Key Insights

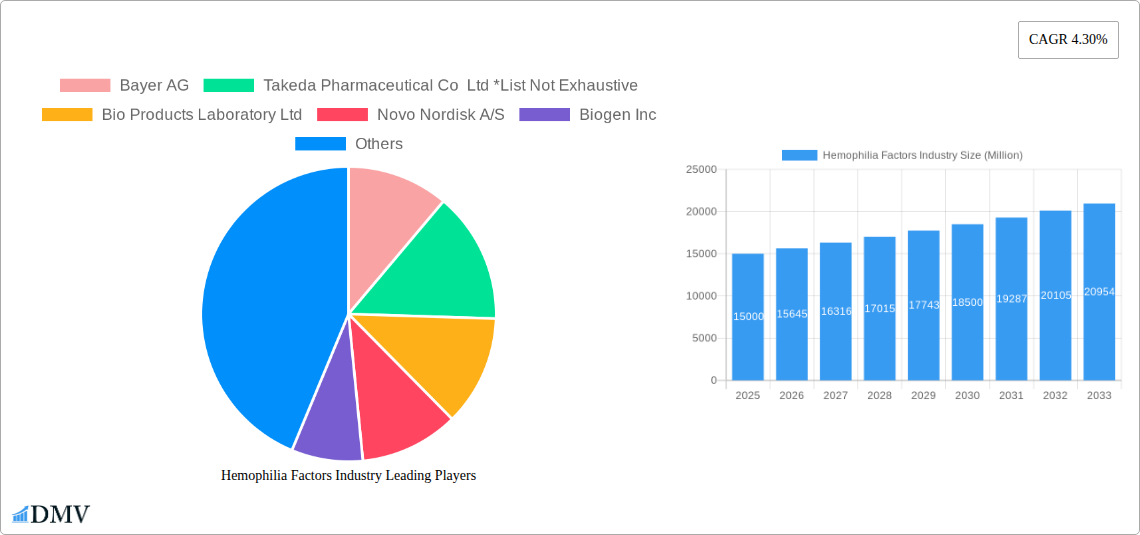

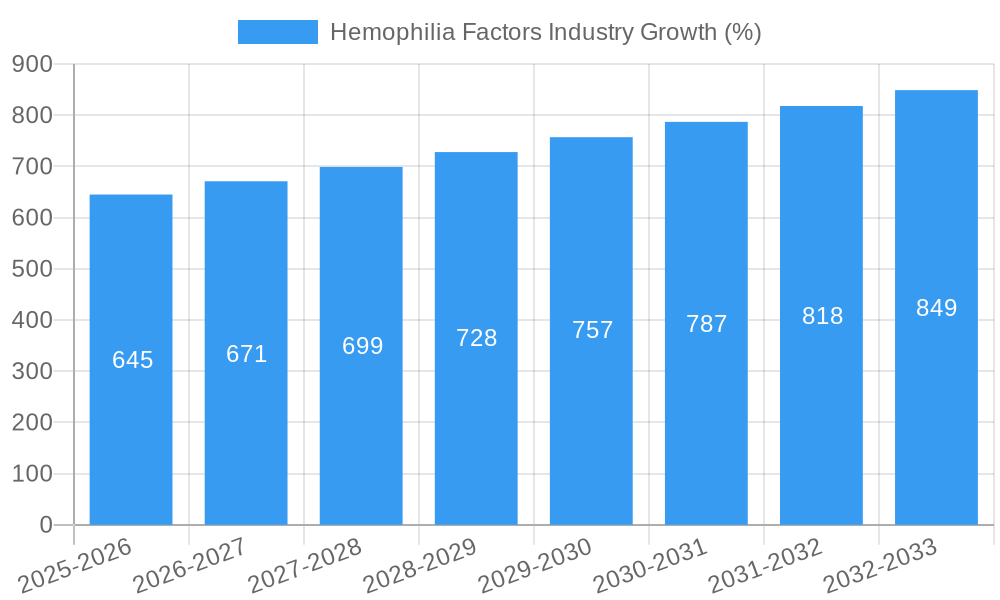

The Hemophilia Factors market, valued at approximately $15 billion in 2025, is projected to experience robust growth, driven by increasing prevalence of hemophilia, advancements in treatment modalities, and rising healthcare expenditure globally. A compound annual growth rate (CAGR) of 4.30% from 2025 to 2033 signifies a significant expansion in market size, reaching an estimated $22 billion by 2033. This growth is fueled by the increasing availability and adoption of Factor VIII and IX concentrates, along with the development of novel therapies offering improved efficacy and convenience. The market is segmented by treatment type, with Factor Concentrate holding the largest market share due to its established efficacy and widespread usage. However, the segments for Fresh Frozen Plasma (FFP) and Cryoprecipitate are anticipated to witness moderate growth driven by their cost-effectiveness in certain treatment scenarios. Geographical expansion, particularly in emerging markets with rising awareness and improved healthcare infrastructure, will further contribute to market expansion. However, factors such as high treatment costs, stringent regulatory approvals for new therapies, and potential side effects associated with some treatments could pose challenges to sustained market growth.

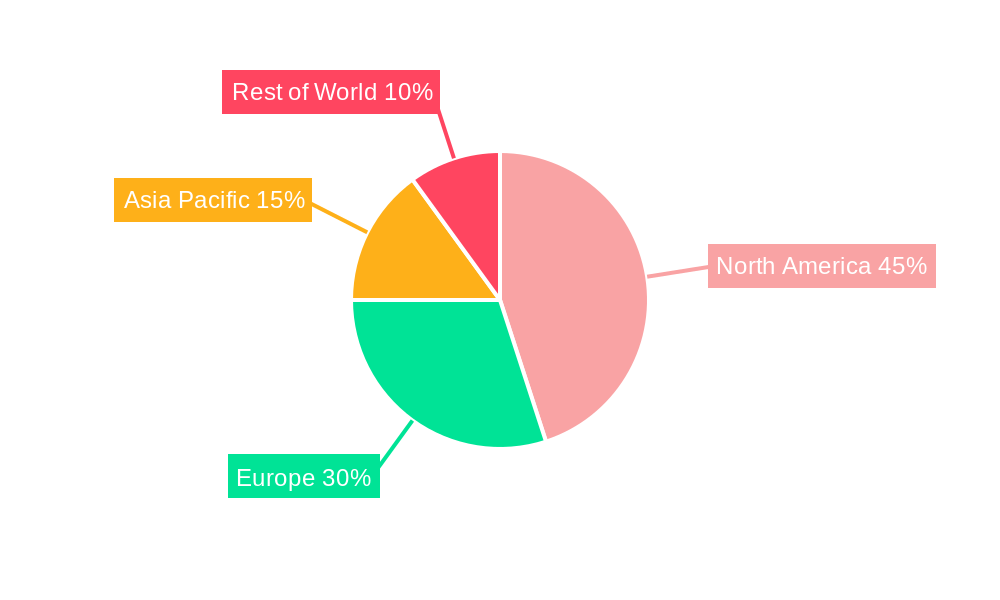

The competitive landscape is highly consolidated, with leading pharmaceutical companies such as Bayer AG, Takeda Pharmaceutical, and Biogen Inc. dominating the market. These key players are actively involved in research and development, strategic acquisitions, and partnerships to strengthen their market position and expand their product portfolios. The focus is on developing next-generation therapies with improved safety profiles and longer half-lives, enhancing patient compliance and reducing the frequency of infusions. Furthermore, the increasing focus on personalized medicine and the development of targeted therapies hold significant promise for improving treatment outcomes and driving further market growth in the future. Regional variations in market growth are expected, with North America and Europe holding significant shares due to established healthcare systems and higher disease prevalence, while the Asia Pacific region shows promising growth potential, driven by rising disposable incomes and increasing awareness about hemophilia.

Hemophilia Factors Industry: Market Analysis & Forecast Report (2019-2033)

This comprehensive report provides an in-depth analysis of the global Hemophilia Factors industry, encompassing market size, growth trajectories, competitive landscape, and future opportunities. The study period covers 2019-2033, with 2025 as the base and estimated year. This report is crucial for stakeholders seeking to understand the dynamics of this vital sector within the healthcare industry. The global market is expected to reach xx Million by 2033.

Hemophilia Factors Industry Market Composition & Trends

The Hemophilia Factors market is characterized by a moderately concentrated landscape, with key players such as Bayer AG, Takeda Pharmaceutical Co Ltd, Bio Products Laboratory Ltd, Novo Nordisk A/S, Biogen Inc, Baxter International Inc, CSL Behring, and Pfizer Inc holding significant market shares. Precise market share distribution for 2025 is currently under analysis but preliminary data suggests a combined market share of approximately 60% for the top four players. Innovation is a key driver, fueled by advancements in recombinant factor concentrates and extended half-life therapies. The regulatory landscape, particularly in developed markets like the US and Europe, significantly influences market access and pricing. Substitute products are limited, largely confined to specific treatment scenarios or patient populations. End-users predominantly comprise hospitals, specialized hemophilia treatment centers, and blood banks. The market has witnessed several M&A activities in recent years, with deal values ranging from tens to hundreds of Millions depending on the scale and target companies involved.

- Market Concentration: Moderately concentrated, with top players controlling a significant share (approximated 60% in 2025 for top four).

- Innovation Catalysts: Recombinant factor concentrates, extended half-life therapies, gene therapy.

- Regulatory Landscape: Stringent approvals and pricing regulations influence market access.

- Substitute Products: Limited availability; generally used in specific treatment scenarios only.

- End-User Profile: Hospitals, hemophilia treatment centers, blood banks.

- M&A Activities: Ongoing consolidations and acquisitions with deal values ranging from tens to hundreds of Millions.

Hemophilia Factors Industry Evolution

The Hemophilia Factors market has witnessed consistent growth during the historical period (2019-2024), driven by increasing prevalence of hemophilia, rising awareness, and technological advancements. The Compound Annual Growth Rate (CAGR) from 2019 to 2024 is estimated to be around xx%. This growth is projected to continue during the forecast period (2025-2033), albeit at a potentially slightly moderated rate, influenced by factors such as increasing competition and pricing pressures. Technological advancements, particularly in the development of extended half-life therapies and gene therapies, are transforming the treatment landscape. Consumer demand is shifting towards more convenient and effective treatment options, including therapies that reduce the frequency of infusions. Adoption of new therapies is gradual but steadily increasing, particularly in high-income nations. By 2033, the adoption rate of extended half-life therapies is estimated to reach xx%, while gene therapy adoption may be around xx% , both estimates based on current clinical trial data and technological projections.

Leading Regions, Countries, or Segments in Hemophilia Factors Industry

North America currently dominates the Hemophilia Factors market, driven by high healthcare expenditure, advanced healthcare infrastructure, and a significant patient population. Within the treatment segments, Factor Concentrates hold the largest market share, primarily due to their established efficacy and widespread availability.

Key Drivers in North America:

- High healthcare expenditure and insurance coverage

- Advanced healthcare infrastructure and access to specialized treatments

- Significant patient population and high prevalence of hemophilia

- Strong regulatory support and robust clinical trial infrastructure

Dominance Factors:

- High prevalence of hemophilia: A significant patient population fuels demand.

- Established healthcare infrastructure: Efficient healthcare systems ensure accessibility and delivery.

- High per-capita healthcare spending: High purchasing power in this region drives market expansion.

- Strong regulatory support: Favourable regulations facilitate market entry and market growth.

Hemophilia Factors Industry Product Innovations

Recent innovations include the development of extended half-life factor concentrates, reducing the frequency of infusions and improving patient compliance. Gene therapy holds immense potential for long-term disease modification, although it's still in earlier stages of commercialization. Novel delivery systems and formulation technologies aim to enhance treatment efficacy and reduce adverse events. These innovations offer unique selling propositions by improving treatment convenience and effectiveness, leading to superior patient outcomes.

Propelling Factors for Hemophilia Factors Industry Growth

Technological advancements like the development of extended half-life therapies and gene therapies are key drivers, offering improved efficacy and convenience. Increasing awareness and diagnosis rates, coupled with rising healthcare expenditure globally, contribute to market expansion. Supportive regulatory frameworks and favorable reimbursement policies further fuel growth.

Obstacles in the Hemophilia Factors Industry Market

High cost of treatment, particularly for newer therapies, poses a significant barrier for access. Supply chain disruptions, especially for raw materials, can impact production and availability. Intense competition among established players can exert downward pressure on prices and profit margins. Regulatory hurdles and lengthy approval processes can delay product launches.

Future Opportunities in Hemophilia Factors Industry

Expansion into emerging markets with high unmet needs presents significant opportunities. The development of next-generation therapies, including gene editing and novel delivery systems, offers further growth potential. Focusing on personalized medicine and predictive analytics to tailor treatment strategies can enhance market value.

Major Players in the Hemophilia Factors Industry Ecosystem

- Bayer AG

- Takeda Pharmaceutical Co Ltd

- Bio Products Laboratory Ltd

- Novo Nordisk A/S

- Biogen Inc

- Baxter International Inc

- CSL Behring

- Pfizer Inc

Key Developments in Hemophilia Factors Industry Industry

- June 2022: FDA grants breakthrough therapy designation to efanesoctocog alfa for hemophilia A.

- May 2022: Takeda launches Adynovate, an extended half-life recombinant Factor VIII treatment in India.

Strategic Hemophilia Factors Industry Market Forecast

The Hemophilia Factors market is poised for sustained growth driven by continuous technological innovation, expanding patient populations, and supportive regulatory environments. The focus on developing more convenient and effective therapies, coupled with improved access in emerging markets, will contribute to significant market expansion throughout the forecast period. Emerging gene therapies and personalized medicine approaches further enhance the long-term growth potential of the industry.

Hemophilia Factors Industry Segmentation

-

1. Treatment

- 1.1. Factor Concentrate

- 1.2. Fresh Frozen Plasma (FFP)

- 1.3. Cryoprecipitate

- 1.4. Others

Hemophilia Factors Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Hemophilia Factors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Adoption and Approval of New Treatment Techniques; Growing Number of Government Initiatives and Funding

- 3.3. Market Restrains

- 3.3.1. High Cost of Treatment

- 3.4. Market Trends

- 3.4.1. Fresh Frozen Plasma (FFP) is Expected to Hold Significant Market Share in the Treatment Segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Treatment

- 5.1.1. Factor Concentrate

- 5.1.2. Fresh Frozen Plasma (FFP)

- 5.1.3. Cryoprecipitate

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East and Africa

- 5.2.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Treatment

- 6. North America Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Treatment

- 6.1.1. Factor Concentrate

- 6.1.2. Fresh Frozen Plasma (FFP)

- 6.1.3. Cryoprecipitate

- 6.1.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Treatment

- 7. Europe Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Treatment

- 7.1.1. Factor Concentrate

- 7.1.2. Fresh Frozen Plasma (FFP)

- 7.1.3. Cryoprecipitate

- 7.1.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Treatment

- 8. Asia Pacific Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Treatment

- 8.1.1. Factor Concentrate

- 8.1.2. Fresh Frozen Plasma (FFP)

- 8.1.3. Cryoprecipitate

- 8.1.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Treatment

- 9. Middle East and Africa Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Treatment

- 9.1.1. Factor Concentrate

- 9.1.2. Fresh Frozen Plasma (FFP)

- 9.1.3. Cryoprecipitate

- 9.1.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Treatment

- 10. South America Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Treatment

- 10.1.1. Factor Concentrate

- 10.1.2. Fresh Frozen Plasma (FFP)

- 10.1.3. Cryoprecipitate

- 10.1.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Treatment

- 11. North America Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America Hemophilia Factors Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Bayer AG

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Takeda Pharmaceutical Co Ltd *List Not Exhaustive

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Bio Products Laboratory Ltd

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Novo Nordisk A/S

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Biogen Inc

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Baxter International Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 CSL Behring

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Pfizer Inc

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.1 Bayer AG

List of Figures

- Figure 1: Global Hemophilia Factors Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Hemophilia Factors Industry Revenue (Million), by Treatment 2024 & 2032

- Figure 13: North America Hemophilia Factors Industry Revenue Share (%), by Treatment 2024 & 2032

- Figure 14: North America Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: North America Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Hemophilia Factors Industry Revenue (Million), by Treatment 2024 & 2032

- Figure 17: Europe Hemophilia Factors Industry Revenue Share (%), by Treatment 2024 & 2032

- Figure 18: Europe Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: Europe Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific Hemophilia Factors Industry Revenue (Million), by Treatment 2024 & 2032

- Figure 21: Asia Pacific Hemophilia Factors Industry Revenue Share (%), by Treatment 2024 & 2032

- Figure 22: Asia Pacific Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Asia Pacific Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Middle East and Africa Hemophilia Factors Industry Revenue (Million), by Treatment 2024 & 2032

- Figure 25: Middle East and Africa Hemophilia Factors Industry Revenue Share (%), by Treatment 2024 & 2032

- Figure 26: Middle East and Africa Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Middle East and Africa Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: South America Hemophilia Factors Industry Revenue (Million), by Treatment 2024 & 2032

- Figure 29: South America Hemophilia Factors Industry Revenue Share (%), by Treatment 2024 & 2032

- Figure 30: South America Hemophilia Factors Industry Revenue (Million), by Country 2024 & 2032

- Figure 31: South America Hemophilia Factors Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Hemophilia Factors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Hemophilia Factors Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 3: Global Hemophilia Factors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: United States Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Canada Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Mexico Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Germany Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: France Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Italy Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Spain Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Europe Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: China Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Japan Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: India Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Australia Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: South Korea Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Rest of Asia Pacific Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: GCC Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: South Africa Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Rest of Middle East and Africa Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Brazil Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Argentina Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Rest of South America Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Global Hemophilia Factors Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 31: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: United States Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Canada Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Mexico Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Global Hemophilia Factors Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 36: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 37: Germany Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: United Kingdom Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: France Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Italy Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Spain Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Rest of Europe Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Global Hemophilia Factors Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 44: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 45: China Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Japan Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: India Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Australia Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: South Korea Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Asia Pacific Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global Hemophilia Factors Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 52: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 53: GCC Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: South Africa Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Rest of Middle East and Africa Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Global Hemophilia Factors Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 57: Global Hemophilia Factors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: Brazil Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: Argentina Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Rest of South America Hemophilia Factors Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hemophilia Factors Industry?

The projected CAGR is approximately 4.30%.

2. Which companies are prominent players in the Hemophilia Factors Industry?

Key companies in the market include Bayer AG, Takeda Pharmaceutical Co Ltd *List Not Exhaustive, Bio Products Laboratory Ltd, Novo Nordisk A/S, Biogen Inc, Baxter International Inc, CSL Behring, Pfizer Inc.

3. What are the main segments of the Hemophilia Factors Industry?

The market segments include Treatment.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Adoption and Approval of New Treatment Techniques; Growing Number of Government Initiatives and Funding.

6. What are the notable trends driving market growth?

Fresh Frozen Plasma (FFP) is Expected to Hold Significant Market Share in the Treatment Segment.

7. Are there any restraints impacting market growth?

High Cost of Treatment.

8. Can you provide examples of recent developments in the market?

In June 2022, the United States Food and Drug Administration granted breakthrough therapy designation to 'efanesoctocog alfa' for hemophilia A.Efanesoctocog alfa is the first factor VIII therapy to be awarded Breakthrough Therapy designation by the FDA. This designation is based on XTEND-1 Phase 3 study data demonstrating clinically meaningful prevention of bleeds and superiority in the prevention of bleeding episodes compared to prior prophylaxis factor treatment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hemophilia Factors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hemophilia Factors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hemophilia Factors Industry?

To stay informed about further developments, trends, and reports in the Hemophilia Factors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence