Key Insights

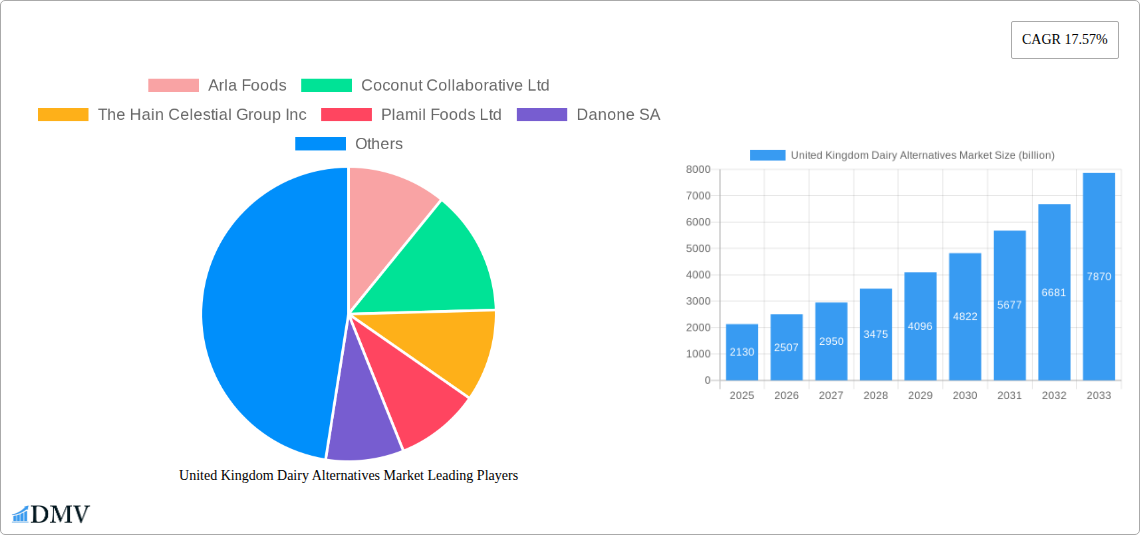

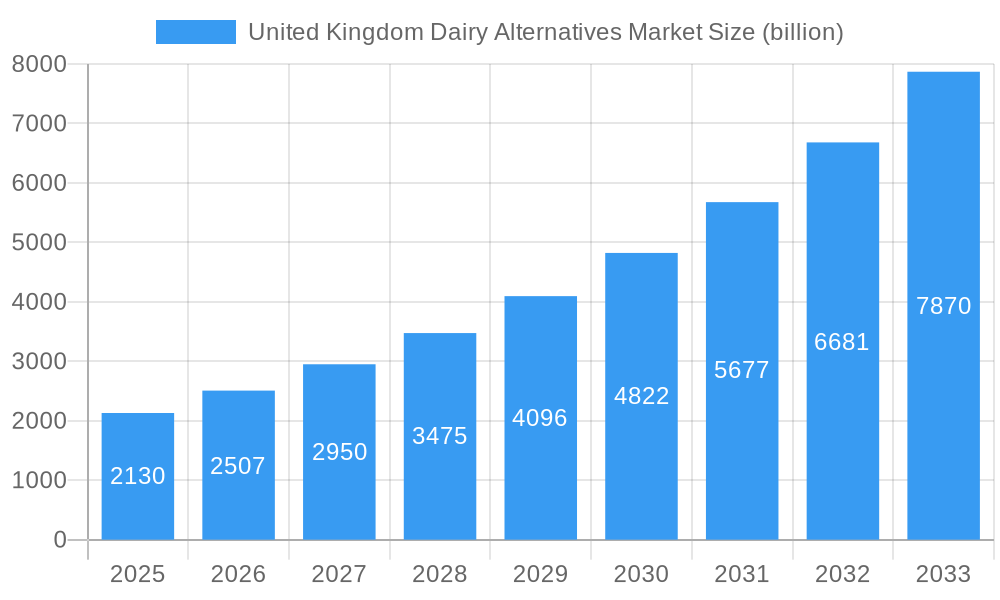

The United Kingdom's dairy alternatives market is experiencing remarkable expansion, projected to reach an estimated £2.13 billion in 2025. This robust growth is fueled by a significant CAGR of 17.57%, indicating a sustained upward trajectory for the foreseeable future. Consumer demand for plant-based options is soaring, driven by a confluence of factors including increasing health consciousness, a growing awareness of environmental sustainability, and a rising prevalence of lactose intolerance and dairy allergies. These trends are compelling a shift away from traditional dairy products, opening up substantial opportunities for dairy alternative manufacturers. Key growth drivers include innovative product development across various categories, such as non-dairy butter, cheese, ice cream, milk (with almond, oat, and soy milk leading the pack), and yogurt. The convenience of off-trade channels, particularly online retail and supermarkets, is further propelling market penetration, making these alternatives more accessible to a wider consumer base.

United Kingdom Dairy Alternatives Market Market Size (In Billion)

The market's dynamism is further underscored by its diverse segmentation and the active participation of key companies like Danone SA, Upfield Holdings BV, and Oatly Group AB. While the market is experiencing rapid growth, certain restraints, such as the higher price point of some dairy alternatives compared to conventional dairy products and consumer perception challenges, remain. However, ongoing technological advancements in product formulation, improved taste profiles, and expanding distribution networks are steadily mitigating these challenges. The United Kingdom, as a focal region for this analysis, demonstrates a strong appetite for these innovative food solutions, positioning it as a crucial market for future investment and development within the global dairy alternatives landscape. The period from 2019 to 2033, with a base year of 2025, highlights a period of sustained and accelerated growth, reflecting a fundamental consumer-led transformation in the UK's food industry.

United Kingdom Dairy Alternatives Market Company Market Share

United Kingdom Dairy Alternatives Market: Comprehensive Growth Analysis and Future Outlook (2019-2033)

This in-depth report provides an exhaustive analysis of the United Kingdom dairy alternatives market, offering critical insights for stakeholders, investors, and industry professionals. Spanning a comprehensive study period from 2019 to 2033, with a detailed focus on the base and estimated year of 2025, and a robust forecast period of 2025–2033, this report delves into market dynamics, emerging trends, and strategic opportunities. With an estimated market size poised for significant expansion, the UK dairy alternatives sector is driven by evolving consumer preferences for healthier, sustainable, and ethically sourced food options. This report offers a data-driven roadmap to navigate this rapidly growing landscape, covering product innovations, distribution channels, key players, and future market potential, valued in billions.

United Kingdom Dairy Alternatives Market Market Composition & Trends

The United Kingdom dairy alternatives market is characterized by a dynamic composition and an accelerated pace of innovation, driven by a confluence of factors including increasing health consciousness, environmental concerns, and ethical considerations. Market concentration is moderately fragmented, with several key players vying for dominance, while a constant influx of new entrants fuels intense competition and encourages product diversification. Innovation catalysts are predominantly rooted in R&D for improved taste profiles, nutritional enhancement, and novel plant-based ingredients. The regulatory landscape, while generally supportive of food innovation, mandates clear labeling and adherence to safety standards. Substitute products are continuously emerging, expanding the range of plant-based options beyond traditional soy and almond milks. End-user profiles are diverse, encompassing health-conscious individuals, vegans, vegetarians, lactose-intolerant consumers, and environmentally aware shoppers. Mergers and acquisitions (M&A) activities are on the rise, signaling industry consolidation and strategic expansion, with recent M&A deal values estimated to be in the range of hundreds of millions of pounds.

- Market Share Distribution: While specific current figures fluctuate, key segments like non-dairy milk and yogurt hold substantial market share.

- Innovation Focus: Emphasis on oat milk, almond milk, and emerging alternatives like cashew and hemp milk.

- Key Drivers: Growing vegan and flexitarian populations, demand for lactose-free options, and sustainability messaging.

- M&A Trends: Acquisition of smaller, innovative brands by larger food conglomerates to expand their plant-based portfolios.

United Kingdom Dairy Alternatives Market Industry Evolution

The United Kingdom dairy alternatives market has witnessed a dramatic and transformative evolution over the past few years, fundamentally reshaping the nation's food consumption patterns and offering a compelling alternative to traditional dairy products. This evolution is marked by a consistent and robust growth trajectory, propelled by a complex interplay of escalating consumer demand, groundbreaking technological advancements, and a significant shift in societal attitudes towards health, environment, and animal welfare. Historically, the market was a niche segment catering primarily to individuals with specific dietary restrictions, such as lactose intolerance. However, recent years have seen an unprecedented surge in adoption, transforming dairy alternatives from a specialized category into a mainstream dietary choice.

This remarkable growth can be attributed to several pivotal factors. Firstly, the increasing consumer awareness regarding the perceived health benefits of plant-based diets has been a primary driver. Studies and widespread media coverage highlighting potential advantages such as lower saturated fat content, cholesterol reduction, and improved digestive health have encouraged a broader demographic to explore dairy alternatives. This health-driven adoption is further amplified by the growing popularity of flexitarianism, where individuals consciously reduce their consumption of animal products without necessarily adopting a strictly vegan lifestyle.

Technological advancements have played an instrumental role in enhancing the appeal and accessibility of dairy alternatives. Significant research and development efforts have focused on improving the taste, texture, and nutritional profile of plant-based products to closely mimic or even surpass their dairy counterparts. Innovations in ingredient processing, such as advanced extraction techniques for plant milks and novel fermentation processes for non-dairy yogurts and cheeses, have led to products that are more palatable and versatile in culinary applications. For instance, the development of barista-edition oat milks, which steam and foam effectively, has been a game-changer for the coffee industry and a major contributor to the mainstream acceptance of oat-based beverages.

Furthermore, the environmental footprint associated with dairy farming, including greenhouse gas emissions and land/water usage, has become a growing concern for many consumers. Plant-based alternatives generally boast a significantly lower environmental impact, aligning with the values of an increasingly eco-conscious population. This ethical dimension, coupled with a heightened awareness of animal welfare issues in industrial farming, has led a substantial segment of consumers to actively seek out dairy-free options.

The distribution channels have also evolved to cater to this expanding market. Dairy alternatives are now readily available across a wide spectrum of retail outlets, from large supermarkets and hypermarkets to online retailers and convenience stores, ensuring widespread accessibility. This accessibility, combined with aggressive marketing campaigns and the increasing presence of dairy alternatives on restaurant menus and in food service establishments, has further normalized their consumption. The market has transitioned from a perception of being a "specialty" product to a common grocery item, reflecting the deep-seated changes in consumer preferences and lifestyles. This evolution is not merely a trend but a fundamental restructuring of the UK's food landscape, with significant implications for the dairy industry and a vast array of associated businesses. The sustained growth rates, with an estimated compound annual growth rate (CAGR) of over 8% for key segments, underscore the enduring strength and transformative power of this market evolution.

Leading Regions, Countries, or Segments in United Kingdom Dairy Alternatives Market

The United Kingdom dairy alternatives market is a multifaceted landscape, with distinct regional dynamics and segment dominance. Among the various categories, Non-Dairy Milk consistently emerges as the leading segment, driven by its versatility, widespread availability, and broad consumer appeal. Within this segment, Oat Milk has experienced an unprecedented surge in popularity, often surpassing traditional alternatives like almond milk in market share and consumer preference. This dominance is fueled by its creamy texture, neutral flavor profile, and its suitability for various applications, including coffee, cereal, and baking. The Almond Milk and Soy Milk segments also maintain significant market presence, catering to established consumer bases and specific taste preferences. Emerging varieties like Cashew Milk, Coconut Milk, Hazelnut Milk, and Hemp Milk are steadily gaining traction, catering to niche preferences and expanding the overall diversity of the non-dairy milk category.

The Distribution Channel landscape is equally dynamic. The Off-Trade channel, encompassing all retail sales outside of food service establishments, is the primary driver of market growth. Within off-trade, Supermarkets and Hypermarkets command the largest share due to their extensive product offerings and wide reach. However, Online Retail is exhibiting the fastest growth rate, driven by convenience, wider selection, and personalized shopping experiences. Specialist retailers and convenience stores also play a crucial role in catering to specific consumer needs and impulse purchases. The On-Trade channel, including cafes, restaurants, and hotels, is also becoming increasingly important as establishments integrate dairy alternatives into their menus and beverage offerings to cater to a broader customer base.

Geographically, while the entire United Kingdom is experiencing growth, England, particularly urban centers like London, Manchester, and Birmingham, often leads in terms of market penetration and consumer adoption due to higher population density, greater disposable income, and a more diverse culinary scene embracing plant-based options. Scotland, Wales, and Northern Ireland are also witnessing substantial growth, mirroring the national trends driven by increasing consumer awareness and product availability.

Key drivers for the dominance of these segments and regions include:

- Investment Trends: Significant investment from both established food corporations and venture capital firms into dairy alternative brands, particularly in oat milk and innovative product development.

- Regulatory Support: Favorable regulations promoting plant-based food innovation and clear labeling standards, encouraging consumer trust and product development.

- Consumer Adoption Rates: High adoption rates among health-conscious individuals, vegans, vegetarians, and those seeking sustainable food choices, particularly in densely populated urban areas.

- Product Innovation: Continuous development of new flavors, textures, and fortified options within the non-dairy milk category, enhancing appeal and addressing diverse consumer needs.

- Retail Expansion: Increased shelf space and promotional activities for dairy alternatives in major supermarket chains, making them readily accessible to a broad consumer base.

- Food Service Integration: Growing inclusion of non-dairy milk options in coffee shops and restaurants, normalizing their consumption and driving trial among new consumers.

The synergy between innovative product development, widespread distribution, and evolving consumer preferences solidifies the leading positions of non-dairy milk and the off-trade retail channel within the burgeoning UK dairy alternatives market.

United Kingdom Dairy Alternatives Market Product Innovations

Product innovation in the United Kingdom dairy alternatives market is a relentless pursuit of mimicking and enhancing the sensory and nutritional aspects of traditional dairy. Key advancements include the development of ultra-creamy oat milks specifically formulated for perfect frothing in barista coffee, significantly improving cafe offerings. Innovations in non-dairy cheese now offer superior meltability and flavor profiles, broadening their application in cooking and snacking. Furthermore, the market is seeing the introduction of allergen-friendly alternatives, such as nut-free oat and soy milks, alongside fortified options with added calcium, Vitamin D, and B12, addressing specific nutritional gaps. Performance metrics are increasingly focused on taste parity with dairy, improved texture, and comparable nutritional value, with brands actively highlighting their unique selling propositions and sustainable sourcing.

Propelling Factors for United Kingdom Dairy Alternatives Market Growth

Several interconnected factors are propelling the growth of the United Kingdom dairy alternatives market. The burgeoning health and wellness trend is a primary driver, with consumers increasingly seeking plant-based options perceived as healthier. Environmental consciousness is another significant factor, as consumers opt for products with a lower carbon footprint. Technological advancements in product formulation are leading to improved taste and texture, making alternatives more appealing. Furthermore, growing awareness of ethical and animal welfare concerns associated with dairy farming is encouraging a shift towards plant-based diets. Government initiatives promoting sustainable food systems and favorable regulatory environments for food innovation also contribute to this upward trajectory.

Obstacles in the United Kingdom Dairy Alternatives Market Market

Despite its robust growth, the United Kingdom dairy alternatives market faces several obstacles. Price sensitivity remains a significant barrier, as many dairy alternatives are priced higher than conventional dairy products, limiting accessibility for some consumers. Taste and texture perceptions can still be a deterrent for a portion of the population, although significant improvements have been made. Supply chain disruptions, particularly concerning ingredient sourcing and volatility in commodity prices, can impact production costs and availability. Regulatory challenges related to labeling and marketing claims can create confusion and require careful navigation. Intense competitive pressure among an increasing number of brands necessitates continuous innovation and marketing investment.

Future Opportunities in United Kingdom Dairy Alternatives Market

The United Kingdom dairy alternatives market is ripe with future opportunities. The expansion into new product categories, such as dairy-free cheeses with improved meltability and a wider range of plant-based yogurts with novel flavors and textures, presents significant potential. The food service sector offers a vast untapped market, with increasing demand for dairy-free options in restaurants, cafes, and hospitality settings. Further development of innovative ingredients and processing technologies can lead to even more sustainable and cost-effective alternatives. Emerging consumer trends like personalized nutrition and functional foods also present avenues for specialized dairy-free product development. Expanding into export markets from the UK base also offers considerable growth prospects.

Major Players in the United Kingdom Dairy Alternatives Market Ecosystem

- Arla Foods

- Coconut Collaborative Ltd

- The Hain Celestial Group Inc

- Plamil Foods Ltd

- Danone SA

- Upfield Holdings BV

- Blue Diamond Growers

- Oatly Group AB

- Britvic PLC

- VBites Foods Lt

Key Developments in United Kingdom Dairy Alternatives Market Industry

- November 2022: Oatly Group AB announced that it would release a new range of oat-based yogurt. The new range comes in four flavors: strawberry, blueberry, plain, and Greek style, expanding consumer choice and reinforcing Oatly's position in the yogurt segment.

- October 2022: Plenish launched a new line of plant-based products. The three-strong range of unsweetened plenish-enriched milk almond, oat, and soy is fortified with nutrients, including iodine, omega-3, and vitamin D, addressing consumer demand for fortified and healthier alternatives.

- September 2022: Swedish coffee chain Espresso House, which operates 35 stores in Germany, extended an existing partnership with Oatly to serve Oatly Barista Edition across its coffee shops in the Nordics and Germany, highlighting the growing integration of dairy alternatives within the professional beverage sector and expanding reach.

Strategic United Kingdom Dairy Alternatives Market Market Forecast

The strategic United Kingdom dairy alternatives market forecast indicates sustained and significant growth, driven by deeply embedded consumer shifts towards healthier, ethical, and environmentally conscious food choices. The forecast period of 2025–2033 is projected to see continued expansion, fueled by ongoing innovation in product taste, texture, and nutritional fortification. The increasing acceptance of plant-based options across all demographics, coupled with expanding distribution channels, particularly online retail and food service integration, will be critical growth catalysts. Investments in sustainable sourcing and production technologies will further enhance market appeal. Emerging opportunities in functional dairy alternatives and a wider array of plant-based cheese and ice cream products are expected to tap into new consumer segments. The market's ability to adapt to evolving consumer demands and regulatory landscapes will be paramount to achieving its full growth potential, with a projected market valuation reaching tens of billions by the end of the forecast period.

United Kingdom Dairy Alternatives Market Segmentation

-

1. Category

- 1.1. Non-Dairy Butter

- 1.2. Non-Dairy Cheese

- 1.3. Non-Dairy Ice Cream

-

1.4. Non-Dairy Milk

-

1.4.1. By Product Type

- 1.4.1.1. Almond Milk

- 1.4.1.2. Cashew Milk

- 1.4.1.3. Coconut Milk

- 1.4.1.4. Hazelnut Milk

- 1.4.1.5. Hemp Milk

- 1.4.1.6. Oat Milk

- 1.4.1.7. Soy Milk

-

1.4.1. By Product Type

- 1.5. Non-Dairy Yogurt

-

2. Distribution Channel

-

2.1. Off-Trade

- 2.1.1. Convenience Stores

- 2.1.2. Online Retail

- 2.1.3. Specialist Retailers

- 2.1.4. Supermarkets and Hypermarkets

- 2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 2.2. On-Trade

-

2.1. Off-Trade

United Kingdom Dairy Alternatives Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Dairy Alternatives Market Regional Market Share

Geographic Coverage of United Kingdom Dairy Alternatives Market

United Kingdom Dairy Alternatives Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.57% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Category

- 5.1.1. Non-Dairy Butter

- 5.1.2. Non-Dairy Cheese

- 5.1.3. Non-Dairy Ice Cream

- 5.1.4. Non-Dairy Milk

- 5.1.4.1. By Product Type

- 5.1.4.1.1. Almond Milk

- 5.1.4.1.2. Cashew Milk

- 5.1.4.1.3. Coconut Milk

- 5.1.4.1.4. Hazelnut Milk

- 5.1.4.1.5. Hemp Milk

- 5.1.4.1.6. Oat Milk

- 5.1.4.1.7. Soy Milk

- 5.1.4.1. By Product Type

- 5.1.5. Non-Dairy Yogurt

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Off-Trade

- 5.2.1.1. Convenience Stores

- 5.2.1.2. Online Retail

- 5.2.1.3. Specialist Retailers

- 5.2.1.4. Supermarkets and Hypermarkets

- 5.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 5.2.2. On-Trade

- 5.2.1. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Category

- 6. United Kingdom Dairy Alternatives Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Category

- 6.1.1. Non-Dairy Butter

- 6.1.2. Non-Dairy Cheese

- 6.1.3. Non-Dairy Ice Cream

- 6.1.4. Non-Dairy Milk

- 6.1.4.1. By Product Type

- 6.1.4.1.1. Almond Milk

- 6.1.4.1.2. Cashew Milk

- 6.1.4.1.3. Coconut Milk

- 6.1.4.1.4. Hazelnut Milk

- 6.1.4.1.5. Hemp Milk

- 6.1.4.1.6. Oat Milk

- 6.1.4.1.7. Soy Milk

- 6.1.4.1. By Product Type

- 6.1.5. Non-Dairy Yogurt

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Off-Trade

- 6.2.1.1. Convenience Stores

- 6.2.1.2. Online Retail

- 6.2.1.3. Specialist Retailers

- 6.2.1.4. Supermarkets and Hypermarkets

- 6.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 6.2.2. On-Trade

- 6.2.1. Off-Trade

- 6.1. Market Analysis, Insights and Forecast - by Category

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Arla Foods

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Coconut Collaborative Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 The Hain Celestial Group Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Plamil Foods Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Danone SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Upfield Holdings BV

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Blue Diamond Growers

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Oatly Group AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Britvic PLC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 VBites Foods Lt

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Arla Foods

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Dairy Alternatives Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United Kingdom Dairy Alternatives Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Dairy Alternatives Market Revenue billion Forecast, by Category 2020 & 2033

- Table 2: United Kingdom Dairy Alternatives Market Volume K Tons Forecast, by Category 2020 & 2033

- Table 3: United Kingdom Dairy Alternatives Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: United Kingdom Dairy Alternatives Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: United Kingdom Dairy Alternatives Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: United Kingdom Dairy Alternatives Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: United Kingdom Dairy Alternatives Market Revenue billion Forecast, by Category 2020 & 2033

- Table 8: United Kingdom Dairy Alternatives Market Volume K Tons Forecast, by Category 2020 & 2033

- Table 9: United Kingdom Dairy Alternatives Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: United Kingdom Dairy Alternatives Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 11: United Kingdom Dairy Alternatives Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Dairy Alternatives Market Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Dairy Alternatives Market?

The projected CAGR is approximately 17.57%.

2. Which companies are prominent players in the United Kingdom Dairy Alternatives Market?

Key companies in the market include Arla Foods, Coconut Collaborative Ltd, The Hain Celestial Group Inc, Plamil Foods Ltd, Danone SA, Upfield Holdings BV, Blue Diamond Growers, Oatly Group AB, Britvic PLC, VBites Foods Lt.

3. What are the main segments of the United Kingdom Dairy Alternatives Market?

The market segments include Category, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.13 billion as of 2022.

5. What are some drivers contributing to market growth?

Surge in Participation of Sports Activities; Functional and Processing Bnefits of Whey Protein.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

High Manufacturing Costs and Fluctuations in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

November 2022: Oatly Group AB announced that it would release a new range of oat-based yogurt. The new range comes in four flavors: strawberry, blueberry, plain, and Greek style.October 2022: Plenish launched a new line of plant-based products. The three-strong range of unsweetened plenish-enriched milk almond, oat, and soy is fortified with nutrients, including iodine, omega-3, and vitamin D.September 2022: Swedish coffee chain Espresso House, which operates 35 stores in Germany, extended an existing partnership with Oatly to serve Oatly Barista Edition across its coffee shops in the Nordics and Germany.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Dairy Alternatives Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Dairy Alternatives Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Dairy Alternatives Market?

To stay informed about further developments, trends, and reports in the United Kingdom Dairy Alternatives Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence