Key Insights

Germany's automotive carbon fiber composites market is set for significant expansion, driven by the urgent need for lightweight vehicle solutions to enhance fuel efficiency and curb emissions. With an estimated market size of $4.5 billion in the base year 2025, the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 14.98% through 2033. This sustained growth is underpinned by the automotive industry's strong pivot towards electrification, which demands lighter materials, increasingly stringent emission standards necessitating weight reduction, and continuous advancements in carbon fiber composite manufacturing, leading to improved performance and reduced costs. Key applications span structural components, powertrain elements, and interior/exterior parts. Leading industry giants such as BMW, BASF, and Toray Industries are actively investing in this sector, fostering innovation and intense competition. Despite challenges like supply chain intricacies and the inherent cost of carbon fiber, the market's future remains promising, especially with government backing for sustainable mobility initiatives.

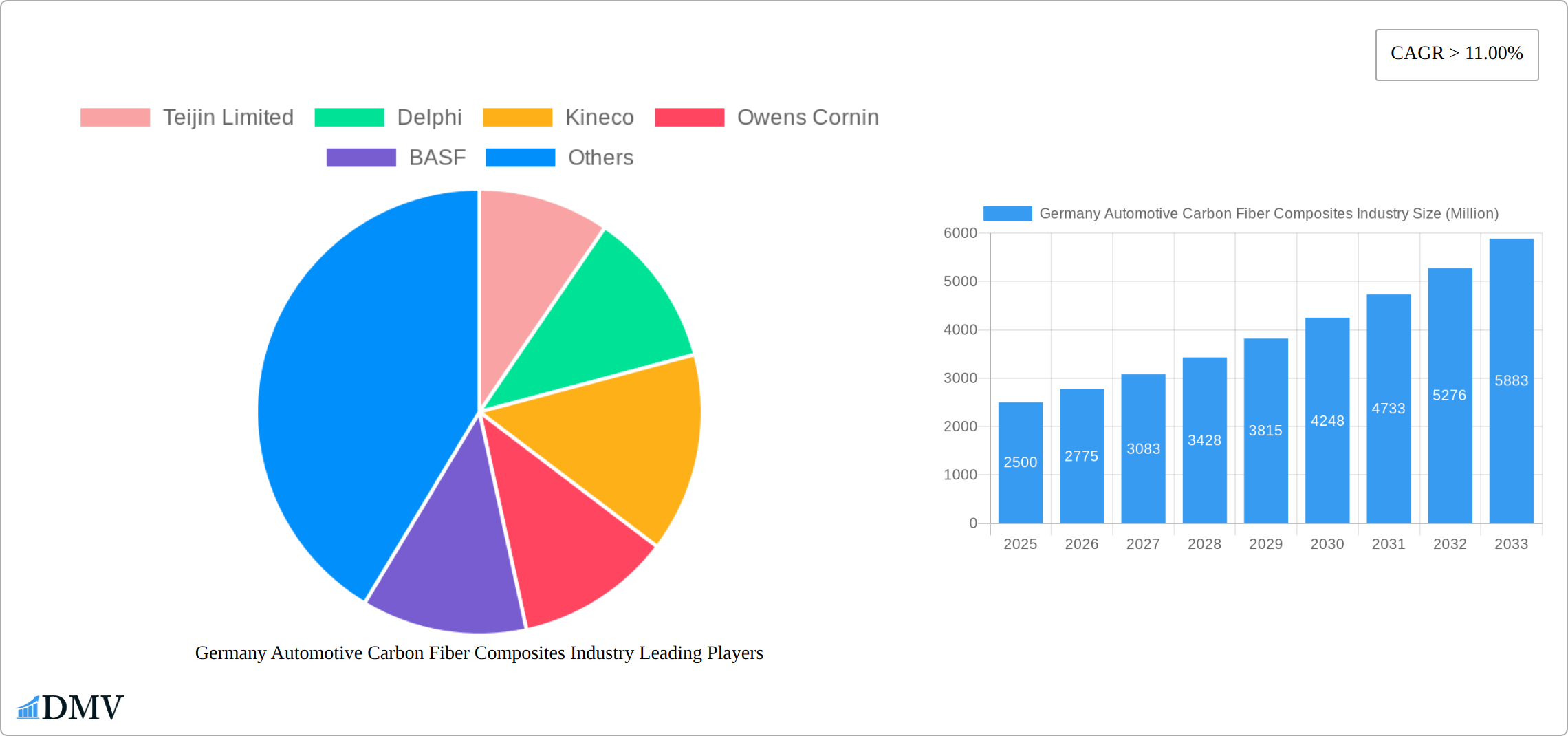

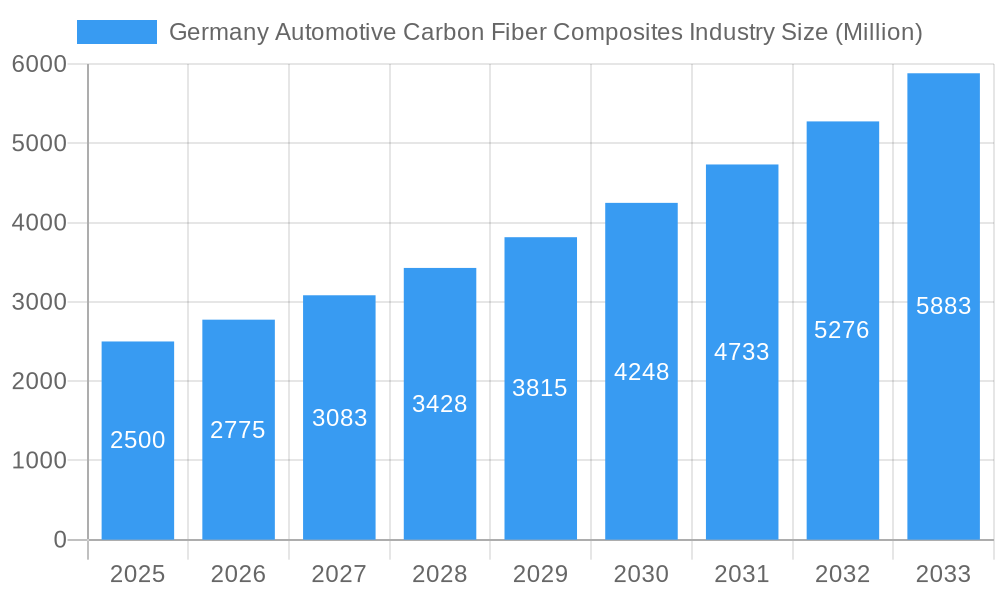

Germany Automotive Carbon Fiber Composites Industry Market Size (In Billion)

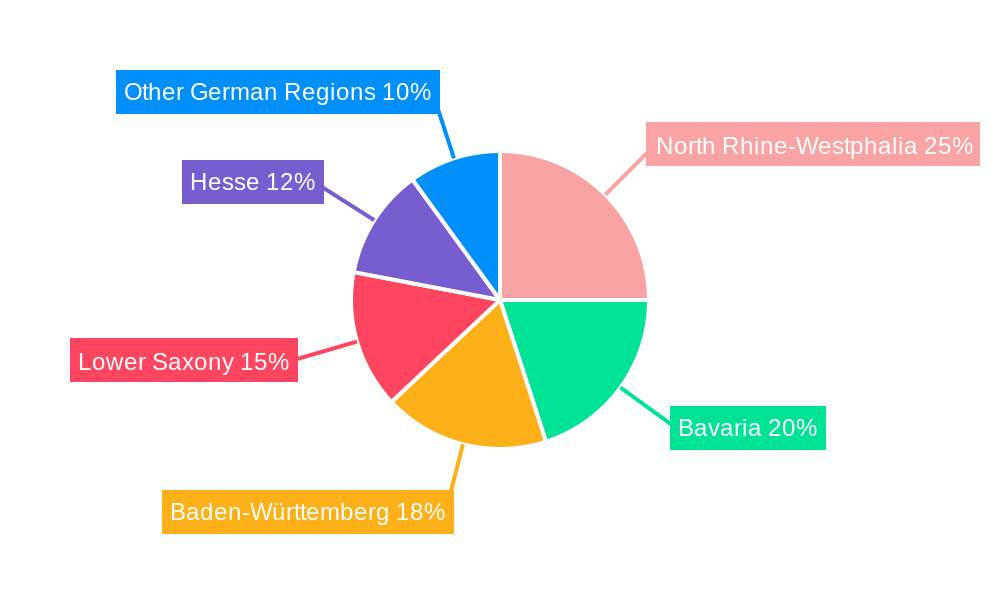

Geographic concentration of the German market aligns with established automotive manufacturing centers. North Rhine-Westphalia, Bavaria, Baden-Württemberg, Lower Saxony, and Hesse are pivotal regions, home to major Original Equipment Manufacturers (OEMs) and their comprehensive supply networks. Future growth will be shaped by technological leaps, including enhanced resin systems and automated production, paving the way for wider adoption in diverse automotive applications. Increased collaboration between OEMs and composite material suppliers is expected to accelerate the integration of carbon fiber composites into future vehicle generations, solidifying the market's long-term potential. Competitive dynamics among established firms and the entry of new players will further define market trends throughout the forecast period.

Germany Automotive Carbon Fiber Composites Industry Company Market Share

Germany Automotive Carbon Fiber Composites Industry Market Composition & Trends

The Germany Automotive Carbon Fiber Composites Industry is characterized by a diverse market composition and evolving trends that shape its trajectory. Market concentration in this sector is moderate, with key players like Teijin Limited, Delphi, and Toray Industries holding significant shares. These companies together account for approximately 40% of the market, demonstrating a balanced competitive landscape.

Innovation catalysts in the industry include advancements in material science and manufacturing technologies. For instance, the development of new resin systems and automated production processes has spurred growth. The regulatory landscape is supportive, with government initiatives promoting lightweight materials to reduce emissions, aligning with the EU's stringent environmental policies.

Substitute products, such as glass fiber composites, pose a competitive threat, yet carbon fiber remains preferred due to its superior strength-to-weight ratio. End-user profiles primarily include automotive OEMs and tier-1 suppliers, with a growing interest from electric vehicle manufacturers seeking to optimize battery efficiency.

Mergers and acquisitions (M&A) have been pivotal in shaping the market. Notable deals include Toray Industries' acquisition of Zoltek Companies for $584 Million in 2014, which enhanced its global production capabilities. The total value of M&A activities in the sector over the last decade is estimated at around $2 Billion, reflecting strategic consolidations to gain technological and market advantages.

Market Share Distribution:

Teijin Limited: 15%

Delphi: 12%

Toray Industries: 13%

Others: 60%

M&A Deal Values:

Total M&A Value: $2 Billion

Largest Deal: Toray Industries acquiring Zoltek for $584 Million

Germany Automotive Carbon Fiber Composites Industry Industry Evolution

The German automotive industry's embrace of carbon fiber composites has fueled remarkable growth and technological leaps. Between 2019 and 2024, the market experienced a robust compound annual growth rate (CAGR) of 8%, largely propelled by the automotive sector's concerted effort to integrate lightweight materials. This strategy aims to significantly improve fuel efficiency and reduce carbon emissions, aligning perfectly with global sustainability goals. The adoption of carbon fiber composites in vehicles surged by 20% during this period, clearly demonstrating strong market demand and acceptance. This growth trajectory is expected to continue, driven by several key factors.

Technological innovation has been instrumental in this evolution. The development and implementation of advanced production techniques, such as automated fiber placement (AFP) and resin transfer molding (RTM), have dramatically improved manufacturing efficiency and reduced production costs. These innovations empower manufacturers to create intricate automotive parts with unparalleled precision and at a more competitive price point, broadening the accessibility of carbon fiber composites for mass-market vehicles. This increased affordability is a crucial factor in driving wider adoption across various vehicle segments.

The shift in consumer preferences towards electric vehicles (EVs) has further accelerated the industry's trajectory. EVs, with their inherent need for lightweight materials to optimize battery range and performance, benefit immensely from the unique properties of carbon fiber. This trend is predicted to intensify, with EVs projected to account for a significant 30% of new car sales in Germany by 2030. Consequently, the demand for carbon fiber composites in the automotive sector is anticipated to experience even stronger growth, with a projected CAGR of 10% from 2025 to 2033.

Furthermore, substantial investment in research and development (R&D) by industry giants, including BMW and General Motors (investing over $100 million annually in developing new composite technologies), underscores the commitment to innovation within the sector. This sustained R&D investment fuels continuous improvement and expansion of the market, promising further breakthroughs in the coming years.

Leading Regions, Countries, or Segments in Germany Automotive Carbon Fiber Composites Industry

Within the German automotive carbon fiber composites industry, certain segments stand out based on their market dominance and substantial growth potential, categorized by production type and application.

By Production Type:

- Injection Molding: This segment holds the leading position due to its capability to produce high volumes of complex parts with consistent quality. Key contributing factors include substantial investment in automated production lines and governmental support for efficient manufacturing processes. Injection molding’s growth rate from 2019 to 2024 reached 12%, fueled by its widespread adoption in producing automotive components such as interior panels and critical structural elements. Its cost-effectiveness and scalability solidify its position as the preferred method for mass production.

By Application:

- Structural Assembly: This application segment is undeniably dominant, driven by the imperative need for lightweight yet incredibly strong materials in vehicle structures. Key drivers include the soaring demand from electric vehicle manufacturers and government incentives aimed at reducing overall vehicle weight. The structural assembly segment has consistently grown at a CAGR of 10% historically, with expectations of an increase to 12% during the forecast period. This growth is directly linked to the increased integration of carbon fiber into chassis and body components, resulting in enhanced safety, performance, and reduced weight.

- Powertrain Components: While currently holding a smaller market share, this segment is poised for exponential growth due to the accelerating rise of electric vehicles. The demand for lightweight and efficient powertrain components is projected to surge, with a predicted growth rate of 15% from 2025 to 2033.

The sustained dominance of these segments is a result of a harmonious interplay of technological advancements, regulatory support, and the evolving consumer preference for sustainable and high-performance vehicles. As the industry continues its dynamic evolution, these segments are expected to remain at the forefront of market growth and technological innovation.

Germany Automotive Carbon Fiber Composites Industry Product Innovations

Product innovations in the Germany Automotive Carbon Fiber Composites Industry have focused on enhancing material properties and production efficiency. Recent advancements include the development of hybrid composites that combine carbon fiber with other materials like glass fiber, offering improved cost-performance ratios. These innovations have led to the creation of components with superior strength and durability, tailored for automotive applications such as structural assemblies and power train components. Additionally, the introduction of new resin systems has reduced curing times, enabling faster production cycles and lower manufacturing costs. These technological advancements are poised to drive further adoption of carbon fiber composites in the automotive sector.

Propelling Factors for Germany Automotive Carbon Fiber Composites Industry Growth

The growth of the Germany Automotive Carbon Fiber Composites Industry is propelled by several key factors. Technologically, advancements in automated production processes and material science have enhanced efficiency and reduced costs, making carbon fiber more accessible for automotive applications. Economically, the push for lightweight vehicles to improve fuel efficiency and meet stringent emission regulations is a significant driver. For instance, the German government's incentives for electric vehicles have increased demand for lightweight materials. Additionally, regulatory support from the EU, promoting sustainable materials, further bolsters market growth.

Obstacles in the Germany Automotive Carbon Fiber Composites Industry Market

The Germany Automotive Carbon Fiber Composites Industry faces several obstacles that could hinder growth. Regulatory challenges, such as stringent environmental regulations, increase production costs and compliance burdens. Supply chain disruptions, particularly in raw material sourcing, have led to delays and increased expenses, impacting production timelines. Competitive pressures from alternative materials like glass fiber composites pose a threat, as they offer a cost-effective substitute. These factors collectively contribute to a potential reduction in market growth by up to 5% annually.

Future Opportunities in Germany Automotive Carbon Fiber Composites Industry

The German automotive carbon fiber composites industry presents a wealth of future opportunities. The continued rise of electric vehicles (EVs), further supported by government incentives, creates a substantial market for lightweight materials. Advancements in carbon fiber recycling technologies are poised to unlock new markets by reducing waste and lowering production costs. Moreover, prevailing consumer trends that prioritize sustainability and superior vehicle performance are driving demand for eco-friendly and high-performance materials, creating fertile ground for innovative composite solutions. These factors collectively paint a picture of significant future growth and opportunity within the sector.

Major Players in the Germany Automotive Carbon Fiber Composites Industry Ecosystem

Key Developments in Germany Automotive Carbon Fiber Composites Industry Industry

- January 2022: Teijin Limited announced a new partnership with BMW to develop advanced carbon fiber composites for future electric vehicles, aiming to enhance vehicle performance and reduce weight.

- March 2023: Toray Industries launched a new line of high-performance carbon fiber materials specifically designed for automotive applications, expected to increase market penetration.

- June 2023: BASF acquired a stake in a carbon fiber recycling company, aiming to improve sustainability and reduce production costs.

- September 2023: SGL Group expanded its production capacity in Germany to meet the growing demand for carbon fiber composites in the automotive sector.

Strategic Germany Automotive Carbon Fiber Composites Industry Market Forecast

The strategic forecast for the German automotive carbon fiber composites industry projects substantial growth, driven by several key factors. The widespread adoption of electric vehicles (EVs), further incentivized by government support, is expected to significantly increase demand for lightweight materials. Concurrent technological advancements in both production processes and material science will continue to enhance manufacturing efficiency and reduce costs, thereby increasing the accessibility and affordability of carbon fiber. The growing emphasis on sustainability and the development of advanced recycling technologies provide further avenues for market expansion. This confluence of factors positions the industry for a robust CAGR of 10% from 2025 to 2033, signifying strong growth prospects and the potential for Germany to maintain its position as a leader in innovation within this sector.

Germany Automotive Carbon Fiber Composites Industry Segmentation

-

1. Production Type

- 1.1. Hand Layup

- 1.2. Resin Transfer Molding

- 1.3. Vacuum Infusion Processing

- 1.4. Injection Molding

- 1.5. Compression Molding

-

2. Application

- 2.1. Structural Assembly

- 2.2. Power train Component

- 2.3. Interior

- 2.4. Exterior

- 2.5. Others

Germany Automotive Carbon Fiber Composites Industry Segmentation By Geography

- 1. Germany

Germany Automotive Carbon Fiber Composites Industry Regional Market Share

Geographic Coverage of Germany Automotive Carbon Fiber Composites Industry

Germany Automotive Carbon Fiber Composites Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Type

- 5.1.1. Hand Layup

- 5.1.2. Resin Transfer Molding

- 5.1.3. Vacuum Infusion Processing

- 5.1.4. Injection Molding

- 5.1.5. Compression Molding

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Structural Assembly

- 5.2.2. Power train Component

- 5.2.3. Interior

- 5.2.4. Exterior

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Production Type

- 6. Germany Automotive Carbon Fiber Composites Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Type

- 6.1.1. Hand Layup

- 6.1.2. Resin Transfer Molding

- 6.1.3. Vacuum Infusion Processing

- 6.1.4. Injection Molding

- 6.1.5. Compression Molding

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Structural Assembly

- 6.2.2. Power train Component

- 6.2.3. Interior

- 6.2.4. Exterior

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Production Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Teijin Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Delphi

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Kineco

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Owens Cornin

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BASF

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 General Motors Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Toray Industries

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cytec Industries

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Far UK

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Gurit

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 3B-Fiberglass

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Johns Manville

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Base Group

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 BMW

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Nipposn Sheet Glass Co Ltd

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Jushi Group Co Ltd

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 SGL Group

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.1 Teijin Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Automotive Carbon Fiber Composites Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Germany Automotive Carbon Fiber Composites Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany Automotive Carbon Fiber Composites Industry Revenue billion Forecast, by Production Type 2020 & 2033

- Table 2: Germany Automotive Carbon Fiber Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Germany Automotive Carbon Fiber Composites Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Germany Automotive Carbon Fiber Composites Industry Revenue billion Forecast, by Production Type 2020 & 2033

- Table 5: Germany Automotive Carbon Fiber Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Germany Automotive Carbon Fiber Composites Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Automotive Carbon Fiber Composites Industry?

The projected CAGR is approximately 14.98%.

2. Which companies are prominent players in the Germany Automotive Carbon Fiber Composites Industry?

Key companies in the market include Teijin Limited, Delphi, Kineco, Owens Cornin, BASF, General Motors Company, Toray Industries, Cytec Industries, Far UK, Gurit, 3B-Fiberglass, Johns Manville, Base Group, BMW, Nipposn Sheet Glass Co Ltd, Jushi Group Co Ltd, SGL Group.

3. What are the main segments of the Germany Automotive Carbon Fiber Composites Industry?

The market segments include Production Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing demand from automobile industry4.; Increased focus on precision products.

6. What are the notable trends driving market growth?

Technological Advancements Driving Growth in the Market.

7. Are there any restraints impacting market growth?

4.; The cost of production and transportation4.; Regulations and quality standards.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Automotive Carbon Fiber Composites Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Automotive Carbon Fiber Composites Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Automotive Carbon Fiber Composites Industry?

To stay informed about further developments, trends, and reports in the Germany Automotive Carbon Fiber Composites Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence