Key Insights

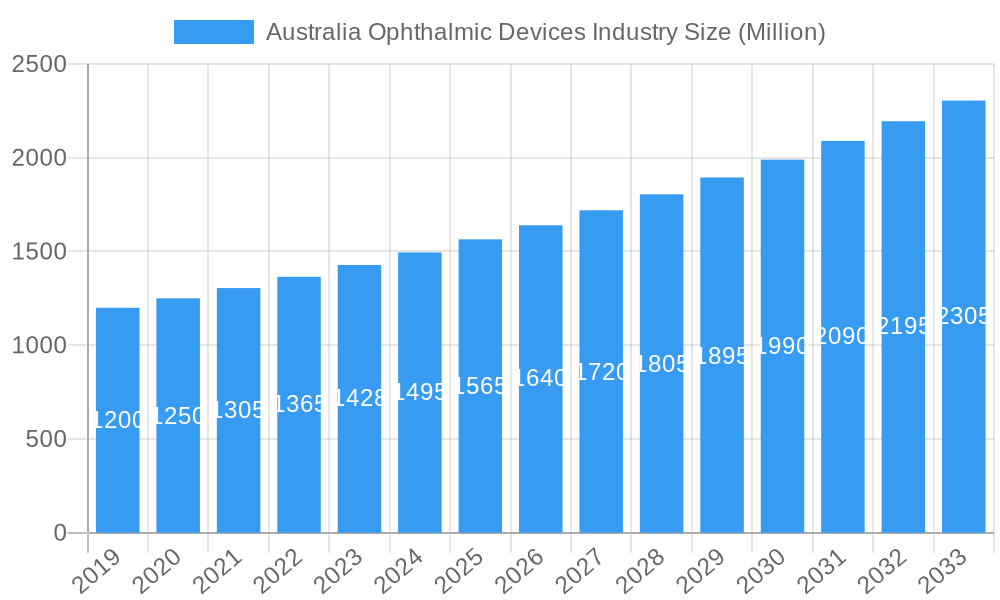

The Australian ophthalmic devices market is poised for robust growth, driven by an aging population, increasing prevalence of eye diseases like glaucoma and cataracts, and a rising demand for advanced vision correction solutions. With an estimated market size of approximately AUD 1,500 million (derived by estimating based on a global market size often in the tens of billions and Australia's share), the industry is projected to expand at a Compound Annual Growth Rate (CAGR) of 5.50% from 2025 to 2033. This sustained growth trajectory is underpinned by significant investments in research and development, leading to the introduction of innovative surgical devices such as advanced intraocular lenses (IOLs) and minimally invasive glaucoma drainage devices. Furthermore, the increasing adoption of sophisticated diagnostic and monitoring equipment, including autorefractors, corneal topography systems, and ophthalmic ultrasound imaging, is crucial in early disease detection and personalized treatment planning. The demand for vision correction devices, encompassing eyeglasses, contact lenses, and refractive surgery technologies, also continues to rise as awareness and disposable income grow.

Australia Ophthalmic Devices Industry Market Size (In Billion)

Key growth drivers within the Australian ophthalmic devices market include the high incidence of age-related macular degeneration (AMD), diabetic retinopathy, and cataracts, necessitating effective diagnostic and therapeutic interventions. Technological advancements, such as AI-powered diagnostic tools and robotic surgery systems, are gaining traction, promising enhanced precision and patient outcomes. However, the market also faces certain restraints, including the high cost of some advanced ophthalmic equipment, reimbursement challenges for certain procedures, and the need for specialized training for healthcare professionals to utilize cutting-edge technologies. Despite these challenges, the market is expected to witness substantial expansion across its various segments. Surgical devices, including glaucoma drainage devices and intraocular lenses, are anticipated to be significant contributors, alongside diagnostic and monitoring devices that facilitate early detection and management of eye conditions. The vision correction segment will also continue its upward trend, catering to a broad consumer base seeking improved visual acuity.

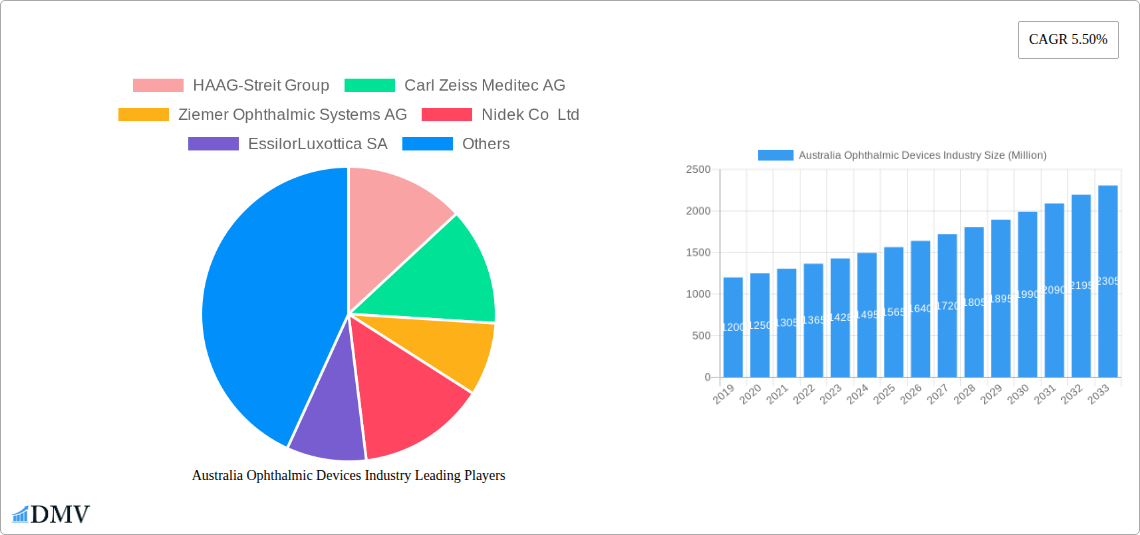

Australia Ophthalmic Devices Industry Company Market Share

Australia Ophthalmic Devices Industry Market Composition & Trends

The Australian ophthalmic devices market is characterized by a dynamic interplay of established players and emerging innovators, with a forecast market size estimated at $1,200 Million by 2025. Market concentration is moderate, driven by the presence of global giants alongside specialized local manufacturers. Innovation is a key catalyst, fueled by increasing investments in research and development for advanced diagnostics and minimally invasive surgical solutions. Regulatory frameworks, while stringent, are designed to ensure product safety and efficacy, influencing market entry and product lifecycle. Substitute products, such as eyeglasses and conventional contact lenses, continue to hold a share, but are increasingly challenged by superior technological advancements in surgical and advanced vision correction devices. End-user profiles are evolving, with a growing demand from an aging population experiencing age-related eye conditions and a younger demographic seeking convenient vision correction solutions. Mergers and acquisitions (M&A) activity is anticipated to remain robust, with estimated deal values reaching $300 Million annually as companies seek to consolidate market share, acquire innovative technologies, and expand their product portfolios. This strategic consolidation is crucial for navigating the competitive landscape and capitalizing on the burgeoning demand for cutting-edge ophthalmic solutions.

Australia Ophthalmic Devices Industry Industry Evolution

The Australian ophthalmic devices industry has witnessed a significant evolutionary trajectory from 2019 to 2024, driven by a confluence of technological advancements, shifting demographic patterns, and evolving consumer expectations. The historical period saw steady growth, underpinned by an increasing prevalence of age-related eye diseases such as cataracts and glaucoma, and a burgeoning awareness of refractive errors. This demand fueled the market for both diagnostic equipment and vision correction solutions. The base year, 2025, marks a pivotal point, with the market size projected to reach $1,200 Million, reflecting a compound annual growth rate (CAGR) of approximately 7.5% over the historical period. Technological advancements have been a primary engine of this evolution. The introduction of sophisticated surgical devices, including advanced intraocular lenses (IOLs) with enhanced multifocal and toric capabilities, has revolutionized cataract surgery, offering patients improved visual outcomes and reduced reliance on corrective eyewear. Similarly, the development of premium diagnostic and monitoring devices, such as high-resolution optical coherence tomography (OCT) systems and automated perimeters, has enabled earlier and more accurate detection of eye conditions, leading to timely interventions.

Shifting consumer demands have also played a crucial role. There's a discernible trend towards minimally invasive procedures, with patients increasingly opting for surgeries that offer quicker recovery times and fewer complications. This preference has spurred innovation in surgical instrumentation and implantable devices. Furthermore, the demand for personalized vision correction solutions is on the rise, with advancements in contact lens technology, including daily disposable silicone hydrogel lenses offering superior comfort and oxygen permeability, gaining substantial traction. The growing adoption of telehealth and remote monitoring technologies is also influencing the market, particularly for chronic eye condition management, driving the need for integrated diagnostic and software solutions. The forecast period, 2025–2033, is expected to witness continued robust growth, propelled by these ongoing trends and further technological breakthroughs. Projections indicate a sustained CAGR of approximately 8% for the forecast period, culminating in a market size estimated to exceed $2,000 Million by 2033. This sustained growth underscores the enduring demand for advanced ophthalmic care and the industry's capacity for innovation.

Leading Regions, Countries, or Segments in Australia Ophthalmic Devices Industry

The Australian ophthalmic devices industry exhibits a clear dominance by Surgical Devices, which are poised to capture a significant market share, projected to be around 45% by 2025. Within this segment, Intraocular Lenses (IOLs) stand out as a particularly high-growth sub-segment. The increasing incidence of age-related cataracts, coupled with a growing preference for advanced IOLs offering enhanced visual acuity and reduced dependence on spectacles, is a primary driver. Australia’s aging demographic, with a higher proportion of individuals over 60, directly correlates with the demand for cataract surgery and, consequently, IOLs. Investment trends in this sub-segment are substantial, with both local and international manufacturers investing heavily in R&D to develop premium IOLs with improved optical designs, accommodating designs, and enhanced biocompatibility. Regulatory support, while stringent in its approval processes, prioritizes patient safety and efficacy, which in turn encourages the development and adoption of high-quality surgical implants.

Another significant contributor to the dominance of Surgical Devices is the sub-segment of Other Surgical Devices. This encompasses a broad range of instruments and implants used in various ophthalmic surgeries beyond cataract procedures, including glaucoma surgery, retinal surgery, and refractive surgery. The rising adoption of minimally invasive surgical techniques in Australia is a key factor propelling the demand for specialized surgical tools and implants. For instance, advancements in glaucoma drainage devices, offering more predictable outcomes and improved patient comfort, are witnessing increased uptake.

While Surgical Devices lead, Diagnostic and Monitoring Devices are also crucial to the industry's landscape, expected to hold approximately 35% of the market share by 2025. Within this segment, Autorefractors and Keratometers remain foundational tools for refractive error assessment. However, Corneal Topography Systems and Ophthalmic Ultrasound Imaging Systems are experiencing accelerated growth due to their critical role in diagnosing complex corneal diseases, planning refractive surgeries, and monitoring post-operative outcomes. The increasing sophistication of these diagnostic tools, offering higher resolution imaging and advanced analytical capabilities, is driving their adoption in both hospital settings and private ophthalmology clinics across major urban centers like Sydney, Melbourne, and Brisbane. Investment in these areas is driven by the need for early and accurate disease detection, which ultimately leads to better treatment outcomes and reduced long-term healthcare costs.

The Vision Correction Devices segment, which includes contact lenses and spectacle lenses, is projected to account for the remaining 20% of the market share. While a mature market, innovation in contact lens materials, such as silicone hydrogels, and the increasing popularity of daily disposable lenses, are contributing to its sustained relevance and growth. Consumer demand for convenience and enhanced comfort in vision correction solutions continues to be a significant factor. The dominance of Surgical Devices, particularly IOLs, is a testament to Australia's focus on addressing age-related eye conditions and embracing advanced surgical interventions.

Australia Ophthalmic Devices Industry Product Innovations

The Australian ophthalmic devices industry is a hotbed of product innovation, consistently delivering advancements that enhance patient outcomes and physician capabilities. Recent breakthroughs include the development of next-generation intraocular lenses (IOLs) featuring enhanced aberration control for improved visual quality and reduced glare, particularly in low-light conditions. These innovations aim to minimize the need for corrective eyewear post-surgery. In the diagnostic realm, portable and AI-integrated autorefractors are emerging, offering faster and more accurate refractive error assessments, even in remote settings. Furthermore, advanced corneal topography systems are now capable of detecting subtle corneal irregularities that were previously undetectable, aiding in the early diagnosis and management of conditions like keratoconus. These product innovations are characterized by their increased precision, user-friendliness, and ability to provide personalized treatment plans, ultimately contributing to improved vision and eye health for the Australian population.

Propelling Factors for Australia Ophthalmic Devices Industry Growth

The Australia ophthalmic devices industry is propelled by several key growth drivers. An aging population is a significant demographic factor, increasing the prevalence of age-related eye conditions like cataracts and glaucoma, thereby driving demand for surgical interventions and related devices. Technological advancements, including the development of high-precision surgical instruments, sophisticated diagnostic imaging systems, and advanced intraocular lenses (IOLs), are continuously expanding treatment options and improving patient outcomes. Furthermore, government initiatives and private sector investments in healthcare infrastructure and research are fostering innovation and market expansion. The growing awareness among the Australian populace about eye health and the availability of advanced treatment options is also contributing to increased patient uptake of ophthalmic procedures and devices.

Obstacles in the Australia Ophthalmic Devices Industry Market

Despite its growth trajectory, the Australia ophthalmic devices industry faces certain obstacles. Stringent regulatory approval processes, while essential for patient safety, can sometimes lead to longer time-to-market for innovative products, increasing development costs. Reimbursement policies for advanced ophthalmic procedures and devices can also be a barrier, potentially limiting patient access to cutting-edge technologies. The high cost of some advanced ophthalmic devices can also present a challenge for widespread adoption, particularly in public healthcare settings. Furthermore, the industry is susceptible to global supply chain disruptions, which can impact the availability and pricing of raw materials and finished products. Competitive pressures from both established global players and emerging niche manufacturers also necessitate continuous innovation and cost-efficiency.

Future Opportunities in Australia Ophthalmic Devices Industry

The future of the Australia ophthalmic devices industry is ripe with opportunities. The increasing demand for refractive error correction, driven by lifestyle changes and a desire for convenient vision solutions, presents a significant avenue for growth in the vision correction devices segment, particularly for advanced contact lenses and innovative spectacle lens technologies. The burgeoning field of artificial intelligence (AI) in ophthalmology offers vast potential for developing smarter diagnostic tools, predictive analytics for disease progression, and AI-assisted surgical planning, leading to more personalized and effective treatments. Furthermore, the expansion of telehealth and remote patient monitoring solutions for chronic eye diseases presents an opportunity for integrated diagnostic and therapeutic device systems. Emerging markets and underserved regional areas within Australia also represent untapped potential for expanding access to advanced ophthalmic care.

Major Players in the Australia Ophthalmic Devices Industry Ecosystem

- HAAG-Streit Group

- Carl Zeiss Meditec AG

- Ziemer Ophthalmic Systems AG

- Nidek Co Ltd

- EssilorLuxottica SA

- Johnson and Johnson

- Topcon Corporation

- Alcon Inc

- Bausch Health Companies Inc

- Hoya Corporation

Key Developments in Australia Ophthalmic Devices Industry Industry

- March 2022: Rayner, the British manufacturer and distributor of intraocular lenses (IOLs) and ophthalmic solutions, established a regional office in Sydney to directly manage its product distribution.

- October 2021: SEED Co., Ltd. launched a new SEED 1-day Silfa silicone hydrogel daily disposable contact lens in Australia. SEED 1day Silfa features a low modulus allowing for excellent fitting characteristics and providing all-day comfort.

Strategic Australia Ophthalmic Devices Industry Market Forecast

The strategic forecast for the Australian ophthalmic devices industry indicates a sustained and robust growth trajectory, driven by a combination of demographic shifts, technological advancements, and evolving consumer needs. The increasing prevalence of age-related eye diseases like cataracts and glaucoma, coupled with a growing demand for minimally invasive surgical procedures and advanced vision correction solutions, will continue to fuel market expansion. Investment in research and development for innovative diagnostic equipment, sophisticated surgical devices, and premium IOLs is expected to remain high, leading to improved treatment efficacy and patient outcomes. The strategic imperative for market players will be to leverage these opportunities by focusing on product differentiation, expanding their distribution networks, and adapting to evolving reimbursement landscapes. The market is projected to reach $1,200 Million by 2025 and is anticipated to see continued growth through 2033.

Australia Ophthalmic Devices Industry Segmentation

-

1. Devices

-

1.1. Surgical Devices

- 1.1.1. Glaucoma Drainage Devices

- 1.1.2. Intraocular Lenses

- 1.1.3. Other Surgical Devices

-

1.2. Diagnostic and Monitoring Devices

- 1.2.1. Autorefractors and Keratometers

- 1.2.2. Corneal Topography Systems

- 1.2.3. Ophthalmic Ultrasound Imaging Systems

- 1.2.4. Other Diagnostic and Monitoring Devices

- 1.3. Vision Correction Devices

-

1.1. Surgical Devices

Australia Ophthalmic Devices Industry Segmentation By Geography

- 1. Australia

Australia Ophthalmic Devices Industry Regional Market Share

Geographic Coverage of Australia Ophthalmic Devices Industry

Australia Ophthalmic Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Devices

- 5.1.1. Surgical Devices

- 5.1.1.1. Glaucoma Drainage Devices

- 5.1.1.2. Intraocular Lenses

- 5.1.1.3. Other Surgical Devices

- 5.1.2. Diagnostic and Monitoring Devices

- 5.1.2.1. Autorefractors and Keratometers

- 5.1.2.2. Corneal Topography Systems

- 5.1.2.3. Ophthalmic Ultrasound Imaging Systems

- 5.1.2.4. Other Diagnostic and Monitoring Devices

- 5.1.3. Vision Correction Devices

- 5.1.1. Surgical Devices

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Devices

- 6. Australia Ophthalmic Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Devices

- 6.1.1. Surgical Devices

- 6.1.1.1. Glaucoma Drainage Devices

- 6.1.1.2. Intraocular Lenses

- 6.1.1.3. Other Surgical Devices

- 6.1.2. Diagnostic and Monitoring Devices

- 6.1.2.1. Autorefractors and Keratometers

- 6.1.2.2. Corneal Topography Systems

- 6.1.2.3. Ophthalmic Ultrasound Imaging Systems

- 6.1.2.4. Other Diagnostic and Monitoring Devices

- 6.1.3. Vision Correction Devices

- 6.1.1. Surgical Devices

- 6.1. Market Analysis, Insights and Forecast - by Devices

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 HAAG-Streit Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Carl Zeiss Meditec AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Ziemer Ophthalmic Systems AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Nidek Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 EssilorLuxottica SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Johnson and Johnson

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Topcon Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Alcon Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Bausch Health Companies Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Hoya Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 HAAG-Streit Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Ophthalmic Devices Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Australia Ophthalmic Devices Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Ophthalmic Devices Industry Revenue Million Forecast, by Devices 2020 & 2033

- Table 2: Australia Ophthalmic Devices Industry Volume K Unit Forecast, by Devices 2020 & 2033

- Table 3: Australia Ophthalmic Devices Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Australia Ophthalmic Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 5: Australia Ophthalmic Devices Industry Revenue Million Forecast, by Devices 2020 & 2033

- Table 6: Australia Ophthalmic Devices Industry Volume K Unit Forecast, by Devices 2020 & 2033

- Table 7: Australia Ophthalmic Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Australia Ophthalmic Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Ophthalmic Devices Industry?

The projected CAGR is approximately 5.50%.

2. Which companies are prominent players in the Australia Ophthalmic Devices Industry?

Key companies in the market include HAAG-Streit Group, Carl Zeiss Meditec AG, Ziemer Ophthalmic Systems AG, Nidek Co Ltd, EssilorLuxottica SA, Johnson and Johnson, Topcon Corporation, Alcon Inc, Bausch Health Companies Inc, Hoya Corporation.

3. What are the main segments of the Australia Ophthalmic Devices Industry?

The market segments include Devices.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Demographic Shift and Increasing Prevalence of Eye Diseases; Rising Geriatric Population; Technological Advancements in Ophthalmic Devices.

6. What are the notable trends driving market growth?

Vision Correction Devices are Expected to Register a High Growth CAGR Over the Forecast Period.

7. Are there any restraints impacting market growth?

Risk Associated with Ophthalmic Procedures.

8. Can you provide examples of recent developments in the market?

In March 2022, Rayner, the British manufacturer and distributor of intraocular lenses (IOLs) and ophthalmic solutions, established a regional office in Sydney to directly manage its product distribution.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Ophthalmic Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Ophthalmic Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Ophthalmic Devices Industry?

To stay informed about further developments, trends, and reports in the Australia Ophthalmic Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence