Key Insights

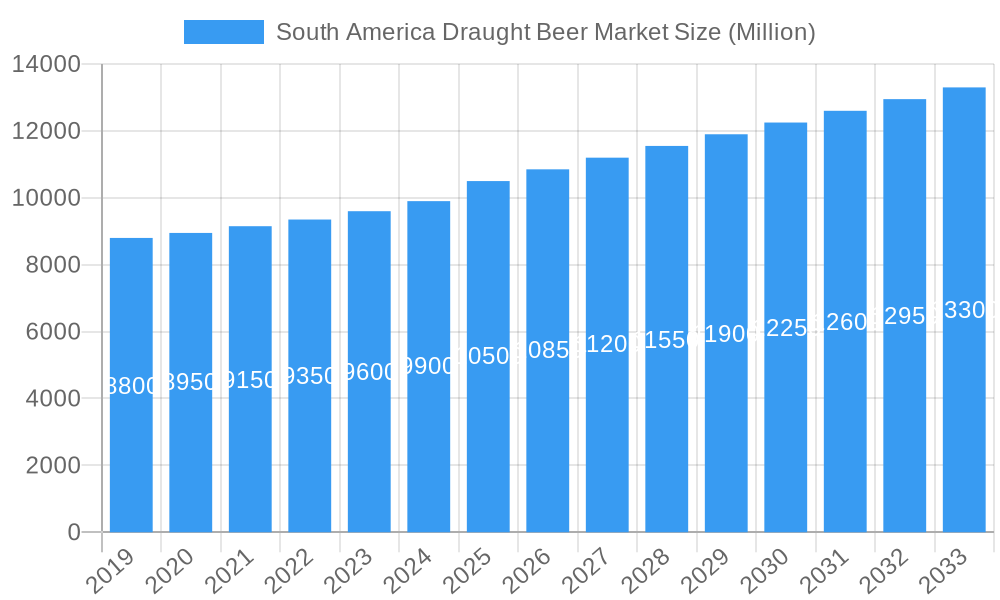

The South America draught beer market is projected for robust expansion, forecasted to reach $46.51 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 5.6% through 2033. This growth is propelled by evolving consumer demand for premium, fresh draught beer over packaged alternatives. Key drivers include rising disposable incomes in South America, increasing out-of-home consumption in urban centers, and the growing popularity of craft breweries and specialized beer pubs offering diverse artisanal selections. Enhanced distribution networks across off-trade (supermarkets, convenience stores), online retail, and on-trade (bars, restaurants) channels further boost accessibility and cater to varied consumer preferences.

South America Draught Beer Market Market Size (In Billion)

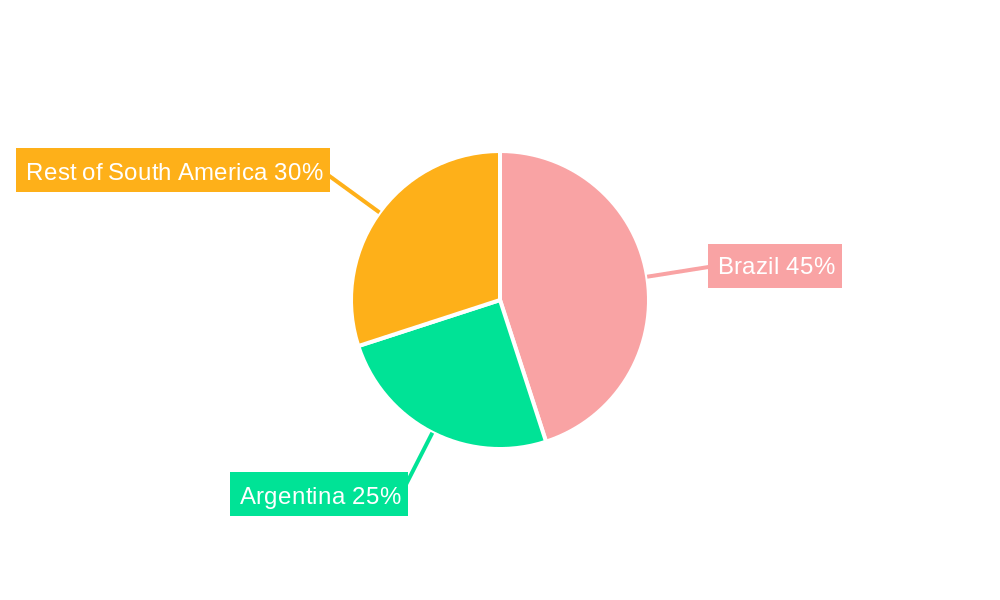

Brazil leads the South American draught beer market due to its substantial population and established beer culture. Argentina also represents a significant market with discerning consumers valuing quality and variety. Emerging economies within the region show promising growth driven by urbanization and a growing middle class adopting Western lifestyles. Potential restraints include fluctuating raw material costs (malt, hops) and stringent government regulations on alcohol sales and taxation. However, the overarching trend towards premiumization and experiential consumption supports a positive outlook, with key players like Anheuser-Busch InBev, Heineken N.V., Bavaria Brewery, and Brahma actively influencing market dynamics.

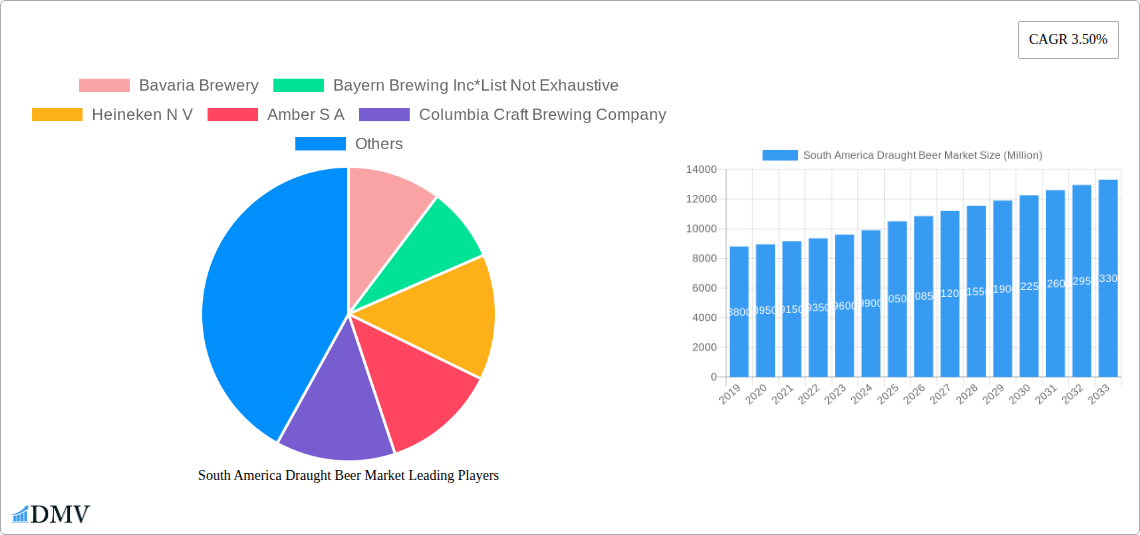

South America Draught Beer Market Company Market Share

This comprehensive report offers in-depth insights into the South America draught beer market from 2019 to 2033, with 2025 as the base year. It analyzes historical trends, current market composition, and provides a robust future forecast. Understand critical market drivers, emerging opportunities, and the competitive landscape shaped by leading players such as Bavaria Brewery, Heineken N.V., and Anheuser-Busch InBev. This analysis is crucial for breweries, distributors, investors, and industry stakeholders aiming to capitalize on the growing South American beverage sector.

South America Draught Beer Market Market Composition & Trends

The South America draught beer market is characterized by a moderate to high concentration, with major multinational corporations holding significant market share. However, the growing craft beer movement is fostering increased innovation and fragmenting the market in specific niches. Key innovation catalysts include advancements in brewing technology, the introduction of novel hop varieties, and a growing consumer preference for unique and premium draught beer experiences. Regulatory landscapes vary across the region, with some countries implementing stricter advertising laws while others encourage local production and tourism. Substitute products, such as bottled and canned beer, continue to be prevalent, but the superior quality and social experience of draught beer are driving its growth. End-user profiles are diverse, ranging from young adult consumers seeking social experiences to discerning aficionados appreciating complex flavor profiles. Merger and acquisition activities are strategic, aimed at expanding geographical reach and product portfolios. For instance, Compania Cervecerias Unidas (CCU) has demonstrated a commitment to growth, evidenced by its USD 23 million investment in production capacity expansion in Argentina. M&A deal values in the region are expected to increase as larger players seek to consolidate their positions and smaller craft breweries become acquisition targets.

- Market Share Distribution: Dominated by major international players with a growing presence of regional and craft breweries.

- Innovation Catalysts: Craft beer boom, new hop varieties, improved dispensing technology.

- Regulatory Landscape: Varied across countries, impacting advertising and distribution.

- Substitute Products: Bottled beer, canned beer, ready-to-drink beverages.

- End-User Profiles: Young adults, social drinkers, craft beer enthusiasts.

- M&A Activities: Strategic acquisitions to enhance market presence and product offerings.

South America Draught Beer Market Industry Evolution

The South America draught beer market has witnessed a significant evolutionary trajectory, driven by a confluence of shifting consumer preferences, technological advancements, and strategic investments. Historically, the market was largely dominated by mainstream lagers produced by a few large breweries. However, the last decade has seen a paradigm shift, marked by the rise of craft brewing and a discerning consumer base eager to explore diverse beer styles and premium offerings. This evolution is clearly reflected in the market growth trajectories, which have shown a steady upward trend, with an estimated Compound Annual Growth Rate (CAGR) of approximately 4.5% from 2019 to 2025. Technological advancements have played a crucial role, particularly in brewing and dispensing systems. Innovations in kegging technology, such as smaller, more portable kegs and improved sanitation methods, have made draught beer more accessible to a wider range of establishments, including smaller bars and restaurants. Furthermore, advancements in yeast strains and fermentation techniques have enabled brewers to create more complex and nuanced flavor profiles, appealing to a more sophisticated palate. Shifting consumer demands are perhaps the most potent force shaping the industry. There's a discernible move away from mass-produced, generic beers towards artisanal and locally sourced options. Consumers are increasingly valuing authenticity, craftsmanship, and the story behind their beer. This has led to a surge in demand for specialty draught beers like IPAs, sours, and stouts, challenging the long-standing dominance of pale lagers. The increasing adoption of online platforms for information gathering and even direct-to-consumer sales (where regulations permit) has also empowered consumers, allowing them to discover and engage with new brands and styles more readily. The on-trade channel, particularly bars, pubs, and restaurants, remains the primary distribution point for draught beer, but the off-trade channel, especially specialized liquor stores and, to a lesser extent, online retailers offering draught beer systems for home use, is also experiencing growth. The "experience economy" further fuels this evolution, with consumers seeking unique social settings and high-quality beverages to accompany them. The forecast period (2025–2033) is expected to see continued growth, with an estimated CAGR of around 5.2%, driven by ongoing premiumization and the expanding reach of craft breweries. The market's ability to adapt to evolving consumer tastes, embrace innovation, and navigate regulatory complexities will be paramount to its sustained success.

Leading Regions, Countries, or Segments in South America Draught Beer Market

The South America draught beer market exhibits distinct regional dominance and segment leadership, with Brazil emerging as the largest and most influential market, followed closely by Argentina. Within Brazil, the lager segment continues to hold the lion's share of the draught beer market, owing to its widespread appeal and long-standing cultural presence. However, the ale segment is experiencing rapid growth, driven by the increasing popularity of craft breweries and a consumer base eager for more diverse flavor profiles.

Geographical Dominance:

- Brazil: Accounts for approximately 45% of the South American draught beer market. Its large population, developed tourism sector, and established brewing industry contribute to its leading position. Investment trends in Brazil are focused on expanding production capacities and modernizing distribution networks to cater to both traditional and emerging consumption channels.

- Argentina: Holds a significant share, estimated at around 25%. Argentina has a robust craft beer scene, with a strong emphasis on quality and innovation, particularly in the ale segment. Regulatory support for local breweries and the growing popularity of beer festivals are key drivers. Compania Cervecerias Unidas (CCU)'s investment of USD 23 million in expanding its beer production capacity in Argentina underscores the strategic importance of this market.

- Rest of South America: Encompasses countries like Colombia, Chile, Peru, and Ecuador, collectively representing the remaining 30%. While individual market sizes may be smaller, these regions are showing promising growth rates, driven by increasing disposable incomes, a rising middle class, and a growing appreciation for premium beverage options.

Product Type Dominance:

- Lager: Remains the most consumed type of draught beer across the region, accounting for an estimated 70% of the market. Its crisp, refreshing profile is favored by a broad consumer base.

- Ale: Experiencing substantial growth, with an estimated market share of 25%. This segment is fueled by the craft beer revolution, with consumers actively seeking out diverse styles like IPAs, pale ales, and stouts.

- Other Beer Types: Includes wheat beers, porters, and other specialty brews, holding a smaller but growing segment of 5%.

Distribution Channel Dominance:

- On-Trade Channel: This remains the dominant channel, comprising approximately 75% of draught beer sales. Bars, restaurants, pubs, and hotels are the primary venues for draught beer consumption, leveraging the social and experiential aspects of this format.

- Off-Trade Channel: While smaller, this channel is growing rapidly, especially the Online Retail Channel. This growth is facilitated by advancements in home draught beer systems and a consumer desire for convenience. The Offline Retail Channel, including specialized liquor stores, also contributes to off-trade sales.

The dominance of Brazil and Argentina, coupled with the strong performance of the lager segment and the on-trade channel, provides a clear picture of the current market landscape. However, the significant growth in the ale segment and the burgeoning off-trade channel signal future shifts and emerging opportunities within the South American draught beer market.

South America Draught Beer Market Product Innovations

Product innovation in the South America draught beer market is a vibrant and evolving landscape, catering to increasingly sophisticated consumer palates. A notable trend is the introduction of limited edition releases and collaborations, exemplified by Novo Brazil Brewing Company's launch of its TRES beer collection, featuring high ABV (around 9.5%) and generous hop content (approximately 1.7 oz of hops per gallon). This highlights a move towards more complex and intensely flavored brews. Furthermore, brewers are experimenting with unique flavor infusions and seasonal offerings. River North Brewery's launch of its Socorro Chile Lager, a light lager with a spicy flavor profile (5% ABV), on Chile Beer Day showcases this innovation, alongside variations like pineapple jalapeno imperial Saison and Mayan chocolate imperial stout. These innovations not only expand product diversity but also create buzz and drive consumer engagement, pushing the boundaries of traditional beer offerings and enhancing the overall draught beer experience.

Propelling Factors for South America Draught Beer Market Growth

The South America draught beer market is propelled by several key factors:

- Growing Middle Class and Disposable Income: Increased purchasing power allows consumers to opt for premium and craft draught beers.

- Rising Popularity of Craft Beer Culture: A burgeoning interest in artisanal brewing, unique flavors, and authentic experiences is driving demand for diverse draught offerings.

- Expansion of the On-Trade Sector: Growth in bars, pubs, and restaurants provides more outlets for draught beer consumption, fostering social drinking occasions.

- Technological Advancements in Brewing and Dispensing: Innovations in production efficiency and draught systems enhance accessibility and quality.

- Tourism and Hospitality Sector Growth: These sectors are significant drivers for draught beer consumption, catering to both local and international tastes.

Obstacles in the South America Draught Beer Market Market

Despite robust growth, the South America draught beer market faces several obstacles:

- Regulatory Hurdles and Taxation: Diverse and sometimes stringent regulations regarding alcohol production, distribution, and advertising can impact market entry and operational costs. High excise taxes in some countries can also deter consumption.

- Supply Chain Disruptions: Volatility in raw material prices (e.g., hops, malt) and logistical challenges within the vast continent can affect production costs and availability.

- Intense Competition: The market is characterized by competition from established global players, local breweries, and an increasing number of craft beer producers, leading to price pressures and market saturation in certain segments.

- Economic Instability: Fluctuations in national economies across South America can impact consumer spending on discretionary items like premium draught beer.

Future Opportunities in South America Draught Beer Market

The South America draught beer market is ripe with future opportunities:

- Untapped Rural and Emerging Urban Markets: Significant potential exists in expanding reach into less saturated regions and smaller cities.

- Growth in Home Draught Systems: The increasing adoption of home draught beer systems presents a lucrative new channel for sales and brand engagement.

- Focus on Sustainable Brewing Practices: Growing consumer awareness of environmental issues creates opportunities for brands that adopt eco-friendly production and packaging.

- Innovation in Low and No-Alcohol Draught Options: Catering to health-conscious consumers with innovative low or no-alcohol draught beers can tap into a new market segment.

- Cross-Regional Collaborations and Exports: Opportunities for cross-border partnerships and exporting unique South American draught beers to global markets.

Major Players in the South America Draught Beer Market Ecosystem

- Bavaria Brewery

- Bayern Brewing Inc

- Heineken N V

- Amber S A

- Columbia Craft Brewing Company

- Brahma

- Carlsberg Group

- Anheuser-Bushch InBev

- Novo Brazil Brewing Company

- Muller Inc

Key Developments in South America Draught Beer Market Industry

- May 2022: Compania Cervecerias Unidas (CCU) invested approximately USD 23 million to expand its beer production capacity in Argentina, aiming to strengthen its regional footprint through increased production and logistics.

- November 2021: Novo Brazil Brewing Company launched its two limited editions of the TRES beer collection, featuring high ABV (around 9.5%) and significant hop content (approximately 1.7 oz of hops per gallon), including triple-hazy and hoppy flavors.

- September 2021: River North Brewery launched its new Socorro Chile Lager (5% ABV) on Chile Beer Day, a light and spicy lager. This launch also included variations like pineapple jalapeno imperial Saison and Mayan chocolate imperial stout.

Strategic South America Draught Beer Market Market Forecast

The strategic forecast for the South America draught beer market anticipates continued robust growth, driven by an evolving consumer base prioritizing premium experiences and diverse flavor profiles. The increasing accessibility of craft beers through both on-trade and emerging off-trade channels, coupled with ongoing investments in production capacity by key players like CCU, will significantly propel market expansion. Future opportunities lie in capitalizing on the burgeoning interest in low and no-alcohol options, the adoption of sustainable brewing practices, and expanding into untapped regional markets. The forecast period of 2025–2033 is expected to see the market thrive, with an estimated CAGR of 5.2%, as innovation and consumer demand converge to shape a dynamic and expanding draught beer landscape across South America.

South America Draught Beer Market Segmentation

-

1. Product Type

- 1.1. Lager

- 1.2. Ale

- 1.3. Other Beer types

-

2. distribution channel

-

2.1. Off trade Channel

- 2.1.1. Online Retail Channel

- 2.1.2. Offline Retail Channel

- 2.2. On Trade Channel

-

2.1. Off trade Channel

-

3. Geography

-

3.1. South America

- 3.1.1. Brazil

- 3.1.2. Argentina

- 3.1.3. Rest of South America

-

3.1. South America

South America Draught Beer Market Segmentation By Geography

-

1. South America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Rest of South America

South America Draught Beer Market Regional Market Share

Geographic Coverage of South America Draught Beer Market

South America Draught Beer Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Lager

- 5.1.2. Ale

- 5.1.3. Other Beer types

- 5.2. Market Analysis, Insights and Forecast - by distribution channel

- 5.2.1. Off trade Channel

- 5.2.1.1. Online Retail Channel

- 5.2.1.2. Offline Retail Channel

- 5.2.2. On Trade Channel

- 5.2.1. Off trade Channel

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. South America

- 5.3.1.1. Brazil

- 5.3.1.2. Argentina

- 5.3.1.3. Rest of South America

- 5.3.1. South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. South America Draught Beer Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Lager

- 6.1.2. Ale

- 6.1.3. Other Beer types

- 6.2. Market Analysis, Insights and Forecast - by distribution channel

- 6.2.1. Off trade Channel

- 6.2.1.1. Online Retail Channel

- 6.2.1.2. Offline Retail Channel

- 6.2.2. On Trade Channel

- 6.2.1. Off trade Channel

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. South America

- 6.3.1.1. Brazil

- 6.3.1.2. Argentina

- 6.3.1.3. Rest of South America

- 6.3.1. South America

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bavaria Brewery

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bayern Brewing Inc*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Heineken N V

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Amber S A

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Columbia Craft Brewing Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Brahma

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Carlsberg Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Anheuser-Bushch InBev

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Novo Brazil Brewing Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Muller Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Bavaria Brewery

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South America Draught Beer Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America Draught Beer Market Share (%) by Company 2025

List of Tables

- Table 1: South America Draught Beer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: South America Draught Beer Market Volume liter Forecast, by Product Type 2020 & 2033

- Table 3: South America Draught Beer Market Revenue billion Forecast, by distribution channel 2020 & 2033

- Table 4: South America Draught Beer Market Volume liter Forecast, by distribution channel 2020 & 2033

- Table 5: South America Draught Beer Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: South America Draught Beer Market Volume liter Forecast, by Geography 2020 & 2033

- Table 7: South America Draught Beer Market Revenue billion Forecast, by Region 2020 & 2033

- Table 8: South America Draught Beer Market Volume liter Forecast, by Region 2020 & 2033

- Table 9: South America Draught Beer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 10: South America Draught Beer Market Volume liter Forecast, by Product Type 2020 & 2033

- Table 11: South America Draught Beer Market Revenue billion Forecast, by distribution channel 2020 & 2033

- Table 12: South America Draught Beer Market Volume liter Forecast, by distribution channel 2020 & 2033

- Table 13: South America Draught Beer Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 14: South America Draught Beer Market Volume liter Forecast, by Geography 2020 & 2033

- Table 15: South America Draught Beer Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: South America Draught Beer Market Volume liter Forecast, by Country 2020 & 2033

- Table 17: Brazil South America Draught Beer Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Brazil South America Draught Beer Market Volume (liter ) Forecast, by Application 2020 & 2033

- Table 19: Argentina South America Draught Beer Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina South America Draught Beer Market Volume (liter ) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America South America Draught Beer Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of South America South America Draught Beer Market Volume (liter ) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Draught Beer Market?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the South America Draught Beer Market?

Key companies in the market include Bavaria Brewery, Bayern Brewing Inc*List Not Exhaustive, Heineken N V, Amber S A, Columbia Craft Brewing Company, Brahma, Carlsberg Group, Anheuser-Bushch InBev, Novo Brazil Brewing Company, Muller Inc.

3. What are the main segments of the South America Draught Beer Market?

The market segments include Product Type, distribution channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 46.51 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend.

6. What are the notable trends driving market growth?

Growing microbreweries leading to increased consumption..

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Product Guidelines.

8. Can you provide examples of recent developments in the market?

In May 2022, Compania Cervecerias Unidas (CCU) invested about USD 23 million to expand its beer production capacity in Argentina. The company aims to strengthen its footprints across the region with increasing production and logistic capacity to reach maximum consumers in the market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Draught Beer Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Draught Beer Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Draught Beer Market?

To stay informed about further developments, trends, and reports in the South America Draught Beer Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence