Key Insights

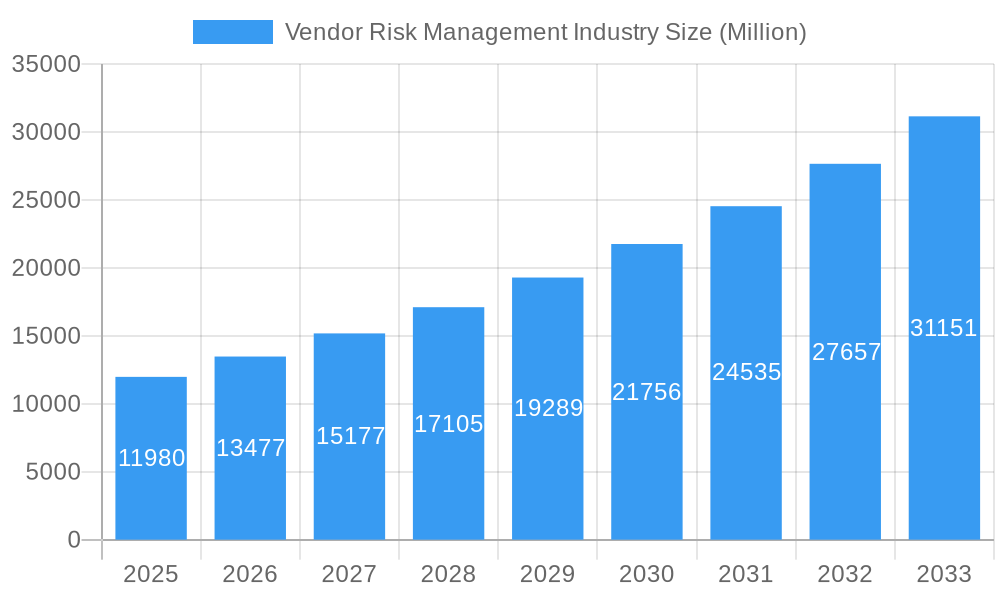

The Vendor Risk Management (VRM) market is experiencing robust expansion, projected to reach a substantial USD 11.98 billion in value with a compelling Compound Annual Growth Rate (CAGR) exceeding 12.50% throughout the forecast period of 2025-2033. This significant growth is propelled by a confluence of critical drivers. Increasing regulatory scrutiny across industries, coupled with the escalating sophistication and frequency of cyber threats, are compelling organizations to adopt comprehensive VRM solutions to safeguard sensitive data and ensure business continuity. The growing interconnectedness of supply chains further amplifies the need for robust vendor assessment and ongoing monitoring. Moreover, the recognition of VRM as a strategic imperative for maintaining brand reputation and fostering stakeholder trust is a key enabler of market momentum.

Vendor Risk Management Industry Market Size (In Billion)

The VRM landscape is characterized by dynamic trends, including a pronounced shift towards cloud-based deployment models, offering greater scalability, flexibility, and cost-effectiveness. The market is also witnessing a surge in demand for advanced solutions such as AI-powered risk assessment, continuous monitoring, and automated compliance checks, enabling proactive identification and mitigation of potential vendor-related risks. While the market exhibits strong growth, certain restraints such as the initial cost of implementation and the need for skilled personnel to manage complex VRM programs may pose challenges. However, the overwhelming benefits of enhanced security, regulatory adherence, and operational resilience are driving widespread adoption across diverse industry verticals like BFSI, Healthcare, and Manufacturing, with Small and Medium-sized Enterprises (SMEs) increasingly recognizing the value proposition.

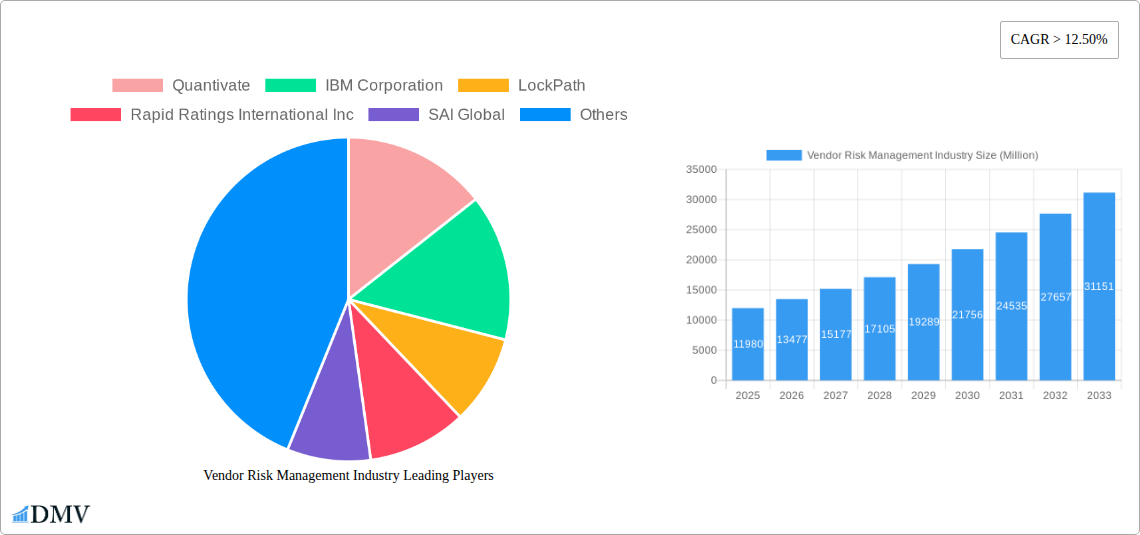

Vendor Risk Management Industry Company Market Share

This in-depth report, "Vendor Risk Management Industry: Market Composition, Trends, and Future Outlook," provides unparalleled insights into the dynamic global Vendor Risk Management (VRM) market. Spanning the historical period of 2019–2024, the base year 2025, and a robust forecast period of 2025–2033, this analysis empowers stakeholders with strategic intelligence. We dissect market composition, analyze industry evolution, and pinpoint leading segments and regions, offering a clear roadmap for navigating the complexities of third-party risk. With a focus on key players like Quantivate, IBM Corporation, LockPath, Rapid Ratings International Inc, SAI Global, MetricStream, Resolver Inc, Optiv Security Inc, RSA Security LLC, and Genpact Limited, and an exploration of critical segments including Solutions (Vendor Information Management, Quality Assurance Management, Financial Control, Compliance Management, Audit Management, Contract Management), Services, Deployment Types (On-Premises, Cloud), Organization Sizes (SMEs, Large Enterprises), and Industry Verticals (BFSI, Telecom & IT, Manufacturing, Government, Healthcare), this report is an essential resource for optimizing vendor risk management strategies, enhancing supply chain security, and ensuring regulatory compliance.

Vendor Risk Management Industry Market Composition & Trends

The Vendor Risk Management industry is characterized by a moderately consolidated market structure, driven by increasing regulatory scrutiny and the escalating sophistication of cyber threats. Innovation catalysts, such as the integration of artificial intelligence (AI) and machine learning (ML) into VRM platforms, are reshaping how organizations assess and mitigate risks. The global regulatory landscape, with mandates focusing on data privacy and third-party risk management, continues to be a significant driver for VRM adoption. While substitute products exist in the form of manual processes and fragmented solutions, the market is rapidly shifting towards integrated VRM platforms offering comprehensive risk assessment and compliance management. End-user profiles increasingly demand automated workflows, real-time risk intelligence, and streamlined onboarding processes for vendors. Merger and acquisition (M&A) activities are prevalent, with notable deals demonstrating the strategic importance of acquiring advanced VRM capabilities. For instance, the Certa funding round of USD 35 Million highlights the significant investment in AI-driven policy conversion for enhanced vendor lifecycle management.

- Market Share Distribution: While specific figures are proprietary, leading solutions providers are capturing significant market share through feature-rich platforms and strategic partnerships.

- M&A Deal Values: Industry reports indicate M&A deals in the hundreds of millions of dollars, signaling high strategic value placed on VRM capabilities.

- Innovation Trends: Focus on AI for automated policy analysis, predictive risk modeling, and enhanced vendor due diligence.

- Regulatory Impact: Continuous evolution of data protection laws (e.g., GDPR, CCPA) and industry-specific regulations driving VRM adoption.

Vendor Risk Management Industry Industry Evolution

The Vendor Risk Management industry has undergone a significant transformation, evolving from basic vendor onboarding and compliance checks to sophisticated, proactive third-party risk management programs. This evolution is marked by a consistent upward trajectory in market growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 15-20% over the forecast period. Technological advancements have been pivotal, with the integration of AI and ML revolutionizing the efficiency and accuracy of risk assessments. The introduction of SaaS-based VRM solutions, such as Vanta's recent offering, underscores the shift towards cloud-native, automated platforms that streamline security reviews and compliance workflows. This technological leap allows for more granular insights into vendor vulnerabilities, enabling organizations to move beyond reactive measures to predictive risk mitigation. Shifting consumer demands, influenced by high-profile data breaches and increasing stakeholder expectations for ESG (Environmental, Social, and Governance) compliance, have further propelled the industry forward. Businesses are no longer content with simply identifying risks; they demand robust solutions that offer continuous monitoring, automated remediation, and comprehensive audit trails. The market has seen a substantial increase in adoption rates, with an estimated 75% of large enterprises and 50% of medium-sized businesses either having implemented or actively planning to implement advanced VRM solutions within the next three years. This surge in demand is driven by the critical need to protect sensitive data, maintain business continuity, and safeguard brand reputation in an increasingly interconnected and risk-prone global economy. The ability to manage the entire vendor lifecycle, from initial vetting and contract management to ongoing performance monitoring and offboarding, within a single, integrated platform is now a key differentiator.

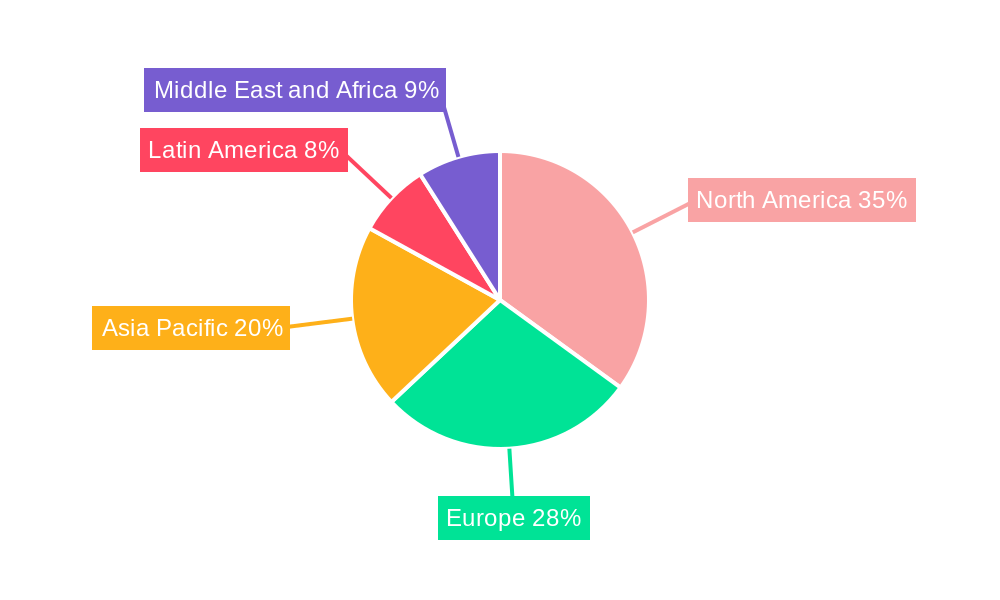

Leading Regions, Countries, or Segments in Vendor Risk Management Industry

North America currently dominates the Vendor Risk Management industry landscape, driven by a mature regulatory environment, a high concentration of large enterprises, and a proactive approach to cybersecurity. The United States, in particular, leads in VRM adoption, fueled by stringent financial regulations and a robust technology sector. However, the Asia-Pacific region is emerging as a significant growth market, with countries like China and India rapidly increasing their investments in vendor risk mitigation due to expanding digital ecosystems and growing awareness of cyber threats.

Within segment analysis, Solutions are the primary market driver, accounting for an estimated 70% of the overall market revenue. Within solutions, Vendor Information Management and Compliance Management are the most sought-after sub-segments, reflecting the fundamental need for organized vendor data and adherence to diverse regulatory frameworks. Services, including consulting, implementation, and managed VRM, represent the remaining 30% of the market.

Deployment types show a clear preference for Cloud-based VRM solutions, which are projected to capture over 80% of the market by 2033, owing to their scalability, flexibility, and cost-effectiveness compared to On-Premises deployments.

In terms of organization size, Large Enterprises constitute the largest customer base, with an estimated 65% market share, due to their complex supply chains and higher risk exposure. However, the adoption rate among Small and Medium-Sized Enterprises (SMEs) is growing rapidly, driven by the availability of more affordable and user-friendly VRM solutions.

The Banking, Financial Services, and Insurance (BFSI) sector remains the dominant industry vertical, representing approximately 40% of the VRM market. This is attributed to the highly regulated nature of the industry and the immense value of the data handled. The Telecom and IT sector follows closely, with increasing reliance on third-party services making robust VRM crucial for security and compliance.

- Dominant Region: North America, followed by Europe.

- Emerging Markets: Asia-Pacific, driven by digital transformation and increasing cyber risk awareness.

- Leading Segment (Type): Solutions (Vendor Information Management, Compliance Management).

- Deployment Preference: Cloud (projected to exceed 80% by 2033).

- Key Organization Size: Large Enterprises, with rapid growth in SMEs.

- Primary Industry Vertical: BFSI, followed by Telecom & IT.

Vendor Risk Management Industry Product Innovations

Product innovations in the Vendor Risk Management industry are relentlessly focused on automation, intelligence, and integration. Leading platforms are now incorporating advanced AI and ML algorithms to perform predictive risk analytics, automatically identify anomalies in vendor behavior, and generate actionable insights. Real-time monitoring capabilities have been significantly enhanced, allowing for continuous assessment of vendor security posture and compliance status. Furthermore, innovations in natural language processing (NLP) are enabling platforms to analyze unstructured data from contracts and policies, translating complex legal and compliance jargon into actionable workflows. The development of robust APIs and pre-built integrations with other critical business systems, such as CRM, ERP, and cybersecurity tools, is a key differentiator, enabling a holistic view of risk across the enterprise. These advancements are not just about feature enhancement; they are about fundamentally transforming the vendor risk management process from a manual, labor-intensive task into an intelligent, automated, and proactive discipline, significantly reducing the time and resources required for vendor due diligence and ongoing oversight.

Propelling Factors for Vendor Risk Management Industry Growth

The Vendor Risk Management industry is propelled by a confluence of powerful factors. The ever-increasing sophistication and frequency of cyberattacks, targeting vulnerabilities within an organization's extended supply chain, are a primary driver. Regulatory bodies worldwide are imposing stricter mandates for data protection and third-party risk accountability, compelling businesses to invest in robust VRM solutions. The digital transformation initiatives across industries, leading to a greater reliance on external vendors and cloud services, inherently expand the attack surface, necessitating comprehensive vendor risk assessment. Furthermore, the growing emphasis on ESG compliance requires organizations to assess the environmental and social practices of their vendors, adding another layer of complexity and demand for VRM. Economic pressures also play a role, as efficient VRM can prevent costly data breaches and ensure business continuity, thereby safeguarding financial stability.

- Cybersecurity Imperative: Rising threat landscape and sophisticated attacks.

- Regulatory Compliance: Stringent data protection laws and industry-specific mandates.

- Digital Transformation: Increased reliance on third-party services and cloud adoption.

- ESG Demands: Growing scrutiny of vendor environmental, social, and governance practices.

- Economic Resilience: Preventing breach costs and ensuring business continuity.

Obstacles in the Vendor Risk Management Industry Market

Despite the robust growth, the Vendor Risk Management industry faces several significant obstacles. The sheer volume and complexity of third-party relationships can overwhelm even advanced systems, making comprehensive vendor due diligence a persistent challenge. Regulatory fragmentation across different jurisdictions adds layers of complexity for global organizations, requiring constant adaptation of VRM strategies. The cost of implementing and maintaining sophisticated VRM solutions, particularly for SMEs, can be prohibitive. Furthermore, the lack of standardized metrics and consistent data quality from vendors can hinder accurate risk assessment. Finally, a skills gap in cybersecurity and risk management professionals capable of effectively leveraging advanced VRM technologies presents a human resource challenge that can slow down adoption and effective utilization.

- Scalability Challenges: Managing vast and complex vendor ecosystems.

- Regulatory Nuances: Navigating diverse and evolving compliance landscapes.

- Implementation Costs: High upfront and ongoing investment in VRM solutions.

- Data Inconsistency: Vendor-provided data quality and standardization issues.

- Talent Shortage: Lack of skilled professionals in VRM and cybersecurity.

Future Opportunities in Vendor Risk Management Industry

The future of the Vendor Risk Management industry is ripe with opportunities. The continued advancements in AI and ML will unlock new avenues for predictive risk intelligence and automated remediation, moving VRM towards a self-healing security model. The growing demand for integrated supply chain risk management solutions presents a significant expansion opportunity, where VRM becomes a core component of a broader resilience strategy. As the ESG landscape matures, there will be a greater demand for VRM solutions that can effectively assess and report on vendor sustainability practices. The burgeoning IoT (Internet of Things) ecosystem will introduce new classes of vendor risks, requiring specialized VRM capabilities. Furthermore, the increasing adoption of VRM by SMEs, driven by affordable SaaS offerings and a heightened awareness of cyber threats, represents a substantial untapped market segment.

- AI-Powered Predictive Analytics: Enhancing proactive risk identification.

- Integrated Supply Chain Resilience: VRM as a component of holistic risk management.

- ESG Risk Assessment: Growing demand for sustainability-focused VRM.

- IoT Vendor Risk: Addressing emerging threats from connected devices.

- SME Market Expansion: Tapping into the growing needs of smaller businesses.

Major Players in the Vendor Risk Management Industry Ecosystem

- Quantivate

- IBM Corporation

- LockPath

- Rapid Ratings International Inc

- SAI Global

- MetricStream

- Resolver Inc

- Optiv Security Inc

- RSA Security LLC

- Genpact Limited

Key Developments in Vendor Risk Management Industry Industry

- September 2023: Certa, a third-party management platform, raised USD 35 Million to invest in artificial intelligence. This AI integration focuses on converting text-based policies (ESG, legal, compliance, procurement) into controlled workflows, streamlining integration with third-party tools and enabling customers to reduce vendor management team size and accelerate third-party onboarding.

- May 2023: Vanta, a SaaS-based security and compliance solution provider, launched a Vendor Risk Management (VRM) offering. This new VRM solution is designed to streamline third-party security with automated workflows for vendor security reviews and compliance, consolidating the entire vendor management process into a single, automated workflow with necessary integrations for applications, identity providers, and database systems.

Strategic Vendor Risk Management Industry Market Forecast

The strategic Vendor Risk Management industry market forecast indicates sustained and robust growth, propelled by the persistent evolution of cyber threats and the unwavering demand for regulatory compliance. The increasing adoption of AI and ML will further automate and enhance the accuracy of risk assessment and mitigation, creating more intelligent and proactive VRM ecosystems. The expansion into managing ESG risks and the complexities introduced by the IoT will open new market frontiers. Consequently, the market is poised for significant expansion, with projections suggesting substantial growth in both cloud-based solutions and specialized services catering to the evolving needs of businesses seeking to build resilient and secure supply chains in an increasingly interconnected world. The strategic imperative to safeguard sensitive data and maintain operational continuity will continue to drive investment in advanced vendor risk management capabilities.

Vendor Risk Management Industry Segmentation

-

1. Type

-

1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 1.1.1. Vendor Information Management

- 1.1.2. Quality Assurance Management

- 1.1.3. Financial Control

- 1.1.4. Compliance Management

- 1.1.5. Audit Management

- 1.1.6. Contract Management and Others

- 1.2. Services

-

1.1. Solutions (Qualitative Analysis for Sub-Segments)

-

2. Deployment Type

- 2.1. On-Premises

- 2.2. Cloud

-

3. Organization Size

- 3.1. Small and Medium-Sized Enterprises

- 3.2. Large Enterprises

-

4. Industry Vertical

- 4.1. Banking, Financial Services, and Insurance

- 4.2. Telecom and IT

- 4.3. Manufacturing

- 4.4. Government

- 4.5. Healthcare

- 4.6. Others (

Vendor Risk Management Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Vendor Risk Management Industry Regional Market Share

Geographic Coverage of Vendor Risk Management Industry

Vendor Risk Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 12.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Need for the Efficient Management of Complex Vendor Ecosystems; View the Risk Levels Associated With Various Tasks

- 3.3. Market Restrains

- 3.3.1. Dependence on Non-Formal and Manual Processes By Many Organizations

- 3.4. Market Trends

- 3.4.1. BFSI is Expected to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Vendor Risk Management Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 5.1.1.1. Vendor Information Management

- 5.1.1.2. Quality Assurance Management

- 5.1.1.3. Financial Control

- 5.1.1.4. Compliance Management

- 5.1.1.5. Audit Management

- 5.1.1.6. Contract Management and Others

- 5.1.2. Services

- 5.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 5.2. Market Analysis, Insights and Forecast - by Deployment Type

- 5.2.1. On-Premises

- 5.2.2. Cloud

- 5.3. Market Analysis, Insights and Forecast - by Organization Size

- 5.3.1. Small and Medium-Sized Enterprises

- 5.3.2. Large Enterprises

- 5.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.4.1. Banking, Financial Services, and Insurance

- 5.4.2. Telecom and IT

- 5.4.3. Manufacturing

- 5.4.4. Government

- 5.4.5. Healthcare

- 5.4.6. Others (

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Vendor Risk Management Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 6.1.1.1. Vendor Information Management

- 6.1.1.2. Quality Assurance Management

- 6.1.1.3. Financial Control

- 6.1.1.4. Compliance Management

- 6.1.1.5. Audit Management

- 6.1.1.6. Contract Management and Others

- 6.1.2. Services

- 6.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 6.2. Market Analysis, Insights and Forecast - by Deployment Type

- 6.2.1. On-Premises

- 6.2.2. Cloud

- 6.3. Market Analysis, Insights and Forecast - by Organization Size

- 6.3.1. Small and Medium-Sized Enterprises

- 6.3.2. Large Enterprises

- 6.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.4.1. Banking, Financial Services, and Insurance

- 6.4.2. Telecom and IT

- 6.4.3. Manufacturing

- 6.4.4. Government

- 6.4.5. Healthcare

- 6.4.6. Others (

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Vendor Risk Management Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 7.1.1.1. Vendor Information Management

- 7.1.1.2. Quality Assurance Management

- 7.1.1.3. Financial Control

- 7.1.1.4. Compliance Management

- 7.1.1.5. Audit Management

- 7.1.1.6. Contract Management and Others

- 7.1.2. Services

- 7.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 7.2. Market Analysis, Insights and Forecast - by Deployment Type

- 7.2.1. On-Premises

- 7.2.2. Cloud

- 7.3. Market Analysis, Insights and Forecast - by Organization Size

- 7.3.1. Small and Medium-Sized Enterprises

- 7.3.2. Large Enterprises

- 7.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 7.4.1. Banking, Financial Services, and Insurance

- 7.4.2. Telecom and IT

- 7.4.3. Manufacturing

- 7.4.4. Government

- 7.4.5. Healthcare

- 7.4.6. Others (

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Vendor Risk Management Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 8.1.1.1. Vendor Information Management

- 8.1.1.2. Quality Assurance Management

- 8.1.1.3. Financial Control

- 8.1.1.4. Compliance Management

- 8.1.1.5. Audit Management

- 8.1.1.6. Contract Management and Others

- 8.1.2. Services

- 8.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 8.2. Market Analysis, Insights and Forecast - by Deployment Type

- 8.2.1. On-Premises

- 8.2.2. Cloud

- 8.3. Market Analysis, Insights and Forecast - by Organization Size

- 8.3.1. Small and Medium-Sized Enterprises

- 8.3.2. Large Enterprises

- 8.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 8.4.1. Banking, Financial Services, and Insurance

- 8.4.2. Telecom and IT

- 8.4.3. Manufacturing

- 8.4.4. Government

- 8.4.5. Healthcare

- 8.4.6. Others (

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Latin America Vendor Risk Management Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 9.1.1.1. Vendor Information Management

- 9.1.1.2. Quality Assurance Management

- 9.1.1.3. Financial Control

- 9.1.1.4. Compliance Management

- 9.1.1.5. Audit Management

- 9.1.1.6. Contract Management and Others

- 9.1.2. Services

- 9.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 9.2. Market Analysis, Insights and Forecast - by Deployment Type

- 9.2.1. On-Premises

- 9.2.2. Cloud

- 9.3. Market Analysis, Insights and Forecast - by Organization Size

- 9.3.1. Small and Medium-Sized Enterprises

- 9.3.2. Large Enterprises

- 9.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 9.4.1. Banking, Financial Services, and Insurance

- 9.4.2. Telecom and IT

- 9.4.3. Manufacturing

- 9.4.4. Government

- 9.4.5. Healthcare

- 9.4.6. Others (

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Vendor Risk Management Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 10.1.1.1. Vendor Information Management

- 10.1.1.2. Quality Assurance Management

- 10.1.1.3. Financial Control

- 10.1.1.4. Compliance Management

- 10.1.1.5. Audit Management

- 10.1.1.6. Contract Management and Others

- 10.1.2. Services

- 10.1.1. Solutions (Qualitative Analysis for Sub-Segments)

- 10.2. Market Analysis, Insights and Forecast - by Deployment Type

- 10.2.1. On-Premises

- 10.2.2. Cloud

- 10.3. Market Analysis, Insights and Forecast - by Organization Size

- 10.3.1. Small and Medium-Sized Enterprises

- 10.3.2. Large Enterprises

- 10.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 10.4.1. Banking, Financial Services, and Insurance

- 10.4.2. Telecom and IT

- 10.4.3. Manufacturing

- 10.4.4. Government

- 10.4.5. Healthcare

- 10.4.6. Others (

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Quantivate

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 IBM Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 LockPath

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Rapid Ratings International Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SAI Global

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MetricStream

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Resolver Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Optiv Security Inc *List Not Exhaustive

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 RSA Security LLC

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Genpact Limited

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Quantivate

List of Figures

- Figure 1: Global Vendor Risk Management Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Vendor Risk Management Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Vendor Risk Management Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Vendor Risk Management Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 5: North America Vendor Risk Management Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 6: North America Vendor Risk Management Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 7: North America Vendor Risk Management Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 8: North America Vendor Risk Management Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 9: North America Vendor Risk Management Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 10: North America Vendor Risk Management Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Vendor Risk Management Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Vendor Risk Management Industry Revenue (Million), by Type 2025 & 2033

- Figure 13: Europe Vendor Risk Management Industry Revenue Share (%), by Type 2025 & 2033

- Figure 14: Europe Vendor Risk Management Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 15: Europe Vendor Risk Management Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 16: Europe Vendor Risk Management Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 17: Europe Vendor Risk Management Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 18: Europe Vendor Risk Management Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 19: Europe Vendor Risk Management Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 20: Europe Vendor Risk Management Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Vendor Risk Management Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Vendor Risk Management Industry Revenue (Million), by Type 2025 & 2033

- Figure 23: Asia Pacific Vendor Risk Management Industry Revenue Share (%), by Type 2025 & 2033

- Figure 24: Asia Pacific Vendor Risk Management Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 25: Asia Pacific Vendor Risk Management Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 26: Asia Pacific Vendor Risk Management Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 27: Asia Pacific Vendor Risk Management Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 28: Asia Pacific Vendor Risk Management Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 29: Asia Pacific Vendor Risk Management Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 30: Asia Pacific Vendor Risk Management Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Vendor Risk Management Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Vendor Risk Management Industry Revenue (Million), by Type 2025 & 2033

- Figure 33: Latin America Vendor Risk Management Industry Revenue Share (%), by Type 2025 & 2033

- Figure 34: Latin America Vendor Risk Management Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 35: Latin America Vendor Risk Management Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 36: Latin America Vendor Risk Management Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 37: Latin America Vendor Risk Management Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 38: Latin America Vendor Risk Management Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 39: Latin America Vendor Risk Management Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 40: Latin America Vendor Risk Management Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Vendor Risk Management Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Vendor Risk Management Industry Revenue (Million), by Type 2025 & 2033

- Figure 43: Middle East and Africa Vendor Risk Management Industry Revenue Share (%), by Type 2025 & 2033

- Figure 44: Middle East and Africa Vendor Risk Management Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 45: Middle East and Africa Vendor Risk Management Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 46: Middle East and Africa Vendor Risk Management Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 47: Middle East and Africa Vendor Risk Management Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 48: Middle East and Africa Vendor Risk Management Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 49: Middle East and Africa Vendor Risk Management Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 50: Middle East and Africa Vendor Risk Management Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East and Africa Vendor Risk Management Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vendor Risk Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Vendor Risk Management Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 3: Global Vendor Risk Management Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 4: Global Vendor Risk Management Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 5: Global Vendor Risk Management Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Vendor Risk Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 7: Global Vendor Risk Management Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 8: Global Vendor Risk Management Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 9: Global Vendor Risk Management Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 10: Global Vendor Risk Management Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Vendor Risk Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 12: Global Vendor Risk Management Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 13: Global Vendor Risk Management Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 14: Global Vendor Risk Management Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 15: Global Vendor Risk Management Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Vendor Risk Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Global Vendor Risk Management Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 18: Global Vendor Risk Management Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 19: Global Vendor Risk Management Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 20: Global Vendor Risk Management Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Vendor Risk Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 22: Global Vendor Risk Management Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 23: Global Vendor Risk Management Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 24: Global Vendor Risk Management Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 25: Global Vendor Risk Management Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Vendor Risk Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 27: Global Vendor Risk Management Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 28: Global Vendor Risk Management Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 29: Global Vendor Risk Management Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 30: Global Vendor Risk Management Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vendor Risk Management Industry?

The projected CAGR is approximately > 12.50%.

2. Which companies are prominent players in the Vendor Risk Management Industry?

Key companies in the market include Quantivate, IBM Corporation, LockPath, Rapid Ratings International Inc, SAI Global, MetricStream, Resolver Inc, Optiv Security Inc *List Not Exhaustive, RSA Security LLC, Genpact Limited.

3. What are the main segments of the Vendor Risk Management Industry?

The market segments include Type, Deployment Type, Organization Size, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.98 Million as of 2022.

5. What are some drivers contributing to market growth?

Need for the Efficient Management of Complex Vendor Ecosystems; View the Risk Levels Associated With Various Tasks.

6. What are the notable trends driving market growth?

BFSI is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Dependence on Non-Formal and Manual Processes By Many Organizations.

8. Can you provide examples of recent developments in the market?

September 2023 - Certa, a third-party management platform, has raised USD 35 million to invest in artificial intelligence that takes text-based policies around everything from ESG and legal to compliance and procurement and converts them into controlled workflows that integrate with third-party tools. Using artificial intelligence will allow customers to reduce the size of their vendor management team and onboard third-party providers more quickly.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vendor Risk Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vendor Risk Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vendor Risk Management Industry?

To stay informed about further developments, trends, and reports in the Vendor Risk Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence