Key Insights

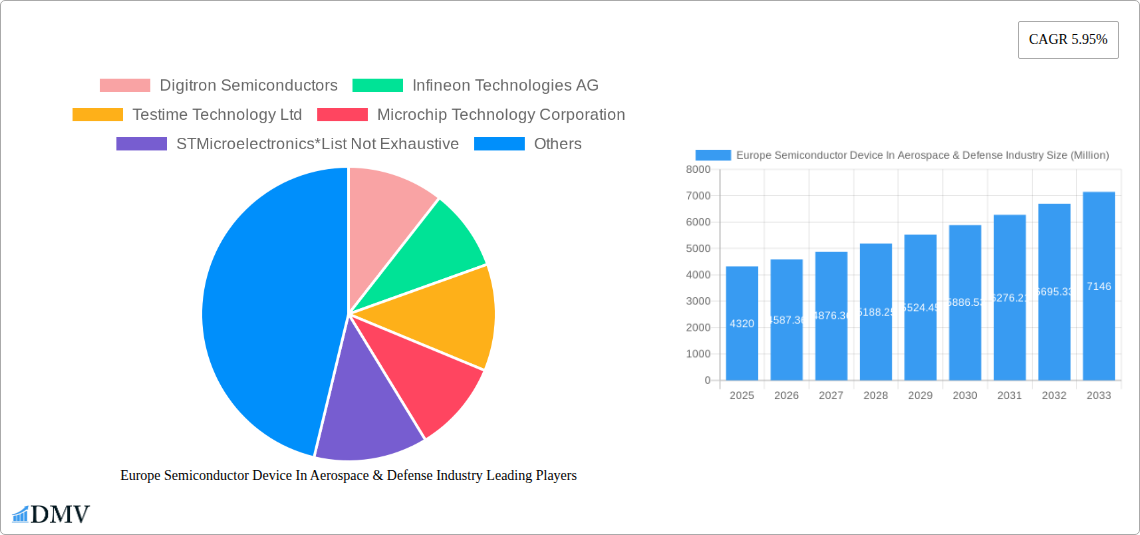

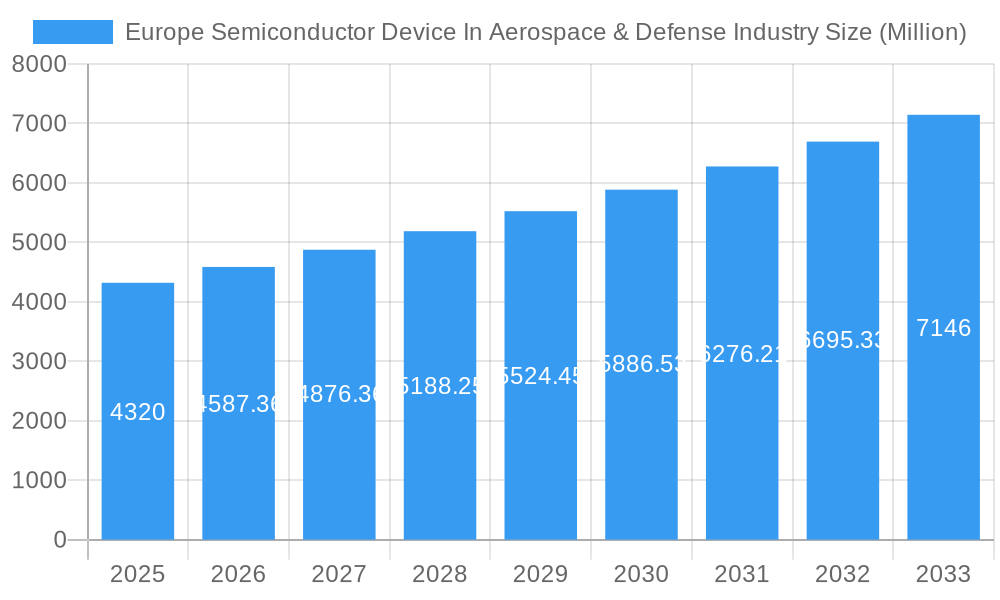

The European semiconductor device market within the aerospace and defense industry is poised for substantial growth, projected to be valued at €4.32 billion in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) of 5.95% from 2025 to 2033. This expansion is driven by several key factors. Firstly, increasing demand for advanced avionics and sophisticated weaponry systems necessitates the integration of high-performance semiconductors. Secondly, the ongoing technological advancements in areas such as artificial intelligence (AI), machine learning (ML), and sensor technology are creating new opportunities for semiconductor applications in aerospace and defense. This includes the development of more autonomous systems, improved situational awareness, and enhanced data processing capabilities. Furthermore, government initiatives focused on modernizing defense capabilities and investing in research and development contribute significantly to market growth. While supply chain disruptions and potential geopolitical uncertainties pose challenges, the long-term outlook remains positive, fueled by consistent technological innovation and persistent demand from both civilian and military sectors.

Europe Semiconductor Device In Aerospace & Defense Industry Market Size (In Billion)

Major market segments include discrete semiconductors, optoelectronics, sensors, and integrated circuits, with microprocessors, microcontrollers, and digital signal processors representing key micro-component categories. Germany, France, and the United Kingdom are the leading national markets within Europe, benefiting from established aerospace and defense industries. The competitive landscape is characterized by a mix of established players like Infineon Technologies AG, STMicroelectronics, Texas Instruments Incorporated, and NXP Semiconductors, alongside specialized companies catering to the niche demands of the aerospace and defense sector. These companies are continuously investing in research and development to offer innovative products that meet the stringent reliability and performance requirements of this demanding market. The future growth trajectory is likely to be influenced by factors such as the adoption of advanced materials, miniaturization technologies, and the increasing focus on cybersecurity within these critical applications.

Europe Semiconductor Device In Aerospace & Defense Industry Company Market Share

Europe Semiconductor Device in Aerospace & Defense Industry Market: 2019-2033 Forecast

This comprehensive report provides a detailed analysis of the European semiconductor device market within the aerospace and defense sectors, offering invaluable insights for stakeholders from 2019 to 2033. We delve into market size, growth drivers, competitive landscape, and future opportunities, equipping you with the knowledge to navigate this dynamic industry. The report covers a study period of 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The historical period analyzed is 2019-2024. The market is projected to reach xx Million by 2033.

Europe Semiconductor Device In Aerospace & Defense Industry Market Composition & Trends

This section analyzes the market's competitive dynamics, innovation drivers, regulatory environment, and end-user profiles. We examine market concentration, identifying key players and their market share distribution. The report also details significant M&A activities, including deal values, and assesses the impact of substitute products on market growth. The European aerospace and defense semiconductor market is characterized by a moderately concentrated landscape, with key players such as Infineon Technologies AG, STMicroelectronics, and Texas Instruments Incorporated holding significant market share. However, the presence of numerous smaller specialized firms contributes to a dynamic and competitive environment.

- Market Concentration: Infineon Technologies AG holds an estimated xx% market share in 2025, followed by STMicroelectronics at xx% and Texas Instruments at xx%. The remaining market share is distributed among numerous smaller players.

- Innovation Catalysts: Government funding initiatives and the increasing demand for advanced functionalities in aerospace and defense applications are driving innovation.

- Regulatory Landscape: Stringent quality and safety standards within the aerospace and defense sector influence technology adoption and supplier selection. Compliance with regulations like those from the European Aviation Safety Agency (EASA) is paramount.

- Substitute Products: The emergence of alternative technologies like GaN and SiC presents both opportunities and challenges for traditional semiconductor materials.

- End-User Profiles: The primary end-users are Original Equipment Manufacturers (OEMs) in the aerospace and defense industries, with a diverse range of needs depending on the specific application.

- M&A Activities: Recent M&A activities, such as the acquisition of SET GmbH by NI (National Instruments) in March 2023 (USD xx Million estimated deal value), indicate strategic consolidation and technological advancements within the sector.

Europe Semiconductor Device In Aerospace & Defense Industry Industry Evolution

This section explores the evolution of the European aerospace and defense semiconductor market, examining growth trajectories, technological advancements, and shifting consumer demands. We analyze historical data and forecast future trends, providing detailed information on market growth rates and technology adoption metrics. The market has witnessed substantial growth driven by the increasing adoption of advanced technologies in aerospace and defense systems. The shift towards electric and autonomous aircraft, coupled with the rising demand for improved performance, reliability, and miniaturization, are key factors driving market expansion. Annual growth rates are estimated to be xx% between 2025 and 2033, driven by several factors: The integration of advanced semiconductor technologies such as SiC and GaN is expected to accelerate, resulting in lighter, more efficient aircraft systems. The increasing demand for improved sensor technology and connectivity, particularly within the context of IoT and autonomous systems, presents a significant growth opportunity.

Leading Regions, Countries, or Segments in Europe Semiconductor Device In Aerospace & Defense Industry

This section identifies the dominant regions, countries, and segments within the European semiconductor device market for aerospace and defense. We provide a detailed analysis of the key factors driving the dominance of specific regions and segments, including investment trends and regulatory support.

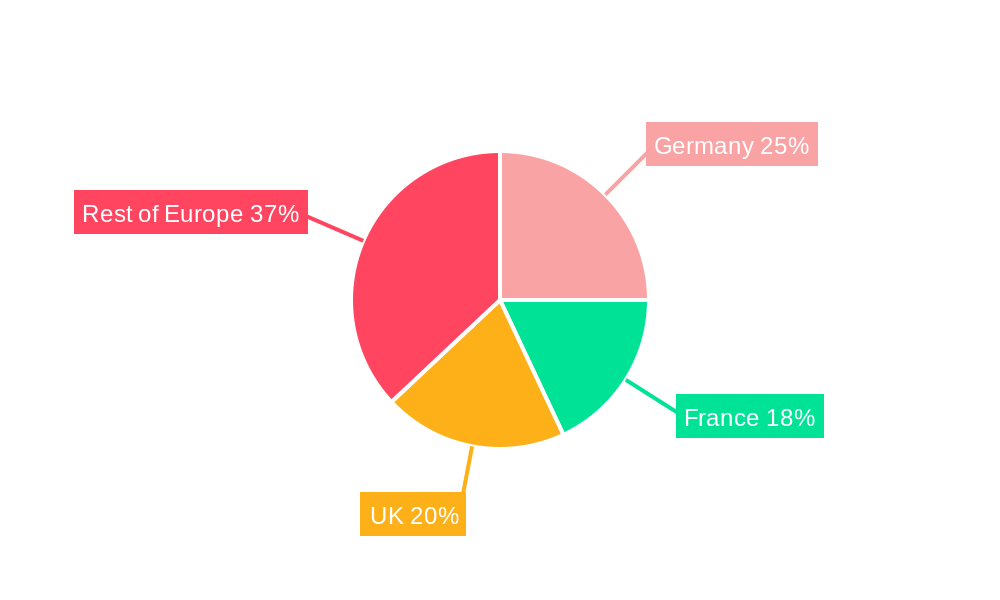

Leading Countries: The United Kingdom and Germany are currently leading the market, driven by strong government support and a robust aerospace and defense industrial base. France is also a significant contributor. The Rest of Europe segment shows promising growth potential.

Key Drivers:

- United Kingdom: Significant government investment in aerospace technology, as evidenced by the GBP 113.6 million (USD 136 million) funding for electric aircraft development in February 2023.

- Germany: Strong presence of established semiconductor manufacturers and a robust automotive industry which is increasingly collaborating with the aerospace sector.

- France: Significant investments in national defense and a growing aerospace industry contributing to the demand for advanced semiconductor solutions.

Leading Device Types: Integrated circuits (ICs) dominate the market due to their versatile applications in avionics, communication, and guidance systems. Microprocessors, microcontrollers, and digital signal processors (DSPs) are also key segments, with continuous demand for higher performance and computing capabilities. The growing importance of sensors in various applications, from flight control to environmental monitoring, is boosting the optoelectronics and sensor segments.

Europe Semiconductor Device In Aerospace & Defense Industry Product Innovations

Recent innovations focus on enhancing performance, reducing size and weight, and improving reliability in harsh environments. The increasing use of GaN and SiC is improving power efficiency and thermal management, while advancements in miniaturization allow for more compact and powerful systems. New integrated circuits with enhanced processing capabilities and improved radiation hardness are also driving innovation in the aerospace and defense sectors. These advancements cater to the growing demand for smaller, lighter, and more efficient systems with improved performance and extended operational life.

Propelling Factors for Europe Semiconductor Device In Aerospace & Defense Industry Growth

Several factors are driving growth within this market. Firstly, technological advancements, including the adoption of GaN and SiC, lead to greater efficiency and improved performance in aerospace and defense systems. Secondly, significant government investment and supportive regulatory environments are creating a favorable climate for industry expansion. Finally, the increasing demand for enhanced functionalities, such as advanced sensor technologies and improved connectivity, are pushing market growth.

Obstacles in the Europe Semiconductor Device In Aerospace & Defense Industry Market

The market faces certain challenges. Supply chain disruptions can impact production and delivery timelines, causing delays and increasing costs. Furthermore, the stringent regulatory landscape necessitates significant investment in testing and certification, increasing time to market. Finally, intense competition, particularly from established players, can limit profitability and market share for smaller companies.

Future Opportunities in Europe Semiconductor Device In Aerospace & Defense Industry

Future opportunities reside in emerging technologies, such as AI and machine learning, which will enable advanced autonomous systems and improve situational awareness. The increasing adoption of electric and hydrogen-powered aircraft is also opening up new avenues for semiconductor manufacturers, requiring the development of specialized components for these propulsion systems. Furthermore, the expanding global defense budgets indicate a sustained demand for advanced semiconductor solutions in this sector.

Major Players in the Europe Semiconductor Device In Aerospace & Defense Industry Ecosystem

Key Developments in Europe Semiconductor Device In Aerospace & Defense Industry Industry

February 2023: The UK government announced GBP 113.6 million (USD 136 million) in funding for electric and hydrogen aircraft development, boosting the demand for related semiconductor devices. This significantly impacts the market by creating new opportunities for companies specializing in power electronics and sensor technology.

March 2023: NI's acquisition of SET GmbH strengthens the capabilities for testing and reliability assessment of semiconductors used in aerospace and defense applications. This positively impacts the market by accelerating the adoption of new materials like SiC and GaN, ultimately shortening the time to market for advanced technologies.

Strategic Europe Semiconductor Device In Aerospace & Defense Industry Market Forecast

The European semiconductor device market for aerospace and defense is poised for sustained growth, driven by increasing demand for advanced technologies, government investments, and the ongoing shift towards more sophisticated and autonomous systems. The market is expected to experience significant expansion throughout the forecast period, with continuous innovation and technological advancements solidifying its position as a critical component of the aerospace and defense industries. Opportunities abound for companies that can offer cutting-edge solutions to meet the stringent requirements of the sector.

Europe Semiconductor Device In Aerospace & Defense Industry Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

-

1.4.4. Micro

- 1.4.4.1. Microprocessor

- 1.4.4.2. Microcontroller

- 1.4.4.3. Digital Signal Processors

Europe Semiconductor Device In Aerospace & Defense Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Semiconductor Device In Aerospace & Defense Industry Regional Market Share

Geographic Coverage of Europe Semiconductor Device In Aerospace & Defense Industry

Europe Semiconductor Device In Aerospace & Defense Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.95% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro

- 5.1.4.4.1. Microprocessor

- 5.1.4.4.2. Microcontroller

- 5.1.4.4.3. Digital Signal Processors

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Europe Semiconductor Device In Aerospace & Defense Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. Discrete Semiconductors

- 6.1.2. Optoelectronics

- 6.1.3. Sensors

- 6.1.4. Integrated Circuits

- 6.1.4.1. Analog

- 6.1.4.2. Logic

- 6.1.4.3. Memory

- 6.1.4.4. Micro

- 6.1.4.4.1. Microprocessor

- 6.1.4.4.2. Microcontroller

- 6.1.4.4.3. Digital Signal Processors

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Digitron Semiconductors

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Infineon Technologies AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Testime Technology Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Microchip Technology Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 STMicroelectronics*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 SEMICOA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Skyworks Solutions Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 NXP Semiconductors

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Texas Instruments Incorporated

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Teledyne Technologies

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Digitron Semiconductors

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Semiconductor Device In Aerospace & Defense Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Semiconductor Device In Aerospace & Defense Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 2: Europe Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Europe Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 4: Europe Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: France Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Semiconductor Device In Aerospace & Defense Industry?

The projected CAGR is approximately 5.95%.

2. Which companies are prominent players in the Europe Semiconductor Device In Aerospace & Defense Industry?

Key companies in the market include Digitron Semiconductors, Infineon Technologies AG, Testime Technology Ltd, Microchip Technology Corporation, STMicroelectronics*List Not Exhaustive, SEMICOA, Skyworks Solutions Inc, NXP Semiconductors, Texas Instruments Incorporated, Teledyne Technologies.

3. What are the main segments of the Europe Semiconductor Device In Aerospace & Defense Industry?

The market segments include Device Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.32 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing government spending on space technology and modernizing the Defense industry; Increasing global issues like climate and biodiversity crises.

6. What are the notable trends driving market growth?

Sensors Segment to Grow Significantly.

7. Are there any restraints impacting market growth?

Limited Supply of Semiconductors.

8. Can you provide examples of recent developments in the market?

March 2023: NI (National Instruments) revealed the acquisition of SET GmbH, renowned experts in aerospace and defense test systems development, and recent pioneers in electrical reliability testing for semiconductors. This strategic move aims to expedite the introduction of critical, uniquely advanced solutions and promote the integration of power electronic materials like silicon carbide (SiC) and gallium nitride (GaN) across the semiconductor-to-transportation supply chain, ultimately reducing time to market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Semiconductor Device In Aerospace & Defense Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Semiconductor Device In Aerospace & Defense Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Semiconductor Device In Aerospace & Defense Industry?

To stay informed about further developments, trends, and reports in the Europe Semiconductor Device In Aerospace & Defense Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence