Key Insights

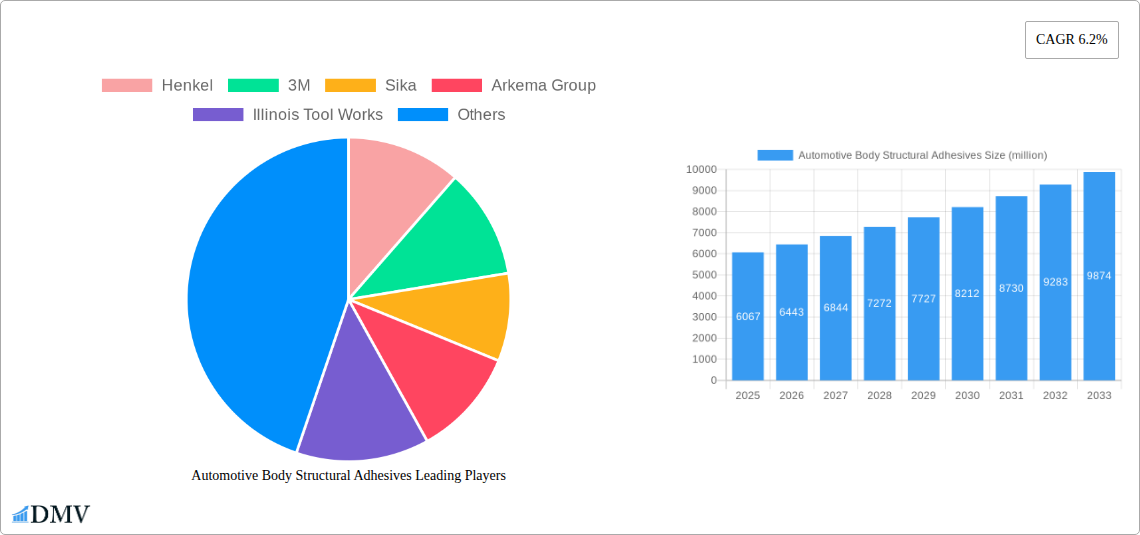

The global Automotive Body Structural Adhesives market is poised for substantial growth, with an estimated market size of USD 6,067 million in 2025, projected to expand at a Compound Annual Growth Rate (CAGR) of 6.2% through 2033. This robust expansion is fundamentally driven by the automotive industry's relentless pursuit of lighter, stronger, and more fuel-efficient vehicles. Traditional joining methods like welding are increasingly being supplemented, and in some cases replaced, by advanced structural adhesives that offer superior performance in terms of vibration dampening, stress distribution, and corrosion resistance. The burgeoning demand for passenger vehicles, coupled with the evolving needs of the commercial vehicle sector for enhanced durability and payload capacity, are key accelerators for this market. Furthermore, the ongoing integration of advanced materials like high-strength steel, aluminum, and composites in vehicle construction necessitates innovative bonding solutions, further solidifying the importance of structural adhesives.

The market is segmented by application into Commercial Vehicles and Passenger Vehicles, with Passenger Vehicles expected to dominate due to higher production volumes. By type, Epoxy and Urethane adhesives are anticipated to command significant market share owing to their exceptional mechanical properties and versatility. Emerging trends include the development of faster-curing adhesives, environmentally friendly formulations, and adhesive solutions designed for the unique challenges of electric vehicle (EV) manufacturing, such as battery pack assembly and thermal management. While the market benefits from strong underlying demand, potential restraints such as the need for specialized application equipment, stringent regulatory compliances for chemical usage, and the initial cost of implementation for certain advanced adhesive systems need to be navigated. However, the long-term benefits of improved vehicle performance, reduced manufacturing complexity, and enhanced safety are expected to outweigh these challenges, paving a clear path for sustained market expansion.

Automotive Body Structural Adhesives Market Research Report: Analysis, Trends, and Forecast 2019–2033

Unlock critical insights into the dynamic global Automotive Body Structural Adhesives market. This comprehensive report provides an in-depth analysis of market composition, industry evolution, regional dominance, product innovations, growth drivers, obstacles, and future opportunities. Covering a study period from 2019 to 2033, with a base year of 2025, this report equips stakeholders with actionable intelligence for strategic decision-making in the evolving automotive manufacturing landscape. Analyze key trends and forecasts to gain a competitive edge.

Automotive Body Structural Adhesives Market Composition & Trends

The Automotive Body Structural Adhesives market is characterized by a moderate level of concentration, with key players like Henkel, 3M, Sika, Arkema Group, and Illinois Tool Works holding significant market share. Innovation is a primary catalyst, driven by the increasing demand for lightweighting, enhanced safety, and improved vehicle performance. Regulatory landscapes, particularly concerning emissions and material sustainability, are also shaping product development. Substitute products, such as mechanical fasteners and welding, are being increasingly displaced by advanced structural adhesives due to their superior bonding capabilities and design flexibility. End-user profiles are diverse, encompassing major automotive OEMs and Tier-1 suppliers focused on both passenger vehicles and commercial vehicles. Mergers and acquisitions (M&A) activities, with estimated deal values in the hundreds of millions, are prevalent as companies seek to expand their product portfolios and geographic reach. For instance, the market share distribution reveals a competitive landscape where innovation and strategic partnerships are paramount for sustained growth. M&A activities valued at over $500 million have been observed, signaling consolidation and investment in promising technologies.

Automotive Body Structural Adhesives Industry Evolution

The Automotive Body Structural Adhesives industry has witnessed a remarkable evolution, marked by sustained market growth trajectories driven by the increasing adoption of lightweight materials and advanced manufacturing techniques in vehicle assembly. Technological advancements have been pivotal, with ongoing research and development in epoxy and urethane-based adhesives leading to enhanced bond strength, durability, and process efficiency. The shift towards electric vehicles (EVs) and autonomous driving technologies has further amplified the demand for specialized structural adhesives capable of managing complex battery pack integration and sensor mounting. Consumer demands for quieter, safer, and more fuel-efficient vehicles are directly fueling the adoption of these advanced bonding solutions. Market growth rates have consistently been in the high single digits, projected to exceed 7% annually during the forecast period. Adoption metrics indicate that over 80% of new passenger vehicles now incorporate structural adhesives in their assembly, a significant leap from the early 2010s. The development of novel formulations, such as high-temperature resistant adhesives for powertrain applications and flexible adhesives for noise, vibration, and harshness (NVH) reduction, are key indicators of this industrial evolution. Furthermore, the industry is increasingly focused on sustainable adhesive solutions, with a growing emphasis on bio-based and recyclable materials, aligning with global environmental regulations and OEM sustainability goals. The intricate interplay between material science innovation, evolving vehicle architectures, and stringent safety standards continues to propel this segment forward, promising continued expansion and diversification in its product offerings and applications.

Leading Regions, Countries, or Segments in Automotive Body Structural Adhesives

The Passenger Vehicles segment, particularly within the Epoxy and Urethane types, holds a dominant position in the global Automotive Body Structural Adhesives market. This dominance is primarily driven by the sheer volume of passenger vehicle production worldwide and the inherent need for advanced bonding solutions to meet stringent safety, performance, and weight reduction targets.

- Key Drivers in the Passenger Vehicles Segment:

- Stringent Safety Regulations: Global NCAP and Euro NCAP ratings necessitate robust structural integrity, directly increasing the reliance on high-strength structural adhesives for crashworthiness.

- Lightweighting Initiatives: OEMs are aggressively pursuing vehicle weight reduction to improve fuel efficiency and reduce CO2 emissions, with structural adhesives playing a crucial role in bonding dissimilar materials like aluminum, high-strength steel, and composites.

- Enhanced NVH Performance: Structural adhesives contribute significantly to reducing noise, vibration, and harshness, leading to a more comfortable and premium driving experience, a key differentiator in the competitive passenger vehicle market.

- Design Flexibility: Adhesives offer greater design freedom compared to traditional welding, enabling more aerodynamic and aesthetically appealing vehicle designs.

- Electrification Trend: The rise of Electric Vehicles (EVs) presents new bonding challenges and opportunities, particularly for battery pack assembly and structural reinforcement, where specialized adhesives are essential.

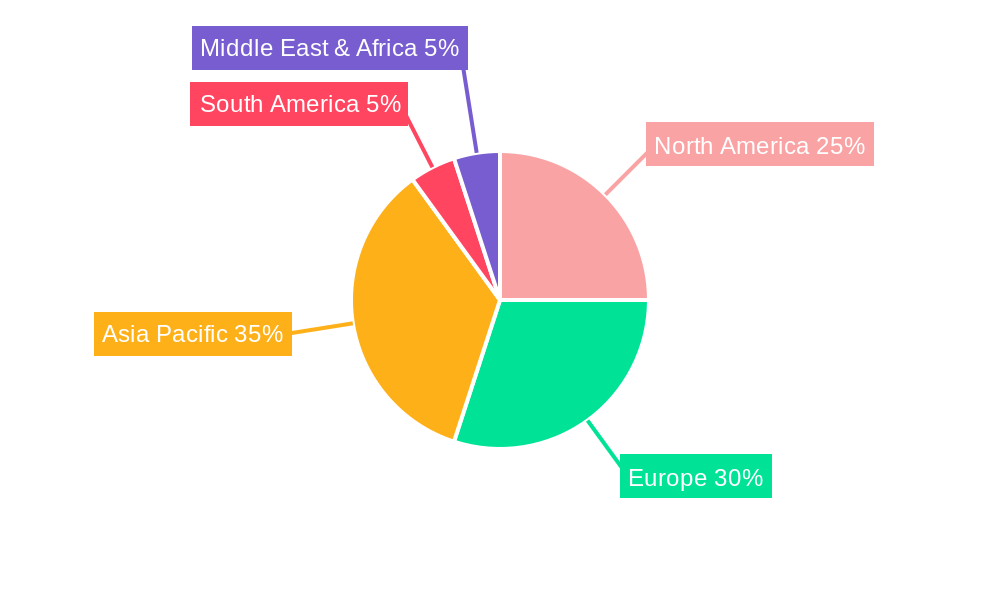

The Asia Pacific region, particularly China, is the leading geographical market. This supremacy is attributed to its status as the world's largest automotive manufacturing hub, coupled with significant government initiatives promoting advanced manufacturing and the adoption of new technologies. The region's robust domestic demand for passenger vehicles, combined with its export capabilities, further solidifies its leading position. Investment trends in the Asia Pacific region have seen substantial growth, with both domestic and international players investing heavily in R&D and manufacturing facilities. Regulatory support, including incentives for the automotive sector and a growing focus on environmental standards, also plays a crucial role in driving the adoption of modern structural adhesives. The dominance of passenger vehicles is further amplified by the continuous innovation in this segment, pushing the boundaries of adhesive performance to meet evolving vehicle demands. The market for specialty adhesives, such as those used in EV battery manufacturing and advanced driver-assistance systems (ADAS), is also expanding rapidly within this dominant segment and region.

Automotive Body Structural Adhesives Product Innovations

Recent product innovations in Automotive Body Structural Adhesives are revolutionizing vehicle manufacturing. Companies are developing advanced formulations that offer superior adhesion to a wider range of substrates, including dissimilar materials like aluminum, carbon fiber, and advanced composites. These innovations focus on enhancing bond strength, improving impact resistance, and enabling faster curing times, which directly translate to increased production line efficiency. Notable advancements include one-component moisture-cure urethanes for improved application ease and structural epoxies offering exceptional thermal resistance and durability for demanding automotive environments. Performance metrics are seeing significant improvements, with tensile strengths exceeding 30 megapascals and elongation properties tailored for flexibility and vibration dampening. These technological leaps are crucial for meeting the evolving demands of lightweighting and enhanced vehicle safety.

Propelling Factors for Automotive Body Structural Adhesives Growth

Several key factors are propelling the growth of the Automotive Body Structural Adhesives market. The relentless pursuit of vehicle lightweighting to enhance fuel efficiency and reduce emissions is a primary driver. Advances in adhesive technology, offering superior bonding capabilities for dissimilar materials, are enabling manufacturers to replace heavier traditional joining methods. Furthermore, increasing global safety regulations mandating higher crashworthiness and occupant protection directly benefit structural adhesives. The burgeoning electric vehicle market also presents significant opportunities, with adhesives crucial for battery pack assembly and thermal management. The demand for improved Noise, Vibration, and Harshness (NVH) performance further contributes to their adoption, leading to a more refined driving experience.

Obstacles in the Automotive Body Structural Adhesives Market

Despite robust growth, the Automotive Body Structural Adhesives market faces several obstacles. Stringent regulatory compliance, particularly concerning VOC emissions and the lifecycle assessment of adhesive materials, can pose challenges. Fluctuations in raw material prices, especially for petrochemical-based components, can impact cost-effectiveness. Supply chain disruptions, as witnessed in recent global events, can affect material availability and lead times. Intense competition from established players and the emergence of new technologies also exert pressure on market participants. Additionally, the initial investment required for specialized application equipment and the need for skilled labor can be a barrier for some smaller manufacturers.

Future Opportunities in Automotive Body Structural Adhesives

The future of Automotive Body Structural Adhesives is ripe with opportunities. The accelerating transition to electric vehicles will drive demand for specialized adhesives for battery systems, thermal management, and lightweight chassis components. The development of sustainable and bio-based adhesives presents a significant avenue for growth, aligning with increasing environmental consciousness and regulatory pressures. Advancements in smart adhesives, capable of self-healing or sensor integration, offer novel functionalities for future vehicles. Expansion into emerging automotive markets with growing manufacturing bases also presents significant potential. The continuous innovation in bonding dissimilar materials for advanced composite structures will further solidify the market's trajectory.

Major Players in the Automotive Body Structural Adhesives Ecosystem

- Henkel

- 3M

- Sika

- Arkema Group

- Illinois Tool Works

- ThreeBond

- Uniseal

- Sunstar

- Hubei Huitian New Materials

- H.B.Fuller

- Dow

- Parker

- Lord Corporation

- L&L Products

- PPG

- DuPont

- Parker Hannifin

- Unitech

- Jowat

- Darbond Technology

Key Developments in Automotive Body Structural Adhesives Industry

- 2023 November: Henkel launched a new generation of high-performance structural adhesives for EV battery pack assembly, offering improved thermal conductivity and fire resistance.

- 2023 October: 3M introduced a novel structural adhesive tape with enhanced peel strength and stress distribution capabilities for advanced composite bonding.

- 2023 September: Sika expanded its global manufacturing capacity for automotive adhesives to meet the growing demand in Southeast Asia.

- 2023 July: Arkema Group acquired a leading manufacturer of specialty adhesives for lightweight vehicle structures, strengthening its portfolio.

- 2023 March: Illinois Tool Works (ITW) announced the development of a faster-curing structural adhesive, aiming to reduce vehicle assembly cycle times.

- 2022 December: H.B. Fuller introduced a new line of structural adhesives designed for extreme temperature applications in automotive powertrains.

- 2022 August: DuPont showcased its advanced adhesive solutions for autonomous vehicle sensor integration and structural reinforcement.

- 2022 May: Lord Corporation unveiled a new series of vibration-damping structural adhesives for enhanced NVH performance in passenger vehicles.

Strategic Automotive Body Structural Adhesives Market Forecast

The strategic Automotive Body Structural Adhesives market forecast points towards continued robust growth, driven by the accelerating automotive industry's transition towards electrification, lightweighting, and enhanced safety features. The increasing adoption of advanced materials and the growing demand for improved vehicle performance and sustainability will be key growth catalysts. Emerging opportunities in smart adhesives and bio-based formulations, coupled with expansion into new geographical markets, are set to further boost market potential. Continuous innovation in adhesive technologies and strategic collaborations among key players will be crucial in capitalizing on these future opportunities, ensuring sustained expansion and market leadership.

Automotive Body Structural Adhesives Segmentation

-

1. Application

- 1.1. Commercial Vehicles

- 1.2. Passenger Vehicles

-

2. Type

- 2.1. Epoxy

- 2.2. Urethane

- 2.3. Others

Automotive Body Structural Adhesives Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Body Structural Adhesives REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.2% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Body Structural Adhesives Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicles

- 5.1.2. Passenger Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Epoxy

- 5.2.2. Urethane

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Body Structural Adhesives Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicles

- 6.1.2. Passenger Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Epoxy

- 6.2.2. Urethane

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Body Structural Adhesives Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicles

- 7.1.2. Passenger Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Epoxy

- 7.2.2. Urethane

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Body Structural Adhesives Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicles

- 8.1.2. Passenger Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Epoxy

- 8.2.2. Urethane

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Body Structural Adhesives Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicles

- 9.1.2. Passenger Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Epoxy

- 9.2.2. Urethane

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Body Structural Adhesives Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicles

- 10.1.2. Passenger Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Epoxy

- 10.2.2. Urethane

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Henkel

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 3M

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sika

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Arkema Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Illinois Tool Works

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ThreeBond

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Uniseal

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sunstar

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hubei Huitian New Materials

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 H.B.Fuller

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Dow

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Parker

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Lord Corporation

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 L&L Products

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 PPG

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 DuPont

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Parker Hannifin

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Unitech

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Jowat

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Darbond Technology

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Henkel

List of Figures

- Figure 1: Global Automotive Body Structural Adhesives Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Automotive Body Structural Adhesives Revenue (million), by Application 2024 & 2032

- Figure 3: North America Automotive Body Structural Adhesives Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Automotive Body Structural Adhesives Revenue (million), by Type 2024 & 2032

- Figure 5: North America Automotive Body Structural Adhesives Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Automotive Body Structural Adhesives Revenue (million), by Country 2024 & 2032

- Figure 7: North America Automotive Body Structural Adhesives Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Automotive Body Structural Adhesives Revenue (million), by Application 2024 & 2032

- Figure 9: South America Automotive Body Structural Adhesives Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Automotive Body Structural Adhesives Revenue (million), by Type 2024 & 2032

- Figure 11: South America Automotive Body Structural Adhesives Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Automotive Body Structural Adhesives Revenue (million), by Country 2024 & 2032

- Figure 13: South America Automotive Body Structural Adhesives Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Automotive Body Structural Adhesives Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Automotive Body Structural Adhesives Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Automotive Body Structural Adhesives Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Automotive Body Structural Adhesives Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Automotive Body Structural Adhesives Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Automotive Body Structural Adhesives Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Automotive Body Structural Adhesives Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Automotive Body Structural Adhesives Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Automotive Body Structural Adhesives Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Automotive Body Structural Adhesives Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Automotive Body Structural Adhesives Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Automotive Body Structural Adhesives Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Automotive Body Structural Adhesives Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Automotive Body Structural Adhesives Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Automotive Body Structural Adhesives Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Automotive Body Structural Adhesives Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Automotive Body Structural Adhesives Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Automotive Body Structural Adhesives Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Body Structural Adhesives Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Body Structural Adhesives Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Automotive Body Structural Adhesives Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Automotive Body Structural Adhesives Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Automotive Body Structural Adhesives Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Automotive Body Structural Adhesives Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Automotive Body Structural Adhesives Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Automotive Body Structural Adhesives Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Automotive Body Structural Adhesives Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Automotive Body Structural Adhesives Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Automotive Body Structural Adhesives Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Automotive Body Structural Adhesives Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Automotive Body Structural Adhesives Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Automotive Body Structural Adhesives Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Automotive Body Structural Adhesives Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Automotive Body Structural Adhesives Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Automotive Body Structural Adhesives Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Automotive Body Structural Adhesives Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Automotive Body Structural Adhesives Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Automotive Body Structural Adhesives Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Body Structural Adhesives?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Automotive Body Structural Adhesives?

Key companies in the market include Henkel, 3M, Sika, Arkema Group, Illinois Tool Works, ThreeBond, Uniseal, Sunstar, Hubei Huitian New Materials, H.B.Fuller, Dow, Parker, Lord Corporation, L&L Products, PPG, DuPont, Parker Hannifin, Unitech, Jowat, Darbond Technology.

3. What are the main segments of the Automotive Body Structural Adhesives?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6067 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Body Structural Adhesives," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Body Structural Adhesives report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Body Structural Adhesives?

To stay informed about further developments, trends, and reports in the Automotive Body Structural Adhesives, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence