Key Insights

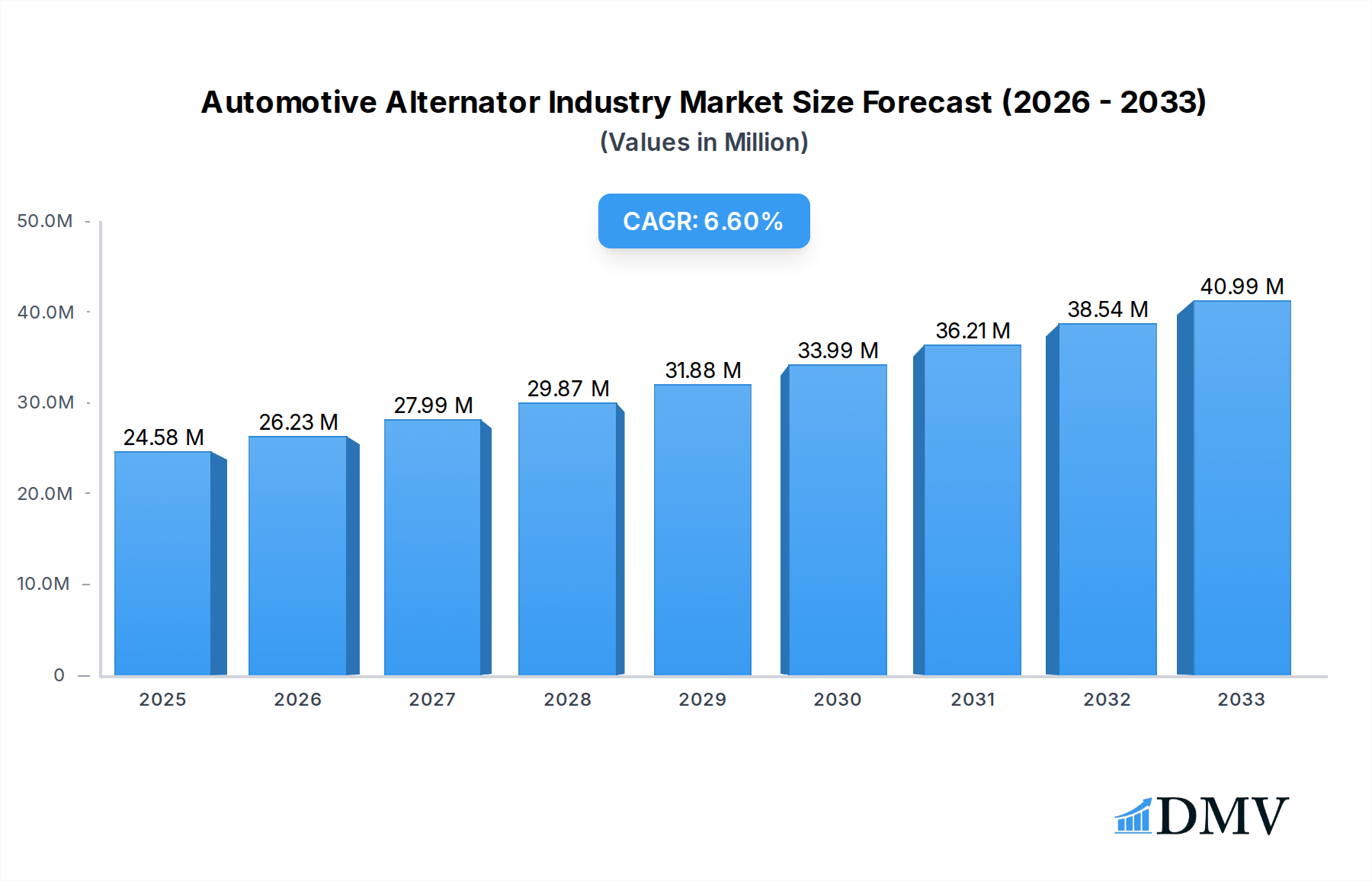

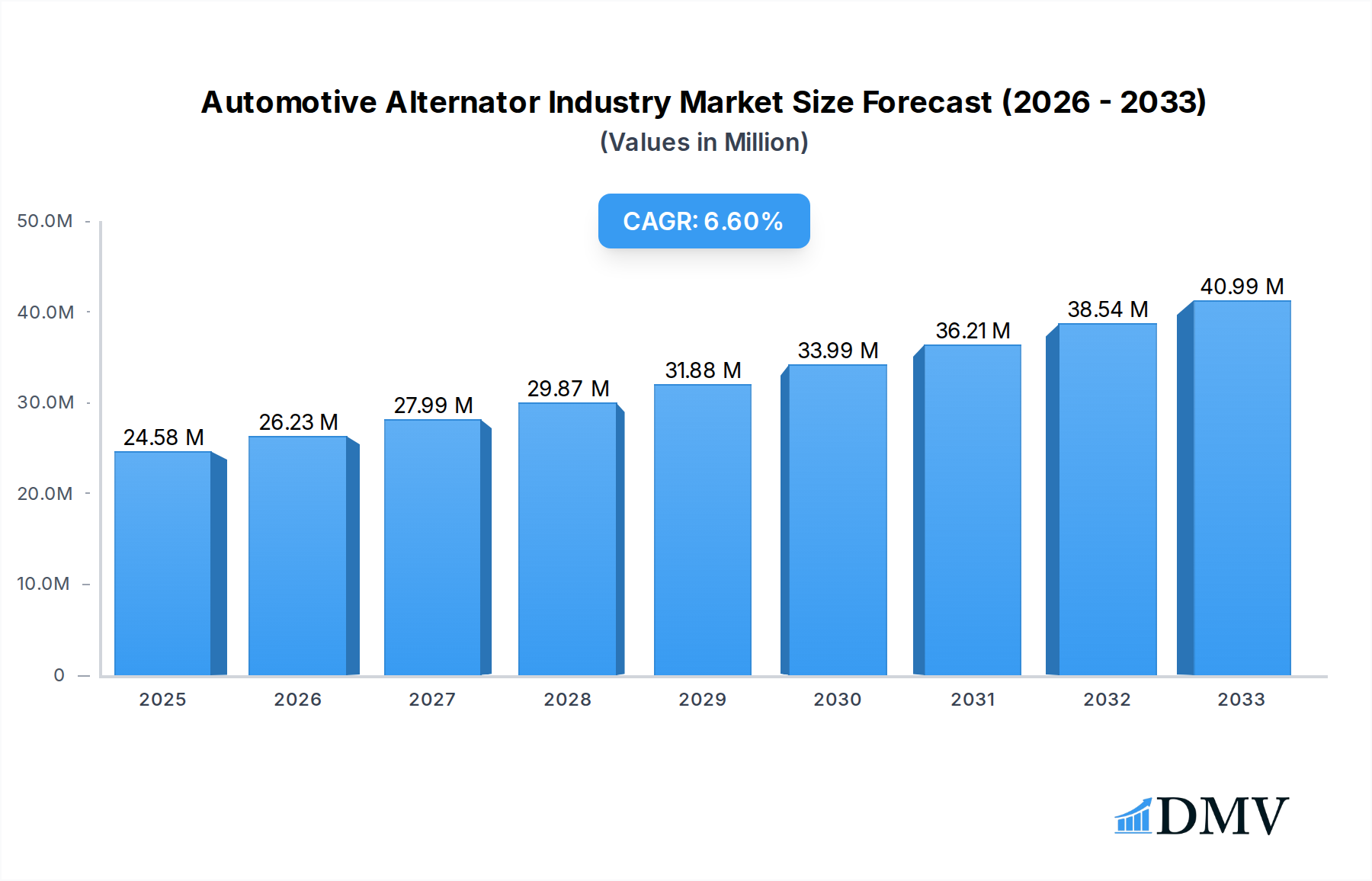

The global Automotive Alternator industry is projected to experience robust growth, with an estimated market size of $24.58 billion by 2025. This expansion is driven by a CAGR of 6.70% throughout the forecast period of 2019-2033, indicating sustained momentum in the market. A key driver for this growth is the increasing global vehicle production, particularly in emerging economies, coupled with the rising demand for advanced automotive features that require consistent and reliable electrical power. The ongoing technological advancements in alternators, focusing on improved efficiency, reduced weight, and enhanced durability, are also significantly contributing to market expansion. Furthermore, the growing adoption of hybrid and electric vehicles, which, while featuring batteries, still utilize alternators in their complex powertrains for charging and power management, presents a substantial opportunity for innovation and market penetration. The shift towards stricter emission regulations worldwide also indirectly supports the alternator market, as more efficient alternators contribute to better fuel economy and reduced emissions in internal combustion engine (ICE) vehicles.

Automotive Alternator Industry Market Size (In Million)

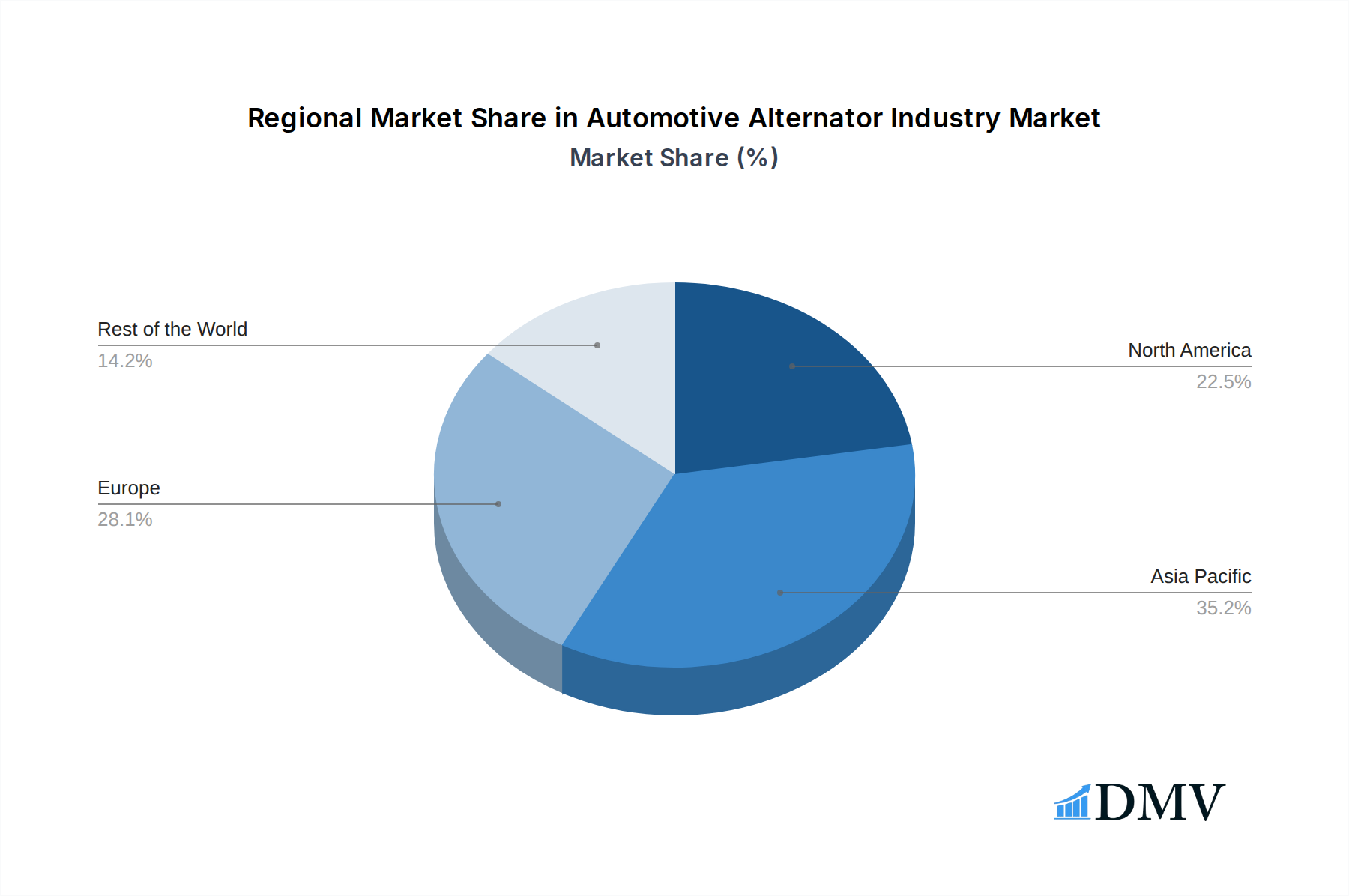

The market landscape is characterized by a dynamic segmentation across powertrains, vehicle types, and electrical phase configurations. While traditional IC engine vehicles continue to be a significant segment, the substantial growth in hybrid and electric vehicles is reshaping demand patterns. Passenger cars represent the largest vehicle type segment, but the commercial vehicle segment is also showing considerable expansion due to increasing logistics and transportation needs. In terms of electrical phase, both single-phase and three-phase alternators are crucial, with the latter gaining prominence in higher-power applications and advanced vehicle architectures. Key industry players, including Mitsubishi Corporation, Hitachi Automotive Systems Ltd, BorgWarner Inc, Tenneco Inc, Valeo, Robert Bosch GmbH, Hella KGaA Hueck & Co, Mecc Alt, DENSO Corporation, and Lucas Industries PLC, are actively investing in research and development to cater to these evolving market demands. Geographically, the Asia Pacific region, particularly China and India, is anticipated to be a major growth engine due to its massive automotive manufacturing base and burgeoning consumer market. North America and Europe also remain critical markets, driven by technological adoption and stringent quality standards.

Automotive Alternator Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Automotive Alternator Industry, a critical component in modern vehicle electrification and powertrain management. Spanning a study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this report offers invaluable insights for stakeholders navigating this dynamic market. We dissect market composition, industry evolution, regional dominance, product innovations, growth drivers, challenges, and future opportunities, culminating in a strategic market forecast.

Automotive Alternator Industry Market Composition & Trends

The Automotive Alternator Industry is characterized by a moderate level of market concentration, with key players like Robert Bosch GmbH, DENSO Corporation, and Valeo holding significant shares. Innovation remains a primary catalyst, driven by the relentless demand for enhanced fuel efficiency, reduced emissions, and the increasing integration of hybrid and electric vehicle (HEV) technologies. The regulatory landscape, particularly stringent emission standards across North America, Europe, and Asia Pacific, continues to shape product development and market entry. Substitute products, while present in niche applications, face significant barriers to widespread adoption due to the established reliability and cost-effectiveness of traditional alternators. End-user profiles are diversifying, encompassing not only passenger car manufacturers but also the rapidly expanding commercial vehicle sector. Mergers and acquisitions (M&A) activity has been steady, with deal values ranging from tens of millions to hundreds of millions of US dollars, reflecting strategic consolidation and technology acquisition. For instance, M&A deal values in the past year alone have been estimated to be in the range of $500 Million, underscoring the strategic importance of this sector.

- Market Share Distribution: Dominant players hold approximately 65% of the global market share.

- Innovation Focus: Development of lightweight, high-efficiency, and integrated starter-generator (ISG) alternators for mild-hybrid systems.

- Regulatory Impact: Increasing demand for alternators that support advanced start-stop systems and regenerative braking.

- M&A Drivers: Acquisition of specialized technologies in power electronics and advanced materials.

Automotive Alternator Industry Industry Evolution

The Automotive Alternator Industry has undergone a significant transformation, evolving from a simple power generation device to a sophisticated component integral to modern vehicle electrification strategies. The historical period (2019–2024) witnessed a steady market growth of approximately 3% CAGR, primarily driven by the robust demand for IC engine vehicles. However, the foundational year of 2025 marks a pivotal shift, with the projected growth rate accelerating to an estimated 5.5% CAGR during the forecast period (2025–2033). This acceleration is intrinsically linked to the burgeoning adoption of hybrid and electric vehicles, which, while introducing new powertrain architectures, still rely on alternator-like functionalities for battery management and auxiliary power in their hybrid variants. Technological advancements have been at the forefront of this evolution. The transition from single-phase to three-phase alternators has become standard for enhanced power output and efficiency, catering to the escalating electrical demands of modern vehicles. Furthermore, the development of advanced alternator technologies, such as integrated starter-generators (ISGs) and smart alternators with sophisticated control units, is becoming increasingly prevalent. These innovations not only improve fuel economy by enabling features like regenerative braking and extended start-stop capabilities but also contribute to a smoother and more responsive driving experience. Consumer demand is also playing a crucial role, with a growing preference for vehicles offering superior fuel efficiency and reduced environmental impact. This trend directly fuels the demand for advanced alternator systems that can optimize energy management and minimize parasitic losses. The industry is actively responding to these evolving demands by investing heavily in research and development, aiming to produce alternators that are lighter, more compact, and capable of higher power outputs while maintaining exceptional reliability and durability. The projected market size for alternators, including integrated systems, is expected to reach approximately $25 Billion by 2033.

Leading Regions, Countries, or Segments in Automotive Alternator Industry

The global Automotive Alternator Industry exhibits a pronounced regional and segmental dominance, driven by a confluence of factors including vehicle production volumes, technological adoption rates, and regulatory mandates. Asia Pacific, led by China and Japan, stands as the undisputed leader in terms of both production and consumption of automotive alternators. This dominance is underpinned by its position as the world's largest automotive manufacturing hub, catering to a massive domestic demand for passenger cars and an ever-increasing volume of commercial vehicles. The region's aggressive push towards vehicle electrification, particularly in China, further solidifies its leadership. Japan, with its pioneering role in hybrid vehicle technology, continues to be a significant market for advanced alternator systems.

Within the powertrain types, IC Engine Vehicles still constitute the largest segment, accounting for an estimated 70% of the total market demand. However, the Hybrid and Electric Vehicles segment is exhibiting the most dynamic growth, with a projected CAGR of over 12% during the forecast period. This surge is directly attributable to global efforts to reduce carbon emissions and government incentives promoting the adoption of greener mobility solutions.

In terms of vehicle types, Passenger Cars remain the predominant segment, driven by global sales volumes and the increasing sophistication of their electrical systems. However, the Commercial Vehicles segment is rapidly gaining traction, fueled by the growing need for enhanced power solutions in heavy-duty trucks, buses, and other specialized vehicles to support advanced onboard electronics and electrification initiatives.

The technological divide is also apparent, with Three Phase alternators increasingly dominating the market due to their superior efficiency and power output compared to Single Phase alternators, particularly in higher-end vehicles and HEVs.

Key Drivers in Asia Pacific:

- Massive Vehicle Production: China's unparalleled automotive manufacturing capacity.

- Electrification Mandates: Strong government support and targets for EV and HEV adoption.

- Technological Advancement: Leading role of Japanese manufacturers in hybrid technologies.

- Growing Middle Class: Increased demand for passenger cars with advanced features.

Dominance Factors for IC Engine Vehicles:

- Existing Fleet Size: A substantial global fleet of internal combustion engine vehicles necessitates ongoing replacement parts.

- Cost-Effectiveness: Traditional ICE vehicles and their components remain more affordable for a significant portion of the global market.

- Infrastructure: Established refueling and maintenance infrastructure supports ICE vehicles.

Growth Catalysts for Hybrid and Electric Vehicles Segment:

- Environmental Regulations: Stringent emission norms pushing manufacturers towards electrified powertrains.

- Consumer Awareness: Growing public concern for climate change and demand for sustainable transport.

- Government Incentives: Subsidies, tax credits, and preferential policies for EVs and HEVs.

- Technological Improvements: Advancements in battery technology and charging infrastructure.

Automotive Alternator Industry Product Innovations

Product innovation in the Automotive Alternator Industry is rapidly moving beyond basic power generation. Key advancements include the development of highly efficient, lightweight, and compact alternator designs, often integrating starter functions for mild-hybrid systems. These Integrated Starter-Generators (ISGs) offer enhanced fuel economy through regenerative braking and seamless start-stop functionality, significantly improving the driving experience. Performance metrics are seeing improvements with higher power outputs (up to 3 kW for advanced ISGs) and reduced energy losses. Unique selling propositions now revolve around intelligent control systems that optimize charging based on driving conditions and battery health, contributing to extended battery life and overall vehicle efficiency. The focus is on creating robust, reliable, and scalable solutions for both traditional internal combustion engine vehicles and next-generation electrified powertrains.

Propelling Factors for Automotive Alternator Industry Growth

The Automotive Alternator Industry is propelled by a dynamic interplay of technological advancements, economic imperatives, and regulatory pressures. The increasing sophistication of vehicle electrical systems, driven by infotainment, driver-assistance systems (ADAS), and connectivity features, demands higher alternator output and efficiency. The global push towards decarbonization and stringent emission standards is a paramount driver, compelling automakers to adopt more fuel-efficient technologies like start-stop systems and mild-hybrid powertrains, all of which rely on advanced alternators. Economic factors such as rising fuel prices also encourage consumers to seek out vehicles with better fuel economy, indirectly boosting the demand for efficient alternator solutions. For example, government mandates in Europe and Asia Pacific for fleet-wide CO2 emission reductions directly incentivize the adoption of technologies that utilize advanced alternators. The market is also benefiting from ongoing innovation in materials science, leading to lighter and more durable alternator components.

Obstacles in the Automotive Alternator Industry Market

Despite robust growth prospects, the Automotive Alternator Industry faces several significant obstacles. The primary challenge stems from the long-term transition towards fully electric vehicles (BEVs), which, by design, do not require traditional alternators. This presents a gradual but inevitable decline in demand for conventional alternators in the distant future. Supply chain disruptions, as evidenced by recent global events, can lead to material shortages and increased manufacturing costs, impacting production volumes and pricing. Furthermore, intense price competition among manufacturers, particularly in mature markets, can squeeze profit margins and necessitate continuous cost optimization. Evolving regulatory landscapes can also pose challenges, requiring significant investment in R&D to meet new standards, and the high cost of advanced technology development can be a barrier for smaller players.

Future Opportunities in Automotive Alternator Industry

The Automotive Alternator Industry is ripe with emerging opportunities, primarily driven by the continued growth of hybrid vehicle technology and the demand for sophisticated power management solutions in traditional vehicles. The expansion of mild-hybrid systems, which offer a cost-effective path to improved fuel efficiency, presents a significant growth avenue. As vehicle electrification progresses, there will be a sustained need for advanced alternator-like components in hybrid powertrains for many years to come. Furthermore, the increasing complexity of vehicle electronics, from advanced driver-assistance systems (ADAS) to sophisticated infotainment and connectivity features, necessitates higher power output and more intelligent charging solutions, creating opportunities for upgraded and specialized alternators. The aftermarket segment also offers a steady stream of opportunities as existing vehicle fleets require replacement parts. The development of more efficient and robust alternators for commercial vehicles, which have a higher power demand, is another promising area.

Major Players in the Automotive Alternator Industry Ecosystem

- Mitsubishi Corporation

- Hitachi Automotive Systems Ltd

- BorgWarner Inc

- Tenneco Inc

- Valeo

- Robert Bosch GmbH

- Hella KGaA Hueck & Co

- Mecc Alt

- DENSO Corporation

- Lucas Industries PLC

Key Developments in Automotive Alternator Industry Industry

- 2023 Q4: Valeo launches a new generation of high-efficiency alternators for passenger cars, improving fuel economy by up to 3%.

- 2023 Q3: Hitachi Automotive Systems Ltd announces a strategic partnership with a leading battery manufacturer to develop integrated power solutions for hybrid vehicles.

- 2023 Q2: Robert Bosch GmbH unveils an advanced starter-generator system offering improved performance and reduced emissions for mild-hybrid applications.

- 2023 Q1: DENSO Corporation expands its alternator production capacity in Southeast Asia to meet growing regional demand.

- 2022 Q4: BorgWarner Inc acquires a company specializing in advanced power electronics for automotive applications, strengthening its electrification portfolio.

- 2022 Q3: Mecc Alt introduces a new line of robust alternators designed for demanding commercial vehicle applications.

- 2022 Q2: Hella KGaA Hueck & Co develops a smart alternator control unit that optimizes battery charging and enhances vehicle efficiency.

- 2022 Q1: Tenneco Inc announces significant investments in R&D for next-generation emission control and powertrain components, including advanced alternators.

- 2021 Q4: Lucas Industries PLC focuses on modernizing its aftermarket alternator offerings to cater to newer vehicle models.

Strategic Automotive Alternator Industry Market Forecast

The strategic outlook for the Automotive Alternator Industry remains positive, particularly in the medium term, driven by the sustained demand for hybrid vehicle technologies and the increasing electrical loads in conventional vehicles. While the long-term trajectory will be influenced by the pace of full electrification, the current market dynamics present significant growth catalysts. The continuous evolution of alternator technology towards higher efficiency, lighter weight, and integrated functionalities will be key to capturing market share. Strategic investments in R&D, particularly in areas like advanced materials and intelligent control systems, will be crucial for players to maintain a competitive edge. The expanding commercial vehicle segment and the growing aftermarket also offer considerable potential. Therefore, the market is poised for continued expansion, driven by innovation and the evolving needs of the automotive landscape, with an estimated market size of approximately $22 Billion in 2025, projected to reach $25 Billion by 2033.

Automotive Alternator Industry Segmentation

-

1. Powertrain Type

- 1.1. IC Engine Vehicles

- 1.2. Hybrid and Electric Vehicles

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

-

3. Type

- 3.1. Single Phase

- 3.2. Three Phase

Automotive Alternator Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Asia Pacific

- 2.1. China

- 2.2. Japan

- 2.3. India

- 2.4. South Korea

- 2.5. Rest of Asia Pacific

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. Brazil

- 4.2. Saudi Arabia

- 4.3. Other Countries

Automotive Alternator Industry Regional Market Share

Geographic Coverage of Automotive Alternator Industry

Automotive Alternator Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 5.1.1. IC Engine Vehicles

- 5.1.2. Hybrid and Electric Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Type

- 5.3.1. Single Phase

- 5.3.2. Three Phase

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Asia Pacific

- 5.4.3. Europe

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 6. Global Automotive Alternator Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 6.1.1. IC Engine Vehicles

- 6.1.2. Hybrid and Electric Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Type

- 6.3.1. Single Phase

- 6.3.2. Three Phase

- 6.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 7. North America Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 7.1.1. IC Engine Vehicles

- 7.1.2. Hybrid and Electric Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.3. Market Analysis, Insights and Forecast - by Type

- 7.3.1. Single Phase

- 7.3.2. Three Phase

- 7.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 8. Asia Pacific Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 8.1.1. IC Engine Vehicles

- 8.1.2. Hybrid and Electric Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.3. Market Analysis, Insights and Forecast - by Type

- 8.3.1. Single Phase

- 8.3.2. Three Phase

- 8.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 9. Europe Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 9.1.1. IC Engine Vehicles

- 9.1.2. Hybrid and Electric Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.3. Market Analysis, Insights and Forecast - by Type

- 9.3.1. Single Phase

- 9.3.2. Three Phase

- 9.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 10. Rest of the World Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 10.1.1. IC Engine Vehicles

- 10.1.2. Hybrid and Electric Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.3. Market Analysis, Insights and Forecast - by Type

- 10.3.1. Single Phase

- 10.3.2. Three Phase

- 10.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Mitsubishi Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Hitachi Automotive Systems Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 BorgWarner Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Tenneco Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Valeo

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Robert Bosch GmbH

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Hella KGaA Hueck & Co

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Mecc Alt

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 DENSO Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Lucas Industries PLC

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Mitsubishi Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Alternator Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 3: North America Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 4: North America Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 5: North America Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 7: North America Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: North America Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 11: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 12: Asia Pacific Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 13: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 14: Asia Pacific Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 19: Europe Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 20: Europe Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 21: Europe Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 22: Europe Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 23: Europe Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 24: Europe Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 27: Rest of the World Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 28: Rest of the World Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 29: Rest of the World Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 30: Rest of the World Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 31: Rest of the World Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 32: Rest of the World Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 2: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Automotive Alternator Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 6: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 7: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of North America Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 14: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 15: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 16: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: China Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Japan Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: India Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: South Korea Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 23: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 24: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 25: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Germany Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: France Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Italy Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 32: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 33: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: Brazil Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Saudi Arabia Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Other Countries Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Alternator Industry?

The projected CAGR is approximately 6.70%.

2. Which companies are prominent players in the Automotive Alternator Industry?

Key companies in the market include Mitsubishi Corporation, Hitachi Automotive Systems Ltd, BorgWarner Inc, Tenneco Inc, Valeo, Robert Bosch GmbH, Hella KGaA Hueck & Co, Mecc Alt, DENSO Corporation, Lucas Industries PLC.

3. What are the main segments of the Automotive Alternator Industry?

The market segments include Powertrain Type, Vehicle Type, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.58 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Production.

6. What are the notable trends driving market growth?

Passenger Car Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Shift Towards Electric powertrain.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Alternator Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Alternator Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Alternator Industry?

To stay informed about further developments, trends, and reports in the Automotive Alternator Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence