Key Insights

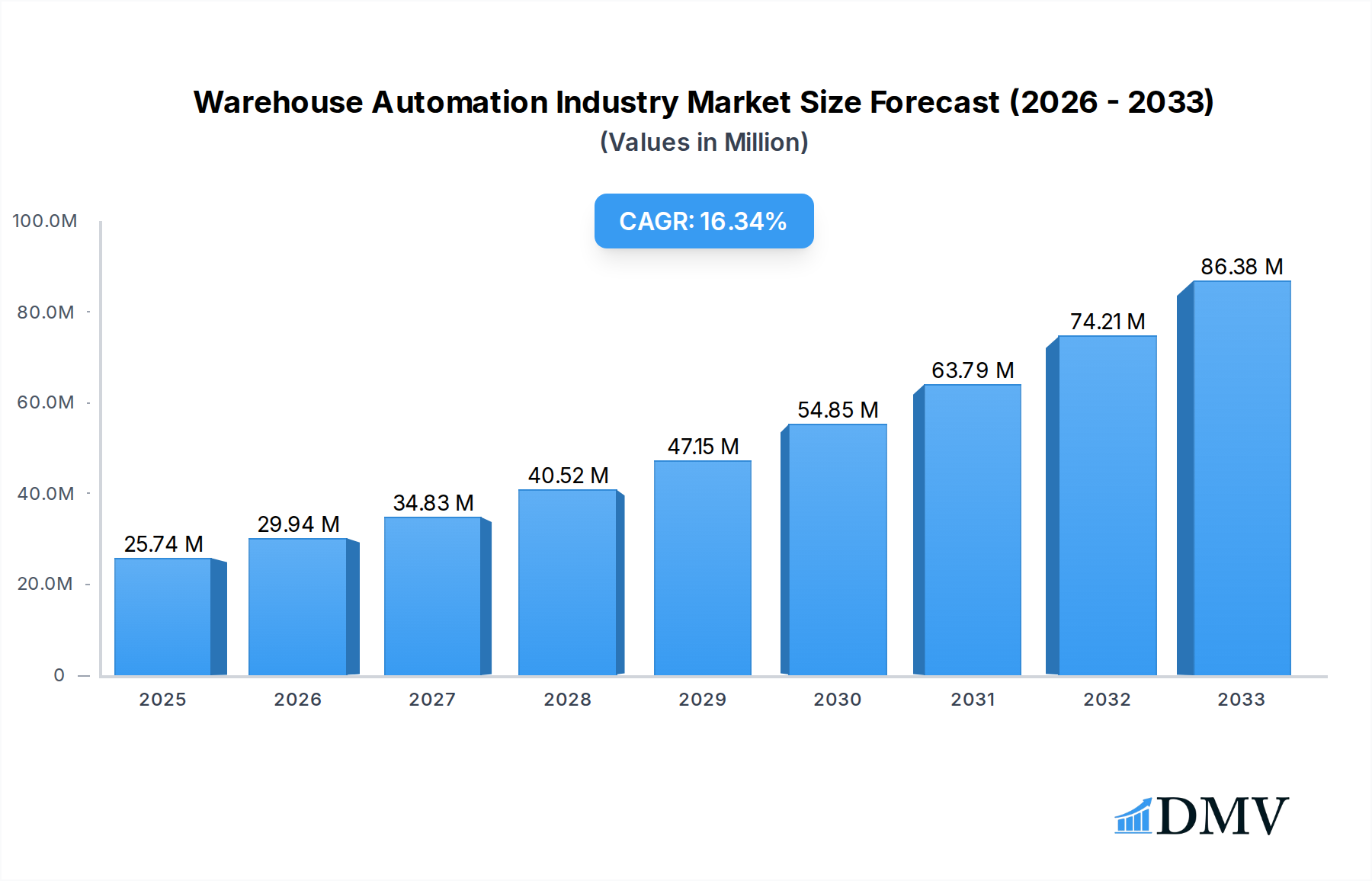

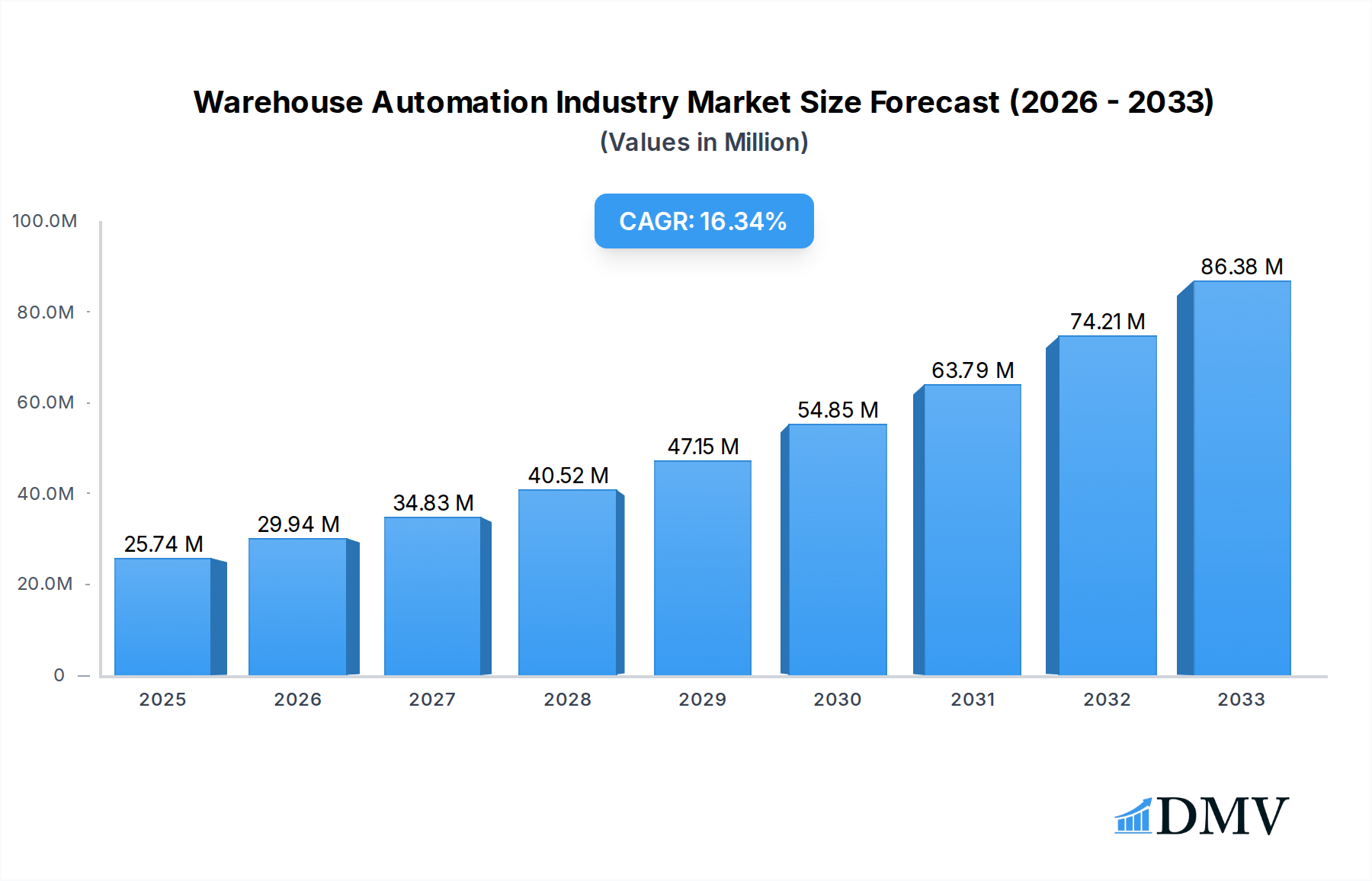

The global Warehouse Automation Industry is poised for remarkable expansion, projected to reach $25.74 million by 2025, fueled by a robust Compound Annual Growth Rate (CAGR) of 16.20% throughout the forecast period of 2025-2033. This significant surge is primarily driven by the escalating demand for enhanced operational efficiency, reduced labor costs, and improved accuracy in warehousing and logistics operations across diverse sectors. The increasing adoption of advanced technologies like Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT) is further catalyzing this growth, enabling more intelligent and autonomous warehouse management systems. Key market drivers include the growing e-commerce landscape, necessitating faster order fulfillment and streamlined inventory management, alongside the push for supply chain resilience and optimization in the face of global disruptions. The industry is also experiencing a trend towards flexible and scalable automation solutions, moving beyond traditional fixed systems to embrace modular and adaptable robots like Autonomous Mobile Robots (AMRs) and advanced automated storage and retrieval systems (AS/RS).

Warehouse Automation Industry Market Size (In Million)

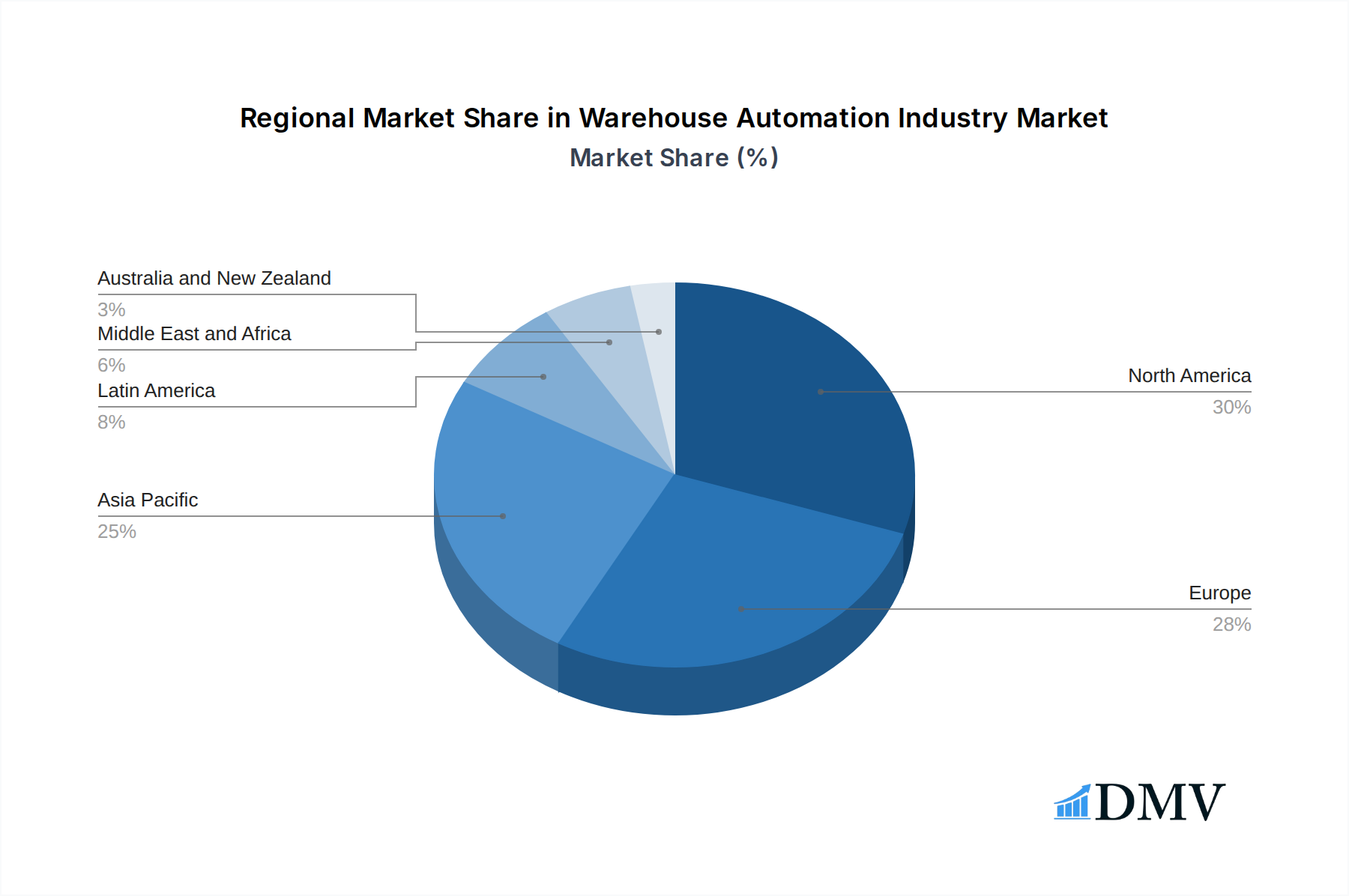

The Warehouse Automation Industry encompasses a comprehensive suite of solutions, with the "Component" segment being led by Hardware innovations. Within Hardware, Mobile Robots (AGVs and AMRs), Automated Storage and Retrieval Systems (AS/RS), and Automated Conveyor & Sorting Systems are at the forefront of adoption. The "Software" segment is crucial for orchestrating these physical systems, enabling intelligent planning, execution, and optimization. "Services," including value-added services and ongoing maintenance, are vital for ensuring the seamless operation and longevity of these complex automated solutions. Geographically, North America and Europe currently represent significant markets, driven by mature logistics infrastructure and high adoption rates of automation. However, the Asia-Pacific region is anticipated to exhibit the fastest growth, propelled by its burgeoning e-commerce sector and increasing investments in modernizing supply chains. Restraints, such as the high initial capital investment and the need for skilled personnel to manage and maintain automated systems, are being addressed through the development of more cost-effective solutions and a greater emphasis on training programs.

Warehouse Automation Industry Company Market Share

Warehouse Automation Industry Market Composition & Trends

The warehouse automation industry is characterized by a dynamic market composition driven by rapid technological advancements and increasing demand for efficient supply chain solutions. Market concentration is a key aspect, with major players like Daifuku Co Limited, Honeywell Intelligrated (Honeywell International Inc), and Dematic Group (Kion Group AG) holding significant shares in the automated storage and retrieval systems (AS/RS) and automated material handling equipment segments. Innovation catalysts include the proliferation of e-commerce, the need for labor cost reduction, and the pursuit of enhanced operational accuracy and speed. Regulatory landscapes are evolving, with a growing emphasis on safety standards and data security for automated systems. Substitute products are emerging in the form of advanced manual processes, but the inherent scalability and efficiency of automation continue to drive adoption. End-user profiles span diverse sectors, including Food and Beverage, Retail, and Post and Parcel, each with unique automation requirements. Mergers and acquisitions (M&A) are a significant trend, with deal values often in the hundreds of millions of dollars, indicating a consolidation phase and strategic expansion by leading companies. For instance, the acquisition of One Network Enterprise by Blue Yonder for approximately USD 839 Million highlights the increasing integration of software and network solutions within the broader automation ecosystem.

- Market Share Distribution: Dominant players in AS/RS and automated material handling hold a collective market share of over 60%.

- M&A Deal Values: Recent transactions, such as the acquisition of One Network Enterprises for an estimated XXX Million, underscore substantial financial investments in the sector.

- Key M&A Activities: Strategic acquisitions aim to bolster software capabilities, expand geographic reach, and integrate advanced AI and robotics solutions.

Warehouse Automation Industry Industry Evolution

The evolution of the warehouse automation industry is a compelling narrative of technological acceleration, driven by an insatiable demand for optimized logistics and supply chain resilience. Over the study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, the market has witnessed an exponential growth trajectory. This growth is intrinsically linked to the burgeoning e-commerce sector, which has placed unprecedented pressure on traditional warehousing operations to handle higher volumes, faster order fulfillment, and increased SKU complexity. The historical period from 2019 to 2024 laid the groundwork for this transformation, characterized by increasing adoption of Automated Storage and Retrieval Systems (AS/RS) and Mobile Robots (AGV, AMR). Technological advancements have been the primary engine of this evolution. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into warehouse management systems (WMS) and robotics has enabled more intelligent decision-making, predictive maintenance, and adaptive operations. For example, Jungheinrich's premiere of its latest mobile robot solution at LogiMAT 2023, featuring a robot that finds its own solutions and adapts to changing warehouse needs, exemplifies this leap in autonomous capability. The increasing sophistication of Piece Picking Robots and Automated Conveyor & Sorting Systems has further enhanced throughput and accuracy, directly addressing labor shortages and rising operational costs. Shifting consumer demands for faster delivery times and personalized shopping experiences have acted as a powerful catalyst, pushing businesses to invest in automation that can deliver on these expectations. The market is projected to see a Compound Annual Growth Rate (CAGR) of XX% during the forecast period, reaching an estimated XXX Billion by 2033. This expansion is not merely about speed but also about creating more agile, resilient, and sustainable supply chains capable of withstanding disruptions. The continuous refinement of software components, including advanced WMS and enterprise resource planning (ERP) integrations from giants like SAP S and Oracle Corporation, plays a pivotal role in orchestrating these complex automated environments. Furthermore, the growing emphasis on sustainability is driving the adoption of energy-efficient automation solutions, aligning with global environmental goals.

Leading Regions, Countries, or Segments in Warehouse Automation Industry

The global warehouse automation industry exhibits pronounced regional dominance and segment leadership, driven by distinct economic, regulatory, and technological factors. North America and Europe currently lead the market, owing to their mature e-commerce landscapes, significant investments in logistics infrastructure, and stringent labor regulations that incentivize automation. Asia-Pacific is emerging as a rapid growth region, fueled by the expansion of manufacturing hubs and a burgeoning middle class driving consumer demand.

Within the Component segment, Hardware remains the largest contributor. Specifically, Automated Storage and Retrieval Systems (AS/RS) and Mobile Robots (AGV, AMR) are spearheading this growth. The demand for high-density storage solutions offered by AS/RS is critical for optimizing space utilization in increasingly land-scarce urban environments. The flexibility and scalability of AGVs and AMRs, exemplified by Jungheinrich’s recent advancements in adaptable mobile robot solutions, cater to a wide range of material handling needs, from simple pallet transport to complex order picking. The Software segment, while smaller in current market share, is experiencing the fastest growth. This is driven by the increasing need for sophisticated Warehouse Management Systems (WMS) and Warehouse Control Systems (WCS) to orchestrate complex automated operations. Integrations with Enterprise Resource Planning (ERP) systems from companies like SAP S and Oracle Corporation are crucial for seamless data flow and operational visibility.

The Services segment, including Value Added Services and Maintenance, is also witnessing robust expansion. As automation deployments become more prevalent, the need for ongoing support, system upgrades, and predictive maintenance is paramount to ensure operational uptime and return on investment.

In terms of End-User industries, Food and Beverage and Retail are the largest adopters of warehouse automation. The perishable nature of food products necessitates rapid throughput and temperature-controlled environments, making AS/RS and advanced conveyor systems indispensable. The rapid growth of online retail, driven by consumer demand for quick delivery, has made automation a critical competitive differentiator. The Post and Parcel industry is another significant driver, constantly seeking ways to increase sortation speed and handling capacity to meet peak season demands. Manufacturing, encompassing both Durable and Non-Durable goods, is also a substantial market, particularly in areas requiring precise material handling and inventory management.

- Key Drivers for Hardware Dominance:

- Space Optimization: AS/RS solutions are crucial for maximizing storage capacity.

- Flexibility & Scalability: AGVs and AMRs offer adaptable material handling for diverse operational needs.

- Labor Shortages: Automation addresses the growing challenge of finding and retaining warehouse labor.

- Key Drivers for Software Growth:

- Operational Complexity: Advanced WMS and WCS are essential for managing integrated automated systems.

- Data Integration: Seamless connectivity with ERP systems is vital for end-to-end supply chain visibility.

- AI/ML Integration: Enhancing decision-making, predictive analytics, and autonomous operations.

- Key Drivers for Services Expansion:

- Maximizing Uptime: Proactive maintenance and support ensure continuous operations.

- System Upgrades: Keeping pace with technological advancements and evolving business needs.

- Return on Investment (ROI): Services contribute to the long-term value realization of automation investments.

- Dominance Factors in End-User Segments:

- Food & Beverage: Need for rapid, temperature-controlled, and compliant material handling.

- Retail: Driven by e-commerce growth and the demand for fast, accurate order fulfillment.

- Post & Parcel: High-volume sorting and handling requirements, especially during peak periods.

Warehouse Automation Industry Product Innovations

Recent product innovations in the warehouse automation industry are significantly enhancing operational efficiency and adaptability. Jungheinrich's new mobile robot solution, showcased at LogiMAT 2023, represents a leap in autonomy, featuring self-navigating capabilities and seamless integration into existing warehouse environments. This robot’s adaptive control system and toolchain allow for easy implementation and offer impressive flexibility from planning to daily operations, boosting performance and efficiency. Furthermore, advancements in Automated Storage and Retrieval Systems (AS/RS) are focusing on higher throughput, greater energy efficiency, and the ability to handle a wider range of product types and sizes. The development of more sophisticated Piece Picking Robots, utilizing AI and advanced vision systems, is improving accuracy and speed in e-commerce fulfillment.

Propelling Factors for Warehouse Automation Industry Growth

The warehouse automation industry's growth is propelled by a confluence of powerful factors. The relentless surge in e-commerce necessitates faster order fulfillment and increased inventory accuracy, directly driving the adoption of automated solutions. Persistent labor shortages across various regions compel businesses to invest in automation to maintain operational continuity and mitigate rising labor costs. Technological advancements, particularly in robotics, AI, and IoT, are continuously improving the capabilities and cost-effectiveness of automated systems. Furthermore, increasing consumer expectations for same-day or next-day delivery are pressuring businesses to optimize their logistics operations through automation.

- E-commerce Boom: Expanding online retail drives demand for rapid fulfillment.

- Labor Scarcity: Automation provides a sustainable solution to workforce challenges.

- Technological Advancements: Innovations in AI, robotics, and software enhance automation capabilities.

- Customer Expectations: Pressure for faster delivery times fuels automation investment.

Obstacles in the Warehouse Automation Industry Market

Despite its robust growth, the warehouse automation industry faces several significant obstacles. The substantial initial capital investment required for advanced automation systems can be a barrier for small and medium-sized enterprises (SMEs). Regulatory hurdles and the need for compliance with evolving safety standards can slow down implementation timelines. Supply chain disruptions, as witnessed in recent years, can impact the availability of critical components and delay project deployments, leading to increased costs. Moreover, the integration of new automated systems with existing legacy infrastructure often presents complex technical challenges, requiring specialized expertise and careful planning.

- High Initial Investment: Significant capital expenditure can deter smaller businesses.

- Regulatory Compliance: Navigating and adhering to evolving safety and operational standards.

- Supply Chain Volatility: Disruptions can affect component availability and project timelines.

- System Integration Complexity: Challenges in integrating new automation with existing IT and operational infrastructure.

Future Opportunities in Warehouse Automation Industry

The future of warehouse automation is ripe with opportunities, driven by emerging trends and unmet needs. The increasing demand for sustainable logistics presents a significant avenue for growth, focusing on energy-efficient automation solutions and robotics that reduce environmental impact. The expansion of Industry 4.0 principles, emphasizing interconnectedness and data-driven decision-making, will further integrate automation into the broader manufacturing and supply chain ecosystem. The development of more sophisticated AI and machine learning algorithms will enable even greater autonomy and predictive capabilities in warehouse operations. Furthermore, the growing adoption of automation in emerging markets and specialized sectors like pharmaceuticals and cold storage offers new frontiers for expansion.

- Sustainable Logistics: Development of eco-friendly automation solutions.

- Industry 4.0 Integration: Seamless connectivity within smart manufacturing and supply chains.

- Advanced AI & ML: Driving enhanced autonomy and predictive capabilities.

- Emerging Markets & Niches: Expansion into new geographies and specialized industry verticals.

Major Players in the Warehouse Automation Industry Ecosystem

- Jungheinrich AG

- Swisslog Holding AG (KUKA AG)

- Murata Machinery Ltd

- SAP S

- BEUMER Group GmbH & Co KG

- Daifuku Co Limited

- Honeywell Intelligrated (Honeywell International Inc)

- SSI Schaefer AG

- WITRON Logistik + Informatik GmbH

- TGW Logistics Group GmbH

- Kardex Group

- Oracle Corporation

- One Network Enterprises Inc

- Vanderlande Industries BV

- Knapp AG

- Mecalux SA

- Dematic Group (Kion Group AG)

Key Developments in Warehouse Automation Industry Industry

- July 2023: Jungheinrich premiered its latest mobile robot solution at Stuttgart's LogiMAT 2023. This robot is designed for easy integration into any warehouse, autonomously finding solutions and adapting to changing needs, thereby increasing performance and efficiency. Its newly developed control system and toolchain facilitate smooth, simple integration with existing warehouse environments, ensuring flexibility from planning to daily operations.

- March 2024: Blue Yonder announced an agreement to acquire One Network Enterprises for approximately USD 839 Million, subject to adjustments. One Network, a provider of the Digital Supply Chain Network, is recognized for its autonomous and resilience services and is a leading global provider of intelligent control towers. This acquisition positions Blue Yonder to better serve customer needs across planning, execution, commerce, and networks.

Strategic Warehouse Automation Industry Market Forecast

The strategic forecast for the warehouse automation industry is overwhelmingly positive, driven by the continuous evolution of e-commerce, the imperative for supply chain resilience, and relentless technological innovation. The market is poised for significant expansion as businesses globally prioritize efficiency, accuracy, and cost optimization in their logistics operations. Key growth catalysts include the increasing adoption of AI and machine learning for intelligent automation, the development of more versatile and adaptable robotic solutions, and the growing demand for integrated software platforms that provide end-to-end visibility and control. Opportunities in emerging markets and specialized sectors, coupled with a focus on sustainable automation practices, will further fuel this growth. By 2033, the industry is projected to reach an estimated market size of XXX Billion, underscoring its critical role in modern commerce.

Warehouse Automation Industry Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Mobile Robots (AGV, AMR)

- 1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 1.1.3. Automated Conveyor & Sorting Systems

- 1.1.4. De-palletizing/Palletizing Systems

- 1.1.5. Automati

- 1.1.6. Piece Picking Robots

- 1.2. Software

- 1.3. Services (Value Added Services, Maintenance, etc.)

-

1.1. Hardware

-

2. End-User

- 2.1. Food and

- 2.2. Post and Parcel

- 2.3. Retail

- 2.4. Apparel

- 2.5. Manufacturing (Durable and Non-Durable)

- 2.6. Other End-user Industries

Warehouse Automation Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Warehouse Automation Industry Regional Market Share

Geographic Coverage of Warehouse Automation Industry

Warehouse Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Mobile Robots (AGV, AMR)

- 5.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 5.1.1.3. Automated Conveyor & Sorting Systems

- 5.1.1.4. De-palletizing/Palletizing Systems

- 5.1.1.5. Automati

- 5.1.1.6. Piece Picking Robots

- 5.1.2. Software

- 5.1.3. Services (Value Added Services, Maintenance, etc.)

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Food and

- 5.2.2. Post and Parcel

- 5.2.3. Retail

- 5.2.4. Apparel

- 5.2.5. Manufacturing (Durable and Non-Durable)

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Warehouse Automation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Mobile Robots (AGV, AMR)

- 6.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3. Automated Conveyor & Sorting Systems

- 6.1.1.4. De-palletizing/Palletizing Systems

- 6.1.1.5. Automati

- 6.1.1.6. Piece Picking Robots

- 6.1.2. Software

- 6.1.3. Services (Value Added Services, Maintenance, etc.)

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Food and

- 6.2.2. Post and Parcel

- 6.2.3. Retail

- 6.2.4. Apparel

- 6.2.5. Manufacturing (Durable and Non-Durable)

- 6.2.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Warehouse Automation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.1.1. Mobile Robots (AGV, AMR)

- 7.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 7.1.1.3. Automated Conveyor & Sorting Systems

- 7.1.1.4. De-palletizing/Palletizing Systems

- 7.1.1.5. Automati

- 7.1.1.6. Piece Picking Robots

- 7.1.2. Software

- 7.1.3. Services (Value Added Services, Maintenance, etc.)

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Food and

- 7.2.2. Post and Parcel

- 7.2.3. Retail

- 7.2.4. Apparel

- 7.2.5. Manufacturing (Durable and Non-Durable)

- 7.2.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Warehouse Automation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.1.1. Mobile Robots (AGV, AMR)

- 8.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 8.1.1.3. Automated Conveyor & Sorting Systems

- 8.1.1.4. De-palletizing/Palletizing Systems

- 8.1.1.5. Automati

- 8.1.1.6. Piece Picking Robots

- 8.1.2. Software

- 8.1.3. Services (Value Added Services, Maintenance, etc.)

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Food and

- 8.2.2. Post and Parcel

- 8.2.3. Retail

- 8.2.4. Apparel

- 8.2.5. Manufacturing (Durable and Non-Durable)

- 8.2.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Warehouse Automation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.1.1. Mobile Robots (AGV, AMR)

- 9.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 9.1.1.3. Automated Conveyor & Sorting Systems

- 9.1.1.4. De-palletizing/Palletizing Systems

- 9.1.1.5. Automati

- 9.1.1.6. Piece Picking Robots

- 9.1.2. Software

- 9.1.3. Services (Value Added Services, Maintenance, etc.)

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Food and

- 9.2.2. Post and Parcel

- 9.2.3. Retail

- 9.2.4. Apparel

- 9.2.5. Manufacturing (Durable and Non-Durable)

- 9.2.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Australia and New Zealand Warehouse Automation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.1.1. Mobile Robots (AGV, AMR)

- 10.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 10.1.1.3. Automated Conveyor & Sorting Systems

- 10.1.1.4. De-palletizing/Palletizing Systems

- 10.1.1.5. Automati

- 10.1.1.6. Piece Picking Robots

- 10.1.2. Software

- 10.1.3. Services (Value Added Services, Maintenance, etc.)

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Food and

- 10.2.2. Post and Parcel

- 10.2.3. Retail

- 10.2.4. Apparel

- 10.2.5. Manufacturing (Durable and Non-Durable)

- 10.2.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Latin America Warehouse Automation Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.1.1. Mobile Robots (AGV, AMR)

- 11.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 11.1.1.3. Automated Conveyor & Sorting Systems

- 11.1.1.4. De-palletizing/Palletizing Systems

- 11.1.1.5. Automati

- 11.1.1.6. Piece Picking Robots

- 11.1.2. Software

- 11.1.3. Services (Value Added Services, Maintenance, etc.)

- 11.1.1. Hardware

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Food and

- 11.2.2. Post and Parcel

- 11.2.3. Retail

- 11.2.4. Apparel

- 11.2.5. Manufacturing (Durable and Non-Durable)

- 11.2.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Middle East and Africa Warehouse Automation Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Component

- 12.1.1. Hardware

- 12.1.1.1. Mobile Robots (AGV, AMR)

- 12.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 12.1.1.3. Automated Conveyor & Sorting Systems

- 12.1.1.4. De-palletizing/Palletizing Systems

- 12.1.1.5. Automati

- 12.1.1.6. Piece Picking Robots

- 12.1.2. Software

- 12.1.3. Services (Value Added Services, Maintenance, etc.)

- 12.1.1. Hardware

- 12.2. Market Analysis, Insights and Forecast - by End-User

- 12.2.1. Food and

- 12.2.2. Post and Parcel

- 12.2.3. Retail

- 12.2.4. Apparel

- 12.2.5. Manufacturing (Durable and Non-Durable)

- 12.2.6. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Component

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Jungheinrich AG

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Swisslog Holding AG (KUKA AG)

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Murata Machinery Ltd

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 SAP S

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 BEUMER Group GmbH & Co KG

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Daifuku Co Limited

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Honeywell Intelligrated (Honeywell International Inc )

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 SSI Schaefer AG

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 WITRON Logistik + Informatik GmbH

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 TGW Logistics Group GmbH

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Kardex Group

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Oracle Corporation

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 One Network Enterprises Inc

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Vanderlande Industries BV

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Knapp AG

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Mecalux SA

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 Dematic Group (Kion Group AG)

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.1 Jungheinrich AG

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Warehouse Automation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Warehouse Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 3: North America Warehouse Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Warehouse Automation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 5: North America Warehouse Automation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 6: North America Warehouse Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Warehouse Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Warehouse Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 9: Europe Warehouse Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 10: Europe Warehouse Automation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 11: Europe Warehouse Automation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 12: Europe Warehouse Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Warehouse Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Warehouse Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 15: Asia Warehouse Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 16: Asia Warehouse Automation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 17: Asia Warehouse Automation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 18: Asia Warehouse Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Warehouse Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 21: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 22: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 23: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Australia and New Zealand Warehouse Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Australia and New Zealand Warehouse Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Warehouse Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 27: Latin America Warehouse Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 28: Latin America Warehouse Automation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 29: Latin America Warehouse Automation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 30: Latin America Warehouse Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Latin America Warehouse Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East and Africa Warehouse Automation Industry Revenue (Million), by Component 2025 & 2033

- Figure 33: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by Component 2025 & 2033

- Figure 34: Middle East and Africa Warehouse Automation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 35: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 36: Middle East and Africa Warehouse Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Middle East and Africa Warehouse Automation Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 3: Global Warehouse Automation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 5: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 8: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 9: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 11: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 12: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 14: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 15: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 17: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 18: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Global Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 20: Global Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 21: Global Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Warehouse Automation Industry?

The projected CAGR is approximately 16.20%.

2. Which companies are prominent players in the Warehouse Automation Industry?

Key companies in the market include Jungheinrich AG, Swisslog Holding AG (KUKA AG), Murata Machinery Ltd, SAP S, BEUMER Group GmbH & Co KG, Daifuku Co Limited, Honeywell Intelligrated (Honeywell International Inc ), SSI Schaefer AG, WITRON Logistik + Informatik GmbH, TGW Logistics Group GmbH, Kardex Group, Oracle Corporation, One Network Enterprises Inc, Vanderlande Industries BV, Knapp AG, Mecalux SA, Dematic Group (Kion Group AG).

3. What are the main segments of the Warehouse Automation Industry?

The market segments include Component, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.74 Million as of 2022.

5. What are some drivers contributing to market growth?

Exponential Growth of the E-commerce Industry and Customer Expectation; Increasing Manufacturing Complexity and Technology Availability.

6. What are the notable trends driving market growth?

Retail to Have a Significant Growth.

7. Are there any restraints impacting market growth?

Optimizing Battery Life of Hearable Device.

8. Can you provide examples of recent developments in the market?

July 2023 - Jungheinrich, premiered its latest mobile robot solution at Stuttgart's LogiMAT 2023, the international trade fair for intralogistics solutions. It's a robot that can be easily integrated into any warehouse, which finds its own solutions, and which adapts to changing warehouse needs, increasing performance and efficiency. Its newly developed control system and toolchain enable smooth, simple integration with any existing warehouse environment and guarantee impressive flexibility from planning stage to day-to-day operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Warehouse Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Warehouse Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Warehouse Automation Industry?

To stay informed about further developments, trends, and reports in the Warehouse Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence