Key Insights

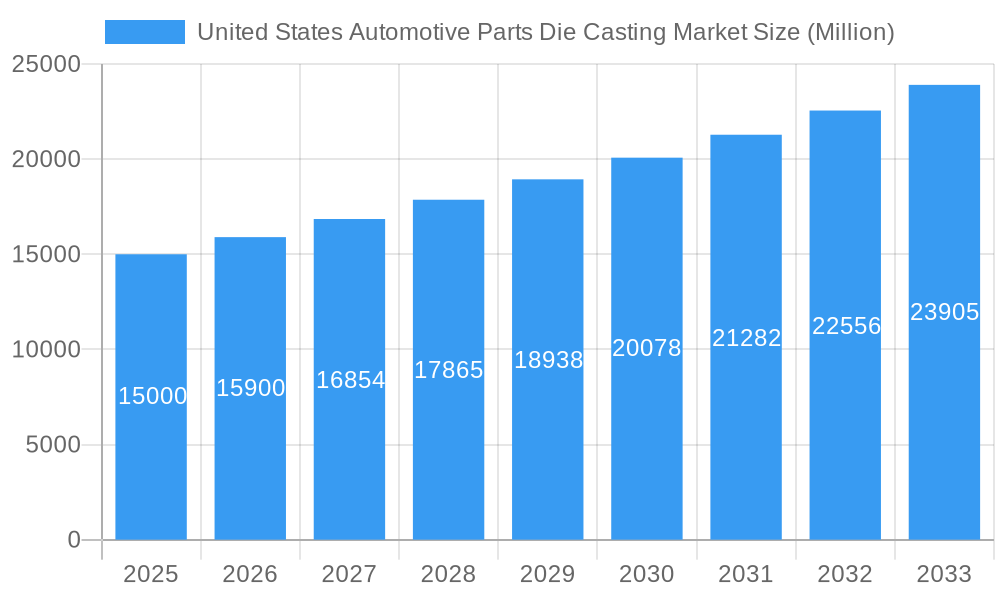

The United States automotive parts die casting market is projected for substantial growth, propelled by the increasing demand for lightweight vehicles to enhance fuel efficiency and reduce emissions. The market is forecast to reach 3580.4 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 4.7% from the base year of 2025. This expansion is further stimulated by the rising adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs), which necessitate precision-engineered die-cast components. Aluminum remains the primary raw material, valued for its strength and low weight, with magnesium usage increasing for applications requiring extreme lightweighting. Pressure die casting dominates due to speed and cost-efficiency, though vacuum and squeeze die casting are gaining traction for superior surface finish and dimensional accuracy in high-performance parts. Key industry leaders are investing in advanced technologies and production capacity to meet this escalating demand. Despite potential supply chain and material cost challenges, technological advancements and environmental mandates remain significant market drivers.

United States Automotive Parts Die Casting Market Market Size (In Billion)

Market segmentation highlights critical trends. Pressure die casting leads in market share, but vacuum and squeeze die casting are seeing increased adoption for intricate component designs and enhanced surface qualities, aligning with automotive industry advancements. Aluminum continues to be the preferred raw material due to its optimal strength-to-weight ratio and cost. However, magnesium is expected to witness steady growth, driven by the imperative for lightweighting in electric and hybrid vehicles. The market exhibits moderate concentration, featuring a blend of global corporations and regional specialists. This competitive environment fosters innovation and cost optimization, enhancing market accessibility and growth. The forecast period (2025-2033) anticipates sustained growth, though economic conditions and regulatory frameworks may influence the trajectory.

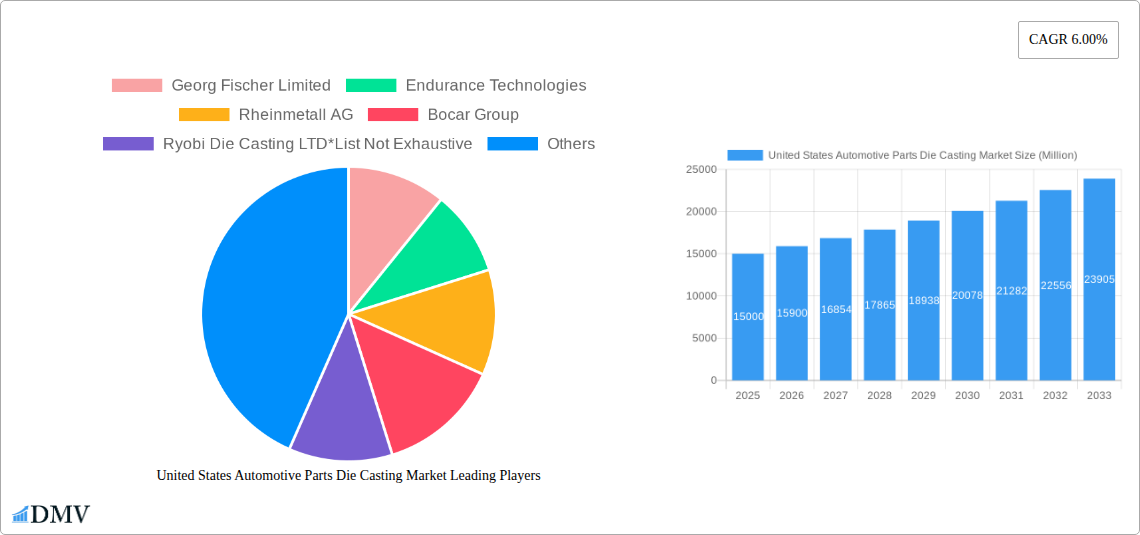

United States Automotive Parts Die Casting Market Company Market Share

United States Automotive Parts Die Casting Market: A Comprehensive Report (2019-2033)

This insightful report provides a deep dive into the dynamic United States automotive parts die casting market, offering a comprehensive analysis of market trends, growth drivers, challenges, and future opportunities. Covering the period from 2019 to 2033, with a focus on 2025 as the base and estimated year, this study is essential for stakeholders seeking to navigate this evolving landscape. The report meticulously examines market segmentation by process (Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, Others) and raw material (Aluminum, Magnesium, Zinc), providing granular insights for strategic decision-making. With a market value projected to reach xx Million by 2033, understanding this sector's intricacies is paramount.

United States Automotive Parts Die Casting Market Market Composition & Trends

This section offers a detailed analysis of the competitive landscape, encompassing market concentration, innovative advancements, regulatory frameworks, substitute products, end-user profiles, and merger & acquisition (M&A) activities within the US automotive parts die casting market. We delve into the market share distribution among key players, quantifying the influence of each major participant. The report further explores the impact of technological disruptions, government regulations (such as emission standards and safety regulations impacting material choices), and the emergence of substitute materials on market dynamics. Finally, we examine the strategic implications of M&A activities, providing insights into deal values and their influence on market consolidation. Key players analyzed include Georg Fischer Limited, Endurance Technologies, Rheinmetall AG, Bocar Group, Ryobi Die Casting LTD, Nemak, Form Technologies Inc., Shiloh Industries, and Rockman Industries (list not exhaustive). We analyze the impact of these factors on the market’s overall trajectory, predicting a xx% CAGR during the forecast period (2025-2033).

- Market Concentration: Analysis of market share distribution among top players, revealing the level of competition and potential for consolidation. xx% of the market is controlled by the top 5 players in 2025.

- Innovation Catalysts: Examination of technological advancements driving innovation, such as advancements in die casting alloys and automation.

- Regulatory Landscape: Assessment of the impact of government regulations on market growth and material selection.

- Substitute Products: Analysis of alternative manufacturing processes and materials challenging die casting's dominance.

- End-User Profiles: Profiling key automotive manufacturers driving demand for die-cast components.

- M&A Activities: Review of significant M&A deals, including their value and implications for market structure. Total M&A deal value in the past five years is estimated at xx Million.

United States Automotive Parts Die Casting Market Industry Evolution

This section provides a comprehensive overview of the historical and projected growth trajectory of the US automotive parts die casting market. We analyze the long-term market trends, pinpointing key inflection points influenced by technological advancements, shifting consumer preferences, and evolving automotive manufacturing techniques. The analysis incorporates detailed data points on growth rates, adoption metrics for new technologies, and the impact of macroeconomic factors. This section will quantify the market's response to the increased demand for lightweight vehicles and the transition towards electric vehicles, highlighting the market's adaptability and resilience in the face of change. The historical period (2019-2024) shows a CAGR of xx%, while the forecast period (2025-2033) projects a CAGR of xx%. This difference will be explained through factors such as economic shifts and material availability. We discuss the increasing adoption of automation, the shift towards sustainable manufacturing practices, and their implications for the future growth of the market. The transition from traditional gasoline-powered vehicles to electric vehicles (EVs) and hybrids will be discussed in depth.

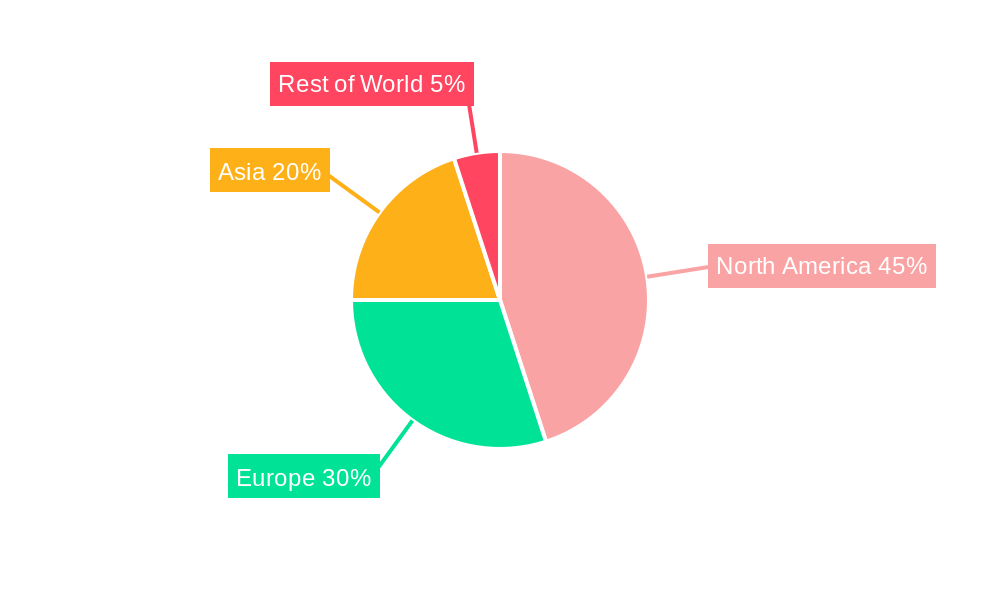

Leading Regions, Countries, or Segments in United States Automotive Parts Die Casting Market

This section identifies the dominant regions, countries, or segments within the US automotive parts die casting market. We will analyze the market share held by each segment (by process and raw material) and pinpoint the key drivers behind their leadership positions. This analysis incorporates detailed data on investment trends, regulatory support, and the specific factors contributing to each segment's dominance. The Midwest region is projected to lead the market in 2025, driven by a high concentration of automotive manufacturing facilities.

By Process:

- Pressure Die Casting: This segment dominates the market due to its cost-effectiveness and high production rates. Key drivers include high volume production capabilities and established infrastructure.

- Vacuum Die Casting: This segment shows potential for growth due to its ability to produce high-quality castings with improved surface finish. Key drivers include its superior quality and the increasing demand for precision components.

- Squeeze Die Casting: This niche segment holds a smaller share but caters to specific high-precision applications. Key drivers include its ability to create complex geometries and tighter tolerances.

- Others: This segment represents emerging technologies and specialized processes with limited market share.

By Raw Material:

- Aluminum: This is the most widely used material due to its lightweight properties and high strength-to-weight ratio. Key drivers include the automotive industry's focus on fuel efficiency and lightweighting initiatives.

- Magnesium: Magnesium shows growth potential due to its even lighter weight, but faces challenges related to higher cost and processing complexities. Key drivers include the increasing demand for ultra-lightweight components and government regulations supporting fuel efficiency.

- Zinc: Zinc is used for specific applications where corrosion resistance is crucial. Key drivers include its cost effectiveness and excellent corrosion resistance properties.

United States Automotive Parts Die Casting Market Product Innovations

This section highlights recent product innovations in die casting technology and their impact on the market. We showcase unique selling propositions (USPs) of newly launched products and explore technological advancements like the use of advanced alloys and improved casting processes, including automation technologies. These innovations enhance product performance, reduce production costs, and improve overall efficiency. The adoption of additive manufacturing techniques in die design and development is discussed, leading to faster development cycles and cost optimization.

Propelling Factors for United States Automotive Parts Die Casting Market Growth

Several factors drive the growth of the US automotive parts die casting market. Technological advancements in die casting processes and materials, coupled with the automotive industry's ongoing pursuit of lightweighting and fuel efficiency, are key drivers. The demand for electric vehicles (EVs) is significantly impacting the market, necessitating components with specific properties and creating new opportunities for die casters. Favorable government regulations, supporting initiatives like fuel efficiency standards, further encourage market expansion.

Obstacles in the United States Automotive Parts Die Casting Market Market

The US automotive parts die casting market faces several challenges. Fluctuations in raw material prices and supply chain disruptions impact production costs and profitability. Intense competition among established players and the entry of new competitors create pricing pressures. Strict environmental regulations and the need for sustainable manufacturing practices increase operational costs. Furthermore, the cyclical nature of the automotive industry adds further volatility to the market.

Future Opportunities in United States Automotive Parts Die Casting Market

Emerging opportunities exist within the US automotive parts die casting market. The growing demand for electric and hybrid vehicles creates new opportunities for specialized die-cast components. Advancements in materials science and die casting processes continuously open up new possibilities. Further penetration into niche markets, such as aerospace and medical devices, offer significant growth potential. The adoption of Industry 4.0 technologies, such as automation and data analytics, will further boost market expansion.

Major Players in the United States Automotive Parts Die Casting Market Ecosystem

- Georg Fischer Limited [Georg Fischer Limited]

- Endurance Technologies

- Rheinmetall AG [Rheinmetall AG]

- Bocar Group

- Ryobi Die Casting LTD

- Nemak [Nemak]

- Form Technologies Inc.

- Shiloh Industries [Shiloh Industries]

- Rockman Industries

Key Developments in United States Automotive Parts Die Casting Market Industry

- January 2023: Company X launched a new high-strength aluminum alloy for automotive applications.

- March 2024: Company Y acquired Company Z, expanding its market share and production capacity.

- October 2024: Significant investment in automation technology by a major die casting company. (Specific company name and details will be added in final report)

Strategic United States Automotive Parts Die Casting Market Market Forecast

The US automotive parts die casting market is poised for continued growth, fueled by technological advancements, the rise of EVs, and favorable government regulations. While challenges remain, the market's adaptability and innovative capabilities position it for substantial expansion in the coming years. The strategic focus on lightweighting, sustainability, and automation will be crucial factors determining market success in the forecast period. This report provides critical insights to help navigate the market’s complexities and capitalize on emerging opportunities.

United States Automotive Parts Die Casting Market Segmentation

-

1. Process

- 1.1. Pressure Die Casting

- 1.2. Vacuum Die Casting

- 1.3. Squeeze Die Casting

- 1.4. Others

-

2. Raw Material

- 2.1. Aluminium

- 2.2. Magnesium

- 2.3. Zinc

United States Automotive Parts Die Casting Market Segmentation By Geography

- 1. United States

United States Automotive Parts Die Casting Market Regional Market Share

Geographic Coverage of United States Automotive Parts Die Casting Market

United States Automotive Parts Die Casting Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Process

- 5.1.1. Pressure Die Casting

- 5.1.2. Vacuum Die Casting

- 5.1.3. Squeeze Die Casting

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Raw Material

- 5.2.1. Aluminium

- 5.2.2. Magnesium

- 5.2.3. Zinc

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Process

- 6. United States Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Process

- 6.1.1. Pressure Die Casting

- 6.1.2. Vacuum Die Casting

- 6.1.3. Squeeze Die Casting

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Raw Material

- 6.2.1. Aluminium

- 6.2.2. Magnesium

- 6.2.3. Zinc

- 6.1. Market Analysis, Insights and Forecast - by Process

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Georg Fischer Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Endurance Technologies

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Rheinmetall AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bocar Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ryobi Die Casting LTD*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nemak

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Form Technologies In

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shiloh Industries

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rockman Industries

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Georg Fischer Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Automotive Parts Die Casting Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: United States Automotive Parts Die Casting Market Share (%) by Company 2025

List of Tables

- Table 1: United States Automotive Parts Die Casting Market Revenue million Forecast, by Process 2020 & 2033

- Table 2: United States Automotive Parts Die Casting Market Revenue million Forecast, by Raw Material 2020 & 2033

- Table 3: United States Automotive Parts Die Casting Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: United States Automotive Parts Die Casting Market Revenue million Forecast, by Process 2020 & 2033

- Table 5: United States Automotive Parts Die Casting Market Revenue million Forecast, by Raw Material 2020 & 2033

- Table 6: United States Automotive Parts Die Casting Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Automotive Parts Die Casting Market?

The projected CAGR is approximately 4.7%.

2. Which companies are prominent players in the United States Automotive Parts Die Casting Market?

Key companies in the market include Georg Fischer Limited, Endurance Technologies, Rheinmetall AG, Bocar Group, Ryobi Die Casting LTD*List Not Exhaustive, Nemak, Form Technologies In, Shiloh Industries, Rockman Industries.

3. What are the main segments of the United States Automotive Parts Die Casting Market?

The market segments include Process, Raw Material.

4. Can you provide details about the market size?

The market size is estimated to be USD 3580.4 million as of 2022.

5. What are some drivers contributing to market growth?

Surge in Trend of Yacht Tourism.

6. What are the notable trends driving market growth?

Cost Issues and Resource Inefficiencies.

7. Are there any restraints impacting market growth?

Higher Rentals During Peak Season.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Automotive Parts Die Casting Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Automotive Parts Die Casting Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Automotive Parts Die Casting Market?

To stay informed about further developments, trends, and reports in the United States Automotive Parts Die Casting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence