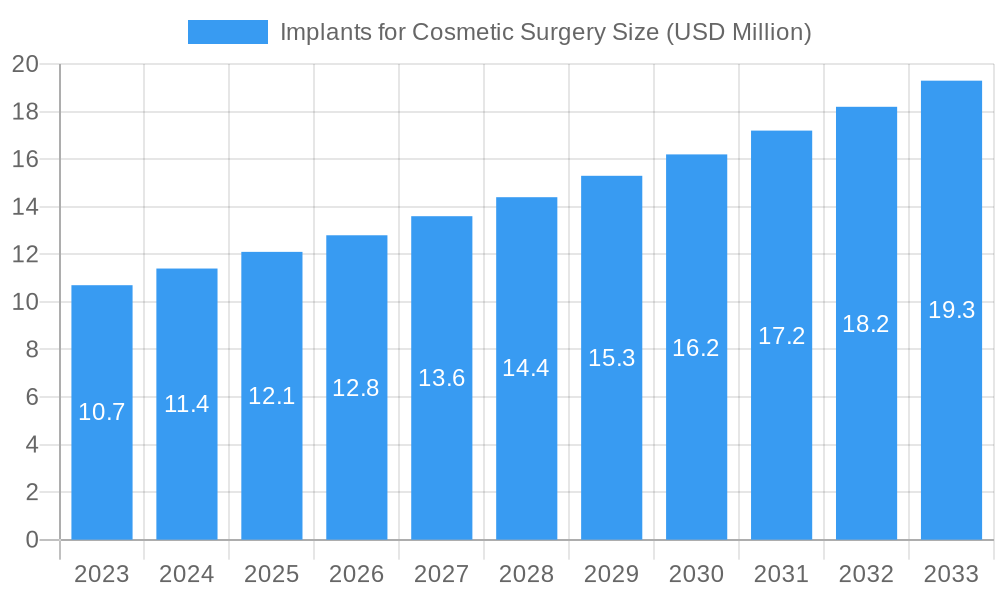

Implants for Cosmetic Surgery Market Size (In Million)

The market is segmented into applications across Hospitals, Dermatology Clinics, and Beauty Centers, with Hospitals likely dominating due to their comprehensive surgical infrastructure and specialized care. Types of implants primarily include Breast Implants and Chin & Cheek Implants, catering to the most popular areas of cosmetic enhancement. Restraints such as stringent regulatory approvals, potential post-operative complications, and the high cost of procedures are being mitigated by technological advancements and a greater emphasis on patient safety and education. The competitive landscape is characterized by the presence of major global players like Allergan, Mentor, Johnson & Johnson, and Medtronic, all investing heavily in research and development to maintain market share and introduce novel solutions. The Asia Pacific region, particularly China and India, is expected to emerge as a key growth engine due to a burgeoning middle class and a growing acceptance of aesthetic treatments.

Implants for Cosmetic Surgery Company Market Share

Implants for Cosmetic Surgery Market Composition & Trends

The global Implants for Cosmetic Surgery market is characterized by a dynamic blend of innovation and strategic consolidation. During the historical period of 2019-2024, market concentration has seen fluctuations driven by key acquisitions and technological advancements. Leading companies like Allergan, Mentor, and Johnson & Johnson have maintained significant market share, accounting for an estimated 60% of the total market value, which stood at $15 billion in 2024. Innovation catalysts are primarily focused on enhancing implant safety, longevity, and natural aesthetics, with ongoing research into bio-compatible materials and advanced imaging techniques for pre-operative planning. The regulatory landscape, particularly stringent in North America and Europe, continues to shape product development and market entry strategies, demanding rigorous clinical trials and post-market surveillance. Substitute products, such as minimally invasive aesthetic treatments, present a growing challenge, though they often target different patient needs and price points. End-user profiles are diversifying, encompassing a broader demographic seeking both reconstructive and aesthetic enhancements. Mergers and acquisitions (M&A) activities are expected to continue shaping the market, with estimated deal values in the past year reaching $2 billion, primarily involving smaller innovative firms being integrated into larger portfolios.

- Market Share Distribution: Major players hold an estimated 60% of the market.

- M&A Deal Values (Historical): Estimated at $2 billion in the preceding year.

- Key Market Influencers: Safety enhancements, aesthetic naturalness, regulatory compliance, and patient demographics.

Implants for Cosmetic Surgery Industry Evolution

The Implants for Cosmetic Surgery industry has undergone a remarkable transformation from 2019 to 2033, driven by a confluence of evolving consumer desires, groundbreaking technological leaps, and an increasingly sophisticated healthcare infrastructure. Throughout the historical period (2019-2024), the market witnessed steady growth, buoyed by a rising global disposable income and a burgeoning aesthetic consciousness. The base year, 2025, marks a pivotal point, with the market projected to reach an estimated $20 billion and poised for accelerated expansion throughout the forecast period (2025-2033). This trajectory is largely attributable to continuous innovation in implant materials and designs, leading to improved patient outcomes and reduced complication rates. For instance, the adoption of advanced silicone elastomers and saline-filled implants has become standard, offering greater versatility and patient satisfaction. Furthermore, the emergence of customizable implant solutions, catering to individual patient anatomies, represents a significant technological advancement, driving demand for personalized cosmetic procedures.

The industry's evolution is also intrinsically linked to shifting consumer demands. Beyond mere augmentation, patients now seek natural-looking results that seamlessly integrate with their existing features. This has spurred research and development into biomimetic materials and techniques that enhance tissue integration and minimize the risk of capsular contracture. The increasing acceptance and destigmatization of cosmetic surgery globally, particularly among younger demographics and across diverse socioeconomic strata, have further broadened the market's appeal. This shift is reflected in the growing demand for procedures beyond traditional breast augmentation, including chin and cheek implants, as well as reconstructive applications. Regulatory bodies worldwide have concurrently adapted, implementing stricter guidelines to ensure patient safety and efficacy, which, while initially posing challenges, have ultimately fostered greater trust and confidence in the industry. The integration of digital technologies, such as 3D imaging and virtual reality for pre-operative consultations, has also played a crucial role in enhancing patient education and procedural planning, contributing to higher success rates and improved patient experiences. This continuous cycle of innovation, coupled with expanding market access and evolving societal attitudes, positions the Implants for Cosmetic Surgery market for sustained and robust growth in the coming decade. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8% from 2025 to 2033.

Leading Regions, Countries, or Segments in Implants for Cosmetic Surgery

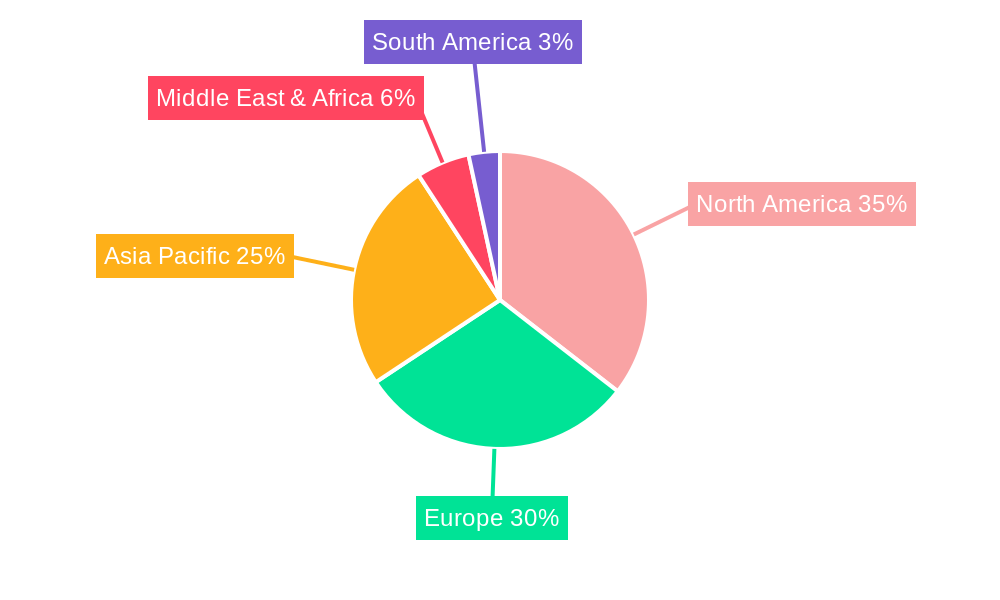

The Implants for Cosmetic Surgery market's dominance is multifaceted, with North America currently leading in terms of market value and adoption rates, projected to account for an estimated 35% of the global market share by 2025. This leadership is underpinned by a combination of factors, including high per capita disposable income, a strong culture of aesthetic enhancement, and advanced healthcare infrastructure that facilitates the adoption of cutting-edge technologies. Within North America, the United States remains the primary driver, supported by a high concentration of skilled surgeons and a robust demand for various implant types.

Dominant Segment: Breast Implants

Breast implants represent the largest and most influential segment within the Implants for Cosmetic Surgery market, expected to hold over 50% of the market value in 2025. This segment's dominance is fueled by several key drivers:

- High Patient Demand: Breast augmentation remains one of the most sought-after cosmetic procedures globally, driven by aesthetic desires and post-mastectomy reconstruction needs.

- Technological Advancements: Continuous improvements in implant materials, such as cohesive gel silicone and advanced surface texturing (e.g., by Mentor and Allergan), have led to more natural results and reduced complication rates. The estimated market size for breast implants alone is projected to reach $10 billion by 2025.

- Brand Influence: Established companies like Allergan and Mentor have built strong brand recognition and trust, influencing consumer choices and surgeon preferences.

- Reconstructive Applications: A significant portion of breast implant usage is for reconstructive purposes following mastectomy, further bolstering demand and market stability.

Leading Application: Hospitals and Dermatology Clinics

In terms of application, Hospitals and Dermatology Clinics are the leading segments, collectively projected to account for over 70% of the total market revenue in 2025.

- Hospitals: These facilities are crucial for both reconstructive surgeries, often covered by insurance, and complex cosmetic procedures requiring a comprehensive medical environment. Their established infrastructure and specialist teams attract a broad patient base.

- Dermatology Clinics: With the increasing integration of surgical and aesthetic services, specialized dermatology clinics are becoming primary centers for elective cosmetic implants. These clinics offer a more focused and personalized patient experience, catering to the growing demand for treatments like chin and cheek implants. The estimated market size for these two application segments combined is expected to be around $14 billion in 2025.

While Beauty Centers also contribute to the market, their role is often supplementary, focusing on non-surgical aesthetic treatments or post-operative care, representing an estimated 20% of the application segment.

Implants for Cosmetic Surgery Product Innovations

The Implants for Cosmetic Surgery landscape is continuously being reshaped by innovative product development focused on enhancing safety, aesthetics, and patient satisfaction. Key advancements include the introduction of next-generation cohesive gel silicone breast implants offering unparalleled natural feel and contouring, significantly reducing the incidence of rupture and leakage. Furthermore, the development of bio-integrative implant surfaces is a major breakthrough, promoting natural tissue adhesion and minimizing capsular contracture, a common complication. Companies like Medtronic and Johnson & Johnson are at the forefront of exploring novel biocompatible materials and incorporating smart technologies for real-time monitoring of implant integrity. The precise design and manufacturing of chin and cheek implants are also witnessing a surge in innovation, with customized solutions tailored to individual facial structures becoming increasingly accessible, leading to more harmonious and natural-looking results.

Propelling Factors for Implants for Cosmetic Surgery Growth

Several potent factors are propelling the growth of the Implants for Cosmetic Surgery market. Firstly, the increasing societal acceptance and destigmatization of aesthetic procedures are driving higher demand across diverse demographics. Technological advancements in implant materials and surgical techniques are leading to improved safety, natural results, and faster recovery times, further boosting patient confidence. The growing disposable income globally, particularly in emerging economies, makes these procedures more accessible to a wider population. Moreover, the expanding role of reconstructive surgery, especially post-mastectomy, provides a consistent and significant demand for implants. Finally, the influence of social media and celebrity culture continues to popularize cosmetic enhancements, creating aspirational trends that translate into market growth. The estimated market value in 2025 is projected to be around $20 billion.

Obstacles in the Implants for Cosmetic Surgery Market

Despite robust growth, the Implants for Cosmetic Surgery market faces several significant obstacles. Stringent and evolving regulatory landscapes across different regions can lead to increased compliance costs and delayed product approvals, impacting market entry for new innovations. The potential for adverse events and complications associated with implants, though decreasing with technological advancements, continues to be a concern that can impact public perception and patient willingness to undergo procedures. Supply chain disruptions, as witnessed in recent global events, can affect the availability and cost of raw materials and finished products. Furthermore, the competitive pressure from minimally invasive aesthetic treatments and the continuous development of non-surgical alternatives pose a threat, particularly for certain patient segments seeking less invasive solutions. The estimated impact of these obstacles on market growth could be a reduction of up to 5% annually.

Future Opportunities in Implants for Cosmetic Surgery

The Implants for Cosmetic Surgery market is ripe with emerging opportunities driven by ongoing innovation and evolving consumer preferences. The development of personalized and custom-fit implants, leveraging 3D printing and advanced imaging, represents a significant growth avenue, catering to the increasing demand for bespoke aesthetic solutions. Expansion into emerging markets in Asia-Pacific and Latin America, where aesthetic awareness is rapidly increasing and disposable incomes are rising, offers substantial untapped potential. Furthermore, advancements in bio-absorbable implants and regenerative technologies hold promise for future applications, potentially reducing the need for permanent implants and offering even greater safety. The integration of AI-powered pre-operative planning and patient selection tools can further enhance outcomes and patient satisfaction, opening new avenues for service integration and value creation.

Major Players in the Implants for Cosmetic Surgery Ecosystem

- Allergan

- Mentor

- Candela

- Cutera

- Lumenis

- Palomar Medical

- Iridex

- Solta Medical

- DermaMed Pharma

- Medtronic

- Johnson & Johnson

- Syneron Medical

- Cynosure

Key Developments in Implants for Cosmetic Surgery Industry

- 2023 (Q4): Allergan launches a new generation of cohesive gel breast implants with enhanced safety profiles and natural aesthetics.

- 2023 (Q3): Mentor announces significant advancements in bio-integrative surface technology for breast implants, aiming to reduce capsular contracture rates.

- 2023 (Q2): Johnson & Johnson acquires a leading developer of AI-powered surgical planning software, enhancing pre-operative customization for implant procedures.

- 2023 (Q1): Solta Medical expands its portfolio with the introduction of innovative chin implant designs focusing on subtle contour enhancement.

- 2022 (Q4): Medtronic receives regulatory approval for a new range of biocompatible materials for facial implants, promising improved tissue integration.

Strategic Implants for Cosmetic Surgery Market Forecast

The strategic Implants for Cosmetic Surgery market forecast is overwhelmingly positive, driven by a confluence of accelerating technological advancements and burgeoning global demand. The continued evolution of implant materials and design, focusing on enhanced safety, natural aesthetics, and patient-specific customization, will be a primary growth catalyst. Expansion into untapped emerging markets, coupled with the increasing acceptance of cosmetic procedures across broader demographic segments, promises significant market penetration. Furthermore, the integration of digital technologies for pre-operative planning and post-operative care will elevate patient outcomes and satisfaction, solidifying the industry's growth trajectory. The market is poised for sustained expansion, with an estimated market size of $35 billion by 2033.

Implants for Cosmetic Surgery Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Dermatology Clinics

- 1.3. Beauty Centers

- 1.4. Othes

-

2. Types

- 2.1. Breast Implants

- 2.2. Chin & Cheek Implants

Implants for Cosmetic Surgery Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Implants for Cosmetic Surgery Regional Market Share

Geographic Coverage of Implants for Cosmetic Surgery

Implants for Cosmetic Surgery REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Implants for Cosmetic Surgery Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Dermatology Clinics

- 5.1.3. Beauty Centers

- 5.1.4. Othes

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Breast Implants

- 5.2.2. Chin & Cheek Implants

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Implants for Cosmetic Surgery Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Dermatology Clinics

- 6.1.3. Beauty Centers

- 6.1.4. Othes

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Breast Implants

- 6.2.2. Chin & Cheek Implants

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Implants for Cosmetic Surgery Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Dermatology Clinics

- 7.1.3. Beauty Centers

- 7.1.4. Othes

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Breast Implants

- 7.2.2. Chin & Cheek Implants

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Implants for Cosmetic Surgery Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Dermatology Clinics

- 8.1.3. Beauty Centers

- 8.1.4. Othes

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Breast Implants

- 8.2.2. Chin & Cheek Implants

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Implants for Cosmetic Surgery Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Dermatology Clinics

- 9.1.3. Beauty Centers

- 9.1.4. Othes

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Breast Implants

- 9.2.2. Chin & Cheek Implants

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Implants for Cosmetic Surgery Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Dermatology Clinics

- 10.1.3. Beauty Centers

- 10.1.4. Othes

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Breast Implants

- 10.2.2. Chin & Cheek Implants

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Allergan

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Mentor

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Candela

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cutera

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lumenis

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Palomar Medical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Iridex

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Solta Medical

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DermaMed Pharma

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Medtronic

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Johnson & Johnson

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Syneron Medical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Cynosure

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Allergan

List of Figures

- Figure 1: Global Implants for Cosmetic Surgery Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Implants for Cosmetic Surgery Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Implants for Cosmetic Surgery Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Implants for Cosmetic Surgery Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Implants for Cosmetic Surgery Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Implants for Cosmetic Surgery Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Implants for Cosmetic Surgery Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Implants for Cosmetic Surgery Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Implants for Cosmetic Surgery Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Implants for Cosmetic Surgery Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Implants for Cosmetic Surgery Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Implants for Cosmetic Surgery Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Implants for Cosmetic Surgery Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Implants for Cosmetic Surgery Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Implants for Cosmetic Surgery Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Implants for Cosmetic Surgery Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Implants for Cosmetic Surgery Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Implants for Cosmetic Surgery Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Implants for Cosmetic Surgery Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Implants for Cosmetic Surgery Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Implants for Cosmetic Surgery Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Implants for Cosmetic Surgery Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Implants for Cosmetic Surgery Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Implants for Cosmetic Surgery Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Implants for Cosmetic Surgery Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Implants for Cosmetic Surgery Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Implants for Cosmetic Surgery Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Implants for Cosmetic Surgery Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Implants for Cosmetic Surgery Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Implants for Cosmetic Surgery Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Implants for Cosmetic Surgery Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Implants for Cosmetic Surgery Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Implants for Cosmetic Surgery Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Implants for Cosmetic Surgery?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Implants for Cosmetic Surgery?

Key companies in the market include Allergan, Mentor, Candela, Cutera, Lumenis, Palomar Medical, Iridex, Solta Medical, DermaMed Pharma, Medtronic, Johnson & Johnson, Syneron Medical, Cynosure.

3. What are the main segments of the Implants for Cosmetic Surgery?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Implants for Cosmetic Surgery," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Implants for Cosmetic Surgery report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Implants for Cosmetic Surgery?

To stay informed about further developments, trends, and reports in the Implants for Cosmetic Surgery, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence