Key Insights

The global Automotive Automatic Gearbox market is projected for significant expansion, driven by increasing demand for passenger and commercial vehicles. Consumer preference for enhanced driving convenience and sophisticated vehicle technologies, including ADAS and the growth of electric and hybrid vehicles, are key growth catalysts. Advanced automatic gearboxes are crucial for improved fuel efficiency and reduced emissions, supporting stringent environmental regulations and sustainability initiatives. Continuous innovation in CVT, DCT, and AMT technologies will further propel market adoption.

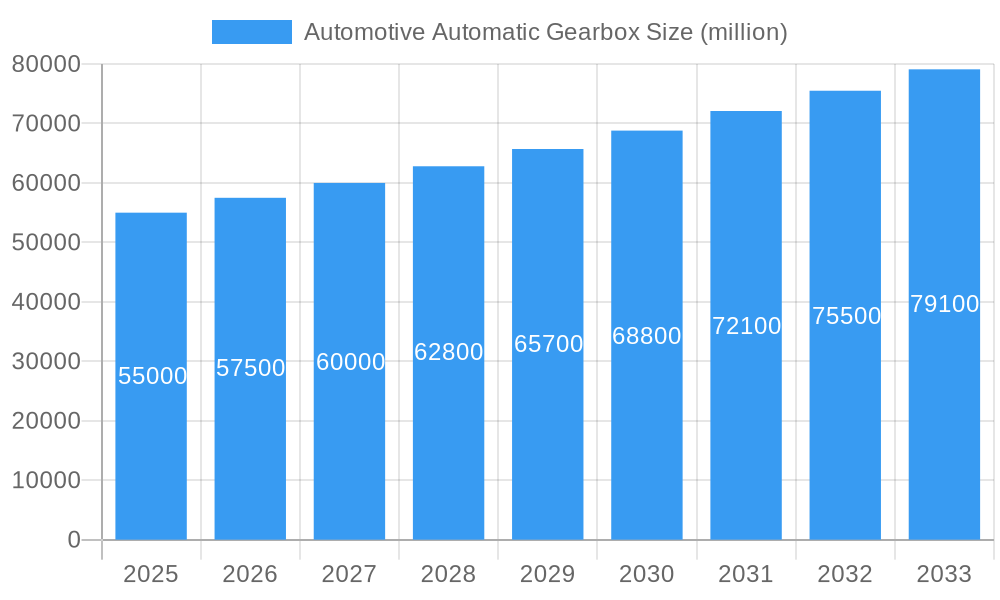

Automotive Automatic Gearbox Market Size (In Billion)

While market growth is robust, initial higher costs and complexity of advanced automatic transmissions present challenges, particularly in price-sensitive emerging markets. However, overwhelming consumer demand for ease of driving and ongoing technological advancements that reduce cost disparities are expected to offset these restraints. Key market trends include the development of more fuel-efficient, compact, and integrated smart technologies for optimized performance. Leading companies are investing in R&D for next-generation gearboxes, focusing on superior performance, durability, and adaptability to evolving powertrain architectures, especially for the electric vehicle sector.

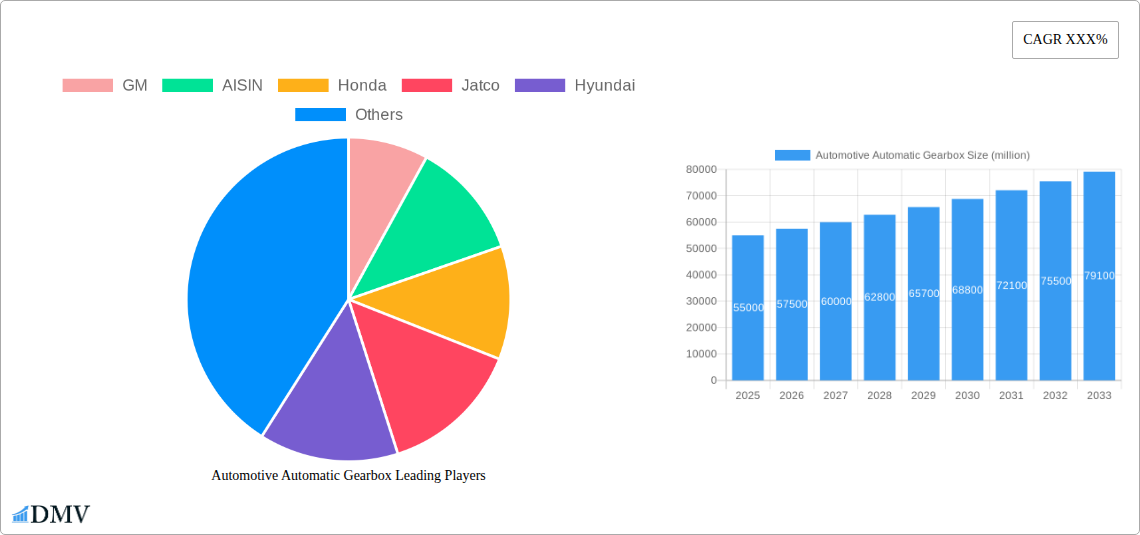

Automotive Automatic Gearbox Company Market Share

This report, Automotive Automatic Gearbox: Market Size, Share, Trends, Growth, and Forecast 2019-2033, provides an in-depth analysis of the global market. It examines key segments, technological advancements, regional trends, and product innovations, making it an essential resource for stakeholders. The market is forecast to reach $114.01 billion by 2025, with a projected CAGR of 2.7% from 2019-2033.

Automotive Automatic Gearbox Market Composition & Trends

The automotive automatic gearbox market is characterized by a dynamic interplay of competition and innovation. Market concentration is influenced by a few dominant players, yet the landscape is continuously reshaped by emerging technologies and strategic collaborations. Innovation catalysts such as advancements in electrification, software integration, and improved fuel efficiency are driving the development of next-generation automatic transmissions. The regulatory landscape, particularly concerning emissions standards and safety, plays a pivotal role in shaping product development and market adoption. Substitute products, primarily manual transmissions and increasingly sophisticated hybrid powertrains, present ongoing competitive pressures. End-user profiles are diverse, ranging from individual passenger vehicle owners seeking comfort and convenience to commercial vehicle fleet operators prioritizing efficiency and durability. Mergers and acquisitions (M&A) activities are strategically important for market leaders to expand their portfolios, gain technological expertise, and consolidate market share. For instance, M&A deal values are anticipated to reach $XX million in the forecast period, reflecting the strategic importance of consolidating capabilities in this high-growth sector. The market share distribution indicates a significant presence of Passenger Vehicle applications, accounting for an estimated XX% of the market by 2025, followed by Commercial Vehicle applications at XX%.

Automotive Automatic Gearbox Industry Evolution

The automotive automatic gearbox industry has witnessed a remarkable evolution driven by relentless technological advancements and shifting consumer preferences. Over the historical period (2019-2024), the market experienced steady growth, with adoption rates for automatic transmissions consistently rising across major automotive markets. The introduction and refinement of various automatic transmission types, including CVTs, DCTs, and DSGs, have significantly broadened consumer choice and offered enhanced driving experiences. Technological progress has been a primary engine of this evolution. Innovations in materials science have led to lighter and more durable gearbox components, while advanced control software has optimized shift patterns for improved fuel economy and performance. The increasing integration of electric and hybrid powertrains has also spurred the development of specialized automatic transmissions designed to seamlessly blend power from multiple sources. Consumer demand has increasingly gravitated towards automatic transmissions due to their inherent ease of use, reduced driver fatigue, and superior comfort in urban driving conditions. This trend is projected to accelerate throughout the forecast period (2025-2033), with an anticipated average annual growth rate of XX%. Adoption metrics indicate that by 2025, automatic transmissions will account for over XX% of all new vehicle sales globally. The market's growth trajectory is further bolstered by a growing emphasis on vehicle performance and driving dynamics, where modern automatic gearboxes excel in delivering swift and smooth gear changes. The continuous pursuit of enhanced efficiency, driven by both regulatory pressures and consumer awareness, ensures that automatic gearbox technology remains at the forefront of automotive innovation, with ongoing research and development focused on reducing friction losses and optimizing power delivery.

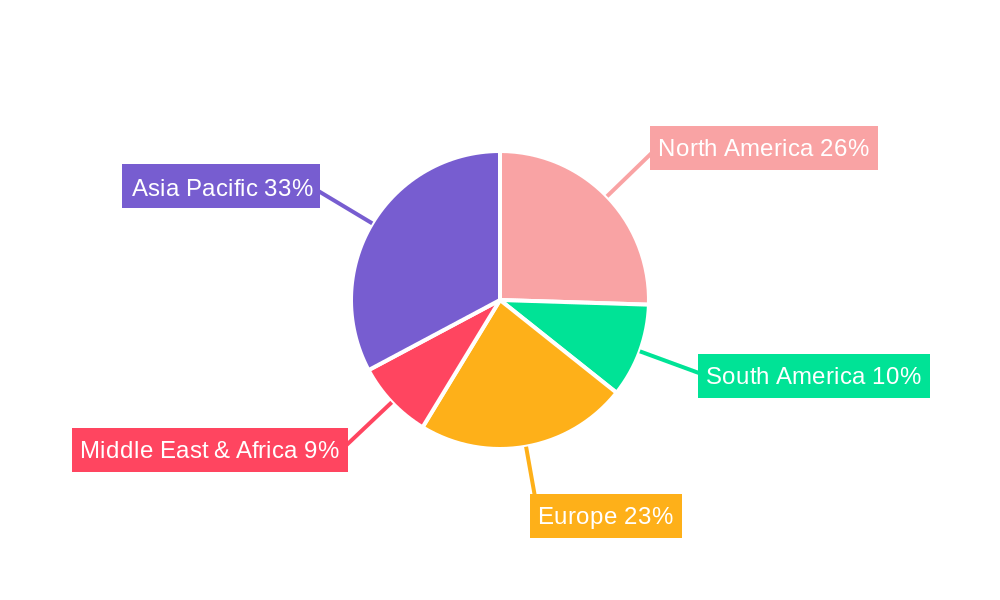

Leading Regions, Countries, or Segments in Automotive Automatic Gearbox

The Passenger Vehicle segment, particularly within the Asia-Pacific region, is currently the dominant force in the global automotive automatic gearbox market. This dominance is driven by a confluence of factors, including the sheer volume of vehicle production and sales in countries like China and India, coupled with a rapidly growing middle class that increasingly favors the convenience and comfort offered by automatic transmissions.

- Key Drivers in Asia-Pacific's Dominance:

- Mass Market Adoption: The vast consumer base in countries like China and India presents an enormous market for passenger vehicles equipped with automatic gearboxes.

- Increasing Disposable Income: Rising disposable incomes translate to a greater willingness among consumers to opt for premium features like automatic transmissions.

- Local Manufacturing Prowess: Key players like SAIC, AISIN, and Hyundai have established robust manufacturing capabilities in the region, leading to cost-effective production and supply.

- Government Initiatives: Favorable government policies aimed at boosting automotive production and promoting technological upgrades indirectly support the automatic gearbox market.

The Type: AT (Automatic Transmission) remains the most prevalent technology within the passenger vehicle segment, accounting for an estimated XX% of the market share in 2025. However, the Type: DCT (Dual-Clutch Transmission) and Type: CVT (Continuously Variable Transmission) segments are experiencing rapid growth, driven by their superior fuel efficiency and performance characteristics. DCTs, in particular, are gaining traction in performance-oriented passenger vehicles, while CVTs are favored for their smooth acceleration and fuel economy in economy and mid-range vehicles.

- Dominance Factors in Passenger Vehicles:

- Consumer Preference for Comfort: The primary driver for automatic transmissions in passenger cars is the enhanced driving experience, reducing driver fatigue in congested urban environments.

- Technological Advancements: Continuous improvements in AT, DCT, and CVT technologies have made them more efficient, responsive, and reliable, further solidifying their position.

- Electrification Synergies: The integration of automatic gearboxes with hybrid and electric powertrains is becoming increasingly sophisticated, offering seamless power delivery and optimized energy recuperation.

While Commercial Vehicles represent a smaller but significant portion of the market, they are increasingly adopting advanced automatic solutions for improved operational efficiency and driver comfort, especially in long-haul applications.

Automotive Automatic Gearbox Product Innovations

Product innovations in the automotive automatic gearbox market are primarily focused on enhancing efficiency, performance, and integration with evolving powertrain technologies. DCTs are pushing boundaries with faster shift times and improved fuel economy through their dual-clutch system, while CVTs are evolving with wider gear ratios and better torque handling capabilities. The integration of advanced electronic control units (ECUs) with sophisticated algorithms optimizes shift logic, leading to a more refined and responsive driving experience. Furthermore, the development of specialized automatic transmissions for hybrid and electric vehicles is a key area of innovation, focusing on seamless power blending, regenerative braking optimization, and torque vectoring for enhanced vehicle dynamics. Unique selling propositions often lie in weight reduction through advanced materials and compact designs, leading to improved vehicle efficiency and handling.

Propelling Factors for Automotive Automatic Gearbox Growth

The automotive automatic gearbox market is propelled by several key growth drivers. Technologically, the relentless pursuit of improved fuel efficiency and reduced emissions is a primary catalyst, pushing the development of more efficient AT, CVT, and DCT technologies. The increasing consumer demand for driving comfort and convenience, particularly in urban environments, is a significant economic factor boosting adoption rates. Furthermore, stringent government regulations mandating higher fuel economy standards and lower emission limits across major automotive markets are compelling manufacturers to integrate advanced automatic transmissions. The growing popularity of SUVs and performance vehicles, which often come standard with advanced automatic gearboxes, also contributes to market expansion. The rise of electrified powertrains necessitates sophisticated and adaptable automatic transmission systems, further driving innovation and market growth.

Obstacles in the Automotive Automatic Gearbox Market

Despite robust growth, the automotive automatic gearbox market faces several obstacles. High development and manufacturing costs associated with advanced technologies like DCTs and specialized hybrid transmissions can be a barrier, especially for smaller automakers. Supply chain disruptions, as evidenced by recent global events, can impact production volumes and increase lead times for critical components. While consumer adoption is high, certain performance purists may still prefer manual transmissions. Regulatory hurdles in certain niche markets or for specific transmission types can also pose challenges. Intense competitive pressures among established players and the constant need for R&D investment to stay ahead of technological advancements require significant capital allocation. The economic impact of these obstacles can lead to increased pricing for consumers and potential delays in new product introductions.

Future Opportunities in Automotive Automatic Gearbox

Emerging opportunities in the automotive automatic gearbox market are abundant and diverse. The continued electrification of the automotive industry presents a massive opportunity for the development of highly specialized and integrated automatic transmission systems for EVs and hybrids. The growing demand for autonomous driving technology requires advanced, highly precise, and responsive transmissions capable of seamless operation in complex driving scenarios. Expansion into emerging markets with rapidly developing automotive sectors offers significant untapped potential. Furthermore, the ongoing evolution of connected vehicle technologies allows for real-time transmission optimization based on traffic conditions and navigation data, creating opportunities for enhanced user experience and efficiency. The development of lighter, more compact, and modular gearbox designs will also cater to the evolving needs of vehicle manufacturers.

Major Players in the Automotive Automatic Gearbox Ecosystem

- GM

- AISIN

- Honda

- Jatco

- Hyundai

- ZF Friedrichshafen

- Ford

- Magna International

- Continental

- AFE

- Getrag

- B&M

- SAIC

- Fast

- Eaton Corporation

- GKN

- BorgWarner

- Allison Transmission

- AC Delco

- Anchor Industries

- ATE

- Allstar Performance

- Dynojet

Key Developments in Automotive Automatic Gearbox Industry

- 2023 September: BorgWarner announces advancements in its dual-clutch transmission technology, enhancing efficiency for hybrid applications.

- 2024 January: ZF Friedrichshafen showcases a new 8-speed automatic transmission designed for increased torque capacity and improved NVH (Noise, Vibration, and Harshness) performance.

- 2024 March: AISIN unveils a next-generation CVT with extended gear ratios and a focus on seamless integration with mild-hybrid systems.

- 2024 June: Jatco demonstrates a new compact automatic transmission for small and medium-sized passenger vehicles, prioritizing fuel economy.

- 2025 February: Continental introduces an intelligent transmission control unit that leverages AI for predictive shifting, optimizing performance and efficiency.

Strategic Automotive Automatic Gearbox Market Forecast

The strategic automotive automatic gearbox market forecast indicates continued robust growth, driven by the synergistic advancements in electrification, autonomous driving, and increasing consumer preference for refined driving experiences. Key growth catalysts include the ongoing transition towards hybrid and electric vehicles, which necessitates sophisticated and adaptable transmission systems, and the demand for enhanced fuel efficiency and reduced emissions, pushing innovation in DCT and CVT technologies. Emerging markets, particularly in Asia, will continue to be significant contributors to market expansion. Strategic investments in research and development, coupled with potential M&A activities, will be crucial for market leaders to maintain their competitive edge and capitalize on the evolving technological landscape. The overall market potential remains substantial, promising a dynamic and rewarding future for stakeholders in the automotive automatic gearbox industry.

Automotive Automatic Gearbox Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Vehicle

-

2. Type

- 2.1. AMT

- 2.2. CVT

- 2.3. DCT

- 2.4. DSG

- 2.5. AT

Automotive Automatic Gearbox Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Automatic Gearbox Regional Market Share

Geographic Coverage of Automotive Automatic Gearbox

Automotive Automatic Gearbox REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Automatic Gearbox Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. AMT

- 5.2.2. CVT

- 5.2.3. DCT

- 5.2.4. DSG

- 5.2.5. AT

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Automatic Gearbox Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. AMT

- 6.2.2. CVT

- 6.2.3. DCT

- 6.2.4. DSG

- 6.2.5. AT

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Automatic Gearbox Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. AMT

- 7.2.2. CVT

- 7.2.3. DCT

- 7.2.4. DSG

- 7.2.5. AT

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Automatic Gearbox Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. AMT

- 8.2.2. CVT

- 8.2.3. DCT

- 8.2.4. DSG

- 8.2.5. AT

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Automatic Gearbox Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. AMT

- 9.2.2. CVT

- 9.2.3. DCT

- 9.2.4. DSG

- 9.2.5. AT

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Automatic Gearbox Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. AMT

- 10.2.2. CVT

- 10.2.3. DCT

- 10.2.4. DSG

- 10.2.5. AT

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 GM

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 AISIN

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Honda

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Jatco

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hyundai

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ZF Friedrichshafen

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ford

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Magna International

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Continental

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 AFE

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Getrag

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 B&M

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 SAIC

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Fast

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Eaton Corporation

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 GKN

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 BorgWarner

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Allison Transmission

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 AC Delco

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Anchor Industries

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 ATE

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Allstar Performance

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Dynojet

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.1 GM

List of Figures

- Figure 1: Global Automotive Automatic Gearbox Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Automatic Gearbox Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Automatic Gearbox Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Automatic Gearbox Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Automotive Automatic Gearbox Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Automatic Gearbox Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Automatic Gearbox Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Automatic Gearbox Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Automatic Gearbox Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Automatic Gearbox Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Automotive Automatic Gearbox Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Automatic Gearbox Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Automatic Gearbox Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Automatic Gearbox Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Automatic Gearbox Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Automatic Gearbox Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Automotive Automatic Gearbox Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Automatic Gearbox Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Automatic Gearbox Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Automatic Gearbox Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Automatic Gearbox Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Automatic Gearbox Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Automatic Gearbox Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Automatic Gearbox Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Automatic Gearbox Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Automatic Gearbox Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Automatic Gearbox Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Automatic Gearbox Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Automatic Gearbox Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Automatic Gearbox Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Automatic Gearbox Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Automatic Gearbox Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Automatic Gearbox Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Automatic Gearbox Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Automatic Gearbox Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Automatic Gearbox Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Automatic Gearbox Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Automatic Gearbox Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Automatic Gearbox Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Automatic Gearbox Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Automatic Gearbox Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Automatic Gearbox Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Automatic Gearbox Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Automatic Gearbox Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Automatic Gearbox Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Automatic Gearbox Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Automatic Gearbox Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Automatic Gearbox Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Automatic Gearbox Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Automatic Gearbox Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Automatic Gearbox?

The projected CAGR is approximately 2.7%.

2. Which companies are prominent players in the Automotive Automatic Gearbox?

Key companies in the market include GM, AISIN, Honda, Jatco, Hyundai, ZF Friedrichshafen, Ford, Magna International, Continental, AFE, Getrag, B&M, SAIC, Fast, Eaton Corporation, GKN, BorgWarner, Allison Transmission, AC Delco, Anchor Industries, ATE, Allstar Performance, Dynojet.

3. What are the main segments of the Automotive Automatic Gearbox?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 114.01 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Automatic Gearbox," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Automatic Gearbox report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Automatic Gearbox?

To stay informed about further developments, trends, and reports in the Automotive Automatic Gearbox, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence