Key Insights

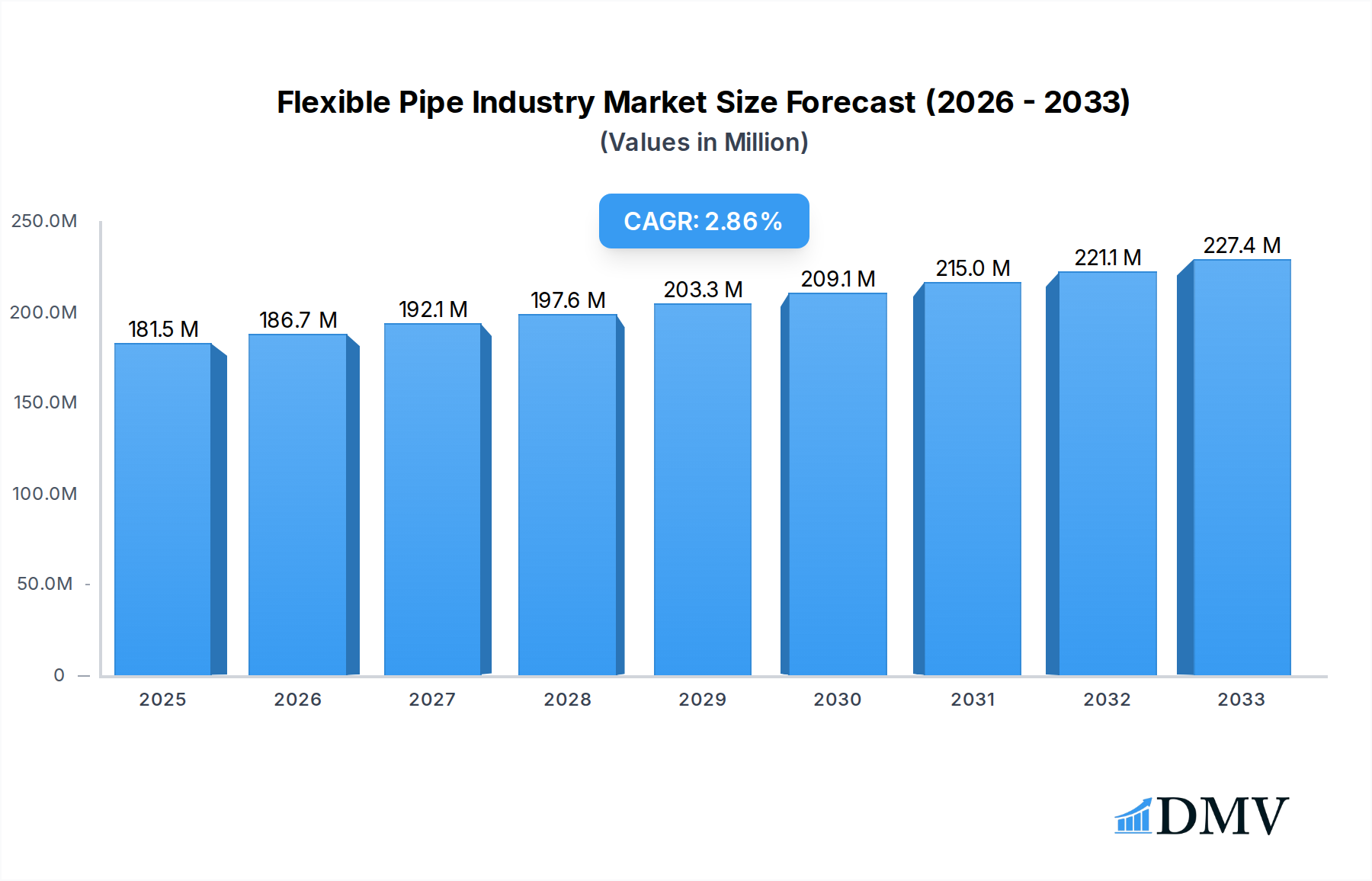

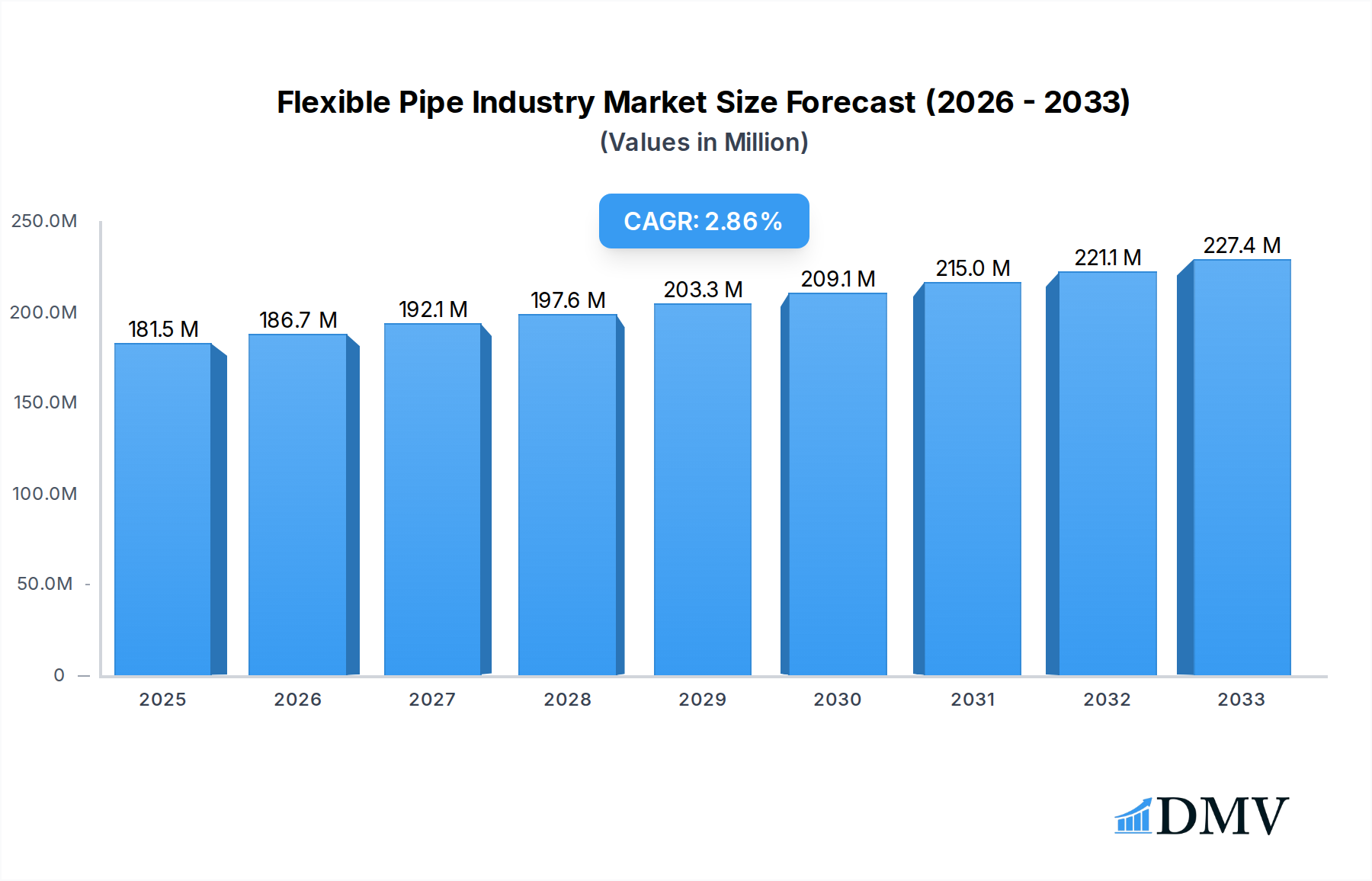

The global Flexible Pipe market is poised for steady growth, with an estimated market size of USD 181.5 million in 2025, projected to expand at a Compound Annual Growth Rate (CAGR) of 2.9% through 2033. This sustained expansion is largely driven by the increasing demand for efficient and reliable fluid transportation solutions in the oil and gas industry, particularly in offshore and deepwater exploration and production activities. The inherent flexibility, corrosion resistance, and ease of installation of these pipes make them an attractive alternative to traditional rigid pipelines, especially in challenging environments. The market's trajectory is further bolstered by ongoing investments in infrastructure development and the need for specialized piping systems in various industrial applications. Key raw materials like High-density Polyethylene (HDPE), Polyamides, and Polyvinylidene Fluoride (PVDF) play a crucial role in determining the performance and application suitability of flexible pipes, with continuous innovation in material science enhancing their capabilities.

Flexible Pipe Industry Market Size (In Million)

The growth of the flexible pipe industry is further fueled by evolving market trends such as the increasing preference for cost-effective and sustainable piping solutions. While the market is predominantly influenced by the oil and gas sector, particularly offshore applications, diversification into other sectors like water management and industrial fluid transfer presents significant growth opportunities. Emerging technologies and advancements in manufacturing processes are contributing to improved product performance, durability, and cost-effectiveness, thereby broadening their adoption. However, the market faces certain challenges, including the fluctuating prices of raw materials and the stringent regulatory landscape governing the oil and gas industry, which can impact project timelines and investment decisions. Despite these hurdles, the inherent advantages and expanding application base of flexible pipes position the market for continued and robust expansion in the foreseeable future.

Flexible Pipe Industry Company Market Share

Flexible Pipe Industry Market Composition & Trends

The Flexible Pipe Industry is a dynamic and increasingly concentrated market, driven by significant technological innovation and evolving regulatory landscapes. The market's competitive intensity is high, with a few key players holding substantial market share, projected to reach $25,000 million by 2025 and expand to $35,000 million by 2033. Innovation in material science and manufacturing processes are the primary catalysts, enabling the development of pipes capable of withstanding extreme pressures, temperatures, and corrosive environments. The increasing demand for efficient and cost-effective solutions in offshore oil and gas exploration, particularly in deepwater and ultra-deepwater applications, is a major trend.

Market Share Distribution (Estimated 2025):

- Leading Players (Top 3): XX%

- Emerging Players: XX%

- Niche Specialists: XX%

Innovation Catalysts:

- Advancements in composite materials for enhanced durability.

- Development of specialized coatings for chemical resistance.

- Digitalization in manufacturing for precision and quality control.

Regulatory Landscapes:

- Stringent safety and environmental regulations (e.g., offshore discharge limits) driving demand for advanced flexible pipe solutions.

- Government initiatives promoting energy infrastructure development.

Substitute Products:

- Rigid pipelines and spoolable composite pipes, though often less adaptable for complex subsea layouts.

End-User Profiles:

- Oil and Gas (Upstream, Midstream, Downstream).

- Petrochemicals.

- Mining and Dredging.

- Water and Wastewater Management.

M&A Activities:

- The market has witnessed strategic acquisitions and partnerships aimed at consolidating expertise, expanding geographical reach, and enhancing product portfolios. M&A deal values are estimated to be in the range of $500 million to $1,500 million in the historical period and are expected to continue with similar or higher valuations.

Flexible Pipe Industry Industry Evolution

The Flexible Pipe Industry has undergone a remarkable evolution, transforming from a niche solution to a critical component across various industrial sectors, most prominently in oil and gas. This evolution has been characterized by consistent market growth, with the global market size estimated to be $25,000 million in the base year of 2025, and projected to ascend to $35,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 4.7% over the forecast period. This growth trajectory is underpinned by significant technological advancements that have pushed the boundaries of material science and engineering.

Historically, flexible pipes were limited in their pressure and temperature ratings, restricting their application to less demanding environments. However, continuous research and development have led to the introduction of high-performance composite materials, such as advanced polyamides and polyvinylidene fluoride (PVDF), capable of withstanding extreme conditions. These advancements have been crucial in enabling the expansion of offshore oil and gas exploration into deeper waters, where traditional rigid pipelines become prohibitively expensive and technically challenging to install and operate. The ability of flexible pipes to accommodate complex subsea terrains, minimize installation time, and reduce the need for specialized support vessels has made them indispensable in deepwater and ultra-deepwater projects.

Shifting consumer demands, driven by the industry's imperative for greater efficiency, cost-effectiveness, and environmental sustainability, have further shaped the evolution of the flexible pipe market. End-users are increasingly seeking solutions that offer longer service life, reduced maintenance requirements, and lower operational risks. This has spurred innovation in areas like corrosion resistance, fatigue life, and dynamic response to external forces. Furthermore, the growing emphasis on environmental protection and stricter regulations concerning hydrocarbon leakage have driven the demand for flexible pipes with enhanced integrity and leak detection capabilities. The adoption of flexible pipes has not only accelerated in the oil and gas sector but has also seen increased interest in other industries like mining, petrochemicals, and even water management, where their inherent flexibility and resistance to harsh chemicals provide distinct advantages. The historical period from 2019–2024 saw a steady increase in adoption, with an estimated growth rate of 5.2% annually, fueled by a surge in offshore exploration activities and infrastructure upgrades. This upward trend is expected to continue, albeit at a slightly moderated pace of 4.7% from 2025–2033, as the market matures and new technological frontiers are explored.

Leading Regions, Countries, or Segments in Flexible Pipe Industry

The Flexible Pipe Industry is experiencing dominance from specific regions and applications, driven by substantial investments, supportive regulatory frameworks, and unique operational demands. Among the applications, Offshore (Deepwater, Ultra-deepwater) stands out as the most significant segment, contributing an estimated 65% to the global market value in 2025. This dominance is directly attributable to the escalating global demand for oil and gas, coupled with the increasing technical feasibility and economic viability of extracting hydrocarbons from increasingly challenging deep-sea reserves. The inherent advantages of flexible pipes in these environments—their ability to be deployed in complex subsea configurations, their resistance to high pressures and corrosive seawater, and their reduced installation costs compared to rigid pipelines—make them the preferred choice for numerous offshore projects.

Within the Raw Material segment, High-density Polyethylene (HDPE) and Polyamides are the leading contributors, collectively accounting for an estimated 55% of the material market share in 2025. HDPE is widely utilized for its excellent chemical resistance, low friction properties, and cost-effectiveness in various onshore and shallower offshore applications. Polyamides, on the other hand, are crucial for high-pressure applications and resistance to hydrocarbons and sour gas environments, making them indispensable for deepwater and ultra-deepwater operations. Polyvinylidene Fluoride (PVDF) also holds a significant share, particularly for its superior chemical and thermal stability in demanding corrosive environments.

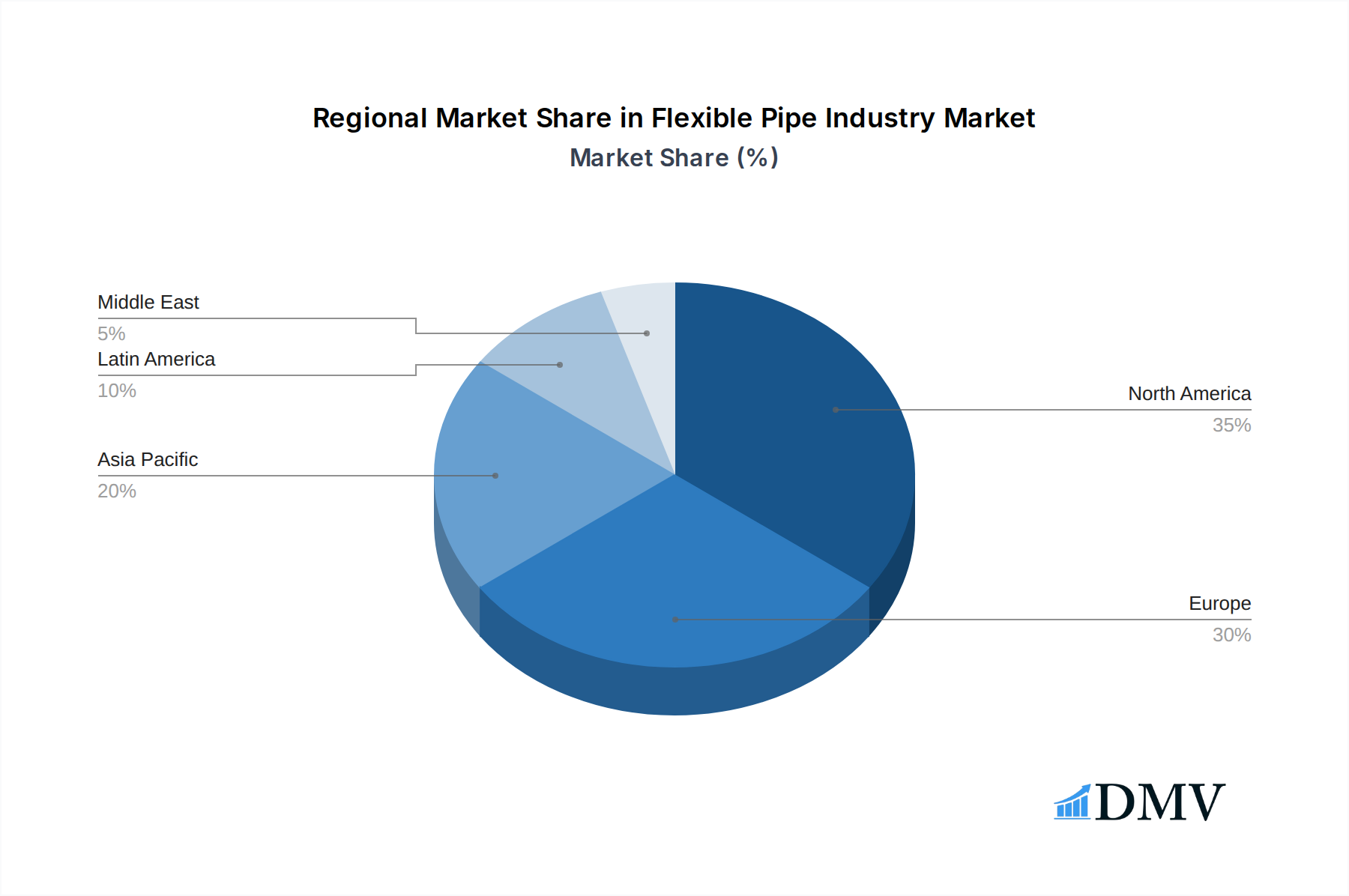

Geographically, North America, particularly the United States and Canada, along with the Asia Pacific region (driven by China, Southeast Asia, and Australia), are emerging as key growth hubs.

Key Drivers for Offshore Dominance:

- Investment Trends: Substantial upstream capital expenditure by major oil and gas companies in deepwater exploration and production projects worldwide. For instance, major projects in the Gulf of Mexico and the South China Sea are heavily reliant on advanced flexible pipe systems, representing billions in investment.

- Regulatory Support: Favorable government policies and production incentive programs in key offshore regions encourage the development of deep-sea resources.

- Technological Advancements: Continued innovation in flexible pipe technology, including higher pressure ratings, improved chemical resistance, and longer service life, directly supports deeper and more challenging offshore operations.

Dominance Factors in Raw Materials:

- Cost-Effectiveness: HDPE offers a balance of performance and cost, making it a popular choice for a wide range of applications.

- Performance Characteristics: Polyamides and PVDF provide the superior mechanical strength, chemical inertness, and thermal resistance required for the most demanding offshore environments.

- Availability: The established global supply chains for these raw materials ensure consistent availability for manufacturers.

Regional Dominance Factors:

- North America: Driven by significant deepwater activities in the Gulf of Mexico and the ongoing development of unconventional oil and gas resources requiring specialized pipeline solutions. The presence of major oilfield service companies and technology providers further bolsters this region.

- Asia Pacific: Rapidly expanding energy demands, coupled with substantial investments in offshore exploration and the development of new oil and gas fields, especially in Southeast Asia, are fueling the demand for flexible pipes. Government initiatives to boost domestic energy production also play a crucial role.

Flexible Pipe Industry Product Innovations

The Flexible Pipe Industry is continuously evolving with groundbreaking product innovations designed to meet increasingly stringent performance requirements and environmental standards. Key advancements include the development of high-pressure, high-temperature (HPHT) flexible pipes engineered to withstand extreme subsea conditions, often exceeding 500 bar and 150°C. Furthermore, significant progress has been made in creating composite flexible pipes with enhanced chemical resistance, enabling reliable transport of aggressive fluids like sour gas and highly acidic compounds. Innovations in internal lining materials, such as advanced polymers like PVDF and fluoropolymers, offer superior protection against corrosion and erosion, thereby extending the service life of the pipes and reducing maintenance needs. The integration of smart sensing technologies within the pipe structure for real-time monitoring of pressure, temperature, and structural integrity is another crucial development, enhancing operational safety and predictive maintenance capabilities.

Propelling Factors for Flexible Pipe Industry Growth

Several critical factors are propelling the growth of the Flexible Pipe Industry. Firstly, the relentless global demand for energy, particularly from offshore oil and gas exploration in deepwater and ultra-deepwater reserves, is a primary driver. This is compounded by advancements in materials science and manufacturing, leading to more robust, cost-effective, and reliable flexible pipe solutions. Secondly, increasingly stringent environmental regulations and safety standards worldwide are pushing industries to adopt more secure and leak-resistant pipeline systems, a role flexible pipes are exceptionally suited to fulfill. Finally, the inherent advantages of flexible pipes, such as ease of installation, adaptability to complex terrains, and reduced project timelines, offer significant economic benefits, making them an attractive alternative to rigid pipelines in many scenarios.

Obstacles in the Flexible Pipe Industry Market

Despite robust growth, the Flexible Pipe Industry faces several obstacles. High upfront capital investment for specialized manufacturing equipment and R&D can be a barrier for new entrants. Fluctuations in raw material prices, particularly for polymers like polyethylene and polyamides, can impact profit margins and pricing stability, with price volatility estimated to cause a 5-10% fluctuation in material costs annually. Stringent and evolving international certifications and regulatory approvals for specific applications, especially in offshore environments, can lead to extended product development cycles and market entry delays. Furthermore, intense competition from established players and emerging alternatives, such as spoolable composite pipes, necessitates continuous innovation and cost optimization to maintain market share.

Future Opportunities in Flexible Pipe Industry

The Flexible Pipe Industry is poised for significant future opportunities. The ongoing expansion of offshore oil and gas exploration into even deeper and more challenging environments will continue to drive demand. Emerging markets in regions like Africa and South America, with their untapped deepwater potential, present substantial growth avenues. Advancements in renewable energy infrastructure, such as offshore wind farms requiring subsea power and data cables, could open new application areas for specialized flexible pipes. Furthermore, the development of smart, self-monitoring flexible pipes integrated with IoT technology offers opportunities for value-added services and enhanced operational efficiency. Increased focus on sustainable solutions may also lead to the development of bio-based or recyclable materials for flexible pipes.

Major Players in the Flexible Pipe Industry Ecosystem

- Flexsteel Pipeline Technologies Inc

- National Oilwell Varco (NOV)

- Magma Global Ltd

- Chevron Phillips Chemical Company LLC

- SoulForce (Pipelife Nederland B V)

- The Prysmian Group

- GE Oil & Gas Corporation

- Shawcor Ltd

- ContiTech AG

- TechnipFMC PLC

- Airborne Oil & Gas BV

Key Developments in Flexible Pipe Industry Industry

- 2023/2024: Introduction of new generation HPHT flexible pipes with enhanced chemical resistance, enabling operations in increasingly challenging offshore reservoirs.

- 2022/2023: Increased adoption of spoolable composite pipes for specific onshore and shallow water applications, creating a competitive dynamic.

- 2021/2022: Strategic partnerships and acquisitions focused on expanding manufacturing capacity and geographical reach in key emerging markets.

- 2020/2021: Development of flexible pipes with integrated fiber optic sensing capabilities for real-time structural health monitoring.

- 2019/2020: Enhanced focus on sustainable material sourcing and manufacturing processes driven by growing environmental concerns.

Strategic Flexible Pipe Industry Market Forecast

The strategic Flexible Pipe Industry market forecast indicates sustained growth driven by the insatiable global demand for energy and the increasing necessity to tap into challenging deepwater reserves. Technological advancements in materials and manufacturing will continue to enhance the performance and cost-effectiveness of flexible pipes, making them indispensable for offshore operations. The growing emphasis on environmental compliance and operational safety further bolsters the demand for high-integrity flexible solutions. Emerging applications in renewable energy infrastructure and the potential for smart, integrated pipeline systems present significant future opportunities, promising a robust and evolving market landscape.

Flexible Pipe Industry Segmentation

-

1. Raw Material

- 1.1. High-density Polyethylene

- 1.2. Polyamides

- 1.3. Polyvinylidene Fluoride

- 1.4. Other Raw Materials

-

2. Application

-

2.1. Offshore

- 2.1.1. Deepwater

- 2.1.2. Ultra-deepwater

- 2.2. On shore

-

2.1. Offshore

Flexible Pipe Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Russia

- 2.3. Norway

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Malaysia

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of Latin America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. United Arab Emirates

- 6.2. Rest of Middle East

Flexible Pipe Industry Regional Market Share

Geographic Coverage of Flexible Pipe Industry

Flexible Pipe Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 5.1.1. High-density Polyethylene

- 5.1.2. Polyamides

- 5.1.3. Polyvinylidene Fluoride

- 5.1.4. Other Raw Materials

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Offshore

- 5.2.1.1. Deepwater

- 5.2.1.2. Ultra-deepwater

- 5.2.2. On shore

- 5.2.1. Offshore

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.3.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 6. Global Flexible Pipe Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 6.1.1. High-density Polyethylene

- 6.1.2. Polyamides

- 6.1.3. Polyvinylidene Fluoride

- 6.1.4. Other Raw Materials

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Offshore

- 6.2.1.1. Deepwater

- 6.2.1.2. Ultra-deepwater

- 6.2.2. On shore

- 6.2.1. Offshore

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 7. North America Flexible Pipe Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 7.1.1. High-density Polyethylene

- 7.1.2. Polyamides

- 7.1.3. Polyvinylidene Fluoride

- 7.1.4. Other Raw Materials

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Offshore

- 7.2.1.1. Deepwater

- 7.2.1.2. Ultra-deepwater

- 7.2.2. On shore

- 7.2.1. Offshore

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 8. Europe Flexible Pipe Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 8.1.1. High-density Polyethylene

- 8.1.2. Polyamides

- 8.1.3. Polyvinylidene Fluoride

- 8.1.4. Other Raw Materials

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Offshore

- 8.2.1.1. Deepwater

- 8.2.1.2. Ultra-deepwater

- 8.2.2. On shore

- 8.2.1. Offshore

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 9. Asia Pacific Flexible Pipe Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 9.1.1. High-density Polyethylene

- 9.1.2. Polyamides

- 9.1.3. Polyvinylidene Fluoride

- 9.1.4. Other Raw Materials

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Offshore

- 9.2.1.1. Deepwater

- 9.2.1.2. Ultra-deepwater

- 9.2.2. On shore

- 9.2.1. Offshore

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 10. Latin America Flexible Pipe Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 10.1.1. High-density Polyethylene

- 10.1.2. Polyamides

- 10.1.3. Polyvinylidene Fluoride

- 10.1.4. Other Raw Materials

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Offshore

- 10.2.1.1. Deepwater

- 10.2.1.2. Ultra-deepwater

- 10.2.2. On shore

- 10.2.1. Offshore

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 11. Middle East Flexible Pipe Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Raw Material

- 11.1.1. High-density Polyethylene

- 11.1.2. Polyamides

- 11.1.3. Polyvinylidene Fluoride

- 11.1.4. Other Raw Materials

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Offshore

- 11.2.1.1. Deepwater

- 11.2.1.2. Ultra-deepwater

- 11.2.2. On shore

- 11.2.1. Offshore

- 11.1. Market Analysis, Insights and Forecast - by Raw Material

- 12. Saudi Arabia Flexible Pipe Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Raw Material

- 12.1.1. High-density Polyethylene

- 12.1.2. Polyamides

- 12.1.3. Polyvinylidene Fluoride

- 12.1.4. Other Raw Materials

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Offshore

- 12.2.1.1. Deepwater

- 12.2.1.2. Ultra-deepwater

- 12.2.2. On shore

- 12.2.1. Offshore

- 12.1. Market Analysis, Insights and Forecast - by Raw Material

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Flexsteel Pipeline Technologies Inc *List Not Exhaustive

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 National Oilwell Varco (NOV)

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Magma Global Ltd

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Chevron Phillips Chemical Company LLC

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 SoulForce (Pipelife Nederland B V )

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 The Prysmian Group

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 GE Oil & Gas Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Shawcor Ltd

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 ContiTech AG

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 TechnipFMC PLC

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Airborne Oil & Gas BV

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 Flexsteel Pipeline Technologies Inc *List Not Exhaustive

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Flexible Pipe Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Flexible Pipe Industry Revenue (million), by Raw Material 2025 & 2033

- Figure 3: North America Flexible Pipe Industry Revenue Share (%), by Raw Material 2025 & 2033

- Figure 4: North America Flexible Pipe Industry Revenue (million), by Application 2025 & 2033

- Figure 5: North America Flexible Pipe Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Flexible Pipe Industry Revenue (million), by Country 2025 & 2033

- Figure 7: North America Flexible Pipe Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Flexible Pipe Industry Revenue (million), by Raw Material 2025 & 2033

- Figure 9: Europe Flexible Pipe Industry Revenue Share (%), by Raw Material 2025 & 2033

- Figure 10: Europe Flexible Pipe Industry Revenue (million), by Application 2025 & 2033

- Figure 11: Europe Flexible Pipe Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Flexible Pipe Industry Revenue (million), by Country 2025 & 2033

- Figure 13: Europe Flexible Pipe Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Flexible Pipe Industry Revenue (million), by Raw Material 2025 & 2033

- Figure 15: Asia Pacific Flexible Pipe Industry Revenue Share (%), by Raw Material 2025 & 2033

- Figure 16: Asia Pacific Flexible Pipe Industry Revenue (million), by Application 2025 & 2033

- Figure 17: Asia Pacific Flexible Pipe Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Flexible Pipe Industry Revenue (million), by Country 2025 & 2033

- Figure 19: Asia Pacific Flexible Pipe Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Flexible Pipe Industry Revenue (million), by Raw Material 2025 & 2033

- Figure 21: Latin America Flexible Pipe Industry Revenue Share (%), by Raw Material 2025 & 2033

- Figure 22: Latin America Flexible Pipe Industry Revenue (million), by Application 2025 & 2033

- Figure 23: Latin America Flexible Pipe Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Latin America Flexible Pipe Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Latin America Flexible Pipe Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Flexible Pipe Industry Revenue (million), by Raw Material 2025 & 2033

- Figure 27: Middle East Flexible Pipe Industry Revenue Share (%), by Raw Material 2025 & 2033

- Figure 28: Middle East Flexible Pipe Industry Revenue (million), by Application 2025 & 2033

- Figure 29: Middle East Flexible Pipe Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East Flexible Pipe Industry Revenue (million), by Country 2025 & 2033

- Figure 31: Middle East Flexible Pipe Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Saudi Arabia Flexible Pipe Industry Revenue (million), by Raw Material 2025 & 2033

- Figure 33: Saudi Arabia Flexible Pipe Industry Revenue Share (%), by Raw Material 2025 & 2033

- Figure 34: Saudi Arabia Flexible Pipe Industry Revenue (million), by Application 2025 & 2033

- Figure 35: Saudi Arabia Flexible Pipe Industry Revenue Share (%), by Application 2025 & 2033

- Figure 36: Saudi Arabia Flexible Pipe Industry Revenue (million), by Country 2025 & 2033

- Figure 37: Saudi Arabia Flexible Pipe Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 2: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 3: Global Flexible Pipe Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 5: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 6: Global Flexible Pipe Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 10: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Flexible Pipe Industry Revenue million Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Russia Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Norway Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Italy Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 18: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 19: Global Flexible Pipe Industry Revenue million Forecast, by Country 2020 & 2033

- Table 20: China Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: India Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Malaysia Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Asia Pacific Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 25: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 26: Global Flexible Pipe Industry Revenue million Forecast, by Country 2020 & 2033

- Table 27: Brazil Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Latin America Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 31: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Flexible Pipe Industry Revenue million Forecast, by Country 2020 & 2033

- Table 33: Global Flexible Pipe Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 34: Global Flexible Pipe Industry Revenue million Forecast, by Application 2020 & 2033

- Table 35: Global Flexible Pipe Industry Revenue million Forecast, by Country 2020 & 2033

- Table 36: United Arab Emirates Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East Flexible Pipe Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flexible Pipe Industry?

The projected CAGR is approximately 2.9%.

2. Which companies are prominent players in the Flexible Pipe Industry?

Key companies in the market include Flexsteel Pipeline Technologies Inc *List Not Exhaustive, National Oilwell Varco (NOV), Magma Global Ltd, Chevron Phillips Chemical Company LLC, SoulForce (Pipelife Nederland B V ), The Prysmian Group, GE Oil & Gas Corporation, Shawcor Ltd, ContiTech AG, TechnipFMC PLC, Airborne Oil & Gas BV.

3. What are the main segments of the Flexible Pipe Industry?

The market segments include Raw Material, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 181.5 million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Demand for Non-corrosive Pipes in Oil and Gas Industry; Technological Advances in Drilling Process.

6. What are the notable trends driving market growth?

Oil and Gas Industry to Drive the Market.

7. Are there any restraints impacting market growth?

; Fluctuating Oil Prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flexible Pipe Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flexible Pipe Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flexible Pipe Industry?

To stay informed about further developments, trends, and reports in the Flexible Pipe Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence